IAS 27 (2008) CONSOLIDATED AND SEPARATE FINANCIAL STATEMENTS, IAS 27 (2011) SEPARATE FINANCIAL STATEMENTS, AND IFRS 10 (2011) CONSOLIDATED FINANCIAL STATEMENTS

1 INTRODUCTION

Consolidated financial statements are the financial statements of a group presented as if the individual subsidiaries of the group and the parent were a single entity. Consolidated financial statements present the individual assets (e.g. buildings, machines, and inventories) and liabilities of the subsidiaries rather than the direct equity interests in the subsidiaries. A subsidiary is an entity that is controlled by another entity (known as the parent). In separate financial statements of a parent, the investments in subsidiaries are accounted for on the basis of the direct equity interest. They do not present the individual assets and liabilities of the subsidiaries (IAS 27.4). The term “separate financial statements” does not comprise the financial statements of an entity that does not have a subsidiary, associate or venturer's interest in a jointly controlled entity (IAS 27.7).

The effects of changes in foreign exchange rates (IAS 21) as well as the aspects with respect to business combinations covered by IFRS 3 (e.g. the acquisition method) are not described in this chapter of the book.

In May 2011, the IASB issued IFRS 10 “Consolidated Financial Statements” as well as a new version of IAS 27 named “Separate Financial Statements.” The new standards have to be applied in the financial statements as at Dec 31, 2013 (if the entity's reporting periods start on Jan 01 and end on Dec 31). Earlier application is permitted by the IASB (IFRS 10.C1 and IAS 27.18). However, in the European Union, new IFRSs have to be endorsed by the European Union before they can be applied. There has been no endorsement with regard to IFRS 10 and the new version of IAS 27 as yet.

The remainder of this chapter is structured as follows:

- Section 2 discusses the rules applicable if the entity decides not to apply the new standards early.

- Section 3 presents the rules of IFRS 10.

- Section 4 introduces the new version of IAS 27.

2 FINANCIAL REPORTING WITHOUT EARLY APPLICATION OF IFRS 10 AND IAS 27 (2011)

2.1 The Concept of “Control”

A subsidiary is an entity that is controlled by another entity (known as the parent). Consolidated financial statements have to include all subsidiaries of the parent (IAS 27.4 and 27.12).

Control is the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities (IAS 27.4). Control is presumed to exist when the parent owns more than half of the voting power of an entity directly or indirectly through subsidiaries. However, in exceptional circumstances it may be clearly demonstrated that such ownership does not constitute control (IAS 27.13).

Control also exists when the parent owns half or less of the voting power when one of the following criteria is met (IAS 27.13):

- The investor has power over more than half of the voting rights by virtue of an agreement with other investors.

- The investor has the power to govern the financial and operating policies of the entity under a statute or an agreement.

- The investor has the power to appoint or remove the majority of the members of the board of directors or equivalent governing body and control of the entity is by that board or body.

- The investor has the power to cast the majority of votes at meetings of the board of directors or equivalent governing body and control of the entity is by that board or body.

Control is not only assessed on the basis of existing voting rights. Potential voting rights (e.g. share call options or convertible bonds that give the investor additional voting power when they are exercised or converted) also have to be taken into account if they are currently exercisable or convertible. Potential voting rights are not currently exercisable or convertible when, for example, they cannot be exercised or converted until the occurrence of a future event or until a future date. All facts and circumstances that affect potential voting rights have to be examined except the intention of management and the financial ability to exercise or convert (IAS 28.8–28.9). The rules for the consideration of potential voting rights when determining if there is control correspond to those when determining if there is significant influence and hence, an associate (IAS 27.14–27.15 and IAS 28.8–28.9).1

The Interpretation SIC 12 deals with the question under which circumstances special purpose entities (SPEs) have to be consolidated. SPEs are created to accomplish a narrow and well-defined objective to the benefit of another entity (= sponsor). Examples of such an objective are to effect a lease, research and development activities or securitization of financial assets (SIC 12.1).

If the sponsor owns more than 50% of the shares of the SPE there is a rebuttable presumption (IAS 27.13) that this constitutes control. Hence, it is not necessary to apply SIC 12. However, in many cases the sponsor owns less than 50% of the shares of an SPE because it is intended to relieve the sponsor's consolidated financial statements, for example, by avoiding presenting doubtful receivables or liabilities and making related disclosures. In such cases SIC 12 is of particular importance.

