IFRS 5 NON-CURRENT ASSETS HELD FOR SALE AND DISCONTINUED OPERATIONS

1 INTRODUCTION AND OVERVIEW1

IFRS 5 includes rules with respect to the sale or abandonment of non-current assets. The differentiation between current and non-current assets according to IFRS 5 corresponds to the differentiation in IAS l2 (IFRS 5.Appendix A and IAS 1.66).

Non-current assets are sold individually in the simplest situation.

However, it may also be the case that a disposal group is sold. A disposal group is a group of assets to be disposed of as a group in a single transaction. A disposal group also includes liabilities directly associated with those assets that will be transferred in the transaction. The group also includes goodwill acquired in a business combination if the group is a cash-generating unit (CGU) according to IAS 36 to which goodwill has been allocated, or if it is an operation within such a CGU (IFRS 5.Appendix A and IAS 36.80–36.87).

A component of an entity comprises operations and cash flows that can be clearly distinguished from the rest of the entity both operationally and for financial reporting purposes. In other words, a component of an entity will have been a CGU or a group of CGUs, while being held for use (IFRS 5.31).

A discontinued operation is a component of an entity that is held for sale or has been disposed of. Furthermore, the component of the entity must meet one of the following criteria (IFRS 5.32):

- It represents a separate major line of business or geographical area of operations.

- It is part of a single coordinated plan to dispose of a separate major line of business or geographical area of operations.

- It is a subsidiary acquired exclusively with a view to resale.

Meeting the above definitions has the following consequences for financial reporting:

- If non-current assets held for sale are to be sold individually, they have to be presented separately in the statement of financial position. In some cases, they are also subject to the specific measurement provisions of IFRS 5.

- Disposal groups that are held for sale have to be presented separately in the statement of financial position. However, the specific measurement provisions of IFRS 5 are not effective for all types of assets that may be part of disposal groups.

- In the case of discontinued operations, the following differentiation is necessary:

- If the component of the entity has already been sold, i.e. if the assets and liabilities have already been derecognized, the issues of applying the specific measurement provisions of IFRS 5 and of separate presentation in the statement of financial position are obsolete. However, separate presentation in the statement of comprehensive income is necessary.

- It may be the case that the assets and liabilities of a disposal group held for sale, which represents a discontinued operation, have not been derecognized until the end of the reporting period. In this case, in addition to separate presentation in the statement of comprehensive income, separate presentation in the statement of financial position and measurement according to IFRS 5 are also necessary.

- If a business unit has been abandoned, separate presentation in the statement of comprehensive income is necessary. However, there is no separate presentation in the statement of financial position and the specific measurement provisions of IFRS 5 are not applied.

2 SCOPE

Regarding the scope of IFRS 5, the following distinction is necessary (IFRS 5.2):

- The requirements of IFRS 5 for classification as “held for sale”3 apply to all recognized non-current assets and to all disposal groups of an entity. Classification as “held for sale” requires the application of the presentation requirements of IFRS 5. Moreover, the Standard includes specific presentation requirements with respect to discontinued operations.

- The measurement provisions of IFRS 5 do not apply to all non-current assets and to all assets included in disposal groups classified as held for sale. The following assets are excluded from the measurement requirements of IFRS 5 regardless of whether they are individual assets or part of a disposal group. Instead, the standards listed apply with respect to their measurement (IFRS 5.5):

- Deferred tax assets (IAS 12).

- Assets arising from employee benefits (IAS 19).

- Financial assets within the scope of IFRS 9.

- Non-current assets that are accounted for in accordance with the fair value model in IAS 40.

- Non-current assets that are measured at fair value less costs to sell in accordance with IAS 41.

- Contractual rights under insurance contracts as defined in IFRS 4.

3 NON-CURRENT ASSETS AND DISPOSAL GROUPS HELD FOR SALE

3.1 Classification as “Held for Sale”

A non-current asset or disposal group is classified as “held for sale,” if its carrying amount will be recovered principally through a sale transaction rather than through continuing use (IFRS 5.6). For this to be the case, the asset or disposal group must be available for immediate sale in its present condition, subject only to terms that are usual and customary for sales of such assets or disposal groups. In addition, the sale must be highly probable (IFRS 5.7).

