IFRS 9 FINANCIAL INSTRUMENTS AND IAS 39 FINANCIAL INSTRUMENTS: RECOGNITION AND MEASUREMENT

1 INTRODUCTION

IAS 39 sets out the requirements for recognizing and measuring financial assets and financial liabilities. However, the IASB is currently developing a new standard (IFRS 9) that will ultimately replace IAS 39 in its entirety. The IASB divided that project to replace IAS 39 into three main phases (IFRS 9.IN1 and 9.IN5–9.IN6):

- Classification and measurement of financial assets and financial liabilities

- Impairment methodology

- Hedge accounting

As the IASB completes each phase, the relevant portions of IAS 39 will be deleted and new chapters will be created in IFRS 9 that replace the requirements in IAS 39.

In November 2009, the Board issued the chapters of IFRS 9 that relate to the classification and measurement of financial assets. In October 2010, the IASB added the requirements to IFRS 9 for classifying and measuring financial liabilities. At the same time, the requirements in IAS 39 related to the derecognition of financial assets and financial liabilities were carried forward unchanged to IFRS 9 (IFRS 9.IN7–IN8). By amending IFRS 9 in October 2010, the Board completed the first main phase of its project to replace IAS 39. However, currently the IASB intends to make limited modifications to the already existing rules of IFRS 9.

IFRS 9 (2010) has to be applied for annual periods beginning on or after Jan 01, 2015. However earlier application is permitted (IFRS 9.7.1.1). In the European Union, new IFRSs have to be endorsed by the European Union before they can be applied. Since there has been no endorsement with regard to IFRS 9 until now, the new rules cannot be applied in the European Union at the moment.

The remaining part of this chapter of the book is subdivided as follows:

- In Section 2, financial instruments accounting is explained on the basis of IFRS 9 (as issued in October 2010) and its consequential amendments to IAS 39.

- In Section 3, the differences between financial instruments accounting prior to IFRS 9 and the requirements applicable when applying IFRS 9 (2010) early are illustrated.

- Each of these two sections closes with a subsection that includes examples.

2 FINANCIAL INSTRUMENTS ACCOUNTING ACCORDING TO IFRS 9 (AS ISSUED IN 2010) AND ITS CONSEQUENTIAL AMENDMENTS TO IAS 39

2.1 Scope1

Generally speaking, IFRS 9 (as issued in October 2010) is applied for recognizing, derecognizing, and measuring financial assets and financial liabilities (IFRS 9.2.1), whereas IAS 39 still sets out the requirements for impairment testing and hedge accounting that are not yet addressed by IFRS 9. Some aspects of financial instruments accounting are not covered by IFRS 9 and IAS 39. These are dealt with in the chapters on IAS 32 (“Financial Instruments: Presentation”) and IFRS 7 (“Financial Instruments: Disclosures”).

In the investor's consolidated financial statements, equity instruments are generally not in the scope of IFRS 9 if they are interests in subsidiaries, joint ventures or associates (IAS 39.2 and IFRS 9.2.1).

2.2 Initial Recognition

As a general principle, a financial asset or a financial liability is recognized in the statement of financial position when the entity becomes a contracting party (IFRS 9.3.1.1). As a consequence, positive and negative fair values of financial derivatives are recognized in that statement (IFRS 9.B3.1.1).

However, receivables and liabilities that are the result of a firm commitment to purchase or sell goods or services are generally not recognized until at least one of the parties has completed their side of the agreement. For example, an entity that receives an order generally does not recognize a trade receivable (and the entity that places the order does not recognize a trade payable) at the time of the commitment but, rather, delays recognition until the ordered goods or services have been shipped, delivered or rendered (IFRS 9.B 3.1.2b).

2.3 Measurement

2.3.1 Derivatives and Financial Instruments Held for Trading

When discussing the measurement of financial instruments, it is first necessary to understand the terms “derivative” and “held for trading:”

- A derivative is a financial instrument or other contract within the scope of IFRS 9 that meets all three of the following criteria (IFRS 9.Appendix A):

- Its value changes in response to the change of an underlying. Examples of underlyings are interest rates, financial instrument prices, commodity prices, foreign exchange rates, indices of prices or rates, credit ratings or credit indices. In the case of a non-financial underlying (e.g. weather conditions), the contract is only considered a derivative if the variable is not specific to a party to the contract. Non-financial variables that are not specific to a party to the contract include an index of earthquake losses in a particular region and an index of temperatures in a particular city. Non-financial variables specific to a party to the contract include the occurrence or non-occurrence of a fire that damages or destroys an asset of a party to the contract (IFRS 9.BA5).

- No initial net investment is necessary or the initial net investment is smaller than would be required for other types of contracts that have a similar response to changes in market factors.

- Settlement is at a future date.

- A financial asset or financial liability meets the definition of held for trading if one of the criteria below is met (IFRS 9.Appendix A):

- It is acquired or incurred principally for the purpose of selling or repurchasing it in the near term or it is part of a portfolio managed in this way.

- It is a derivative that is neither a designated and effective hedging instrument nor a financial guarantee contract.

2.3.2 Initial Measurement

Financial assets and financial liabilities are initially recognized at fair value (IFRS 9.5.1.1). This is the amount for which an asset could be exchanged or a liability settled between knowledgeable, willing parties in an arm's length transaction (IFRS 9.Appendix A).

Transaction costs are incremental costs that are directly attributable to the acquisition, issue or disposal of a financial asset or financial liability. The accounting treatment of transaction costs depends on the subsequent measurement2 of the financial asset or financial liability (IFRS 9.5.1.1, IFRS 9.IG E.1.1, and IAS 39.9):

- If subsequent measurement is at fair value through profit or loss, transaction costs are immediately recognized in profit or loss.

- If subsequent measurement is not at fair value through profit or loss, transaction costs of a financial asset are capitalized and transaction costs of a financial liability are deducted from the carrying amount of the liability.

