IAS 12 INCOME TAXES

1 INTRODUCTION

The objective of IAS 12 is to prescribe the accounting treatment for income taxes. Income taxes include all domestic and foreign taxes which are based on taxable profits and also include taxes, such as withholding taxes, which are payable by a subsidiary, joint venture or associate on distributions to the reporting entity (IAS 12.2).

This chapter consists of two main areas:

- Accounting treatment of current tax, which is the amount of income taxes payable with respect to the taxable profit for the current period (see Section 2).

- Accounting treatment of deferred tax, i.e. of future tax advantages and disadvantages (see Section 3).

2 CURRENT TAX

The entity calculates the amount of current tax payable on the basis of taxable profit for the period (taxable profit · tax rate = current tax payable). Current tax for current and prior periods is, to the extent unpaid, recognized as a liability. If the amount already paid relating to current and prior periods exceeds the amount due for those periods, the excess is recognized as an asset (IAS 12.12).

Current tax liabilities (current tax assets) are measured at the amount expected to be paid to (recovered from) the taxation authorities on the basis of the tax rates (and tax laws) that have been enacted or substantively enacted by the end of the reporting period (IAS 12.46).

Current tax is normally recognized in profit or loss. However, to the extent that the tax arises from a transaction or event that is recognized outside profit or loss, i.e. either in other comprehensive income or directly in equity, the relating tax is recognized in the same way. Moreover, if the tax arises from a business combination, it is neither recognized in profit or loss, nor in other comprehensive income (IAS 12.58 and 12.61A).1

Current tax assets and current tax liabilities have to be offset if the entity has a legally enforceable right to set off the recognized amounts and intends either to settle on a net basis or to realize the asset and settle the liability simultaneously (IAS 12.71–12.73).

3 DEFERRED TAX

3.1 The Logic Behind Recognizing Deferred Tax

The recognition of deferred tax in the statement of financial position may be necessary with respect to temporary differences, the carryforward of unused tax losses, and the carryforward of unused tax credits.

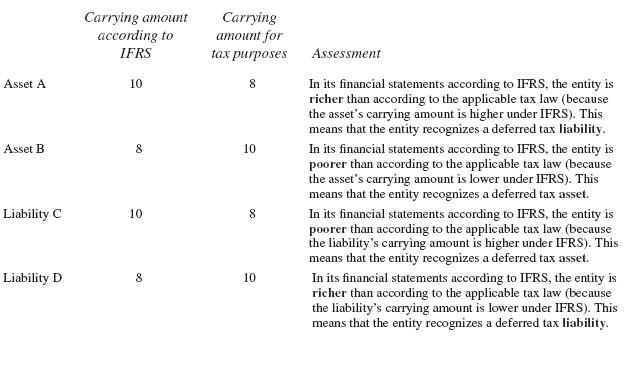

Temporary differences are differences between the carrying amount of an item for tax purposes (its tax base) and its carrying amount according to IFRS which will result in future tax advantages or disadvantages for the entity. Temporary differences resulting in future tax advantages are referred to as “deductible temporary differences,” whereas those resulting in future tax disadvantages are called “taxable temporary differences” (IAS 12.5). Temporary differences that meet the recognition criteria2 are multiplied by the tax rate and recognized as a deferred tax asset (if the difference represents a future tax advantage) or as a deferred tax liability (if the difference represents a future tax disadvantage).

Conceptionally, there is the presumption that the carrying amount for tax purposes will increase or decrease to the carrying amount according to IFRS in the future. It is assumed that the difference between these carrying amounts will affect taxable profit when the carrying amount of the asset or liability is recovered or settled. Assume that the carrying amount of a piece of land is CU 10 according to IFRS and CU 8 for tax purposes. A fictitious sale of the land for CU 10 (i.e. at the carrying amount according to IFRS) would result in a gain of CU 2 under the applicable tax law. Hence, the entity's taxable profit would increase by CU 2 and (assuming that the tax rate is 25%) current tax payable would increase by CU 0.5. This means that a sale in a future period would result in a tax disadvantage of CU 0.5 for the entity. Consequently, the entity recognizes this disadvantage of CU 0.5 as a deferred tax liability.

In practice, it would be time-consuming to perform a detailed analysis for each asset or liability as in the example above. Instead, application of a simplified rule is recommendable. An example is the “poorer-richer-rule” (poorer in the statement of financial position according to IFRS = asset; richer in the statement of financial position according to IFRS = liability), which is illustrated in the table below:

In the table previously the differences between the carrying amounts have to be multiplied by the tax rate. This results in the carrying amount of the deferred tax liability or deferred tax asset. It is important to note that recognition of deferred tax assets and deferred tax liabilities in the statement of financial position requires that the recognition criteria (see below) are met.

