IAS 34 INTERIM FINANCIAL REPORTING

1 INTRODUCTION

The objective of IAS 34 is to prescribe the minimum content of an interim financial report (i.e. of interim financial statements) and to prescribe the principles for recognition and measurement in such a report. An interim financial report is presented for an interim period, i.e. for a financial reporting period that is shorter than a full financial year (IAS 34.1 and 34.4). For example, an entity may prepare quarterly financial statements.

While all entities that apply IFRSs are required to present financial statements at least annually (IAS 1.36), IAS 34 does not contain a commitment to prepare interim reports. Moreover, IAS 34 does not prescribe the length of interim periods. These issues are left to be decided by governments, securities regulators, stock exchanges, and accountancy bodies. However, if an entity is required or elects to publish an interim financial report in accordance with IFRSs, IAS 34 has to be applied (IAS 34.1).

If the entity's most recent annual financial statements were consolidated statements, the entity's interim financial reports also have to be prepared on a consolidated basis (IAS 34.14).

2 CONTENT OF AN INTERIM FINANCIAL REPORT

2.1 Components

IAS 34 defines the minimum content of an interim report as including condensed financial statements (condensed interim report). However, an entity may also prepare a complete set of financial statements as described in IAS 11 (comprehensive interim report) (IAS 34.4. and 34.6).

A condensed interim report consists of the following components (IAS 34.8):

- A condensed statement of financial position

- Either:

- a condensed single statement of comprehensive income (one statement approach) or

- a condensed separate income statement and a condensed separate statement of comprehensive income (two statement approach)

- A condensed statement of changes in equity

- A condensed statement of cash flows

- Selected explanatory notes

If the components of profit and loss are presented in a separate income statement as described in IAS 1.10A, interim condensed information is presented from that separate statement (IAS 34.8A).

A condensed interim report has to include, at a minimum, each of the headings and subtotals that were included in its most recent annual financial statements as well as the selected explanatory notes as required by IAS 34. Additional line items or notes have to be included if their omission would make the condensed interim report misleading (IAS 34.10).

If an entity publishes a complete set of financial statements in its interim report (comprehensive interim report), the form and content of those statements have to conform to the requirements of IAS 1 for a complete set of financial statements (IAS 34.4–34.5 and 34.9).

2.2 Periods and dates to be presented in interim reports

The statement of financial position has to be presented as at the end of the current interim period and as at the end of the immediately preceding financial year (IAS 34.20a). In some cases, it may be necessary to present a third statement of financial position (IAS 34.5f).

The single statement of comprehensive income (one statement approach) or the separate income statement and the separate statement of comprehensive income (two statement approach) have to be presented for the following periods (IAS 34.20b):

- Current interim period

- Cumulatively for the current financial year to date

- Comparable periods (current and year-to-date) of the immediately preceding financial year

The statement of changes in equity and the statement of cash flows are presented cumulatively for the current financial year to date with a comparative statement for the comparable year-to-date period of the immediately preceding financial year (IAS 34.20(c) and (d)).

3 MATERIALITY

In deciding how to recognize, measure, classify or disclose an item for interim financial reporting purposes, materiality has to be assessed in relation to the interim period financial data. In making assessments of materiality, it has to be recognized that interim measurements may rely on estimates to a greater extent than measurements of annual financial data (IAS 34.23).

4 RECOGNITION AND MEASUREMENT

The recognition and measurement guidance of IAS 34 also applies to complete financial statements for an interim period (i.e. to a comprehensive interim report) (IAS 34.7).

4.1 Discrete approach vs. integral approach

The same accounting policies are applied in an entity's interim financial statements as are applied in its annual financial statements. Departures from these accounting policies are subject to the general rules of IFRS (IAS 34.28–34.29). For example, initial application of a new Standard or of an amended version of an existing Standard may lead to the application of a different measurement method in the entity's first quarterly financial statements of the year (as at Mar 31, 02) than in its last annual financial statements (as at Dec 31, 01).