Transaction price is the fair value of the consideration given or received. Normally, the fair value of a financial instrument on initial recognition is the transaction price (IFRS 9.B5.1.1 and 9.B5.4.8). Hence, normally, measurement on initial recognition is actually at cost, when disregarding transaction costs.

2.3.3 Subsequent Measurement of Financial Assets

With regard to financial assets, IFRS 9 is based on a mixed measurement model in which some financial assets are measured at fair value and others at amortized cost after recognition. The distinction between the amortized cost and fair value category is principle-based.

IFRS 9 requires that financial assets are classified at initial recognition into the categories “amortized cost” or “fair value” which are relevant for the assets' subsequent measurement (IFRS 9.3.1.1 and 9.4.1.1–9.4.1.4). This classification is effected on the basis of both (IFRS 9.4.1.1):

- the entity's business model for managing the financial assets, and

- the contractual cash flow characteristics of the financial asset.

A financial asset is classified into the category “amortized cost” if both of the following conditions are met (IFRS 9.4.1.2):

- Subjective condition: The objective of the business model for the group of assets to which the asset under review belongs is to hold assets in order to collect contractual cash flows.

- Objective condition: The contractual terms of the financial asset give rise on specified dates to cash flows which are solely payments of interest and principal on the principal amount outstanding.

If a financial asset does not meet both of these criteria it has to be measured at fair value (IFRS 9.4.1.4).

The objective of the business model is the objective determined by the entity's key management personnel within the meaning of IAS 24 (IFRS 9.B4.1.1).

The business model does not depend on management's intentions for an individual financial asset. This condition should be determined on a higher level of aggregation, i.e. for portfolios of financial assets. A single entity may have one or more such portfolio. For example, an entity may hold a portfolio of financial assets that it manages in order to collect contractual cash flows and another portfolio of financial assets that it manages in order to trade to realize fair value changes (IFRS 9.B4.1.2).

The objective of an entity's business model may be to hold financial assets in order to collect contractual cash flows, even though not all of the assets are held until maturity. However, if more than an infrequent number of sales are made out of a particular portfolio, it is necessary to assess whether and how such sales are consistent with an objective of collecting contractual cash flows (IFRS 9.B4.1.3 and 9.B4.1.4, Example 1).

The classification of a financial asset into the category “amortized cost” requires objectively that the contractual terms of the asset give rise on specified dates to cash flows that are solely payments of interest and principal on the principal amount outstanding (IFRS 9.4.1.2b). For the purpose of IFRS 9, interest is consideration for the time value of money (i.e. for the provision of money to another party over a particular period of time) and for the credit risk associated with the principal amount outstanding (IFRS 9.4.1.3), which may include a premium for liquidity risk (IFRS 9.BC4.22).

The assessment of this criterion is based on the currency in which the financial asset is denominated (IFRS 9.B4.1.8).

Leverage is a characteristic of the contractual cash flows of some financial assets. Leverage increases the variability of the contractual cash flows with the result that they do not have the economic characteristics of interest within the meaning of IFRS 9. Therefore, such contracts cannot be measured at amortized cost. Stand-alone options, forward and swap contracts are examples of financial assets that include leverage (IFRS 9.B4.1.9). A variable interest rate does not preclude contractual cash flows that are solely payments of interest and principal on the principal amount outstanding. However, the variable interest rate has to be consideration for the time value of money (i.e. for the provision of money to another party over a particular period of time) and for the credit risk associated with the principal amount outstanding (IFRS 9.B4.1.12).

In spite of the classification criteria described above, it is possible to designate a financial asset as measured at fair value through profit or loss (fair value option) at initial recognition. This requires that doing so eliminates or significantly reduces a measurement or recognition inconsistency (accounting mismatch) that would otherwise arise from measuring assets or liabilities or recognizing the gains and losses on them on different bases (IFRS 9.4.1.5).3

2.3.4 Subsequent Measurement of Financial Liabilities

With regard to financial liabilities, IFRS 9 is also based on a mixed measurement model in which some financial liabilities are measured at fair value and others at amortized cost after recognition.

Normally, financial liabilities are measured at amortized cost. Exceptions to this rule are, among others, financial liabilities at fair value through profit or loss (see below) and financial guarantee contracts4 (IFRS 9.4.2.1).

The category “financial liabilities at fair value through profit or loss” consists of two sub-categories (IFRS 9.Appendix A):

- Financial liabilities that meet the definition of “held for trading.”5

- Financial liabilities for which the fair value option is exercised, i.e. which are designated upon initial recognition by the entity as “at fair value through profit or loss.” The fair value option may be exercised with respect to a financial liability if one of the following conditions is met (IFRS 9.4.2.2 and IFRS 9.4.3.5):

- Exercising the option eliminates or significantly reduces an inconsistency (accounting mismatch).

- A group of financial liabilities or financial assets and financial liabilities is managed and its performance is evaluated on a fair value basis according to a documented risk management or investment strategy and information about that group is provided internally on that basis to the entity's key management personnel.

- Under certain circumstances, a contract that contains at least one embedded derivative (hybrid or combined instrument) may be designated as at fair value through profit or loss.

2.3.5 Measurement at Amortized Cost: Determining the Effective Interest Rate

Measurement of financial assets or financial liabilities at amortized cost according to IFRS 9 means application of the effective interest method (IAS 39.9 and IFRS 9.4.2.1). Effective interest includes, for example, the contractual interest, premiums, discounts, and transaction costs. The effective interest rate is the rate that discounts the cash payments or receipts of the financial asset or financial liability to the net carrying amount of the asset or liability at initial recognition. When calculating the effective interest rate, the estimated future cash payments or receipts of the financial instrument through its expected life (or, when appropriate, a shorter period) are used. However, future credit losses are not included in this calculation (IAS 39.9).

2.3.6 Determining Fair Values After Recognition

IFRS 9 establishes a fair value hierarchy (IFRS 9.5.4.1, 9.5.4.2, and IFRS 9.B5.4.1–9.B5.4.17):

- The best evidence of fair value is quoted prices in an active market.