The term “highly probable” is quantitatively defined as a probability of significantly more than 51% (IFRS 5.Appendix A). The standard does not leave preparers to interpret what this might mean. Instead, it sets out the criteria for a sale to be highly probable.4 Accordingly, the criterion “highly probable” is met when the following criteria are cumulatively met (IFRS 5.8):

- The appropriate level of management is committed to a plan to sell the asset or disposal group.

- An active program to locate a buyer and complete the plan has been initiated.

- The asset or disposal group is actively marketed for sale at a price that is reasonable in relation to its current fair value.

- The sale should be expected to qualify for recognition as a completed sale within 12 months from the date of classification. However, events or circumstances may extend this period of time (IFRS 5.9 and 5.B1).

- Actions required to complete the plan should indicate that it is unlikely that significant changes to the plan will be made or that the plan will be withdrawn.

The probability of approval of the shareholders (if required in the jurisdiction) should also be considered as part of the assessment as to whether the sale is highly probable (IFRS 5.8).

If the criteria of IFRS 5.7 and 5.8 (see above) are not met until the end of the reporting period, the non-current asset or disposal group in question must not be classified as “held for sale” (IFRS 5.12).

An entity that is committed to a sale plan involving loss of control of a subsidiary must classify all the assets and liabilities of that subsidiary as held for sale when the criteria above (IFRS 5.6–5.8) are met. This applies regardless of whether the entity will retain a non-controlling interest in its former subsidiary after the sale (IFRS 5.8A).

In the case of non-current assets or disposal groups that are exclusively acquired with a view to their subsequent disposal, the following applies: The non-current asset or disposal group is classified as held for sale at the acquisition date only if the 12 month requirement (see above) is met (under consideration of the corresponding exceptions). Furthermore, it must be highly probable that any other criteria mentioned above that are not met at that date will be met within a short period following the acquisition (usually within three months) (IFRS 5.11).

Non-current assets or disposal groups that are to be abandoned must not be classified as “held for sale.” This is because the carrying amount will be recovered principally through continuing use. Non-current assets or disposal groups to be abandoned include non-current assets or disposal groups (IFRS 5.13):

- which are to be used to the end of their economic life,

- that are to be closed rather than sold.

A non-current asset that has been temporarily taken out of use must not be accounted for as if it had been abandoned (IFRS 5.14). The entity may not, for example, stop depreciating the asset.5

3.2 Measurement of Non-current Assets and Disposal Groups Classified as “Held for Sale”

3.2.1 General Aspects

The measurement requirements of IFRS 5 apply to all non-current assets and disposal groups classified as held for sale. However, certain assets are excluded from the measurement provisions of IFRS 5 regardless of whether they are individual assets or part of a disposal group.6

A non-current asset or a disposal group classified as “held for sale” is measured at the lower of its carrying amount and fair value less costs to sell (IFRS 5.15). Fair value is the amount for which an asset could be exchanged, or a liability settled, between knowledgeable, willing parties in an arm's length transaction. Costs to sell are the incremental costs directly attributable to the disposal of an asset or of a disposal group, excluding finance costs and income tax expense (IFRS 5.Appendix A). Also, when a newly acquired asset (or disposal group) is classified as “held for sale,” it is measured at the lower amount as described above. In this case, measurement at initial recognition is effected at the lower of the carrying amount that the asset (or disposal group) would have had without this classification (e.g. costs of purchase) and fair value less costs to sell (IFRS 5.16).

In the case of a business combination, the acquiree's assets and liabilities are generally measured at fair value. However, if a non-current asset (or disposal group) held for sale is received in a business combination, it is measured on the acquisition date at fair value less costs to sell and not at fair value, which differs from the general rules of IFRS 3 (IFRS 5.16 and IFRS 3.31). The difference is not recognized as an impairment loss.

