IAS 16 PROPERTY, PLANT, AND EQUIPMENT

1 INTRODUCTION

Property, plant, and equipment are tangible items that meet both of the following criteria (IAS 16.6):

- They are held for use in the production or supply of goods or services, for rental to others, or for administrative purposes.

- They are expected to be used during more than one period.

Typical examples of property, plant, and equipment are buildings used in the production of goods or for administrative purposes.

IAS 16 does not apply, for example, to property, plant, and equipment classified as “held for sale” in accordance with IFRS 5 (IAS 16.3), and IAS 40 contains specific requirements for investment property.

2 RECOGNITION

The cost of an item of property, plant, and equipment is recognized as an asset if both of the following conditions are met (recognition principle) (IAS 16.7):

- It is probable that future economic benefits associated with the item will flow to the entity.

- The cost of the item can be measured reliably.

Whether these criteria are met for the initial and subsequent costs of a particular item of property, plant, and equipment is a question of recognition. All property, plant, and equipment costs are assessed according to the recognition principle at the time they are incurred (IAS 16.7 and 16.10).

Subsequent costs incurred in order to add to, replace part of, or service an item of property, plant, and equipment are generally recognized in the carrying amount of the item if they increase the economic benefits of the item (e.g. by an extension of the remaining useful life or by an increase in capacity). Parts of some items of property, plant, and equipment may have to be replaced. For example, aircraft interiors such as seats and galleys may require replacement several times during the life of the airframe (IAS 16.13). The costs of replacing parts are recognized in the carrying amount of the item of property, plant, and equipment if the recognition criteria (IAS 16.7) are met. The carrying amounts of replaced parts are derecognized according to the derecognition provisions of IAS 16 (IAS 16.67–16.72)1 (IAS 16.13). In the case of regular major inspections of items of property, plant, and equipment for faults, the cost of the inspection is recognized in the carrying amount of the item of property, plant, and equipment as a replacement if the recognition criteria are met. Any remaining carrying amount of the cost of the previous inspection is derecognized (IAS 16.14).

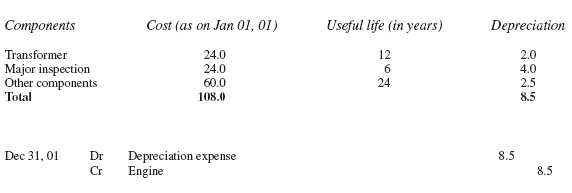

IAS 16 does not prescribe what constitutes an item of property, plant, and equipment. Consequently, judgment is required to determine the unit of measure for recognition. It may be appropriate to aggregate items that are individually insignificant such as molds, tools, and ties and to apply the recognition criteria to the aggregate value (IAS 16.9). In another example, a railroad company could regard an entire engine as a single item of property, plant, and equipment. Alternatively, each of the individual components of the engine (i.e. pivot mounting with wheel sets, the engine box, the transformer, the electric power converter, the control units, and the auxiliary converter) could be regarded as separate items of property, plant, and equipment. However, if the entire locomotive were defined as a single item of property, plant, and equipment, it would be necessary to depreciate the individually significant components separately (component accounting – see Section 4.2.4).

3 MEASUREMENT AT RECOGNITION

An item of property, plant, and equipment that qualifies for recognition as an asset is initially measured at its costs of purchase or conversion (IAS 16.15).

The costs of purchase comprise the following elements (IAS 16.16–16.21):

- The purchase price after deducting trade discounts and rebates. Import duties and nonrefundable purchase taxes are included, whereas refundable purchase taxes are excluded.

- Acquisition-related costs, i.e. any costs directly attributable to bringing the asset to the location and condition necessary for it to be capable of operating in the manner intended by the buyer.

- The initial estimate of the costs of dismantling and removing the item and restoring the site on which it is located to the extent that the entity incurs the obligation for them either when the item is acquired or as a consequence of having used the item during a particular period for purposes other than to produce inventories. By contrast, costs of these obligations that are incurred as a consequence of having used the item during a particular period to produce inventories are included in the costs of conversion of the inventories according to IAS 2 (IAS 16.16c, 16.18, and 16.BC15). These costs are normally included on the basis of their present value (IAS 16.18 and IAS 37.45).

