IFRS 3 BUSINESS COMBINATIONS

1 INTRODUCTION AND SCOPE

In a business combination, an acquirer obtains control of one or more businesses. A business is an integrated set of activities and assets that is capable of being conducted and managed for the purpose of providing economic benefits (e.g. dividends) directly to investors, members or participants. Control is the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities (IFRS 3.Appendix A).

The acquisition of a group of assets or net assets, which do not constitute a business, is not a business combination (IFRS 3.3). In such a case, the cost of acquisition is allocated between the individual identifiable assets and liabilities on the basis of their relative fair values at the date of acquisition (IFRS 3.2b). Fair value is the amount for which an asset could be exchanged, or a liability settled, between knowledgeable, willing parties in an arm's length transaction (IFRS 3.Appendix A). The remaining part of this chapter on IFRS 3 only deals with business combinations.

IFRS 3 does not apply to a combination of entities or businesses under common control (IFRS 3.2c). This is a business combination in which all of the combining businesses or entities are ultimately controlled by the same party or parties both before and after the combination and the control is not transitory (IFRS 3.B1–3.B4). Such transactions often occur during the reorganization of groups.

Frequently, equity interests (i.e. in particular ownership interests of investor-owned entities) are acquired in a business combination. The term “owners” is defined along the same lines (IFRS 3.Appendix A).

2 ACQUISITION OF SHARES VS. ACQUISITION OF THE INDIVIDUAL ASSETS

In the case of an acquisition of shares in which the acquirer obtains control of the acquiree, the acquirer recognizes the shares in its separate financial statements and measures them either at cost or at fair value according to IFRS 9 in these statements (IAS 27.38). According to IFRS 9 there is an irrefutable presumption that fair value can always be determined reliably. However, in some situations cost may be an appropriate estimate of fair value (IFRS 9. B5.4.14–9.B5.4.17).1 In the case of an acquisition of shares, the acquisition method, which requires presentation of the individual assets and liabilities of the acquiree instead of the shares (IFRS 3.5), is only applied in the acquirer's consolidated financial statements.

By contrast, it may also be the case that the acquirer acquires the individual assets and assumes the individual liabilities of the acquiree instead of purchasing shares. In this case, IFRS 3 applies to the consolidated financial statements of the acquirer as well as to its separate financial statements (i.e. in both financial statements, the individual assets and liabilities of the acquiree are recognized).

3 IDENTIFYING THE ACQUIRER

The acquirer is the entity that obtains control of the acquiree (IFRS 3.Appendix A). For each business combination, one of the combining entities has to be identified as the acquirer (IFRS 3.6). In many situations, identification of the acquirer is straightforward. However, in some cases the business combination is a reverse acquisition. This means that the legal acquirer is the acquiree for financial reporting purposes according to the principle of “substance over form”2 (IFRS 3.B15 and 3.B19–B27).

4 ACQUISITION DATE

The acquisition date is the date on which the acquirer obtains control of the acquiree (IFRS 3.8). The acquisition date is determined according to the principle of “substance over form”3 (IFRS 3.9).

5 ACQUISITION-RELATED COSTS

Acquisition-related costs (e.g. external legal and advisory costs and the costs of maintaining an internal acquisitions department) are costs the acquirer incurs to carry through a business combination. These costs are accounted for as expenses in the periods in which the costs are incurred and the services are received. However, the costs to issue debt or equity instruments are recognized according to IAS 32 and IFRS 9 (IFRS 3.53).4

6 ACCOUNTING FOR A BUSINESS COMBINATION ON THE ACQUISITION DATE

6.1 Overview

On the acquisition date, the acquirer generally recognizes the assets (e.g. buildings, machines, intangible assets, and inventories) and liabilities (e.g. issued bonds, trade payables, and provisions) of the acquiree and measures them at their fair values. In a simple situation, in which 100% of another entity is acquired, the acquired net assets (assets less liabilities) are compared with the consideration transferred in order to acquire the acquiree. If the consideration transferred with regard to the acquisition exceeds the acquiree's net assets, goodwill is recognized in the statement of financial position.

These deliberations have to be extended when they are applied to situations in which, e.g. 80% (i.e. not 100%) of another entity (in which the acquirer previously did not hold any equity instruments) is acquired. In this case, the consideration paid only reflects 80% of the acquiree. However, 100% of the individual assets and liabilities of the acquiree have to be recognized. Consequently in the consolidated statement of financial position, a credit entry has to be made that reflects the interest in a subsidiary of the other shareholders (20%). This interest is called the non-controlling interest. It has to be presented as a component of equity, according to IFRS (IAS 27.27 and IAS 1.54q). More precisely, the non-controlling interest is the equity in a subsidiary not attributable, directly or indirectly, to a parent (IFRS 3.Appendix A).