Interim financial reporting according to IAS 34 is primarily based on a discrete view. By contrast, interim financial reporting according to US GAAP (see among others: APB 28) is more based on an integral view:

- Under the discrete approach (IAS 34) interim period profit or loss is measured by viewing each interim period separately and not by anticipation of the annual financial statements. For assets, the same tests of future economic benefits apply at interim dates as at the end of the financial year. Costs that by their nature would not qualify as assets at the financial year-end would not qualify at interim dates either. Similarly, a liability at the end of an interim period has to represent an existing obligation at that date, just as it must at the end of an annual reporting period (IAS 34.32).

- Under the integral approach, interim period profit or loss is measured by viewing each interim period as an integral part of the corresponding annual period. The interim report is intended to enable forecasts of the annual financial statements. For example, it may be the case that an entity performs the day-to-day servicing for its machines during its off-season, which is the first quarter of the year. The expenditures for this work do not qualify for capitalization in the entity's annual financial statements as at Dec 31. Under the discrete approach, the total of these expenditures would be recognized in profit or loss in the entity's first quarterly financial statements as at Mar 31 (IAS 34.B2). However, under the integral approach, an appropriate portion of these expenditures is allocated to each interim period of the year.

4.2 Independence of the annual result from the frequency of reporting

The frequency of an entity's reporting (annual, half-yearly or quarterly) must not affect its annual results (IAS 34.28).

This principle is breached in the case of reversals of impairment losses relating to goodwill. Reversing goodwill impairment losses is prohibited in the annual financial statements (IAS 36.124–36.125). IFRIC 10 extends the scope of that prohibition. It also prohibits, for example, reversing an impairment loss relating to goodwill recognized in the first quarterly financial statements of the year in the annual financial statements.

4.3 Quantity component and price component

Revenues and expenses regularly have a quantity component as well as a price component:

- Quantity component: Under the discrete approach, the actual quantity structure of the quarter is relevant. This means that it is prohibited to recognize an appropriate portion of revenues and expenses that arise in subsequent quarters according to IFRSs in the current quarterly financial statements. Vice versa, it is prohibited to recognize an appropriate portion of revenues and expenses that arise in the current quarter according to IFRSs in the interim reports of the next quarters.

- With regard to the price component, the illustrations in IAS 34 Appendix B are rather based on an integral view than on a discrete view. If the price component depends on whether certain limits will be exceeded for the whole year, the price that is recognized in the first quarters depends on an estimate of whether those limits will be exceeded by the end of the year. An example is a contractually agreed volume rebate, the percentage of which depends on the quantity purchased during the year (IAS 34.B23).

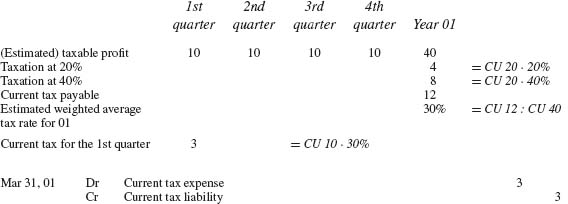

These considerations also apply when measuring interim income tax expense (IAS 34.30c and 34.B12–34.B16):

- The tax base is the taxable profit for the interim period (quantity component in a broader sense).

- In the case of a progressive tax system, the tax rate (price component) is determined on the basis of the estimated amount of taxable profit for the year (estimated weighted average tax rate for the year).

- Finally, the tax rate is multiplied with taxable profit for the interim period.

The estimate of the tax rate for the year may have to be adjusted as a result of the taxable profit for the following interim period (IAS 34.B13).

5 EXAMPLES WITH SOLUTIONS

| Jan 01, 01 – Jun 30, 01 | Jan 01, 00 – Jun 30, 00 |

1 See the chapter on IAS 1, Section 5.

2 If E did not apply IFRS 9 early, and if the shares were classified as “available for sale” (IAS 39.9), the solution of this example would be the same (IAS 39.55b and IAS 18.30c).