SIC 12 contains criteria that may indicate that an entity controls an SPE and consequently has to consolidate the SPE. However, some of these criteria are too vague to use them to determine whether consolidation is necessary. Thus, the question of whether there is control is regularly determined on the basis of the risks and benefits. This means that the SPE is consolidated when the entity is exposed to a majority of the risks and benefits of the SPE (under the presumption that the risks and benefits are allocated symmetrically) (SIC 12.10).

2.2 Balance Sheet Date of the Consolidated Financial Statements and Diverging Balance Sheet Dates of Subsidiaries

The balance sheet date of the consolidated financial statements is the balance sheet date of the parent. Subsidiaries can be consolidated on the basis of financial statements with a different balance sheet date provided that the difference between the balance sheet dates is no more than three months, and that it is impracticable to prepare additional financial statements for the subsidiary. When the financial statements of a subsidiary are prepared at a date different from that of the parent's financial statements, adjustments have to be made for the effects of significant transactions or events (IAS 27.22–27.23).

2.3 Preparing the Consolidated Financial Statements

2.3.1 Overview

The following steps are necessary in preparing the consolidated financial statements (IAS 27.18–27.21 and 27.24–27.29):2

Step (4) is explained in more detail in the following sections of this chapter. With regard to step (3) we refer to the chapter on IFRS 3. Different aspects of non-controlling interests are described in this chapter and in the chapter on IFRS 3.

2.3.2 Elimination of Intragroup Receivables and Liabilities

A group can have neither liabilities to nor receivables from itself. Hence, intragroup receivables and liabilities have to be eliminated (elimination entry on consolidation: “Dr Liability Cr Receivable”).

The accounting treatment of assets and liabilities may differ under IFRS. This situation exists in the following examples:

- At the beginning of 01, subsidiary A grants a loan to subsidiary B. Consequently, A recognizes a receivable whereas B recognizes a liability. It is assumed that B encounters significant financial difficulty, at the end of 01. Thus, A recognizes an impairment loss for its receivable. However, the measurement of the liability in B's financial statements is normally not affected. For this reason, the carrying amount of the receivable differs from the carrying amount of the liability on Dec 31, 01. Therefore, in 01, the elimination entry on consolidation is “Dr Liability Cr Receivable Cr Impairment loss.”5

- An obligation might require recognition as a provision in the debtor's financial statements, but the corresponding claim does not qualify for recognition in the financial statements of the creditor.

Furthermore, differences between the carrying amounts of receivables and the corresponding liabilities may result from different balance sheet dates.

2.3.3 Elimination of Intragroup Income and Expenses

The consolidated statement of comprehensive income presents only the income and expenses of the group. Consequently, intragroup income and expenses have to be eliminated. For example, subsidiary A may lease a machine to subsidiary B under an operating lease. A recognizes lease income and B recognizes lease expenses. These items have to be eliminated because the group (which is regarded as a single entity for consolidation purposes) cannot lease a machine to itself. Therefore, the elimination entry on consolidation is “Dr Lease income Cr Lease expense.”

2.3.4 Elimination of Intragroup Profits and Losses that are Recognized in the Carrying Amounts of Assets

Profits and losses resulting from intragroup transactions that are recognized in the carrying amounts of assets in the separate financial statements are eliminated in full. For example, in 01 subsidiary A purchases merchandise from a supplier for CU 10 which is an unrelated entity from the group's perspective. A sells the merchandise to subsidiary B for CU 12. B does not resell the merchandise in 01. Hence, the consolidated statement of comprehensive income neither includes cost of sales, nor sales revenue with respect to the merchandise since it has not yet been sold from a group perspective. The cost of purchase of the merchandise is CU 10 because this represents the amount paid by the group in order to acquire the merchandise.6

Intragroup losses may indicate an impairment that requires recognition in the consolidated financial statements (IAS 27.20–27.21).

2.3.5 Non-controlling Interests

IAS 27 and IFRS 37 both contain rules regarding non-controlling interests. Non-controlling interests represent the equity in a subsidiary not attributable, directly or indirectly, to a parent (IAS 27.4).

Non-controlling interests are presented within equity in the consolidated statement of financial position. However, they are presented separately from the equity of the owners of the parent (IAS 27.27 and IAS 1.54q).