- If there is no active market, fair value is determined on the basis of recent transactions or by reference to the current fair value of another instrument that is substantially the same.

- If it is not possible to determine fair value as described previously, valuation models are used (in particular discounted cash flow analysis and option pricing models).

- In the case of investments in unquoted equity instruments (and contracts on those investments that must be settled by delivery of the unquoted equity instruments) cost may be an appropriate estimate of fair value, in limited circumstances.

2.3.7 Presentation of Fair Value Gains and Losses

Changes in fair value of financial assets or financial liabilities measured at their fair values and that are not part of a hedging relationship (see IAS 39.89–39.102) are generally recognized in profit or loss.

Exercising the fair value option for financial assets6 means that the changes in fair value are presented in profit or loss (IFRS 9.4.1.5).

If the fair value option is exercised for financial liabilities,7 fair value changes have to be presented as follows (IFRS 9.5.7.1 and 9.5.7.7–9.5.7.8):

- The amount of change in the fair value of the liability that is attributable to changes in the liability's credit risk is presented in other comprehensive income.

- The remaining amount of change in the fair value of the liability is presented in profit or loss.

- However, an exception is applicable if presentation of the changes in the liability's credit risk in other comprehensive income (see above) would create or enlarge an accounting mismatch in profit or loss. In such cases, all fair value changes of that liability (including the effects of changes in the liability's credit risk) have to be presented in profit or loss.

If the fair value option has been exercised for financial liabilities, amounts presented in other comprehensive income must not be subsequently transferred to profit or loss. However, the cumulative gain or loss may be transferred within equity, e.g. to retained earnings (IFRS 9.B5.7.9).

It is possible to recognize the change in the fair value of an equity instrument (e.g. a share) within the scope of IFRS 9 that is not held for trading in other comprehensive income instead of recognizing it in profit or loss. In order to avoid the so-called “cherry picking” (i.e. in order to avoid entities recognizing changes in fair value in profit or loss or in other comprehensive income selectively), this choice can only be made at initial recognition of the equity instrument and is irrevocable in the future (IFRS 9.5.7.5 and IFRS 9.BC5.25d).

Amounts presented in other comprehensive income for such equity instruments must not be subsequently transferred to profit or loss, i.e. not even when the equity instrument is derecognized. However, the entity may transfer the cumulative gain or loss within equity, e.g. to retained earnings (IFRS 9.B5.7.1).

2.3.8 Impairment Losses and Reversals of Impairment Losses

In the case of financial assets measured at fair value, all fair value changes are recognized either in profit or loss or in other comprehensive income (IFRS 9.5.7.1). Amounts recognized in other comprehensive income must not be subsequently transferred to profit or loss (IFRS 9. B5.7.1). Consequently, according to the systematics of IFRS 9, assessing whether financial assets are impaired and recognizing impairment losses is only necessary for financial assets carried at amortized cost. In this respect, the rules of IAS 39 apply because IFRS 9 does not yet contain such rules (IFRS 9.5.2.2).

At the end of each reporting period, it has to be assessed whether there is any objective evidence of impairment (loss events) in respect of financial assets measured at amortized cost (IAS 39.58). IAS 39 includes a list of examples of loss events that relate to financial difficulties of the debtor (e.g. it becoming probable that the borrower will enter bankruptcy) (IAS 39.59).

If there is objective evidence that an impairment loss on these financial assets has been incurred, the following amounts have to be compared with each other (IAS 39.63):

- The asset's carrying amount as at the end of the reporting period determined according to the effective interest method.

- The present value of the asset's estimated future cash flows (excluding future credit losses that have not been incurred). These cash flows are discounted at the financial asset's original effective interest rate (i.e. the effective interest rate computed at initial recognition).

If the asset's carrying amount exceeds its present value, an impairment loss is recognized in profit or loss (IAS 39.63). It is important to note that this present value does not correspond with fair value because the cash flows are not discounted at a market interest rate. This results in moderate impairment losses which reflect financial difficulties of the debtor, but not market risks.

An entity first assesses whether an impairment exists individually for financial assets that are individually significant. If there is objective evidence of impairment, the impairment loss has to be determined and recognized for the financial asset under review. Assessing impairment on the basis of a group of financial assets is possible for insignificant financial assets instead of an assessment on an individual basis. Moreover, assessment on a group basis is necessary in the case of financial assets tested individually for impairment, for which no impairment has been determined on an individual basis and for which statistical credit risks exist (IAS 39.64).

If the amount of an impairment loss recognized in a previous period decreases and the decrease can be related objectively to an event occurring after the impairment was recognized, a reversal of the impairment loss has to be recognized in profit or loss. The reversal must not result in a carrying amount of the asset that exceeds what the amortized cost would have been at the date the impairment is reversed had the impairment not been recognized (IAS 39.65).

2.4 Hybrid Contracts

2.4.1 Introduction

Hybrid or combined instruments consist of a host contract (e.g. a bond) that is supplemented with additional rights or obligations. A simple example is a convertible bond. A convertible bond consists of a bond (host) which is redeemed at maturity if the conversion right is not exercised. However, if the conversion right (embedded derivative) is exercised, the holder of the convertible bond receives shares of the issuer instead of cash.

A derivative that is attached to a financial instrument but is contractually transferable independently of that instrument, or has a different counterparty is not an embedded derivative, but a separate financial instrument (IFRS 9.4.3.1).

If a hybrid contract contains a liability component as well as an equity component (e.g. in the case of a convertible bond from the perspective of the issuer), these components are separated according to the rules of IAS 32 in the issuer's financial statements (IFRS 9.2.1, IAS 39.2d, and IAS 32.28–32.32) which differ from the rules of IFRS 9 illustrated in Sections 2.4.2 and 2.4.3 below.8 However, the holder of such contracts classifies them in accordance with IFRS 9.