The costs of conversion of an item of property, plant, and equipment are calculated according to the same principles that apply to property, plant, and equipment that was purchased. With regard to the determination of the costs of conversion of property, plant, and equipment, the Standard refers to the rules that apply for the calculation of the costs of conversion of inventories (IAS 16.22).

Criteria for the capitalization of borrowing costs are established in IAS 23. The initial measurement of items of property, plant, and equipment leased under a finance lease is dealt with in IAS 17 (IAS 16.27 and IAS 17.20). Government grants are dealt with in IAS 20 (IAS 16.28 and IAS 20.24).

4 MEASUREMENT AFTER RECOGNITION

4.1 Cost Model and Revaluation Model

After recognition, items of property, plant, and equipment have to be measured according to the cost model or according to the revaluation model. A choice between these models can be made for each entire class of property, plant, and equipment (IAS 16.29 and 16.36).

When the cost model is applied, the items of property, plant, and equipment are measured at their costs of purchase or conversion less any accumulated depreciation and accumulated impairment losses (IAS 16.30).

When the revaluation model is applied, the items of property, plant, and equipment are measured at their fair values at the time of the revaluation, less subsequent accumulated depreciation and impairment losses (IAS 16.31). Fair value is the amount for which an asset could be exchanged between knowledgeable, willing parties in an arm's length transaction (IAS 16.6).

In many countries, revaluations of property, plant, and equipment are rare and if and when they do occur, they are often revaluations of land.2 Thus, only the revaluation of land, which is not depreciated, is described. In this case the changes in value are recognized in other comprehensive income to the extent that the changes in value take place above cost. For example, if the value increases from CU 100 to CU 140 and cost is CU 110, CU 30 are recognized in other comprehensive income (ignoring deferred tax in this example). The amounts recognized in other comprehensive income are accumulated in revaluation surplus. However, the changes in value are recognized in profit or loss to the extent that they take place below cost (IAS 1.7, 1.106d, 1.108, IAS 16.39–16.40, IAS 36.60–36.61, and 36.118–36.120). When a revaluation above cost is not permitted for tax purposes, an increase in fair value above cost leads to the recognition of a deferred tax liability (Dr Revaluation surplus, Cr Deferred tax liability) (IAS 12.61A–12.62). Upon derecognition of the land, the revaluation surplus may be transferred directly to retained earnings (i.e. not through profit or loss). However, it is also possible not to make any transfer at all (IAS 1.96 and IAS 16.41).

4.2 Depreciation

4.2.1 Depreciable Amount

The depreciable amount is the costs of purchase or conversion of an asset (or other amount substituted for cost) less its residual value (IAS 16.6). The “other amount substituted for cost” can be, for instance, the new carrying amount of the asset after a revaluation.

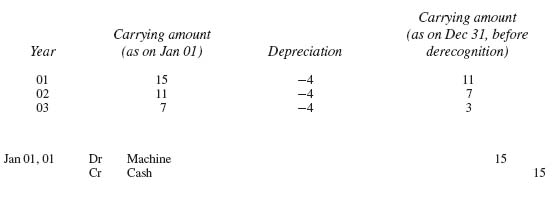

The residual value is the estimated amount that an entity would currently obtain from disposal of the asset after deduction of the estimated costs of disposal if the asset were already of the age and in the condition expected at the end of its useful life (IAS 16.6). In practice, the residual value of an asset is often insignificant. Consequently it is often possible not to deduct it in determining depreciable amount due to materiality reasons (IAS 16.53 and IAS 8.8). However, it is important to deduct residual value, especially when assets are replaced far ahead of the end of their physical life (e.g. for economic reasons or due to technological progress). This may be the case with aircrafts, ships or trucks. The residual value may increase to an amount equal to or greater than the asset's carrying amount. In this case, depreciation is zero unless and until the residual value subsequently decreases to an amount below the carrying amount of the asset (IAS 16.54). The residual value of an asset has to be reviewed at least at the end of each financial year. If expectations differ from previous estimates, the change has to be treated as a change in accounting estimates according to IAS 8 (IAS 16.51).

4.2.2 Depreciation Period

The depreciable amount has to be allocated on a systematic basis over the useful life of the asset (IAS 16.50). An asset's useful life is (IAS 16.6):

- the period over which the asset is expected to be available for use by an entity, or

- the number of production or similar units expected to be obtained from the asset by an entity.