Profit or loss and each component of other comprehensive income are attributed to the owners of the parent and to the non-controlling interests, even if this results in the non-controlling interests having a deficit balance (IAS 27.28).

When potential voting rights exist, the proportions of profit or loss and changes in equity allocated to the non-controlling interests and to the parent are determined on the basis of present ownership interests. They do not reflect the possible exercise or conversion of potential voting rights (IAS 27.19).

2.4 Acquisition and Disposal of Shares

IFRS 3 deals with the situation in which an acquirer obtains control of an acquiree in which it held an equity interest immediately before the acquisition date (business combination achieved in stages or step acquisition) (IFRS 3.41–3.42 and 3.32). Consequently, we refer to the chapter on IFRS 3 in this regard.8

By contrast, the following situations are dealt with in IAS 27:

Both (a) and (b) are accounted for as equity transactions, i.e. as transactions with owners in their capacity as owners, which means that the following procedure is necessary (IAS 27.30–27.31):

- The carrying amount of the non-controlling interests is adjusted.

- Any difference to the fair value of the consideration paid or received is recognized directly in equity (e.g. in retained earnings) and attributed to the owners of the parent.

The accounting treatment of (c) is described in the remainder of this section. In the consolidated financial statements, the disposal of the shares, which results in a loss of control, is regarded as a disposal of the individual assets (including goodwill) and liabilities of the subsidiary.

Assume that parent P holds 90% of the shares of entity E. P sells 60% of the shares. This means that P holds only 30% of the shares of E afterwards, resulting in a loss of control of P over E. The gain or loss on deconsolidation (which has to be recognized in profit or loss attributable to the parent) is calculated as follows:

| Fair value of the consideration received (i.e. for the 60% sold) | |

| + | Carrying amount of the non-controlling interest (10%) |

| + | Fair value of the investment retained in E (30%) |

| = | Value of E (100%) |

| − | Carrying amount of E's net assets (including goodwill) (100%) |

| = | Gain or loss on deconsolidation |

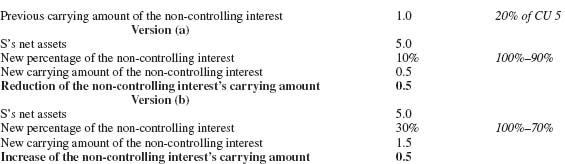

As can be seen from the table above, the parent derecognizes the carrying amount of any non-controlling interests in the former subsidiary at the date when control is lost. If the carrying amount of the non-controlling interests is positive, derecognition increases a gain on deconsolidation or decreases a loss on deconsolidation (IAS 27.34).

If a parent loses control of a subsidiary, the parent has to account for all amounts recognized in other comprehensive income in relation to that subsidiary on the same basis as would be required if the parent had directly disposed of the related assets or liabilities (IAS 27.34e and 27.35).

The treatment of goodwill on deconsolidation has to be described more precisely. It may be the case that an entity sells an operation that was part of a cash-generating unit to which goodwill has been allocated. Upon disposal, the goodwill attributable to the operation disposed of is generally calculated on the basis of the relative values of the operation disposed of and the portion of the CGU retained. The goodwill attributable with the operation disposed of is included in the carrying amount of the operation when determining the gain or loss on disposal (IAS 36.86).

The fair value of any investment retained in the former subsidiary represents the carrying amount on initial recognition of a financial asset according to IFRS 9, or the carrying amount on initial recognition when applying the equity method according to IAS 28 or IAS 31 (IAS 27.36–27.37).

If the loss of control is the result of two or more arrangements (transactions), it may be necessary under certain circumstances to treat them as a single transaction for accounting purposes (IAS 27.33). This means that the principle of substance over form9 applies.

A parent may lose control of a subsidiary (which requires deconsolidation) without disposing of shares. This could occur when the quorum for making decisions is changed from 51% to 67% or when the subsidiary becomes subject to the control of a government, court, administrator or regulator (IAS 27.32).

2.5 Investments in Subsidiaries, Jointly Controlled Entities, and Associates in Separate Financial Statements

In the entity's separate financial statements (IAS 27.4 and 27.7), investments in subsidiaries, jointly controlled entities, and associates are accounted for either (IAS 27.38):

If investments in jointly controlled entities and associates are accounted for in accordance with IFRS 9 in the consolidated financial statements, they have to be accounted for in the same way in the investor's separate financial statements (IAS 27.40). A dividend from a subsidiary, jointly controlled entity or associate is recognized in profit or loss when the right to receive the dividend is established (IAS 27.38A).

