LIQUIDITY AND TRANSACTION COSTS

Liquidity is created by agents transacting in the financial markets when they buy and sell securities. Market makers and brokers–dealers do not create liquidity; they are intermediaries who facilitate trade execution and maintain an orderly market.

Liquidity and transaction costs are interrelated. A highly liquid market is one were large transactions can be immediately executed without incurring high transaction costs. In an indefinitely liquid market, traders would be able to perform very large transactions directly at the quoted bid-ask prices. In reality, particularly for larger orders, the market requires traders to pay more than the ask when buying, and to receive less than the bid when selling. As we discussed previously, this percentage degradation of the bid-ask prices experienced when executing trades is the market impact cost.

The market impact cost varies with transaction size: the larger the trade size the larger the impact cost. Impact costs are not constant in time, but vary throughout the day as traders change the limit orders that they have in the limit order book. A limit order is a conditional order; it is executed only if the limit price or a better price can be obtained. For example, a buy limit order of a security XYZ at $60 indicates that the assets may be purchased only at $60 or lower. Therefore, a limit order is very different from a market order, which is an unconditional order to execute at the current best price available in the market (guarantees execution, not price). With a limit order, a trader can improve the execution price relative to the market order price, but the execution is neither certain nor immediate (guarantees price, not execution).

Notably, there are many different limit order types available such as pegging orders, discretionary limit orders, immediate or cancel order (IOC) orders, and fleeting orders. For example, fleeting orders are those limit orders that are canceled within two seconds of submission. Hasbrouck and Saar find that fleeting limit orders are much closer substitutes for market orders than for traditional limit orders.5 This suggests that the role of limit orders has changed from the traditional view of being liquidity suppliers to being substitutes for market orders.

At any given instant, the list of orders sitting in the limit order book embodies the liquidity that exists at a particular point in time. By observing the entire limit order book, impact costs can be calculated for different transaction sizes. The limit order book reveals the prevailing supply and demand in the market.6 Therefore, in a pure limit order market, we can obtain a measure of liquidity by aggregating limit buy orders (representing the demand) and limit sell orders (representing the supply).7

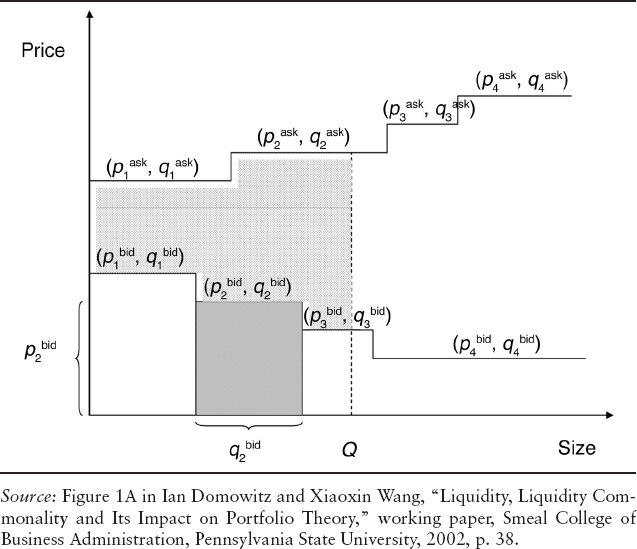

EXHIBIT 17.1 The Supply and Demand Schedule of a SecuritySource:

We start by sorting the bid and ask prices, ![]() and

and ![]() , (from the most to the least competitive) and the corresponding order quantities

, (from the most to the least competitive) and the corresponding order quantities ![]() and

and ![]() . We then combine the sorted bid and ask prices into a supply and demand schedule according to Exhibit 17.1. For example, the block

. We then combine the sorted bid and ask prices into a supply and demand schedule according to Exhibit 17.1. For example, the block ![]() represents the second best sell limit order with price

represents the second best sell limit order with price ![]() and quantity

and quantity ![]() .

.

We note that unless there is a gap between the bid (demand) and the ask (supply) sides, there will be a match between a seller and buyer, and a trade would occur. The larger the gap, the lower the liquidity and the market participants' desire to trade. For a trade of size Q, we can define its liquidity as the reciprocal of the area between the supply and demand curves up to Q (i.e., the “dotted” area in Exhibit 17.1).

However, few order books are publicly available and not all markets are pure limit order markets. In 2004, the New York Stock Exchange (NYSE) started selling information on its limit order book through its new system called the NYSE OpenBook®. The system provides an aggregated real-time view of the exchange's limit-order book for all NYSE-traded securities.8

In the absence of a fully transparent limit order book, expected market impact cost is the most practical and realistic measure of market liquidity. It is closer to the true cost of transacting faced by market participants as compared to other measures such as those based upon the bid-ask spread.