When a non-controlling interest exists, the calculation of goodwill has to be modified because it would not be appropriate to compare the consideration for the acquisition of 80% of the acquiree with 100% of the acquiree's net assets. Therefore, IFRS 3 requires comparing the value of the entire acquiree (100%) determined according to IFRS 3 with the entire net assets of the acquiree (100%) measured according to IFRS 3. This results in the following formula: consideration transferred (for 80%) + carrying amount of the non-controlling interest determined in accordance with IFRS 3 (20%) – net assets (100%) = goodwill (if > 0). The non-controlling interest is generally measured either at its fair value or at its proportionate share in the recognized amounts of the acquiree's identifiable net assets (IFRS 3.19). In the former case, goodwill is recognized with respect to the non-controlling interest. In the latter case, no goodwill is recognized with regard to the non-controlling interest.

An acquirer may obtain control of an acquiree in which it held an equity interest immediately before the acquisition date. This is referred to as a business combination achieved in stages or as a step acquisition (IFRS 3.41).5 In this case the above formula for calculating goodwill has to be extended so that goodwill is increased by the previously held equity interest in the acquiree measured at its acquisition-date fair value.

The table below summarizes important aspects of the accounting for a business combination, which are described in more detail in the following sections (IFRS 3.32 and 3.19):

| Consideration transferred | The consideration transferred is generally measured at acquisition-date fair value. | |

| + | Non-controlling interest | The non-controlling interest is generally measured either at its fair value or at its proportionate share of the acquiree's identifiable net assets. |

| + | Previously held equity interest | The acquisition-date fair value of the acquirer's previously held equity interest in the acquiree. |

| = | Value of the acquiree (100%) | |

| − | Net assets acquired (100%) | The net of the acquisition-date amounts of the identifiable assets acquired and the liabilities assumed determined according to IFRS 3. |

| = | Goodwill | If > 0. |

6.2 Identifiable Assets Acquired and Liabilities Assumed

6.2.1 Recognition in the Statement of Financial Position

To qualify for recognition in a business combination, an item must meet the definition of an asset or a liability in the Conceptual Framework at the acquisition date (IFRS 3.11).6 There is an irrefutable assumption that the recognition criteria of the Conceptual Framework (i.e. reliability of measurement and probability of an inflow or outflow of benefits)7 are always satisfied.8 Hence, the probability of an inflow or outflow of future economic benefits is relevant only for determining fair value of the item (i.e. with regard to measurement).

An asset is identifiable if one of the following criteria is met. These criteria are particularly relevant for intangible assets (IFRS 3.Appendix A and 3.B31–3.B34).

- Separability criterion: The asset is separable, i.e. capable of being separated or divided from the entity and sold, transferred, rented, licensed or exchanged, either individually or together with a related contract, identifiable asset or liability, regardless of whether the entity intends to do so.

- Contractual-legal criterion: The asset arises from contractual or other legal rights, regardless of whether those rights are separable or transferable from the entity or from other rights and obligations.

In a business combination it may be necessary to recognize some assets and liabilities that the acquiree had not previously recognized as assets and liabilities in its financial statements (e.g. internally generated brands that could not be capitalized by the acquiree due to IAS 38.63) (IFRS 3.13).

The acquirer recognizes no assets or liabilities related to an operating lease in which the acquiree is the lessee. However, there are exceptions to this rule (IFRS 3.B28–3.B30):

- The acquirer recognizes an intangible asset if the terms of an operating lease are favorable relative to market terms and a liability if the terms are unfavorable relative to market terms.

- Other benefits may be associated with an operating lease, which may represent an identifiable intangible asset.

6.2.2 Classifications and Designations

At the acquisition date the acquirer has to classify or designate the identifiable assets acquired and liabilities assumed as necessary in order to apply other IFRSs after the acquisition date. These classifications or designations are made on the basis of the conditions as they are at the acquisition date (IFRS 3.15). An example of such a classification is the assignment of financial assets and financial liabilities as measured at amortized cost or at fair value for the purpose of measurement after recognition. An example of a designation is the designation of a derivative as a hedging instrument (IFRS 3.16).9

6.2.3 Measurement

The identifiable assets acquired and the liabilities assumed are measured by the acquirer at their acquisition-date fair values (IFRS 3.18). Fair value is the amount for which an asset could be exchanged or a liability settled between knowledgeable, willing parties in an arm's length transaction (IFRS 3.Appendix A). Fair value is an objective and not a subjective value. This means that fair value is determined under the presumption that the item will be used by the entity in a way in which other market participants would use it. This also applies when the acquirer intends not to use an acquired asset or intends to use the asset in a way that is different from the way in which other market participants would use it (IFRS 3.B43).