2.4.2 Hybrid Contracts with Financial Asset Hosts

When the hybrid contract contains a host that is an asset within the scope of IFRS 9, the hybrid contract is classified either into the category “amortized cost” or into the category “fair value” in its entirety according to the classification rules of IFRS 9 (IFRS 9.4.3.2, 9.B5.2.1, and 9.4.1.1–9.4.1.5).

2.4.3 Other Hybrid Contracts

A hybrid contract may contain a host that is not an asset within the scope of IFRS 9. In such a case it is necessary to determine whether the embedded derivative has to be separated from the host. Separate accounting of an embedded derivative under IFRS 9 is necessary if all of the following criteria are met (IFRS 9.4.3.3):

- The hybrid instrument is not measured at fair value through profit or loss.

- The economic characteristics and risks of the embedded derivative are not closely related to those of the host contract.

- A separate instrument with the same terms as the embedded derivative would meet the definition of a derivative.

If separation of an embedded derivative is necessary, the host is accounted for in accordance with the appropriate IFRSs (IFRS 9.4.3.4) and the embedded derivative is measured at fair value at initial recognition and subsequently (IFRS 9.B4.3.1).

If an entity is unable to determine reliably the fair value of an embedded derivative on the basis of its terms and conditions, the fair value of the embedded derivative is the difference between the fair value of the hybrid contract and the fair value of the host if those can be determined according to IFRS 9. If separate accounting of an embedded derivative from its host is necessary, but the entity is unable to measure the embedded derivative separately either at acquisition or at the end of a subsequent period, the entire hybrid contract has to be designated as at fair value through profit or loss (IFRS 9.4.3.6–9.4.3.7).

Assessment of whether an embedded derivative is required to be separated is made when the entity first becomes a party to the contract. Subsequent reassessment is prohibited unless there is a change in the terms of the contract that significantly modifies the cash flows, in which case reassessment is necessary (IFRS 9.B4.3.11–9.B4.3.12).

There is extensive case history with regard to embedded derivatives (IFRS 9.B4.3.1–9.B4.3.8 and IFRS 9.IG C.1–9.IG C.10). The analysis may be complex depending on the circumstances and the requirements may result in less reliable measures than measuring the entire instrument at fair value through profit or loss. Hence, it is possible to measure the entire hybrid instrument at fair value through profit or loss if certain criteria are met (IFRS 9.4.3.5 and 9.B4.3.9–9.B4.3.10).9 If this form of the fair value option is exercised, separating the embedded derivative becomes unnecessary and is prohibited (IFRS 9.4.3.3c).

2.5 Derecognition of Financial Assets

IFRS 9 contains extensive rules relating to the issue of when and how a previously recognized financial asset has to be removed from the statement of financial position (derecognition) (IFRS 9.Appendix A). Apart from situations in which financial assets (e.g. receivables) are extinguished (e.g. statute of limitation or redemption) and apart from consolidation rules, the following chart applies (IFRS 9.B3.2.1):

Remarks to Step 1

At first it is necessary to investigate whether the financial asset has been transferred. This is the case in each of the following situations:

- The rights to receive the cash flows have been transferred (IFRS 9.3.2.4a) (e.g. a receivable has been sold).

- The entity retains the contractual rights to receive the cash flows of the financial asset but assumes an obligation to pay the cash flows to one or more recipients in an arrangement that meets the conditions specified in IFRS 9.3.2.5 (IFRS 9.3.2.4b).

Remarks to Step 2

If the financial asset has been transferred (see Step 1), it is necessary to investigate whether the entity has retained or substantially transferred all the risks and rewards of ownership of the financial asset. In the case of receivables, the relevant risk is the credit risk, whereas in the case of securities, the relevant risk is the risk of fluctuations in market prices. Three situations are possible:

- The entity has transferred substantially all the risks and rewards (IFRS 9.3.2.6a). In this case, the financial asset has to be derecognized. Moreover, any rights and obligations created or retained in the transfer are recognized separately as assets or liabilities.

- The entity retains substantially all the risks and rewards (IFRS 9.3.2.6b). In this case, the financial asset continues to be recognized. If the entity has, for instance, sold a receivable and already received the consideration therefor, the receivable continues to be recognized in the statement of financial position and the consideration is recognized via the entry “Dr Cash Cr Financial liability” (IFRS 9.3.2.15).

- The entity neither transfers nor retains substantially all the risks and rewards (IFRS 9.3.2.6c). For this situation, we refer to Step 3.

Remarks to Step 3

Step 3 requires determination as to whether control of the asset has been retained (IFRS 9.3.2.9 and IFRS 9.B3.2.7–9.B3.2.9). This involves an assessment as to whether the transferee has the practical ability to sell the transferred asset. If this is the case, the transferor has lost control.

- If control has not been retained, the financial asset is derecognized (IFRS 9.3.2.6(c)(i)). Any rights and obligations created or retained in the transfer are recognized separately as assets or liabilities.

- If control has been retained, the transferor continues to recognize the financial asset to the extent of its continuing involvement in the asset (IFRS 9.3.2.6(c)(ii) and IFRS 9.3.2.16–9.3.2.21).

The gain or loss on derecognition of a financial asset is calculated on the basis of the carrying amount measured at the date of derecognition (IFRS 9.3.2.12, 9.3.2.13, and 9.3.2.20).

2.6 Financial Guarantee Contracts From the Issuer's Perspective

A financial guarantee contract is a contract that requires the issuer to make specified payments to reimburse the holder for a loss it incurs because a specified debtor fails to make payment when due in accordance with the original or modified terms of a debt instrument (IFRS 9.Appendix A). This chapter focuses on the typical accounting treatment of liabilities from co-signing in the financial statements of industrial and mercantile enterprises.

Under certain circumstances, a co-signer can apply IFRS 4. In other situations (these are the normal situations for industrial and mercantile enterprises) application of IFRS 9 is mandatory. Subsequently, only the accounting treatment according to IFRS 9 is illustrated.

Financial guarantees are measured initially at fair value (IFRS 9.5.1.1).

