IMPOSING BENCHMARK NEUTRALITY

To separate the effects of beta and shortfall beta, we rerun the optimizations, this time requiring the beta of all portfolios to be one. Specifically, we add the constraint: h′β = 1 to the problem in (19.3) where β is a vector of betas with respect to the MSCI US Prime Market 750 Index. This is of particular interest to managers who do not time the benchmark.

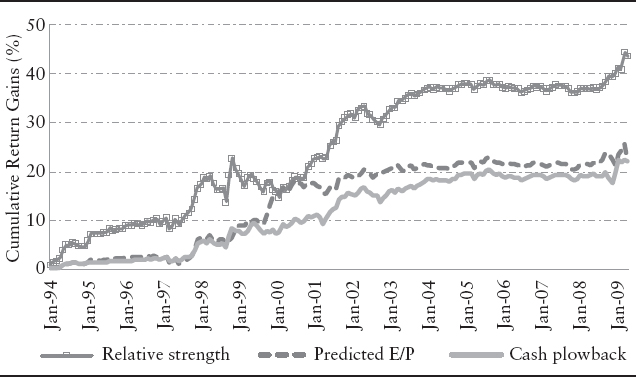

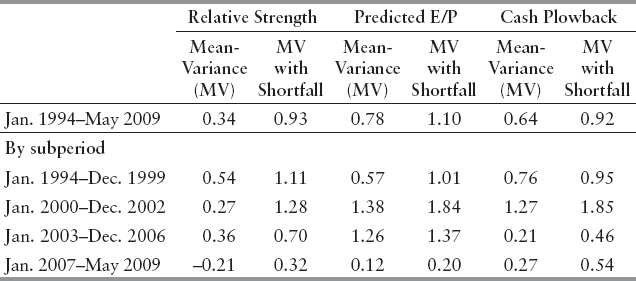

Exhibits 19.3 and 19.4 show that the benefits of constraining shortfall beta are even greater than before. As before, shortfall constrained optimization outperforms standard optimization over the entire period. It also outperforms during the Internet meltdown and to some extent over the more recent turbulent period, particularly for the relative strength strategy. Lastly, we see that by removing the benchmark timing implicit in shortfall optimization, we eliminate its underperformance during the Internet bubble.

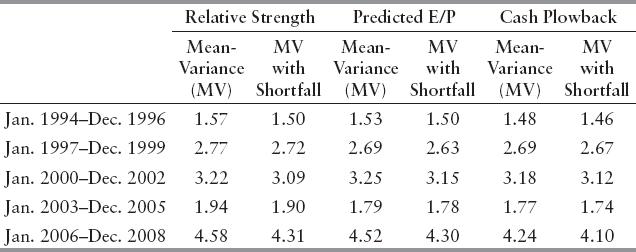

Does constraining shortfall help protect against sharp daily losses? To address this question, we examine the realized shortfall of each portfolio by computing the average return of its 5% worst outcomes—the “bad days.” Exhibit 19.5 shows the realized shortfall for nonoverlapping three year periods. Shortfall constrained portfolios have lower realized losses over each period, even though they have the same ex ante active risk as standard mean-variance portfolios. The difference in shortfall was greatest over the more volatile periods. We also find similar results at the yearly level.

EXHIBIT 19.3 Cumulative Gains from Constraining Shortfall Beta:Benchmark-Neutral Case

EXHIBIT 19.4 Constraining on Shortfall Betas: Benchmark-Neutral Case—Information Ratios

EXHIBIT 19.5 Comparison of Realized Shortfall: Benchmark-Neutral Case