ANALYSIS

How does constraining shortfall beta as shown above improve performance? The shortfall constraint forces the manager to adopt certain positions to limit the exposure to extreme losses. To better understand this, we decompose the active portfolio into positions due to the manager's alpha and positions taken to satisfy individual constraints. This decomposition is based on the portfolio optimality conditions.7

We can express the active portfolio as the sum of four component portfolios:

where hA represents the active holdings and πI,πβ,πBS are the shadow prices8 of the full investment, beta and shortfall beta constraints, respectively. Equation (19.4) shows the portfolio can be decomposed into the positions due to the manager's alpha (hAlpha) and the positions taken to satisfy the three constraints—hFull investment, hBeta neutrality, and hShortfall beta.

The alpha portfolio is the portfolio in which the manager would invest in the absence of constraints. Each constraint portfolio—full investment, beta neutrality, and shortfall beta—contains the additional positions needed to satisfy that constraint in a way that maximizes portfolio utility. We define the return due to each of these sources as the return of the corresponding portfolio.

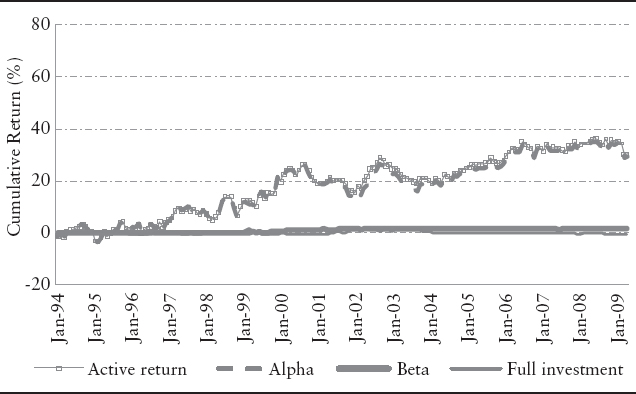

Exhibit 19.6 shows a return decomposition for the relative strength strategy implemented with standard mean variance optimization. The active return comes almost entirely from the alpha. Requiring the portfolio to be beta neutral and fully invested has little effect on performance.

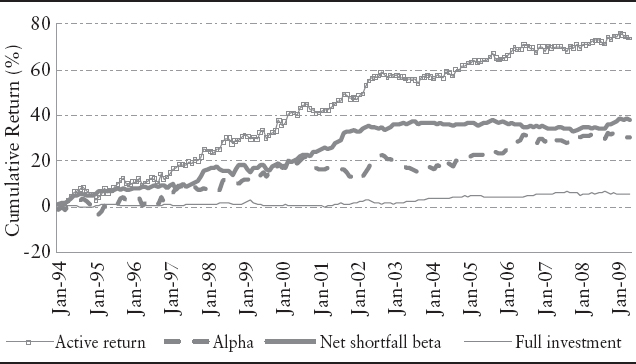

Exhibit 19.7 shows the same breakdown for shortfall constrained optimization. The contribution from alpha is very similar to that obtained with mean-variance optimization. Once again, the full investment constraint has little impact on return. However, in this case, we constrain the shortfall beta while keeping the portfolio beta one. The “net shortfall beta portfolio,” defined as the sum of the two constraint portfolios, hBeta neutrality and hShortfall beta, reflects this stipulation. As Exhibit 19.7 shows, that decision is a significant source of return, contributing roughly as much as the alpha.

EXHIBIT 19.6 Return Decomposition for Standard Mean-Variance Optimization

EXHIBIT 19.7 Return Decomposition for Shortfall Constrained Mean-Variance Optimization

Next, we take a closer look at the impact of constraining shortfall. The contribution of the net shortfall beta portfolio to the active return depends on two things. It depends on the size of the investment in this portfolio. It also depends on how well this portfolio performs. To disentangle these two effects, we note that we can split any component portfolio into two terms:

The first term tells us the size of the investment. The second term, the normalized portfolio, is a portfolio whose return is independent of the size of the investment.

The net shortfall beta portfolio's performance on a normalized basis is reported in Exhibit 19.8. We see that it performs well during our backtesting period, especially during the dot.com meltdown and again during the recent financial crisis. So the return from constraining shortfall beta comes, in part, from the strong performance of this portfolio.

EXHIBIT 19.8 Performance of the Normalized Net Shortfall Beta Portfolio

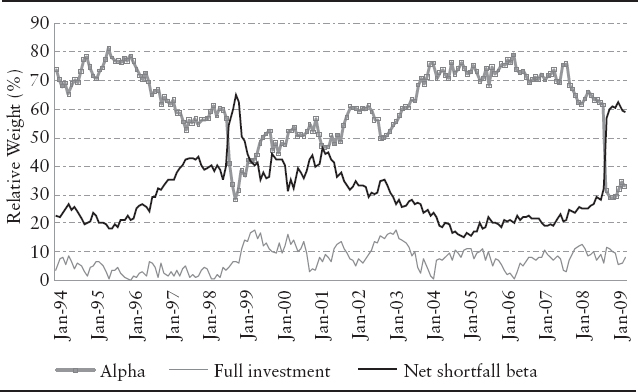

What about the size of the net shortfall beta portfolio? That is, what fraction of the portfolio weight is devoted to limiting extreme losses? To examine this, we define the relative weight of a component as:

The evolution of these weights is shown in Exhibit 19.9. Most of the time, the largest weight is devoted to alpha. However, during periods of market stress, the portfolio may place as much or even greater weight on insuring against losses than it does on pursuing alpha. This occurs around the Russian crisis of 1998 and during the more recent market plunge in the fall of 2008. So the shortfall beta constraint also seems to help by shifting the active portfolio toward the shortfall beta portfolio during periods of stress.

Our simple empirical examples suggest that constraining shortfall beta may offer some downside protection in turbulent periods without sacrificing performance over longer periods. Several questions still remain, including how to effectively capture the information in shortfall beta in the presence of additional constraints and execution costs.

EXHIBIT 19.9 Evolution of the Relative Weights of the Component Portfolios