Two different types of financial guarantees that are issued against consideration have to be distinguished:

- The issuer receives a one-time payment in advance when issuing the guarantee.

- The issuer receives payments on an ongoing basis.

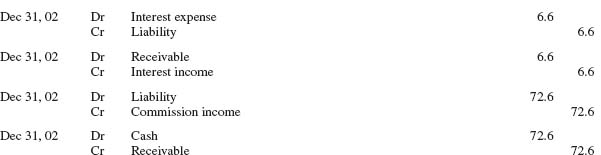

The remaining part of this section focuses on contracts with ongoing payments. In the case of such a contract, the initial fair value of the financial guarantee is the present value of the ongoing payments. In our view, in this case, the entry “Dr Receivable (right to receive commission payments) Cr Liability (obligation from co-signing)” is necessary at initial recognition.

Liabilities from co-signing against consideration are normally measured subsequently at amortized cost in the financial statements of industrial and mercantile enterprises. Two different situations have to be distinguished:

- A default is not expected: In this case, commission income is recognized over the duration of the obligation from co-signing. The entry is “Dr Liability (obligation from co-signing) Cr Commission income” (IFRS 9.4.2.1c). The receivable (right to receive commission payments) is reduced by the ongoing commission payments.

- A default is expected: If risk assessments deteriorate when the liability from co-signing is subsequently measured with the result that the amount of the liability from co-signing under IAS 37 exceeds the amount initially recognized and reduced by the appropriate amount of revenue, this higher amount is the new carrying amount of the liability (IFRS 9.4.2.1c). This means that the carrying amount is increased to the expected value of the obligation (which is the amount co-signed for, multiplied by the probability of default) (“Dr Expense Cr Liability”). Thereby, in our view, only the measurement rules and not the recognition rules of IAS 37 apply. This means that the liability is measured at expected value, even if the default risk is below 50%. This new carrying amount of the liability is amortized according to IAS 18 in subsequent periods. In the case of a deteriorated risk assessment, the carrying amount is again increased to the expected value of the obligation according to IAS 37.

2.7 Hedge Accounting

2.7.1 Introduction

The application of IFRS 9 may lead to measurement or recognition inconsistencies (accounting mismatches). These are sometimes due to the fact that IFRS 9 is based on a mixed measurement model in which some financial assets and financial liabilities are measured at fair value and others at amortized cost after recognition.10

Example 1: Entity E is the creditor of a fixed interest rate loan. An increase (a reduction) in the market interest rate leads to a reduction (an increase) in fair value (calculated as present value) of the loan. Assume that E intends to hedge the risk of changes in fair value. Hence, E enters into an interest rate swap (derivative) under which E pays fixed interest and receives variable interest. This means that in essence, E receives variable interest on the loan instead of fixed interest due to the effect of the derivative. In other words, E receives variable interest from the combination of the loan and the swap, which means that E has eliminated the risk of changes in fair value (hedging strategy). This applies under the presumption that hedge effectiveness is 100%, i.e. if fair value of the loan decreases (increases) by CU 5, fair value of the derivative improves (deteriorates) by CU 5. If E measures the loan at amortized cost (i.e. according to the effective interest method), an increase in fair value above amortized cost must not be recognized in E's financial statements. Only decreases in fair value attributable to the debtor's credit risk (impairment losses) are recognized by E. By contrast, the interest rate swap has to be measured at fair value through profit or loss (IFRS 9.4.2.1(a) and IFRS 9.B4.1.9). Consequently, E has to recognize all changes in fair value of the swap in profit or loss. For example, if fair value of the loan increases by CU 5 above amortized cost, E must not recognize this increase in its financial statements. However, the corresponding deterioration of CU 5 in the fair value of the derivative has to be recognized. This results in an incorrect illustration of the hedging relationship in E's financial statements (inconsistency or accounting mismatch) because the loan and the derivative are measured on different bases, after recognition.

Example 2: Entity E is the creditor of a variable interest rate loan, which is measured at amortized cost. An increase (a reduction) in the market interest rate leads to an increase (a reduction) in the interest payments that E receives on the loan. Assume that E intends to hedge the risk of changes in interest payments. Hence, E enters into an interest rate swap (derivative) under which E receives fixed interest and pays variable interest. This means that in essence, E receives fixed interest on the loan instead of variable interest due to the effect of the derivative. In other words, E receives fixed interest from the combination of the loan and the swap, which means that E has eliminated the risk of changes in cash flows (hedging strategy). This applies under the presumption that hedge effectiveness is 100%. In this situation, applying the general requirements of IFRS 9 results in an inconsistency (accounting mismatch): the interest rate swap has to be measured at fair value through profit or loss (IFRS 9.4.2.1(a) and IFRS 9.B4.1.9). Consequently, E has to recognize all changes in fair value of the swap (present value of the future interest payments arising under the swap) in profit or loss. However, the future cash flows (i.e. the future interest payments) arising on the loan measured at amortized cost that are hedged must not be recognized by E (because they have not yet occurred). Consequently, an inconsistency arises because the hedging derivative affects E's financial statements, whereas the hedged position does not.

In order to avoid such inconsistencies, an entity may – under certain circumstances – (see Section 2.7.2) depart from the general requirements of IFRS 9 and apply the hedge accounting rules of IAS 39 (IFRS 9.5.2.3 and 9.5.3.2). Basically, there are two different types of hedge accounting:

- In the case of a fair value hedge, the accounting treatment of the hedged item (e.g. of the loan of a creditor) is changed so that the inconsistency is eliminated. This means that the hedged item is measured at fair value (with respect to the hedged risk) through profit or loss (which corresponds to the accounting treatment of the hedging derivative) instead of being measured at amortized cost. Thus, the effect of the changes in fair value of the hedged item and of the hedging derivative on profit or loss is zero (if hedge effectiveness is 100%). Consequently, reality is correctly portrayed in the financial statements, meaning the false presentation of results is avoided. In Example 1, application of the concept of fair value hedge would mean that changes in fair value of the loan (caused by changes in market interest rates) would also be recognized in profit or loss. For example, if fair value of the loan increases by CU 5 above amortized cost, this increase would be recognized in profit or loss. The corresponding deterioration of CU 5 in the fair value of the derivative would also be recognized in profit or loss. This results in a correct illustration of reality in E's financial statements.