Useful life is defined in terms of the asset's expected utility to the entity. Under the entity's asset management policy, assets may be disposed of after a specified time or after consumption of a specified proportion of the future economic benefits embodied in the asset. Thus, the useful life of an asset may be shorter than its economic life (IAS 16.57).

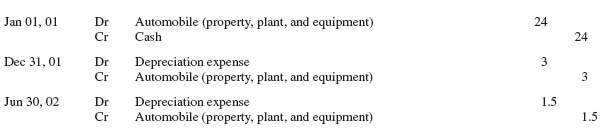

Depreciation starts when the asset is available for use, i.e. when it is in the location and condition necessary for it to be capable of operating in the manner intended by management (IAS 16.55). In many cases applying the concept of materiality (IAS 8.8) will justify calculating depreciation on a monthly and not on a daily basis.

Depreciation ceases at the earlier of the following dates (IAS 16.55):

- Date at which the asset is classified as held for sale (or included in a disposal group that is classified as held for sale) according to IFRS 5.

- Date of derecognition of the asset.

Consequently, depreciation continues to be recognized when the asset becomes idle or is retired from active use. However, under usage methods of depreciation, the depreciation charge can be zero while there is no production (IAS 16.55).

The useful life of an asset has to be reviewed at least at the end of each financial year. If expectations differ from previous estimates, the change has to be treated as a change in accounting estimates according to IAS 8 (IAS 16.51).

4.2.3 Depreciation Method

The depreciation method has to reflect the pattern in which the asset's future economic benefits are expected to be consumed by the entity (IAS 16.60).

Examples of depreciation methods are the straight-line method and the units of production method. In the former case, depreciation is calculated by dividing the depreciable amount by the asset's useful life. In the latter case, depreciation expense depends on the expected use or output of the asset (IAS 16.62).

It is necessary to select the depreciation method that most closely reflects the expected pattern of consumption of the future economic benefits embodied in the asset (IAS 16.62).

The depreciation method has to be reviewed at least at the end of each financial year. If there has been a significant change in the expected pattern of consumption of the future economic benefits embodied in the asset, the depreciation method has to be changed in order to reflect the changed pattern. Such a change has to be treated as a change in an accounting estimate according to IAS 8 (IAS 16.51).

4.2.4 Component Accounting

Each part, i.e. each component of an item of property, plant, and equipment, with a cost that is significant in relation to the total cost of the item has to be depreciated separately unless the useful lives are at least approximately identical (component accounting). Component accounting is also necessary for regular major inspections for faults (IAS 16.14 and 16.43–16.47).

Although individual components are depreciated separately as described above, the statement of financial position continues to disclose a single asset. Moreover, component accounting does not necessitate the splitting of depreciation expense in the statement of comprehensive income. The issue of derecognition of components is dealt with in Section 5.

4.3 Impairment

The issue of impairment is dealt with in the chapter on IAS 36 in this book (IAS 16.63).

4.4 Changes in Existing Decommissioning, Restoration, and Similar Liabilities

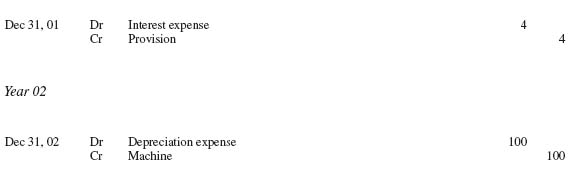

Changes in existing decommissioning, restoration, and similar liabilities for items of property, plant, and equipment accounted for according to the cost model are treated as follows (IFRIC 1):

- If the change in measurement is due to a change in the estimated timing or amount of the outflow of resources embodying economic benefits required to settle the obligation or due to a change in the discount rate, the following applies: Changes in the liability are added to or deducted from the carrying amount of the related asset (“Dr Asset Cr Liability” respectively “Dr Liability Cr Asset”). When this procedure leads to a reduction in the asset's carrying amount to zero, each further reduction in the liability is recognized in profit or loss. If the adjustment results in an increase in the carrying amount of the asset, it has to be considered whether this is an indication that the new carrying amount of the asset is impaired (see IAS 36). The adjusted depreciable amount of the asset is depreciated over the asset's remaining useful life. Once the asset has reached the end of its useful life, all subsequent changes in the liability are recognized in profit or loss.

- The periodic unwinding of the discount is recognized in profit or loss as a finance cost.