Immediately before the initial classification of an asset or of a disposal group as “held for sale,” the asset or all the assets and liabilities in the group have to be measured in accordance with the applicable Standards (IFRS 5.18). A disposal group continues to be consolidated while it is held for sale. Therefore, revenue (e.g. from the sale of inventory) and expenses (including interest) continue to be recognized. However, property, plant, and equipment (IAS 16), and intangible assets (IAS 38) that are classified as “held for sale” or are part of a disposal group classified as “held for sale” are not depreciated or amortized (IFRS 5.25).7

Impairment losses on initial classification of a non-current asset (or disposal group) as held for sale are included in profit or loss even if the asset is (or the disposal group includes assets that are) measured at a revalued amount. The same applies to gains and losses on subsequent remeasurement (IFRS 5.20).8

The application of the measurement requirements of IFRS 5 for disposal groups results in a complex interplay of measurement on an individual basis and on a group basis:

- Immediately before classification of the disposal group as “held for sale,” the individual assets and liabilities in the group have to be measured in accordance with the applicable standards (measurement on an individual basis) (IFRS 5.18). In this way, items of property, plant, and equipment are depreciated until the date of classification as “held for sale.” An impairment test which is normally effected only at the end of the reporting period according to the general accounting rules (e.g. IAS 2, IAS 36, or IAS 39) is also necessary at the date of classification as “held for sale.”

- The resulting net carrying amount of the disposal group (assets less liabilities) has to be compared with the group's fair value less costs to sell (measurement on a group basis) (IFRS 5.4).

- If this results in an impairment loss with respect to the group, the loss has to be allocated to the non-current assets in the group that are within the scope of the measurement requirements of IFRS 5, in the order of allocation set out in IAS 36.104 (IFRS 5.23). Thus, the carrying amount of any goodwill is reduced first. The remaining impairment loss is allocated to the other assets defined above (e.g. items of property, plant, and equipment, and intangible assets) pro rata on the basis of the carrying amount of each asset. Examples of assets that are excluded from the allocation are inventories.

The measurement requirements of IFRS 5 are applied to a disposal group as a whole (i.e. its carrying amount is compared with its fair value less costs to sell), only if the disposal group contains at least one non-current asset that is subject to the measurement requirements of IFRS 5 (IFRS 5.4).

3.2.2 Changes to a Plan of Sale

If an asset (or a disposal group) has been classified as “held for sale,” but the criteria for such classification are no longer met at a later point in time, the classification of the asset (disposal group) as “held for sale” ceases (IFRS 5.26). A non-current asset that ceases to be classified as “held for sale” (or ceases to be included in a disposal group classified as held for sale) is measured at the lower of the following amounts (IFRS 5.27):

- Its carrying amount before classification of the asset (or disposal group) as “held for sale,” adjusted for any depreciation, amortization or revaluations that would have been recognized had the asset (or disposal group) not been classified as “held for sale.”

- Its recoverable amount (according to IAS 36) at the date of the decision not to sell. If the non-current asset is part of a CGU, its recoverable amount is the carrying amount that would have been recognized after the allocation of any impairment loss arising on that CGU according to IAS 36.

3.3 Presentation

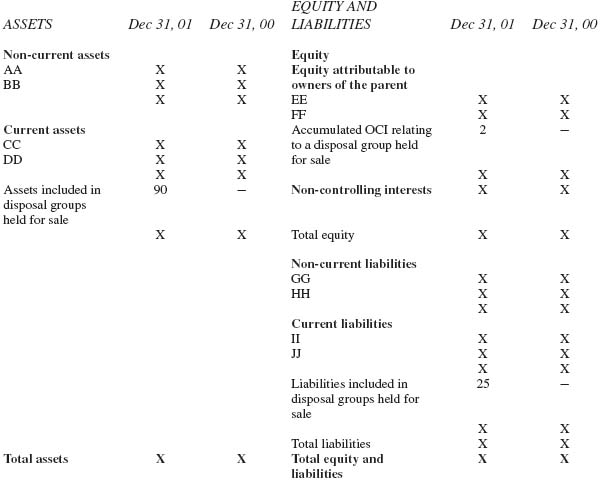

A non-current asset classified as “held for sale” and the assets of a disposal group classified as “held for sale” have to be presented separately from other assets in the statement of financial position. The total of these amounts has to be presented as a separate line item in that statement (IFRS 5.38 and IAS 1.54(j)).