The determination of the fair value of a brand acquired in a business combination according to the “relief from royalty method” as well as the tax amortization benefit are illustrated in the chapter on IFRS 13.10

6.2.4 Exception to the Recognition Rules

The term “contingent liability” is defined in IAS 37.11 The requirements in IAS 37 do not apply in determining which contingent liabilities are recognized on acquisition date. Instead, a contingent liability assumed in a business combination is recognized at the acquisition date if there is a present obligation that arises from past events and its fair value can be determined reliably. This means that, contrary to IAS 37, the acquirer recognizes a contingent liability although it is not probable (i.e. it is not more likely than not) that an outflow of resources will be required to settle the obligation (IFRS 3.22–3.23).

6.2.5 Exceptions to the Recognition and Measurement Rules

Deferred tax assets or liabilities arising from the assets acquired and liabilities assumed in a business combination are recognized and measured by the acquirer in accordance with IAS 12 (IFRS 3.24). The potential tax effects of temporary differences and carryforwards of an acquiree that exist at the acquisition date or arise as a result of the acquisition are accounted for by the acquirer in accordance with IAS 12 (IFRS 3.25).12

As a result of the exception to the recognition and measurement rules with regard to IAS 12, deferred tax assets or liabilities recognized in a business combination are not measured at their acquisition-date fair values because IAS 12.53 prohibits discounting.

A liability (or asset, if any) related to the acquiree's employee benefit arrangements is recognized and measured by the acquirer in accordance with IAS 19 (IFRS 3.26).

6.2.6 Exception to the Measurement Rules

The acquirer measures an acquired non-current asset (or disposal group) that is classified as held for sale at the acquisition date according to IFRS 5 at fair value less costs to sell (in accordance with IFRS 5.15–5.18) (IFRS 3.31).

6.3 Non-controlling Interest

The non-controlling interest in the acquiree is generally measured on the acquisition date either at its fair value or at its proportionate share in the recognized amounts of the acquiree's identifiable net assets. Since this choice also affects the amount of goodwill recognized, it can be referred to as the full goodwill option. The full goodwill option may be exercised differently for each business combination (IFRS 3.19).

In the case of measurement of the non-controlling interest at its fair value, this value is determined on the basis of active market prices for the equity shares not held by the acquirer. When active market prices are not available, the acquirer uses other valuation techniques. The fair value of the acquirer's interest in the acquiree might differ from the fair value of the non-controlling interest on a per-share basis. The main reason is likely to be a control premium. This means that the acquirer might pay a significantly higher price for the acquisition of 51% of the shares (which allows him to exercise the majority of the voting rights) than for the acquisition of 49% of the shares (which does not allow him to exercise the majority of the voting rights) (IFRS 3.B44–3.B45).

6.4 Goodwill and Gain on a Bargain Purchase

Goodwill is the positive difference between the value of the acquiree and the net assets acquired, both determined according to IFRS 3.13 The acquirer subsumes into goodwill any value attributed to items that do not qualify for recognition as assets or liabilities by the acquirer at the acquisition date (IFRS 3.B37–3.B38).

Sometimes the value of the acquiree (determined according to IFRS 3) may exceed the net assets acquired (also determined according to IFRS 3). In these situations, the acquirer has to assess whether it has correctly identified all of the assets acquired and all of the liabilities assumed and whether they have been measured correctly. Moreover, it has to be assessed whether the consideration transferred, the non-controlling interest, and any previously held equity interest have been measured correctly. If the excess remains afterwards, the acquirer recognizes the resulting gain on the bargain purchase in profit or loss on the acquisition date. The gain has to be attributed to the acquirer (IFRS 3.34–3.36).

6.5 Business Combination Achieved in Stages

An acquirer may obtain control of an acquiree in which it held an equity interest immediately before the acquisition date (business combination achieved in stages or step acquisition) (IFRS 3.41). In this case, the formula for calculating goodwill has to be extended so that the goodwill is increased by the previously held equity interest in the acquiree measured at its acquisition-date fair value.14

If the equity instruments held by the acquirer before the business combination were investments accounted for using the equity method or investments measured at fair value through profit or loss according to IFRS 9, a gain or loss from the remeasurement of these equity instruments to fair value is recognized in profit or loss. However, if the previously held equity interest was measured at fair value through other comprehensive income (IFRS 9.5.7.1b and 9.5.7.5), a gain or loss resulting from remeasurement to fair value at the acquisition date is also included in other comprehensive income. Amounts recognized in other comprehensive income according to IFRS 9 are not transferred subsequently to profit or loss (IFRS 3.42 and IFRS 9.B5.7.1).15

6.6 Consideration Transferred (Including Contingent Consideration)

The consideration transferred in a business combination is generally measured at acquisition-date fair value, which is the sum of the fair values of (IFRS 3.37 and 3.32):

- the assets transferred by the acquirer,

- the liabilities incurred by the acquirer to former owners of the acquiree, and

- the equity interests issued by the acquirer.

