FACTOR-BASED TRADING

Since the first version of the classic text on security analysis by Benjamin Graham and David Dodd1—considered to be the Bible on the fundamental approach to security analysis—was published in 1934, equity portfolio management and trading strategies have developed considerably. Graham and Dodd were early contributors to factor-based strategies because they extended traditional valuation approaches by using information throughout the financial statements2 and by presenting concrete rules of thumb to be used to determine the attractiveness of securities.3

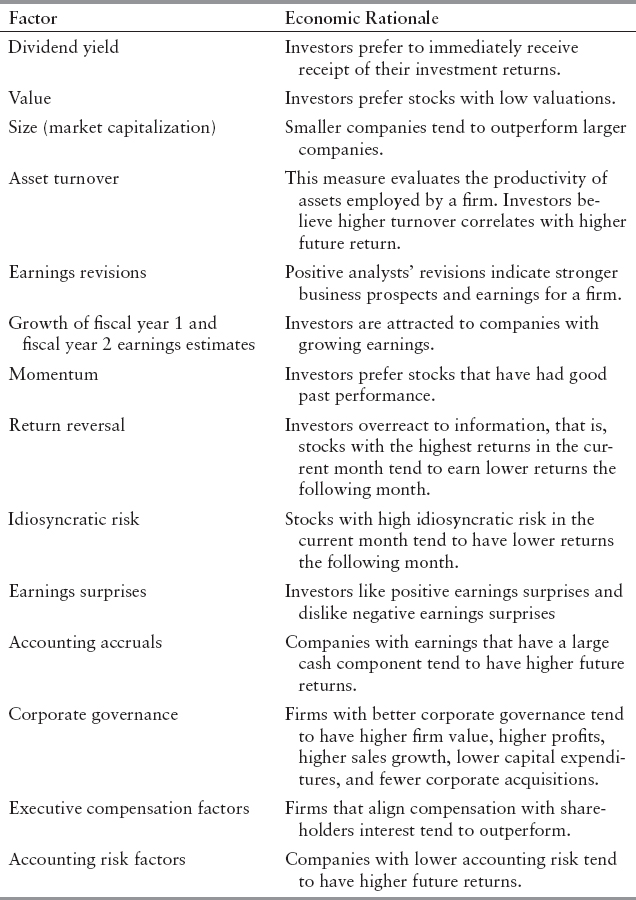

Today's quantitative managers use factors as fundamental building blocks for trading strategies. Within a trading strategy, factors determine when to buy and sell securities. We define a factor as a common characteristic among a group of assets. In the equities market, it could be a particular financial ratio such as the price–earnings (P/E) or the book–price (B/P) ratios. Some of the most well-known factors and their underlying basic economic rationale references are provided in Exhibit 11.1.

Most often this basic definition is expanded to include additional objectives. First, factors frequently are intended to capture some economic intuition. For instance, a factor may help understand the prices of assets by reference to their exposure to sources of macroeconomic risk, fundamental characteristics, or basic market behavior. Second, we should recognize that assets with similar factors (characteristics) tend to behave in similar ways. This attribute is critical to the success of a factor. Third, we would like our factor to be able to differentiate across different markets and samples. Fourth, we want our factor to be robust across different time periods.

EXHIBIT 11.1 Summary of Well-Known Factors and Their Underlying Economic Rationale

Factors fall into three categories—macroeconomic influences, cross-sectional characteristics, and statistical factors. Macroeconomic influences are time series that measure observable economic activity. Examples include interest rate levels, gross domestic production, and industrial production. Cross-sectional characteristics are observable asset specifics or firm characteristics. Examples include, dividend yield, book value, and volatility. Statistical factors are unobservable or latent factors common across a group of assets. These factors make no explicit assumptions about the asset characteristics that drive commonality in returns. Statistical factors, also referred to as latent factors, are not derived using exogenous data but are extracted from other variables such as returns. These factors are calculated using various statistical techniques such as principal components analysis or factor analysis.

Within asset management firms, factors and forecasting models are used for a number of purposes. Those purposes could be central to managing portfolios. For example, a portfolio manager can directly send the model output to the trading desk to be executed. In other uses, models provide analytical support to analysts and portfolio management teams. For instance, models are used as a way to reduce the investable universe to a manageable number of securities so that a team of analysts can perform fundamental analysis on a smaller group of securities.

Factors are employed in other areas of financial theory, such as asset pricing, risk management, and performance attribution. In asset pricing, researchers use factors as proxies for common, undiversifiable sources of risk in the economy to understand the prices or values of securities to uncertain payments. Examples include the dividend yield of the market or the yield spread between a long-term bond yield and a short-term bond yield.4 In risk management, risk managers use factors in risk models to explain and to decompose variability of returns from securities, while portfolio managers rely on risk models for covariance construction, portfolio construction, and risk measurement. In performance attribution, portfolio managers explain past portfolio returns based on the portfolio's exposure to various factors. Within these areas, the role of factors continues to expand. Recent research presents a methodology for attributing active return, tracking error, and the information ratio to a set of custom factors.5

The focus in this and the companion chapter is on using factors to build equity forecasting models, also referred to as alpha or stock selection models. The models serve as mathematical representations of trading strategies. The mathematical representation uses future returns as dependent variables and factors as independent variables.