The liabilities of a disposal group classified as “held for sale” have to be presented separately from other liabilities in the statement of financial position. The total of these liabilities has to be presented as a separate line item in that statement (IFRS 5.38 and IAS 1.54(p)). However, the content of that line item has to be determined restrictively. Liabilities are only part of a disposal group if they are directly associated with the assets of the group and are also transferred on disposal of the assets (IFRS 5.Appendix A).

The assets and liabilities that have to be presented in the statement of financial position according to IFRS 5 (IAS 1.54(j) and 1.54(p)) must not be offset. The major classes of assets and liabilities classified as “held for sale” generally have to be separately disclosed either in the statement of financial position or in the notes. The cumulative income or expense recognized in other comprehensive income relating to a non-current asset or disposal group classified as held for sale shall be presented separately in the statement of financial position (e.g. the fair value reserve in respect of equity instruments measured at fair value through other comprehensive income according to IFRS 9.5.7.1b and 9.5.7.59) (IFRS 5.38–5.39, 5.BC58, 5.IG Example 12, IAS 1.32, and 1.54).

Classification of non-current assets or of disposal groups as “held for sale” in the reporting period does not result in reclassification or re-presentation of the corresponding amounts in the statements of financial position for prior periods (IFRS 5.40).

Non-current assets (as well as assets of a class that the entity would normally regard as non-current that are acquired exclusively with a view to resale) must not be (re)classified as current unless they meet the criteria for classification as “held for sale” according to IFRS 5 (IFRS 5.3). The differentiation between current and non-current assets according to IFRS 5 corresponds to the differentiation in IAS 1 (IFRS 5.Appendix A and IAS 1.66).

According to the guidance on implementing IFRS 5 (IFRS 5.IG, Example 12), a subtotal is presented in the statement of financial position for current assets and current liabilities, without taking into account the amounts classified as “held for sale.” After the subtotal, the latter amounts are presented as separate line items. Afterwards, the total for current assets or current liabilities is presented.

4 PRESENTATION OF DISCONTINUED OPERATIONS

4.1 General Aspects

Meeting the definition of a discontinued operation results in additional disclosures. Among others, a single amount has to be disclosed in the statement of comprehensive income which is the total of the following amounts (IFRS 5.33a and IAS 1.82a):

- Post-tax profit or loss of discontinued operations.

- Post-tax gain or loss recognized on the measurement to fair value less costs to sell or on the disposal of the assets or disposal group(s) constituting the discontinued operation.

This total amount is determined and disclosed for the entire reporting period and not only for the period of time starting on discontinuation. It must also be determined and disclosed for prior periods presented in the financial statements (IFRS 5.34). This amount has to be disclosed separately from continuing operations. In the statement of comprehensive income, all line items from revenue down to profit or loss from continuing operations are presented excluding the amounts attributable to discontinued operations. Generally, among others, the revenue, expenses, and pre-tax profit or loss of discontinued operations included in the amount defined above (IFRS 5.33a) must also be presented in the statement of comprehensive income or in the notes (IFRS 5.33b).

Discontinued operations include operations that were already disposed of and operations classified as “held for sale.” If the entire discontinued operation or a part thereof meets the definition of “held for sale,” the presentation requirements described in Section 3.3 have to be met in addition to those of this chapter. The assets and liabilities that are part of discontinued operations need not be presented or disclosed separately from other assets or liabilities held for sale. If a disposal group becomes a discontinued operation in the reporting period and is classified as “held for sale” in the same period, the prior period information is not adjusted in the statement of financial position.