5 DERECOGNITION

An item of property, plant, and equipment is derecognized on disposal (e.g. by sale or by entering into a finance lease) or when no future economic benefits are expected from its use or disposal (IAS 16.67). The gain or loss arising from the derecognition of an asset is the difference between the net disposal proceeds (if any) and the asset's carrying amount (IAS 16.71).

If, under the recognition principle (IAS 16.7), the cost of a replacement for part of an item of property, plant, and equipment is recognized in the carrying amount of the item, then the carrying amount of the replaced part is derecognized. This applies regardless of whether the replaced part had been depreciated separately (IAS 16.70). The procedure described also applies to a major inspection that was recognized in the carrying amount of the item (see Sections 2 and 4.2.4) and has not been fully depreciated at the time of the next major inspection (IAS 16.14).

The intended sale of a single item of property, plant, and equipment does not lead to a transfer of the item to inventories because the intended sale of the item is not in the ordinary course of business. Therefore, a gain is recognized when the item is derecognized that must not be classified as revenue (IAS 2.6 and IAS 16.68). This gain is presented by deducting the carrying amount of the asset and related selling expenses from the disposal proceeds (IAS 1.34a and IAS 16.71). When the criteria in IFRS 5.6–5.12 are met, the item is classified as “held for sale” in accordance with IFRS 5. In this case the item is presented separately in the statement of financial position (balance sheet) and measured at the lower of its carrying amount and fair value less costs to sell (IFRS 5.15 and 5.37–5.38).

However, if an entity routinely sells items of property, plant, and equipment in the course of its ordinary activities that it has held for rental to others, it has to transfer these assets to inventories at their carrying amount when they cease to be rented and become held for sale. IFRS 5 is not applied. The proceeds from the sale of such assets is recognized as revenue in accordance with IAS 18 (IAS 16.68A).

6 EXAMPLES WITH SOLUTIONS

Reference to another section

With regard to the illustration of the effects of a revaluation of land in the statement of comprehensive income and in the statement of changes in equity we refer to the chapter on IAS 1 (Example 7).

| Costs of purchase | |

| Pivot mounting with wheel sets | 16 |

| Engine box | 19 |

| Transformer | 24 |

| Electric power converter | 13 |

| Control units | 18 |

| Auxiliary converter | 18 |

| Total | 108 |

| Costs of purchase | 15 |

| Residual value | 3 |

| Depreciable amount | 12 |

| Useful life (in years) | 3 |

| Depreciation p.a. | 4 |

| Depreciation 01 = | 12 · 3,000 : 12,000 = 3 |

| Depreciation 02 = | 12 · 5,000 : 12,000 = 5 |

| Depreciation 03 = | 12 · 4,000 : 12,000 = 4 |

| Total | 12 |

| Purchase price | 220 |

| Costs for disposing of the machine appropriately | 92.61 |

| Maturity (in years) | 3 |

| Discount rate (p.a.) | 5% |

| Present value of the obligation | 80 |

| Costs of purchase | 300 |

| Provision as on Dec 31, 02 (CU 92.61) | 88.20 | = CU 80 + CU 4 + CU 4.2 or CU 80 ·1.052 or CU 92.61 : 1.05 |

| Provision as on Dec 31, 02 (CU 63) | 60.00 | = CU 63 : 1.05 |

| Reduction of the provision | 28.20 |

| Dec 31, 01 | 44 |

| Dec 31, 02 | 36 |

| Dec 31, 03 | 48 |

| Carrying amount according to IFRS (as on Dec 31, 01) | 44 |

| Carrying amount according to the applicable tax law (as on Dec 31, 01) | 40 |

| Taxable temporary difference | 4 |

| Tax rate | 25% |

| Deferred tax liability | 1 |

| Carrying amount according to IFRS (as on Dec 31, 03) | 48 |

| Carrying amount according to the applicable tax law (as on Dec 31, 03) | 40 |

| Taxable temporary difference | 8 |

| Tax rate | 25% |

| Deferred tax liability | 2 |

1 See Section 5.

2 See Christensen/Nikolaev, Does fair value accounting for non-financial assets pass the market test?, working paper no. 09–12; ICAEW, EU implementation of IFRS and the fair value directive, a report for the European Commission, 2007, p. 119–120; KPMG/von Keitz, The Application of IFRS: Choices in Practice, 2006, p. 11.

3 See the chapter on IAS 2, Section 3.

4 See the chapter on IAS 12 regarding deferred tax.