IAS 23 BORROWING COSTS

1 INTRODUCTION

IAS 23 is applied to the accounting for borrowing costs (IAS 23.2–23.3). Borrowing costs are interest costs and other costs that the entity incurs in connection with the borrowing of funds (IAS 23.5). Borrowing costs may include the following (IAS 23.6):

- Interest expense calculated according to the effective interest method (IFRS 9, Appendix A and IAS 39.9).

- Finance charges relating to finance leases recognized according to IAS 17 (IAS 17.25–17.26).

Borrowing costs, which are directly attributable to the acquisition, construction or production of a qualifying asset, form part of the cost of that asset, i.e. they are capitalized (IAS 23.1 and 23.8–23.9). A qualifying asset is an asset that necessarily takes a substantial period of time to get ready for its intended use or sale (IAS 23.5). The term “substantial period of time” is not quantified in the standard. In our opinion, this term can be interpreted as a period of at least 12 months. Assets that are ready for their intended use or sale when they are acquired are not qualifying assets (IAS 23.7).

Among others, an entity is not required to apply IAS 23 to the borrowing costs for inventories that are produced in large quantities on a repetitive basis (e.g. whiskey in the financial statements of the producer) (IAS 23.4b).

2 SPECIFIC AND GENERAL BORROWINGS

When calculating the amount of borrowing costs to capitalize, two categories are to be distinguished (IAS 23.10–23.15):

- Specific borrowings (i.e. funds specifically borrowed for the purpose of acquiring, constructing or producing a qualifying asset).

- General borrowings (i.e. other borrowings that could have been repaid if the expenditure on the asset had not been incurred1).

In the case of specific borrowings, the amount to be capitalized is represented by the actual borrowing costs incurred on these borrowings during the period. Investment income on the temporary investment of those borrowings is deducted from the amount to be capitalized (IAS 23.12).

In the case of general borrowings, the amount to be capitalized is calculated by (IAS 23.14):

- applying the weighted average rate for the borrowing costs of general borrowings outstanding during the period,

- to the expenditures on the qualifying asset that are not financed by specific borrowings.

The borrowing costs to be capitalized are those borrowing costs that would have been avoided if the expenditure on the qualifying asset had not been made (IAS 23.10).

The amount of the borrowing costs capitalized during a period must not exceed the amount of borrowing costs incurred during that period (IAS 23.14).

Expenditures on a qualifying asset include only those expenditures that have resulted in payments of cash, transfers of other assets or the assumption of interest-bearing liabilities. Expenditures are reduced by any progress payments received and grants received in connection with the qualifying asset (see IAS 20). The average carrying amount of the qualifying asset during a period, including borrowing costs previously capitalized, is usually a reasonable approximation of the expenditures to which the capitalization rate is applied (IAS 23.18).

3 PERIOD OF CAPITALIZATION

Capitalization of borrowing costs as part of the cost of a qualifying asset begins when the entity first meets all of the following conditions (commencement of capitalization) (IAS 23.17 and 23.19):

- Expenditures for the asset are incurred.

- Borrowing costs are incurred.

- Activities have started that are necessary to prepare the asset for its intended use or sale.

Capitalization of borrowing costs is suspended during extended periods in which the entity suspends active development of a qualifying asset (suspension of capitalization) (IAS 23.20–23.21). During this period of time the borrowing costs are recognized as an expense.

Capitalization of borrowing costs ceases when substantially all activities necessary to prepare the qualifying asset for its intended use or sale are complete (cessation of capitalization) (IAS 23.22–23.23). It may be the case that an entity completes the construction of a qualifying asset in parts and each part is capable of being used while construction continues on other parts (e.g. the construction of a business park consisting of several buildings). In this case, the capitalization of borrowing costs ceases when the entity completes substantially all the activities necessary to prepare that part for its intended use or sale (IAS 23.24–23.25).

4 EXAMPLES WITH SOLUTIONS

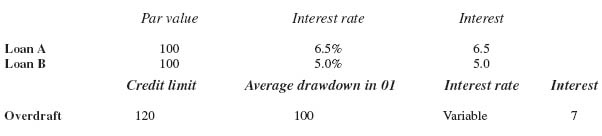

| Loan B | 100 | |

| Overdraft | 100 | |

| General borrowings (I) | 200 | |

| Borrowing costs (loan B) | 5 | |

| Borrowing costs (overdraft) | 7 | |

| General borrowing costs in total (II) | 12 | |

| Weighted average rate for general borrowing costs (III) = (II : I) | 6% | |

| Average expenditures in 01 | 200 | CU 400 : 2 |

| Less specific borrowings (loan A) | 100 | |

| Expenditures financed by general borrowings (IV) | 100 | |

| Borrowing costs for general borrowings attributable to the construction of the qualifying asset (= III · IV) | 6 |

1 See KPMG, Insights into IFRS, 6th edition, 4.6.390.20.