If a disposal group to be abandoned meets one of the criteria in IFRS 5.32(a)–(c), the results and cash flows of the disposal group are presented as discontinued operations according to IFRS 5.33–5.34 in the period in which the disposal takes place. The figures for prior periods have to be adjusted (IFRS 5.34). A disposal group to be abandoned does not meet the definition of “held for sale” (IFRS 5.13).

4.2 Selected Specifics in Consolidated Financial Statements

Generally, among others, the revenue, expenses, and pre-tax profit or loss of discontinued operations must be presented in the statement of comprehensive income or in the notes (IFRS 5.33b). If a subsidiary represents a discontinued operation and revenue and expenses arise between that subsidiary and another subsidiary or the parent of the group, in our view, the following procedure is necessary. In the statement of comprehensive income and in the notes, the marginal revenue and marginal expenses of the group, which are attributable to the discontinued operation, are presented as discontinued operations.

5 EXAMPLES WITH SOLUTIONS

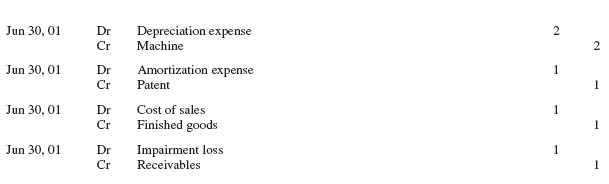

| Carrying amount as at Dec 31, 00 | Additional information | |

| Machine | 20 | Remaining useful life as at Dec 31, 00: 5 years |

| Acquired patent | 10 | Remaining useful life as at Dec 31, 00: 5 years |

| Finished goods | 8 | The net realizable value (IAS 2.6) as at Jun 30, 01 is CU 7 |

| Receivables | 6 | The receivables are measured at amortized cost. On Jun 30, the value of the receivables determined according to IAS 39.63 is CU 5 (IFRS 9.5.2.2) |

- The machine is depreciated and the patent is amortized.

- The finished goods are tested for impairment (i.e. they are measured at the lower of cost and net realizable value) (IAS 2.9).

- The carrying amount of the receivables is reduced to the amount determined according to IAS 39.63.

| Continuing operations | |

| Revenue | 10 |

| Expenses | −9 |

| Profit from continuing operations | 1 |

| Discontinued operations | |

| Revenue | 2 |

| Expenses | −1 |

| Profit from discontinued operations | 1 |

| Profit | 2 |

| 01 | 00 | |

| Continuing operations | ||

| Revenue | X | X |

| Expenses | X | X |

| Profit from continuing operations | X | X |

| Discontinued operations | ||

| Profit from discontinued operations | 7 | 2 |

| Profit | X | X |

| 01 | 00 | |

| Continuing operations | ||

| Revenue | X | X |

| Expenses | X | X |

| Profit from continuing operations | X | X |

| Discontinued operations | ||

| Profit from discontinued operations | 6 | 2 |

| Profit | X | X |

1With regard to the definitions in this section we refer to IFRS 5.Appendix A.

2See the chapter on IAS 1, Section 6.1.

3See Section 3.1.

4See PwC, Manual of Accounting, IFRS 2011, 26.47.

5See PwC, Manual of Accounting, IFRS 2011, 26.74.

6See Section 2.

7See KPMG, Insights into IFRS, 7th edition, 5.4.60.70.

8See KPMG, Insights into IFRS, 6th edition, 5.4.60.40

9Before the consequential amendments to IAS 39 caused by IFRS 9, equity instruments of the category “available for sale” (IAS 39.9) were generally also measured at fair value through other comprehensive income (IAS 39.55b).

10If IFRS 9 (and its consequential amendments to IAS 39) were not applied early, and if the receivables belonged to the category “loans and receivables” (IAS 39.9), the example and its solution would not change.

11If IFRS 9 (and its consequential amendments to IAS 39) were not applied early, the solution to this example would not change if the shares belonged to the category “available for sale” (IAS 39.9).