3.2 Recognition Criteria

3.2.1 Taxable Temporary Differences

Taxable temporary differences give rise to the recognition of a deferred tax liability. An important exception to this rule relates to goodwill. Deferred tax liabilities arising from the initial recognition of goodwill must not be recognized in the statement of financial position (IAS 12.15 and 12.21–12.21B).

3.2.2 Deductible Temporary Differences

A future tax advantage in the form of reductions in tax payments will flow to the entity only if it earns sufficient taxable profits against which the deductions can be offset (IAS 12.27). Hence, the Standard requires (with some exceptions) recognition of a deferred tax asset for all deductible temporary differences to the extent that it is probable that taxable profit will be available against which the deductible temporary difference can be utilized (IAS 12.24).

This criterion is met when there are sufficient taxable temporary differences relating to the same taxation authority and the same taxable entity which are expected to reverse (IAS 12.28)

- in the same period as the expected reversal of the deductible temporary difference, or

- in periods into which a tax loss arising from the deferred tax asset can be carried forward or back.

When there are insufficient taxable temporary differences, the deferred tax asset is recognized to the extent that (IAS 12.29):

- it is probable that the entity will have sufficient taxable profit relating to the same taxation authority and the same taxable entity in the same period as the reversal of the deductible temporary difference (or in the periods into which a tax loss arising from the deferred tax asset can be carried forward or back),3 or

- tax planning opportunities are available to the entity that will create taxable profit in appropriate periods (e.g. generating disposal gains on assets for tax purposes in a particular jurisdiction by sale and leaseback).

The existence of a history of recent losses is strong evidence that future taxable profit may not be available (IAS 12.31 and 12.35–12.36).

If the carrying amount of goodwill arising in a business combination is less than the amount that will be deductible for tax purposes with respect to goodwill, the difference gives rise to a deferred tax asset. The deferred tax asset arising from the initial recognition of goodwill is recognized as part of the accounting for a business combination to the extent that it is probable that taxable profit will be available against which the deductible temporary difference could be utilized (IAS 12.32A).

3.2.3 Unused Tax Losses and Unused Tax Credits

The recognition criteria for deferred tax assets arising from the carryforward of unused tax losses and tax credits are the same as those for deferred tax assets arising from deductible temporary differences (IAS 12.35).

3.2.4 Reassessment of Unrecognized Deferred Tax Assets

At the end of each reporting period, it is reassessed whether previously unrecognized deferred tax assets currently meet the recognition criteria. They are recognized to the extent that the recognition criteria are met, at the current balance sheet date. Examples of events that may result in such recognition in hindsight are a business combination or an improvement in trading conditions (IAS 12.37).

3.2.5 Outside Basis Differences vs. Inside Basis Differences

When a subsidiary, a jointly controlled entity or an associate is consolidated, proportionately consolidated or accounted for using the equity method, deferred tax is systematized as follows:

- Inside basis differences I: Differences between the carrying amounts of the investee's assets and liabilities according to IFRS and for tax purposes in the investee's statement of financial position.

- Inside basis differences II: Fair value adjustments initially arising on consolidation, proportionate consolidation or application of the equity method, which are not recognized according to the applicable tax law.

- Outside basis difference: A difference between the investment's carrying amount determined according to the equity method, consolidation or proportionate consolidation and its carrying amount for tax purposes.

A deferred tax liability is recognized for all taxable temporary outside basis differences except to the extent that both of the following criteria are met (IAS 12.39):

A deferred tax asset is recognized for all deductible temporary outside basis differences to the extent that it is probable that both of the following criteria are met (IAS 12.44):

3.3 Measurement

3.3.1 Applicable Tax Rates and Tax Laws

The measurement of deferred tax assets and liabilities is usually based on the tax rates and tax laws that have been enacted or substantively enacted by the end of the reporting period (IAS 12.47).

3.3.2 Manner of Recovery or Settlement of the Carrying Amount of an Asset or a Liability

In some jurisdictions, the manner in which an entity recovers (settles) the carrying amount of an asset (liability) may affect either or both of the following (IAS 12.51A):

- Tax rate applicable on recovery (settlement).

- Carrying amount of the asset (liability) for tax purposes.