2.6 Examples with Solutions

3 IFRS 10 (ISSUED IN MAY 2011)

3.1 Introduction

In May 2011, the IASB issued IFRS 10 as well as a new version of IAS 27. Together, the two new standards supersede IAS 27 (as amended in 2008) and the Interpretation SIC 12 “Consolidation – Special Purpose Entities” (IAS 27.20 and IFRS 10.C8–10.C9).

IFRS 10 contains requirements for consolidated financial statements. The new explanations and rules of IFRS 10 relevant when assessing control are much more detailed than those of the “old” version of IAS 27. They are dealt with in Section 3.2. By contrast, the remaining rules of the “old” version of IAS 27 relating to consolidated financial statements were carried forward nearly unchanged to IFRS 10 in most areas.

IFRS 10 has to be applied in the financial statements as at Dec 31, 2013 (if the entity's reporting periods are identical with the calendar years). Earlier application is permitted by the IASB (IFRS 10.C1). IFRS 10 has to be applied retrospectively. However there are several exceptions to this principle (IFRS 10.C2–10.C6). In the European Union, there has been no endorsement as yet.22

3.2 Assessing Control

3.2.1 Overview

According to IFRS 10, an investor controls an investee if the investor has all of the following (IFRS 10.6–10.7 and 10.B2):

- Power over the investee (i.e. that the investor has existing rights that give it the current ability to direct the relevant activities of the investee). The relevant activities are the activities of the investee that significantly affect the investee's returns (IFRS 10.10 and 10, Appendix A). The following are examples of activities that may be relevant activities of a particular investee (IFRS 10.B11):

- The purchase and sale of goods or services.

- Researching and developing new products or processes.

- Determining a funding structure or obtaining funding.

- Selecting, acquiring or disposing of assets.

- Exposure or rights to variable returns from its involvement with the investee (i.e. the investor's returns from its involvement have the potential to vary as a result of the investee's performance) (IFRS 10.15 and 10.B55).

- The ability to use its power over the investee to affect the amount of the investor's returns from its involvement with the investee (link between power and returns). Hence, an investor that is an agent does not control an investee when it exercises decision-making rights delegated to it (IFRS 10.17–10.18).

When assessing control of an investee, it is necessary to consider the investee's purpose and design (IFRS 10.B5).

According to IFRS 10, it may also be necessary to consolidate only a portion of an investee in certain circumstances (IFRS 10.B76–10.B79).

It is necessary to reassess whether an investor controls an investee if facts and circumstances indicate that there are changes to one or more of the three elements of control listed in IFRS 10.7 (see above) (IFRS 10.B80–10.B85).

3.2.2 Power

Assessing power may be straightforward. This is the case when power of the investee is obtained directly and solely from the voting rights granted by equity instruments such as shares. In this situation, power is assessed by considering the voting rights from these shares. In other situations, the assessment will be more complex (IFRS 10.11).

The following are examples of rights that either individually or in combination may give the investor power over the investee (IFRS 10.B15):

- Rights in the form of voting rights (or potential voting rights) of an investee.

- Rights to appoint, remove or reassign members of the investee's key management personnel who are able to direct the relevant activities of the investee.

- Rights to appoint or remove another entity that directs the relevant activities of the investee.

- Rights to direct the investee to enter into, or veto any changes to, transactions for the benefit of the investor.

- Other rights (e.g. decision-making rights specified in a management contract) that enable the holder to direct the relevant activities of the investee.

For the purpose of assessing power, only substantive rights relating to the investee (held by the investor and others) and rights that are not protective are considered (IFRS 10.B9 and 10.B22):

- Protective rights represent rights designed in order to protect the interest of the party holding those rights without giving that party power over the entity to which those rights relate (IFRS 10, Appendix A). An example is the right of a party holding a non-controlling interest in an investee to approve the issue of equity or debt instruments (IFRS 10.B28b).

- For a right to be substantive, the holder must have the practical ability to exercise the right. The determination whether a right is substantive requires judgment, taking into account all facts and circumstances. The following are examples of factors to consider in making that determination (IFRS 10.B23):

- Whether there are any barriers that prevent the holder from exercising the rights (e.g. financial penalties and incentives that would prevent or deter the holder from exercising the rights).