- In the case of a cash flow hedge, the accounting treatment of the hedging derivative is changed. This means that the hedging derivative is measured at fair value through other comprehensive income instead of being measured at fair value through profit or loss. Thus, the effect of the hedging relationship on profit or loss is zero (if hedge effectiveness is 100%). This is because the future cash flows arising on the hedged item are not recognized by E (because they did not yet occur) and the fair value changes of the hedging derivative are generally recognized in other comprehensive income. This means that neither the future cash flows arising on the hedged item nor the hedging instrument affect profit or loss. Consequently, there is no inconsistency with regard to profit or loss. However, applying cash flow hedge accounting does not eliminate all inconsistencies in the financial statements because the fair value changes of the hedging derivative affect other comprehensive income (and consequently also equity), whereas the hedged future cash flows do not. These considerations can be applied to Example 2.

2.7.2 The Rules in More Detail

As illustrated above, there may be different types of hedging strategies which are implemented in practice. In order to avoid inconsistencies, the hedge accounting rules allow an entity to depart from the general requirements of IFRS 9 if certain criteria are met (see next) in order to correctly present reality in the financial statements.

If a transaction, which has already been recognized in the financial statements, is hedged (e.g. a bond acquired by the entity), fair value hedge accounting (e.g. if a fixed interest rate loan is hedged against the risk of fair value changes with an interest rate swap) or cash flow hedge accounting (e.g. if a variable interest rate loan is hedged against the risk of changes in future interest payments with an interest rate swap) may be applied. Also a firm commitment can be hedged. A firm commitment is a binding agreement for the exchange of a specified quantity of resources on a specified future date or dates at a specified price (IAS 39.9). For example, entity E may enter into a contract in Nov 01 for the purchase of 10 tons of a specified raw material for 1 million CAD, which will be delivered on Feb 01, 02. On Dec 31, 01 (E's end of the reporting period 01) this transaction is a firm commitment. Generally, a hedge of a firm commitment is accounted for as a fair value hedge. However, a hedge of the foreign currency risk of a firm commitment may be also be accounted for as a cash flow hedge (IAS 39.87). A forecast transaction is an uncommitted but anticipated future transaction (IAS 39.9). In contrast to a firm commitment, no contract has been entered into in the current reporting period. Hedges of forecast transactions may only be accounted for as cash flow hedges.

Hedge accounting can only be applied if restrictive criteria are met. For example, hedge accounting can only be applied if the hedging instrument is a derivative. An exception to this rule only applies in the case of a hedge of the risk of changes in foreign currency exchange rates (IAS 39.9 and 39.72).

In addition to further restrictions, it is necessary that all of the following conditions are met (IAS 39.88):

- Documentation of the hedging relationship.

- Hedge effectiveness has to be demonstrated on a retrospective basis (i.e. relating to the past) as well as on a prospective basis (i.e. effectiveness is expected for the future).

- For cash flow hedges, the occurrence of a forecast transaction must be highly probable.

In some hedging relationships, hedge effectiveness is not 100%. For example, fair value of the hedging instrument may improve by CU 96 if fair value of the hedged item deteriorates by CU 100 due to the hedged risk. In this case, the changes are within the boundaries of 80% and 125%, prescribed by IAS 39,11 which means that continuing hedge accounting is possible (96 : 100 = 96% and 100 : 96 = 104.17%), although the changes in value are not compensated by each other in full.

In the case of hedging relationships that are effective within the meaning of IAS 39, any ineffectiveness is treated as follows:

- In the case of a fair value hedge, the fair value changes of the hedging derivative and the fair value changes of the hedged item that are attributable to the hedged risk are recognized in profit or loss. Due to this procedure, any ineffectiveness is automatically recognized in profit or loss.

- In the case of a cash flow hedge, the hedged future cash flows (IAS 39.AG103) are not recognized in the financial statements in the current reporting period. The hedging derivative is measured at fair value through other comprehensive income. The last principle has to be stated more precisely (IAS 39.95–39.96):

- First, the carrying amount of the hedging derivative is adjusted to fair value.

- The separate component of equity (i.e. the amount of other comprehensive income accumulated in equity) relating to the hedging relationship at the balance sheet date is always the lower of the following amounts:

- The cumulative gain or loss on the hedging derivative from inception of the hedge.

- The cumulative change in fair value (present value) of the expected future cash flows on the hedged item from inception of the hedge.

- After the change in the carrying amount of the hedging derivative and the appropriate amount of other comprehensive income have been recognized, the amount that has to be recognized in profit or loss is the remaining amount.

In the case of cash flow hedge accounting, there are two possibilities for the subsequent accounting treatment of the separate component of equity (hedging reserve) (i.e. the amount of other comprehensive income accumulated in equity):

If the forecast transaction subsequently results in the recognition of a non-financial asset (e.g. a machine or raw materials) or a non-financial liability, or a forecast transaction for a non-financial asset or non-financial liability becomes a firm commitment for which fair value hedge accounting is applied, then the entity applies either (a) or (b) above. In all other cases, alternative (a) is mandatory (IAS 39.97–39.100).

Among others, the entity has to discontinue hedge accounting prospectively if the criteria for applying hedge accounting (IAS 39.88 – see above) are no longer met. Moreover, an entity may discontinue hedge accounting voluntarily by revoking the designation (IAS 39.91 and 39.101).