When the consideration transferred includes assets or liabilities of the acquirer that have carrying amounts that differ from their fair values at the acquisition date, they are remeasured at their fair values as of the acquisition date. A gain or loss arising on remeasurement is recognized in profit or loss. However, sometimes the transferred assets or liabilities remain within the combined entity after the business combination (e.g. because the assets or liabilities were transferred to the acquiree rather than to its former owners), and consequently the acquirer retains control of them. In this situation the acquirer measures those assets and liabilities at their carrying amounts immediately before the acquisition date and does not adjust them to their fair values (IFRS 3.38).

Sometimes a business combination may be achieved without the transfer of consideration, e.g. in the following situations (IFRS 3.43):

- Minority veto rights lapse that previously kept the acquirer from controlling an acquiree in which the acquirer held the majority voting rights.16

- The acquirer previously held 49% of the voting rights of the acquiree that did not result in control. At a particular date, the acquiree repurchases some of its own shares from other shareholders. As a result, the acquirer now holds 51% of the voting rights, which means that it has obtained the majority of the voting rights and control.

In the examples described above, which also represent examples of business combinations achieved in stages, the value of the acquiree at the acquisition date (determined according to IFRS 3)17 is the sum of the carrying amount of the non-controlling interest and the acquisition-date fair value of the acquirer's previously held equity interest in the acquiree (IFRS 3.19, 3.32–3.33, and 3.41–3.42).

The consideration transferred by the acquirer in exchange for the acquiree includes any asset or liability resulting from a contingent consideration arrangement (IFRS 3.39). Contingent consideration is usually an obligation of the acquirer to transfer additional assets or equity interests to the former owners of the acquiree if specified future events occur or conditions are met. However, contingent consideration may also entitle the acquirer to the return of previously transferred consideration if specified conditions are met (IFRS 3.Appendix A).

The acquisition-date fair value of contingent consideration has to be recognized by the acquirer as part of the consideration transferred in exchange for the acquiree (IFRS 3.39). An obligation to pay contingent consideration has to be classified by the acquirer as a liability or as equity on the basis of the definitions of an equity instrument and a financial liability in IAS 32.11, or other applicable IFRSs. For those contingent consideration arrangements where the agreement gives the acquirer the right to the return of previously transferred consideration if specified future events or conditions are met, such a right has to be classified as an asset (IFRS 3.40).18

6.7 Measurement Period

If the initial accounting for a business combination is incomplete by the end of the reporting period in which the combination occurs, the acquirer's consolidated financial statements include provisional amounts for the items for which the accounting is incomplete. During the measurement period, the acquirer retrospectively adjusts these provisional amounts to reflect new information obtained about facts and circumstances that existed as of the acquisition date and, if known, would have affected the measurement of the amounts recognized as of that date. In the same way, it may be necessary to retrospectively recognize additional assets or liabilities (IFRS 3.45).

The measurement period ends when the acquirer receives the information it was seeking about facts and circumstances that existed as of the acquisition date or learns that more information is not obtainable. However, the measurement period must not exceed one year from the acquisition date (IFRS 3.45).

The acquirer has to determine whether information obtained after the acquisition date should lead to a retrospective adjustment to the provisional amounts recognized or whether that information results from events that occurred after the acquisition date (IFRS 3.47).

A retrospective adjustment of provisional carrying amounts of assets or liabilities within the measurement period is recognized by means of a decrease or increase in goodwill (IFRS 3.48). Thus, adjustments of the provisional amounts during the measurement period are effected as if the accounting for the business combination had been completed at the acquisition date. Consequently, comparative information (e.g. depreciation expense) for prior periods presented in the financial statements is also revised as needed (IFRS 3.49).

After the measurement period ends the accounting for a business combination is only revised in order to correct an error in accordance with IAS 8 (IFRS 3.50).

7 SUBSEQUENT MEASUREMENT AND ACCOUNTING

Assets acquired, liabilities assumed or incurred, and equity instruments issued in a business combination are generally subsequently measured and accounted for by the acquirer according to other applicable IFRSs for those items, depending on their nature. However, IFRS 3 contains specific guidance for particular items (IFRS 3.54). Some of these items are discussed below.