- Whether the party that holds the rights (e.g. potential voting rights) would benefit from exercising them.

Usually, in order to be substantive, the rights have to be currently exercisable (IFRS 10. B24). Substantive rights exercisable by other parties may prevent an investor from controlling the investee (IFRS 10.B25).

In many cases, voting rights will indicate that the investee is controlled. However, in other situations voting rights are not the main criterion for determining whether there is control (e.g. when voting rights relate to administrative tasks only and contractual arrangements determine the direction of the relevant activities) (IFRS 10.B16–10.B17). Hence, the investor has to consider whether the relevant activities of the investee are directed through voting rights (IFRS 10.B34). If this is the case, the investor usually has power in each of the following situations if it holds more than half of the voting rights of the investee (IFRS 10. B35):

- The relevant activities of the investee are directed by a vote of the holder of the majority of the voting rights.

- A majority of the members of the governing body that directs the relevant activities of the investee are appointed by a vote of the holder of the majority of the voting rights.

An investor can have power even if it holds less than a majority of the voting rights of the investee, for example, through the following (IFRS 10.B38):

- A contractual arrangement between the investor and other vote holders.

- Rights arising from other contractual arrangements.

- Potential voting rights.

Subsequently, the treatment of potential voting rights when assessing control according to IFRS 10 is discussed in more detail. Potential voting rights represent rights to obtain voting rights of the investee, such as those arising from convertible instruments or options, including forward contracts (IFRS 10.B47).

When determining whether it has power, the investor has to consider its potential voting rights as well as the potential voting rights held by other parties. Potential voting rights are considered only if the rights are substantive (IFRS 10.B47).23 This means that the holder of potential voting rights has to consider, among others, the exercise or conversion price of the instrument. The terms and conditions of potential voting rights are more likely to be substantive when the instrument is in the money or the investor would benefit for other reasons (e.g. by realizing synergies between the investor and the investee) from exercising or converting the instrument (IFRS 10.B23c). Hence, when considering potential voting rights the investor has to consider the purpose and design of the instrument and the purpose and design of any other involvement the investor has with the investee. This includes an assessment of the terms and conditions of the instrument and of the investor's apparent expectations, motives, and reasons for agreeing to them (IFRS 10.B48).

3.2.3 Exposure or Rights to Variable Returns

Variable returns represent returns that are not fixed and have the potential to vary as a result of the performance of an investee. When assessing whether returns from an investee are variable and how variable they are, the principle “substance over form”24 applies. This means that the assessment is made on the basis of the substance of the arrangement and regardless of the legal form of the returns. For example, an entity may hold a bond with fixed interest payments. The fixed interest payments represent variable returns within the meaning of IFRS 10 because they are subject to default risk and they expose the entity to the credit risk of the issuer of the bond. The amount of variability (i.e. how variable those returns are) depends on the credit risk of the bond (IFRS 10.B56).

The following are examples of returns (IFRS 10.B57):

- Dividends and changes in the value of the investor's investment in the investee.

- Returns not available to other interest holders. For example, the investor might use its assets in combination with the assets of the investee, such as combining operating functions in order to achieve economies of scale, cost savings, sourcing scarce products, gaining access to proprietary knowledge or limiting some operations or assets to enhance the value of the investor's other assets.

3.2.4 Link Between Power and Returns

A decision maker (i.e. an entity with decision-making rights) has to determine whether it is a principal or an agent for the purpose of determining whether it controls an investee. An investor also has to assess whether another entity with decision-making rights is acting as an agent for the investor (IFRS 10.B58).

An agent is a party primarily engaged to act on behalf of and for the benefit of another party (the principal). The principal's power is held and exercisable by the agent, but on behalf of the principal. Therefore, the agent does not control the investee when it exercises its decision-making rights. The investor has to treat the decision-making rights delegated to its agent as held by itself directly for the purpose of determining whether it controls the investee (IFRS 10.B58–10.B59).

In particular, the following factors have to be considered in determining whether a decision maker is an agent (IFRS 10.B60):

- The scope of its decision-making authority over the investee.

- The rights held by other parties.

- The remuneration to which it is entitled according to the remuneration agreements.

- Its exposure to variability of returns resulting from other interests that it holds in the investee.