In such cases, the deferred tax liabilities and deferred tax assets are measured using the tax rate and the tax base that are consistent with the expected manner of recovery or settlement (IAS 12.51–12.51A).

3.3.3 Prohibition of Discounting

The Standard prohibits discounting of deferred tax liabilities and assets (IAS 12.53).

3.3.4 Impairment and Reversal of Impairment

The carrying amount of a deferred tax asset has to be reviewed at the end of each reporting period. The carrying amount of a deferred tax asset is reduced to the extent that it is no longer probable that sufficient taxable profit will be available to allow the benefit of part or all of that deferred tax asset to be utilized (“impairment”). Any such reduction is reversed to the extent that it becomes probable that sufficient taxable profit will be available (reversal of “impairment”) (IAS 12.56).

3.4 Presentation

Deferred tax is recognized in profit or loss. However, there are exceptions to this rule (IAS 12.58 and 12.61A):

- Deferred tax is recognized in other comprehensive income if it relates to an item recognized in other comprehensive income.

- Deferred tax is recognized directly in equity, if it relates to an item recognized directly in equity.

- Moreover, if the deferred tax arises as part of the initial accounting of a business combination at acquisition date, it is neither recognized in profit or loss, nor in other comprehensive income.4

Deferred tax assets and deferred tax liabilities have to be offset, if both of the following criteria are met (IAS 12.74):

- the same taxable entity, or

- different taxable entities which intend (in each future period in which significant amounts of deferred tax assets or liabilities are expected to be settled or recovered) either to settle current tax liabilities and assets on a net basis, or to realize the assets and settle the liabilities simultaneously.

3.5 Specific Issues

3.5.1 Change in the Tax Rate

In the case of a change in the tax rate, the carrying amount of the deferred tax assets and liabilities changes even though there is no change in the amount of the related temporary differences. The adjustment of the carrying amount is recognized in profit or loss or outside profit or loss, depending on the manner of previous recognition (IAS 12.60).

3.5.2 Business Combinations

The accounting treatment of deferred tax relating to goodwill and fair value adjustments arising as part of the initial accounting of a business combination at acquisition date has been dealt with in the previous sections.

As a result of a business combination, the following situations may occur with respect to the acquirer's deferred tax assets (IAS 12.67):

- A previously unrecognized deferred tax asset of the acquirer has to be recognized.

- A previously recognized deferred tax asset of the acquirer does not meet the recognition criteria anymore.

In these cases, the acquirer recognizes a change in the deferred tax asset in the period of the business combination but does not include it as part of the accounting for the business combination. Therefore, the acquirer does not take it into account in determining goodwill (IAS 12.67).

An acquiree's income tax loss carryforwards or other deferred tax assets might not satisfy the criteria for separate recognition on initial accounting of a business combination. If the recognition criteria are met, subsequently, the following applies (IAS 12.68):

- Acquired deferred tax benefits recognized within the measurement period5 (IFRS 3.45) that result from new information about facts and circumstances that existed at the acquisition date reduce the carrying amount of any goodwill related to that acquisition (“Dr Deferred tax asset Cr Goodwill”). If the carrying amount of that goodwill is zero, any remaining deferred tax benefits are recognized in profit or loss (“Dr Deferred tax asset Cr Income”).

- All other acquired deferred tax benefits realized subsequently are recognized in profit or loss (“Dr Deferred tax asset Cr Income”), or, if IAS 12 so requires, outside profit or loss.

4 TAX (OR TAX RATE) RECONCILIATION

A tax (or tax rate) reconciliation has to be disclosed in the notes. Thereby, the product of profit before tax according to IFRS multiplied by the applicable tax rate is reconciled to the total of current and deferred tax expense (income). This reconciliation is presented either on an absolute number basis and/or percentage-wise. Percentage-wise means that the numbers are expressed as percentages of profit before tax according to IFRS (IAS 12.81c). The following example of a tax (rate) reconciliation takes only basic issues into account. The profit before tax according to IFRS and the applicable tax rate, as well as the expenses not deductible for tax purposes, are based on random numbers.

| Tax reconciliation in absolute numbers | |

| Profit before tax according to IFRS | 40 |

| Applicable tax rate | 25% |

| Fictitious tax (at the applicable tax rate) | 10 |

| Expenses not deductible for tax purposes | 2 |

| (Current and deferred) tax expense | 12 |

| Tax rate reconciliation | |

| Applicable tax rate | 25% |

| Expenses not deductible for tax purposes | 5% |

| Average effective tax rate | 30% |

5 EXAMPLES WITH SOLUTIONS

References to other chapters

Deferred tax arising in business combinations is also dealt with in the chapter on IFRS 3 (Examples 5 and 6b). Deferred tax arising in the case of revaluations of property, plant, and equipment is dealt with in the chapter on IAS 16 (Example 7). The effects of a retrospective adjustment on deferred tax are illustrated in the chapter on IAS 8 (Example 6).