A contingent liability recognized in a business combination is measured by the acquirer after initial recognition and until it is settled, cancelled or expires at the higher of the following (IFRS 3.56):

- The amount that would be recognized according to IAS 37.

- The amount initially recognized less, if appropriate, cumulative amortization recognized according to IAS 18.

This requirement does not apply to contracts accounted for according to IFRS 9 (IFRS 3.56).

A change in the fair value of contingent consideration within the measurement period as the result of additional information that the acquirer obtained after the acquisition date about facts and circumstances that existed at the acquisition date results in a retrospective adjustment of goodwill. In addition, comparative information for prior periods presented is revised (IFRS 3.58 and 3.45–3.49).

Changes in fair value resulting from events after the acquisition date (e.g. meeting an earnings target, reaching a specified share price or reaching a milestone on a research and development project) are not measurement period adjustments. These changes are accounted for by the acquirer as follows (IFRS 3.58):

- Contingent consideration that represents equity is not remeasured and its subsequent settlement is accounted for within equity.

- If contingent consideration is classified as an asset or a liability, subsequent measurement and accounting depend on whether there is a financial instrument within the scope of IFRS 9.

- If this is the case, measurement is at fair value with any resulting gain or loss recognized either in profit or loss or in other comprehensive income in accordance with IFRS 9.

- If this is not the case, IAS 37 is applied or other IFRSs as appropriate.

After acquisition date, the carrying amount of the non-controlling interest is adjusted for the non-controlling interest's share of changes in equity since acquisition date (IAS 27.18c). Consequently, also changes in deferred tax that affect the acquiree's net assets have to be taken into account when measuring the non-controlling interest. Moreover, if the non-controlling interest has been measured at its fair value at acquisition date, its carrying amount has to be adjusted for the non-controlling interest's share of goodwill impairment losses.19

8 DEFERRED TAX

Regarding deferred tax, we refer to the chapter on IAS 12 and to Examples 5 and 6(b) in Section 11 of this chapter.

9 ENTRIES NECESSARY IN ORDER TO PREPARE THE CONSOLIDATED FINANCIAL STATEMENTS

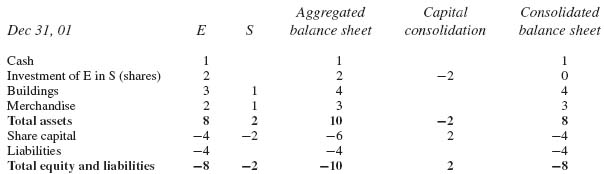

When preparing consolidated financial statements, it is first necessary to adjust the separate financial statements of the parent and of the subsidiaries so that uniform accounting policies for like transactions and other events in similar circumstances are used (IAS 27.24–27.25). The result is the statement of financial position II (also called balance sheet II) and the statement of comprehensive income II of each of these entities.20

Afterwards, the aggregated statement of financial position (also called aggregated balance sheet) and the aggregated statement of comprehensive income are prepared. This means that the balance sheets II and the statements of comprehensive income II of the parent and of the subsidiaries are combined line by line by adding together like items of assets, liabilities, equity, income, and expenses (e.g. machines, inventories, the parent's investments in its subsidiaries, and the amounts of share capital) (IAS 27.18).

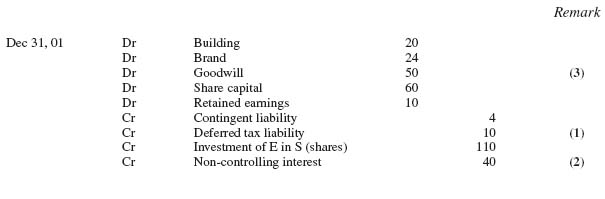

After this addition, the aggregated balance sheet includes the carrying amounts of the parent's investments in its subsidiaries (from the parent's balance sheet II), which often equal cost (IAS 27.38a) (entry “Dr Investment Cr Cash”). Moreover, the aggregated balance sheet not only comprises the assets and liabilities of a particular subsidiary, but also its equity (from the subsidiary's balance sheet II) (current posting status). However, in the consolidated financial statements it is presumed that the acquirer did not acquire the shares of its subsidiary. Instead, the business combination is accounted for as if the acquirer had acquired the individual assets and assumed the individual liabilities of the acquiree (target posting status). Therefore, in order to arrive at the target posting status, the carrying amount of the parent's investment in its subsidiary and the subsidiary's equity (from its balance sheet II) as at the acquisition date have to be eliminated (“Dr Equity Cr Investment”), since they do not occur in the target posting status (IAS 27.18a). Moreover, any goodwill and/or any non-controlling interest are recognized.21 This entry is referred to as capital consolidation.