2.8 Examples with solutions

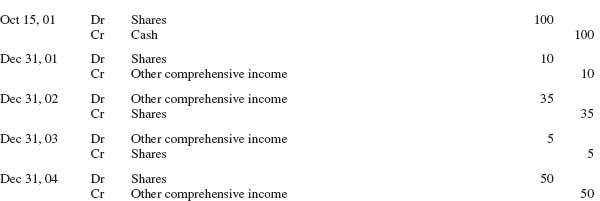

| Dec 31, 01 | 110 |

| Dec 31, 02 | 75 |

| Dec 31, 03 | 70 |

| Dec 31, 04 | 120 |

| Dec 31, 01 | 97 |

| Dec 31, 02 | 90 |

| Dec 31, 03 | 85 |

| Date | Cash inflow (+) and cash outflows (–) | Effective interest rate |

| Jan 01, 01 | 100 | 7.9% |

| Dec 31, 01 | −56 | |

| Dec 31, 02 | −56 |

| Date | Cash inflows (+) and cash outflow (–) | Effective interest rate |

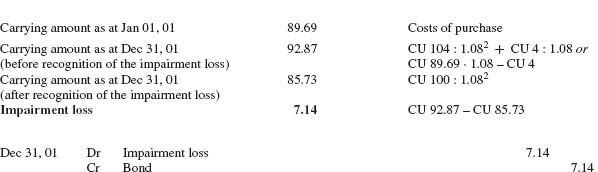

| Jan 01 01 | −89.69 | 8.0% |

| Dec 31, 01 | –4.00 | |

| Dec 31, 02 | –4.00 | |

| Dec 31, 03 | 104.00 |

| Nov 30, 03 | 10 |

| Dec 31, 03 | 8 |

| Mar 31, 04 | 9 |

| Nov 30, 03 | 10 |

| Dec 31, 03 | 8 |

| Mar 31, 04 | 9 |

3 FINANCIAL INSTRUMENTS ACCOUNTING PRIOR TO IFRS 9

This section generally describes financial instruments accounting prior to IFRS 9 only to the extent that it differs from IFRS 9 as issued in October 2010 (and its consequential amendments to IAS 39). Subsequently, references to IAS 39 refer to the “old” version of that Standard, i.e. to IAS 39 before any consequential amendments resulting from IFRS 9.

3.1 Scope18

IAS 39 sets out the requirements for recognizing and measuring financial instruments. However, the scope of IAS 39 does not include all financial instruments. For example, equity instruments are not within the scope of IAS 39 from the issuer's perspective. In the holder's consolidated financial statements, equity instruments are not in the scope of IAS 39 if they are interests in subsidiaries, joint ventures or associates (IAS 39.2).

3.2 Subsequent Measurement

IAS 39 is based on a mixed measurement model in which some financial assets and financial liabilities are measured at fair value and others at amortized cost after recognition. The method of subsequent measurement depends on the measurement category to which the financial asset or financial liability is assigned.

3.2.1 Assigning a Financial Asset or a Financial Liability to a Measurement Category

Loans and receivables This category comprises non-derivative financial assets with fixed or determinable payments that are not quoted in an active market (IAS 39.9). An active market is a market that meets all the following conditions (IAS 36.6):

- The items traded within the market are homogeneous.

- Willing buyers and sellers can normally be found at any time.

- Prices are available to the public.

Held-to-maturity investments This category includes non-derivative financial assets with fixed or determinable payments and fixed maturity. However, they have to be quoted in an active market (e.g. bonds quoted on the stock exchange). Moreover, classification into this category requires that the entity has the positive intention and ability to hold the financial assets to maturity.

In the case of sales of financial assets classified as “held to maturity” that do not meet specified conditions, the entity must not classify any financial assets into this category for a specified period of time. Moreover, any remaining financial assets of the category “held to maturity” have to be reclassified into the category “available for sale” (IAS 39.9 and 39.52).

Financial assets available for sale Available-for-sale financial assets represent primarily a residual category: All financial assets not falling into one of the other categories belong to this category (IAS 39.9).

Financial assets or financial liabilities at fair value through profit or loss This category includes financial assets as well as financial liabilities and consists of two sub-categories (“held for trading” and “fair value option”).

- Financial assets or financial liabilities that meet the definition of “held for trading.” The terms “held for trading” and “derivative” have the same meaning as in IFRS 9 (IFRS 9. Appendix A).19

- Financial assets or financial liabilities for which the fair value option is exercised (i.e. which are designated as at fair value through profit or loss). Exercising that option is possible if one of the following conditions (which correspond with the eligibility criteria for financial liabilities according to IFRS 920) is met and the asset's or liability's fair value can be determined reliably (IAS 39.9 and 39.11 A):

- Exercising the option eliminates or significantly reduces an inconsistency (accounting mismatch). For example, an entity may own a fixed-interest bond (classified as “available for sale”) that is refinanced by a fixed-interest financial liability (measured at amortized cost). Without exercising the option, fair value changes of the bond due to changes in the market interest rate would be recognized outside profit or loss and fair value changes of the financial liability due to changes in the market interest rate would not be recognized at all. Exercising of the option eliminates this inconsistency by recognizing the fair value changes of the asset as well as the fair value changes of the liability in profit or loss.

- A group of financial assets, financial liabilities or both is managed and its performance is evaluated on a fair value basis according to a documented risk management or investment strategy and information about that group is provided internally on that basis to the entity's key management personnel.

- Under certain circumstances (IAS 39.11 A), a contract that contains at least one embedded derivative (hybrid or combined instrument) may be designated as at fair value through profit or loss.

Financial liabilities measured at amortized cost Normally, financial liabilities are measured at amortized cost, i.e. according to the effective interest method.21 Exceptions to this rule are, among others, financial liabilities at fair value through profit or loss (see previous) and financial guarantee contracts (IAS 39.47).