- On Nov 01, 01, E acquired a machine for CU 120. The machine was available for use on the same day. E depreciates the machine on a monthly basis. However, under E's tax law, the machine has to be depreciated for six months in 01 because depreciation starts at the beginning of the half-year in which the machine is available for use. The machine's useful life is 10 years according to IFRS as well as for tax purposes.

- In 01, expenses of CU 8 were incurred for charitable donations. These are not deductible for tax purposes.

| Profit before tax according to IFRS | 100 | |

| Applicable tax rate | 25% | |

| Fictitious tax (at the applicable tax rate) | 25 | |

| Expenses not deductible for tax purposes | 2 | = 8 · 25% |

| (Current and deferred) tax expense | 27 | = 26 + 1 or 25 + 2 |

| Applicable tax rate | 25% | |

| Expenses not deductible for tax purposes | 2% | |

| Average effective tax rate | 27% |

| Profit before tax according to IFRS | 100 | |

| Applicable tax rate | 25% | |

| Fictitious tax (at the applicable tax rate) | 25 | |

| Expenses not deductible for tax purposes | 2 | = 8 · 25% (half of the compensation for non-executive directors) |

| Income outside the scope of taxation | −1 | = −4 · 25% (dividend) |

| (Current and deferred) tax expense | 26 | = 25 + 2 – 1 or current tax expense (35) less deferred tax income (9) |

| Applicable tax rate | 25% |

| Expenses not deductible for tax purposes | 2% |

| Income outside the scope of taxation | –1% |

| Average effective tax rate | 26% |

| Carrying amount according to IFRS as at Dec 31, 01 | 1,000 |

| Carrying amount for tax purposes as at Dec 31, 01 | 900 |

| Taxable temporary difference | 100 |

| Deferred tax liability as at Dec 31, 01 (on the basis of a tax rate of 30%) | 30 |

| Deferred tax liability as at Dec 31, 01 (on the basis of a tax rate of 25%) | 25 |

| Adjustment | −5 |

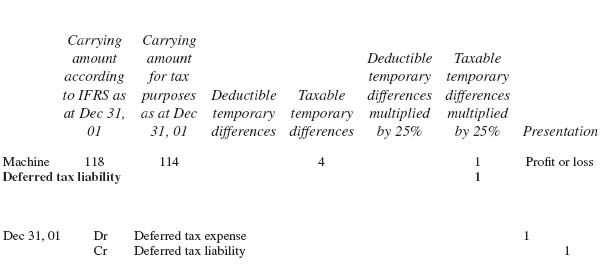

| Pro rata carrying amount of goodwill according to IFRS as at Dec 31, 01 | 60 |

| Carrying amount for tax purposes as at Dec 31, 01 | 56 |

| Taxable temporary difference | 4 |

| Tax rate | 25% |

| Deferred tax liability | 1 |

1 See the chapter on IFRS 3 regarding business combinations.

2 See Section 3.2.

3 Within the frame of this evaluation, taxable amounts arising from deductible temporary differences that are expected to originate in future periods are ignored because the deferred tax asset arising from these deductible temporary differences will itself require future taxable profit in order to be utilized (IAS 12.29).

4 See the chapter on IFRS 3, regarding business combinations.

5 See the chapter on IFRS 3, Section 6.7.

6 See Section 3.2.2.

7 See Section 3.1.

8 See Section 3.1.

9 If IFRS 9 were not yet applied, the same entry would be necessary if the shares were classified as “available for sale” (IAS 39.9).

10 See Section 3.2.2.

11 See Section 3.4.

12 The solution of this example would not change if IFRS 9 and its consequential amendments were not applied early and if the shares were classified as “available for sale” according to the “old” version of IAS 39 (IAS 39.9 and 39.55b).

13 The solution of this example would be the same if IFRS 9 (and its consequential amendments) were not applied early and if the shares of B were classified as “available for sale” (IAS 39.9 and 39.55b).

14 See the chapter on IFRS 3 with regard to the basics of business combinations.