When effecting the capital consolidation, further adjustments pertaining to the business combination are also made (e.g. increasing or decreasing the carrying amounts of the acquiree's assets and liabilities to the amount required by IFRS 3 – which is generally acquisition-date fair value – and recognition of additional assets or liabilities that have not been recognized in the acquiree's statement of financial position II).

The accounting treatment of a business combination at the acquisition date may necessitate further adjustments after the acquisition date. For example, if the carrying amount of a building has been increased to acquisition-date fair value (which means that the building's depreciable amount has increased), it is also necessary to increase depreciation expense after the acquisition date.

When preparing the consolidated financial statements for future periods, the aggregated financial statements for these future periods are used as a basis. By nature, aggregated financial statements do not include consolidation entries. Thus, in order to reach the correct posting status, the capital consolidation, as it has been effected at the acquisition date, has to be repeated. Also, further adjustments made in previous periods in respect of a subsidiary (e.g. an increase in depreciation expense) have to be repeated. Amounts recognized in profit or loss on or after the acquisition date, but before the current reporting period, have to be recognized directly in retained earnings in the current period (e.g. a gain on a bargain purchase22 or an increase in depreciation expense, which has to be recognized for the previous year) and not in the profit or loss for the current period.

Profit or loss for the period as well as total comprehensive income for the period have to be separated into the amounts attributable to the owners of the parent and to the non-controlling interest. These four amounts have to be disclosed in the statement of comprehensive income as allocations for the period (IAS 1.81B). Nevertheless, the entire amounts of profit for the year and total comprehensive income for the year have to be presented in a separate line item in the statement of comprehensive income (IAS 1.81A). If a subsidiary generates a profit for the year, the entry “Dr Profit attributable to the non-controlling interest Cr Non-controlling interest” is made. The former account is a subaccount of the account “profit for the year.” This entry results in an increase in the carrying amount of the non-controlling interest by the pro rata amount of profit (IAS 27.18c).

10 DETERMINING WHAT IS PART OF THE BUSINESS COMBINATION TRANSACTION

The acquirer and the acquiree may have a pre-existing relationship or other arrangement before negotiations for the business combination began (IFRS 3.51). Such a relationship may be on a contractual basis (e.g. licensor and licensee) or on a non-contractual basis (e.g. plaintiff and defendant). Moreover, the acquirer and the acquiree may enter into an arrangement during the negotiations for the business combination that is separate from the business combination (IFRS 3.51).

The following are examples of separate transactions that are not included in applying the acquisition method (IFRS 3.52):

- A transaction that in effect settles pre-existing relationships between the acquiree and acquirer.

- A transaction that remunerates employees or former owners of the acquiree for future services.

- A transaction that reimburses the acquiree or its former owners for paying the acquirer's acquisition-related costs.23

Separate transactions are accounted for according to the relevant IFRSs (IFRS 3.12, 3.51, and 3.B51). If the business combination in effect settles a pre-existing relationship, the acquirer recognizes a gain or loss, measured in accordance with the requirements of IFRS 3.B52.

11 EXAMPLES WITH SOLUTIONS24

Changes in a parent's ownership interest in a subsidiary that do not result in a loss of control as well as such changes that result in a loss of control are dealt with in the chapter on IAS 27/IFRS 10 (Section 2.4 and Example 6). Some of the following examples are first illustrated without deferred tax and afterwards by taking deferred tax into account. Pertaining to the basics of deferred tax, we refer to the chapter on IAS 12. The measurement of a brand acquired in a business combination according to the relief from royalty method (including the tax amortization benefit) is illustrated in the chapter on IFRS 13 (Sections 4.3 and 4.4 and Example 3).

| Dec 31, 01 | E | S |

| Buildings | 250 | 60 |

| Merchandise | 90 | 30 |

| Cash | 40 | 10 |

| Investment of E in S (shares) | 110 | |

| Total assets | 490 | 100 |

| Share capital | −250 | −60 |

| Retained earnings | −50 | −10 |

| Loans payable | −190 | −30 |

| Total equity and liabilities | −490 | −100 |

- Fair value of S's building is CU 80.