3.2.2 Gains and Losses and Technical Aspects

Loans and receivables, held-to-maturity investments, and most financial liabilities are measured at amortized cost, i.e. according to the effective interest method (IAS 39.9 and 39.46–39.47).22

Available-for-sale financial assets are measured at fair value. Changes in fair value are generally recognized in other comprehensive income and accumulated in a separate component of equity (fair value reserve). However, in the case of debt instruments of this category, interest is first calculated using the effective interest method and recognized in profit or loss. Only the change in the difference between amortized cost calculated according to the effective interest method and fair value is recognized in other comprehensive income. Impairment losses arising from available-for-sale financial assets are recognized in profit or loss. When the financial asset is derecognized, the cumulative gain or loss previously recognized in other comprehensive income is reclassified to profit or loss. Impairment losses also lead to the derecognition of amounts previously recognized in other comprehensive income (IAS 39.46, IAS 39.55b, IAS 1.7, and 1.95).23

Financial assets and financial liabilities held for trading or for which the fair value option has been exercised are measured at their fair values. Changes in fair value are recognized in profit or loss (IAS 39.46–39.47 and 39.55a).

3.2.3 Determining Fair Values After Recognition

For debt instruments, there is an irrefutable presumption that fair value can be measured reliably. By contrast, for equity instruments that do not have a quoted market price in an active market, there is a presumption which can be rebutted in certain cases that fair value can be measured reliably. If the presumption is rebutted in the case of equity instruments, they are measured at cost, less any impairment losses. There are also exceptions from fair value measurement for derivatives under certain circumstances (IAS 39.46, 39.66, and 39.AG80–39.AG81).

3.2.4 Impairment Losses and Reversals of Impairment Losses

Financial assets at fair value through profit or loss are not tested for impairment because their fair value changes are recognized in profit or loss. However, all other financial assets are subject to review for impairment (IAS 39.46). This means that it has to be assessed at the end of each reporting period whether there is any objective evidence of impairment (loss events) (IAS 39.58).

IAS 39 includes a list of examples of loss events that relate to financial difficulties of the debtor (e.g. it becoming probable that the borrower will enter bankruptcy) (IAS 39.59).

In the case of equity instruments (e.g. shares), a significant or prolonged decline in fair value below cost is also objective evidence of impairment (IAS 39.61). We believe that it is appropriate to interpret the terms “significant” and “prolonged” as follows:

- A decline is prolonged if the market price of equity instruments – which are quoted in an active market – remains below cost for more than nine months. This criterion of nine months has to be applied retrospectively from the end of the reporting period.

- A decline is significant if the market price of equity instruments is at least 20% below cost. This applies irrespective of the change in value in a certain period of time before or after the end of the reporting period.

It is important to note that IAS 39.61 uses cost as reference point and not the carrying amount as at the end of the previous reporting period.

Three categories of financial assets have to be distinguished with regard to the calculation and accounting treatment of impairment losses and reversals of impairment losses.

Financial assets carried at amortized cost (i.e. loans and receivables as well as held-to-maturity investments)24 The procedure is the same as for financial assets measured at amortized cost according to IFRS 9.25

Financial assets carried at cost If there is objective evidence that an equity instrument carried at cost instead of fair value (because its fair value cannot be reliably measured26) is impaired, the following amounts have to be compared (IAS 39.66):

- Carrying amount of the instrument.

- Present value of the estimated future cash flows discounted at the current market rate of return for a similar financial asset.

If present value is below the instrument's carrying amount, an impairment loss is recognized. In this category, impairment losses must not be reversed (IAS 39.66).

Available-for-sale financial assets If an equity instrument classified as “available for sale” is impaired for the first time, the following applies (IAS 39.67–39.68):

- The cumulative amount previously recognized in other comprehensive income (i.e. the fair value reserve) is derecognized.

- The asset's carrying amount is reduced to fair value.

- An impairment loss (being the difference between cost and fair value) is recognized in profit or loss.

Reversals of impairment losses for equity instruments classified as “available for sale” are recognized in other comprehensive income (IAS 39.69).

3.3 Hybrid Contracts

According to the old version of IAS 39 the separation rules that apply to hybrid contracts with financial liability hosts under IFRS 927 applied to both hybrid contracts with financial asset hosts and hybrid contracts with financial liability hosts.

3.4 Examples with Solutions

1 The terms “financial instrument,” “financial asset,” “financial liability,” and “equity instrument” are defined in IAS 32.11 (see the chapter on IAS 32, Section 1 and Example 1).

2 See Sections 2.3.3 and 2.3.4.

3 Example 1 in Section 2.7.1 illustrates an accounting mismatch.

4 See Section 2.6.

5 See Section 2.3.1.

6 See Section 2.3.3.

7 See Section 2.3.4.

8 See the chapter on IAS 32, Section 3

9 See Section 2.3.4.

10 See Sections 2.3.3 and 2.3.4.

11 The boundaries of 80% and 125% apply when testing hedge effectiveness on a prospective, as well as on a retrospective basis (IAS 39.BC136–39.BC137).

12 The effective interest rate is calculated by applying the formula “IRR” in the English version of Excel to the payments shown below.

13 The effective interest rate is calculated by applying the formula “IRR” in the English version of Excel to the payments shown below.

14 In this example the exchange rates are presented as “1 unit of foreign currency F = x CNY” (e.g. 1 unit of F = 10 CNY).

15 For simplification purposes, differences between the spot exchange rate and the forward exchange rate are ignored in this example.

16 In this example the exchange rates are presented as “1 unit of foreign currency F = x CNY” (e.g. 1 unit of F = 10 CNY).

17 For simplification purposes, differences between the spot exchange rate and the forward exchange rate are ignored in this example.

18 The terms “financial instrument,” “financial asset,” “financial liability,” and “equity instrument” are defined in IAS 32.11 (see the chapter on IAS 32, Section 1 and Example 1).

19 See Section 2.3.1.

20 See Section 2.3.4.

21 See Section 2.3.5 with regard to the effective interest method.

22 See Section 2.3.5 with regard to the effective interest method.

23 Impairment losses and reversals of impairment losses from available-for-sale financial assets are discussed in Section 3.2.4 in more detail.

24 See Sections 3.2.1 and 3.2.2.

25 See Section 2.3.8.

26 See Section 3.2.3.

27 See Section 2.4.3.