3.2.5 Conclusion

The explanations and rules of IFRS 10 relevant when assessing control are set out in a large number of paragraphs and address many aspects and situations. They are much more detailed than those of the “old” version of IAS 27. Nevertheless, it is unclear in some respects how the new rules for assessing control will be interpreted when applying them in practice. Moreover, application of the new rules also requires judgment in many cases (which can hardly be avoided in this area of accounting). It will be seen in the future whether they will lead to an improvement in financial reporting compared with the “old” rules of IAS 27 (as amended in 2008).

3.3 Example with Solution

4 THE NEW VERSION OF IAS 27 (ISSUED IN MAY 2011)

In May 2011, the IASB issued IFRS 10 as well as a new version of IAS 27. Together the two new standards supersede IAS 27 (as amended in 2008) and the Interpretation SIC 12 “Consolidation – Special Purpose Entities” (IAS 27.20 and IFRS 10.C8–10.C9).

The new version of IAS 27 only contains accounting and disclosure requirements for investments in subsidiaries, joint ventures, and associates in the investor's separate financial statements. These requirements were carried forward nearly unchanged from the “old” version of IAS 27. The issues relating to consolidated financial statements that were part of the “old version” of IAS 27 have been deleted because these are now within the scope of IFRS 10.

The new standard has to be applied in the financial statements as at Dec 31, 2013 (if the entity's reporting periods are identical with the calendar years). Earlier application is permitted by the IASB (IAS 27.18). In the European Union, there has been no endorsement as yet.26

1 See the chapter on IAS 28, Section 2.1.

2 The rules for the translation of the financial statements of foreign subsidiaries into the presentation currency of the consolidated financial statements are described in the chapter on IAS 21 (Section 4).

3 See the chapter on IAS 40, Section 4.1.

4 The capital consolidation is discussed in more detail in the chapter on IFRS 3.

5 See Example 2.

6 Example 4 illustrates the entries necessary in a similar situation.

7 See the chapter on IFRS 3, Section 6.3.

8 See the chapter on IFRS 3, Sections 6.1, 6.5, and 6.6, as well as Example 6.

9 See the chapter on Conceptual Framework, Section 4.2.2.

10 If IFRS 9 were not applied early, the investments would normally be measured at fair value. However, the equity instruments would be measured at cost if fair value were not determinable, reliably (IAS 39.AG80–39.AG81).

11 See the chapter on IFRS 3, Section 9 with regard to the repetition of consolidation entries of previous periods.

12 We refer to the chapter on IFRS 3 with regard to the basics of capital consolidation.

13 See the chapter on IFRS 3, Section 6.1 with regard to the computation of goodwill.

14 In this table debit entries and assets are shown with a plus sign whereas credit entries, liabilities, and items of equity are shown with a minus sign.

15 See the chapter on IAS 36, Section 7.1.

16 This does not result in a gain on disposal in P's separate financial statements because the proceeds on disposal and the carrying amount of the investment derecognized (CU 8 were paid for 80% of the shares and consequently the carrying amount of 10% of the shares is CU 1 if it is presumed that there was no control premium) are both CU 1.

17 This results in a gain on disposal of CU 1 in P's separate financial statements which is presented on a net basis (IAS 1.34a). The gain is calculated by deducting the carrying amount of 40% of the shares of CU 4 (CU 8 were paid for 80% of the shares and consequently the carrying amount of 40% of the shares is CU 4 if it is presumed that there was no control premium) from the proceeds on disposal of CU 5.

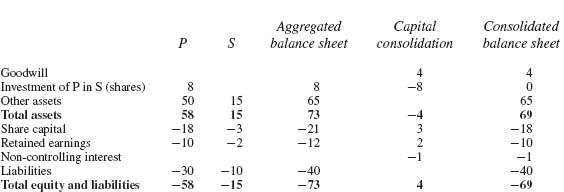

In P's separate financial statements, the account “Investment of P in S (shares)” was credited with CU 4 (see posting status for version (c)). This credit entry has to be reversed in the consolidated financial statements.

S's liabilities have to be derecognized since S is no longer a subsidiary of P.

The gain on disposal recognized in P's separate financial statements has to be derecognized.

S's other assets have to be derecognized since S is no longer a subsidiary of P.

22 See Section 1.

23 See the explanations above with regard to the term “substantive.”

24 See the chapter on Conceptual Framework, Section 4.2.2.

25 The examples are based on IFRS 10.B50.

26 See Section 1.