- S discloses a contingent liability (which can be measured reliably) of CU 4 arising from a present obligation in its notes to its separate financial statements. By nature, this amount has not been recognized in S's statement of financial position (IAS 37.27).28

- E identifies a brand, which has been generated internally by S. Its fair value is CU 24. That brand is not recognized in S's statement of financial position (IAS 38.63).29 However, it qualifies for recognition in E's consolidated statement of financial position according to IFRS 3.

| Net assets (equity) of S (in S's balance sheet II) | 70 | |

| Increase in the carrying amount of S's building | 20 | |

| Brand | 24 | |

| Contingent liability | −4 | |

| Net assets of S (according to IFRS 3) | 110 | |

| Non-controlling interest (40% thereof) | 44 |

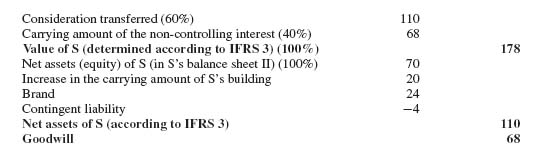

| Consideration transferred (60%) | 110 | |

| Carrying amount of the non-controlling interest (40%) | 44 | |

| Value of S (determined according to IFRS 3) (100%) | 154 | |

| Net assets of S (according to IFRS 3) (100%) (see remark 1) | 110 | |

| Goodwill | 44 |

| Net assets (equity) of S (in S's balance sheet II) | 70 | |

| Increase in the carrying amount of S's building | 40 | |

| Brand | 24 | |

| Contingent liability | −4 | |

| Net assets of S (according to IFRS 3) | 130 | |

| Non-controlling interest (40% thereof) | 52 |

| Goodwill (in E's consolidated financial statements as at Dec 31, 01) | 44 |

| 1st retrospective entry | −20 |

| 2nd retrospective entry | 8 |

| Retrospectively adjusted goodwill as at Dec 31, 01 | 32 |

| Consideration transferred (60%) | 110 |

| Carrying amount of the non-controlling interest (40%) | 52 |

| Value of S (determined according to IFRS 3) (100%) | 162 |

| Net assets of S (according to IFRS 3) (100%) | 130 |

| Goodwill as at Dec 31, 01 | 32 |

| Non-controlling interest as at Dec 31, 01 | 52 | |

| Pro rata profit (40% of CU 100) | 40.0 | |

| NCI's share of the additional depreciation expense (40% of CU -4) | −1.6 | |

| Profit attributable to the non-controlling interest | 38.4 | |

| Non-controlling interest as at Dec 31, 02 | 90.4 |

- The carrying amount of the building for tax purposes as at Dec 31, 01, is CU 60. The building's remaining useful life for tax purposes as at the same date is 10 years.

- The contingent liability and the brand are not recognized as an asset or as a liability for tax purposes.

| Net assets (equity) of S (in S's balance sheet II) | 70 | |

| Increase in the carrying amount of S's building | 20 | |

| Brand | 24 | |

| Contingent liability | −4 | |

| Deferred tax liability | −10 | |

| Net assets of S (according to IFRS 3) | 100 | |

| Non-controlling interest (40% thereof) | 40 |

| Consideration transferred (60%) | 110 | |

| Carrying amount of the non-controlling interest (40%) | 40 | |

| Value of S (determined according to IFRS 3) (100%) | 150 | |

| Net assets of S (according to IFRS 3) (100%) | 100 | |

| Goodwill | 50 |

| Net assets (equity) of S (in S's balance sheet II) | 70 | |

| Increase in the carrying amount of S's building | 40 | |

| Brand | 24 | |

| Contingent liability | −4 | |

| Deferred tax liability | −15 (= 10 + 5) | |

| Net assets of S (according to IFRS 3) | 115 | |

| Non-controlling interest (40% thereof) | 46 |

| Goodwill (in E's consolidated financial statements as at Dec 31, 01) | 50 | |

| 1st retrospective entry | −15 | |

| 2nd retrospective entry | 6 | |

| Retrospectively adjusted goodwill as at Dec 31, 01 | 41 |

| Consideration transferred (60%) | 110 | |

| Carrying amount of the non-controlling interest (40%) | 46 | |

| Value of S (determined according to IFRS 3) (100%) | 156 | |

| Net assets of S (according to IFRS 3) (100%) | 115 | |

| Goodwill | 41 |

| Non-controlling interest as at Dec 31, 01 | 46.0 | |

| Pro rata profit (40% of CU 100) | 40.0 | |

| NCI's share of the additional depreciation expense (40% of CU –4) | −1.6 | |

| NCI's share of deferred tax income (40% of CU 1) | 0.4 | |

| Profit attributable to the non-controlling interest | 38.8 | |

| Non-controlling interest as at Dec 31, 02 | 84.8 |

| Carrying amount of the investment as at Dec 30, 01 | 56 |

| Acquisition-date fair value of the investment | 60 |

| Gain | 4 |

| Consideration transferred (0%) | 0 | |

| Acquisition-date fair value of the investment (60%) | 60 | |

| Carrying amount of the non-controlling interest (40%) | 40 | |

| Value of S (determined according to IFRS 3) (100%) | 100 | |

| Net assets (equity) of S (in S's balance sheet II) | 60 | |

| Increase in the carrying amount of S's building | 8 | |

| Net assets of S (according to IFRS 3) (100%) | 68 | |

| Goodwill | 32 |

| Consideration transferred (0%) | 0 | |

| Acquisition-date fair value of the investment (60%) | 60 | |

| Carrying amount of the non-controlling interest (40%) | 40 | |

| Value of S (determined according to IFRS 3) (100%) | 100 | |

| Net assets (equity) of S (in S's balance sheet II) (100%) | 60 | |

| Increase in the carrying amount of S's building | 8 | |

| Deferred tax liability hereto | −2 | |

| Net assets of S (according to IFRS 3) | 66 | |

| Goodwill | 34 |

| Accumulated EBITDA for the years 02–04 | Contingent consideration | Probability |

| < CU 16 | 0 | 20% |

| ≥ CU 16 and < CU 20 | 5 | 40% |

| ≥ CU 20 | 10 | 40% |

1If IFRS 9 was not applied early, the shares would be measured either at cost or according to IAS 39 (IAS 27.38). In the latter case, the investments would normally be measured at fair value. However, the equity instruments would be measured at cost if it were not possible to determine fair value reliably (IAS 39.AG80–39.AG81).

2See the chapter on Conceptual Framework, Section 4.2.2.

3See the chapter on Conceptual Framework, Section 4.2.2.

4Regarding costs to issue equity instruments, see the chapter on IAS 32, Section 6 and Example 3.

5See Section 6.5.

6See the chapter on Conceptual Framework, Section 6.1.

7See the chapter on Conceptual Framework, Section 6.

8See KPMG, Insights into IFRS, 7th edition, 2.6.570.20

9See the chapter on IFRS 9/IAS 39, Section 2.7. IFRS 9 has not yet changed the hedge accounting requirements of IAS 39. Instead, IFRS 9 refers to IAS 39 in this regard (IFRS 9.5.2.3 and 9.5.3.2).

10See the chapter on IFRS 13, Sections 4.3 and 4.4, as well as Example 3.

11See the chapter on IAS 37, Section 3.

12See the chapter on IAS 12, Sections 3.2.5 and 3.5.2.

13See the table in Section 6.1.

14See the table in Section 6.1.

15If IFRS 9 is not yet applied, a gain or loss from the remeasurement of the equity interest held by the acquirer before the business combination to fair value has to be recognized in profit or loss. Changes in the value of the equity interest that were recognized in other comprehensive income in prior reporting periods (available-for-sale financial assets) have to be transferred to profit or loss (presumption of a disposal of the equity interest).

16See Example 6 regarding minority veto rights that lapse.

17See the table in Section 6.1.

18See Ernst & Young, International GAAP 2011, 536. See Section 7 of this chapter regarding the subsequent measurement and accounting of contingent consideration.

19See the chapter on IAS 36, Section 10 and Example 7.

20 See the chapter on IAS 27/IFRS 10, Section 2.3.1.

21The logic of recognizing goodwill and a non-controlling interest is explained in Section 6.1.

22See Section 6.4.

23See Section 5.

24The examples in this section are based on simplified illustrations of financial statements.

25In this table, assets are shown with a plus sign whereas liabilities and items of equity are shown with a minus sign.

26In this table, debit entries and assets are shown with a plus sign whereas credit entries, liabilities and items of equity are shown with a minus sign.

27In this table, assets are shown with a plus sign whereas liabilities and items of equity are shown with a minus sign.

28See the chapter on IAS 37, Section 3.

29See the chapter on IAS 38, Section 3.4.

30See Section 6.1.

31In this table, debit entries and assets are shown with a plus sign whereas credit entries, liabilities, and items of equity are shown with a minus sign.

32In this table, debit entries and assets are shown with a plus sign whereas credit entries, liabilities, and items of equity are shown with a minus sign.

33See Section 6.7.

34See Section 9.

35See Section 9.

36See the chapter on IAS 12, Section 3.2.5.

37See the chapter on IAS 12, Section 3.2.5.

38In this table, debit entries and assets are shown with a plus sign whereas credit entries, liabilities, and items of equity are shown with a minus sign.

39See Section 9.

40The solution of this example does not change if IFRS 9 (and the consequential amendment of IFRS 3.42 caused by IFRS 9) is not applied early. This is because the previously held shares are an investment in an associate accounted for using the equity method and in that case there is no difference between the “old” and the “new” requirements under IFRS.

41See the chapter on IAS 12, Section 3.2.5.

42See the chapter on IAS 28, Section 2.2.1.

43See Section 2.

44EBITDA = earnings before interest, taxes, depreciation, and amortization.

45See Section 2.