IFRS 2 SHARE-BASED PAYMENT

1 A GENERAL INTRODUCTION TO EMPLOYEE SHARE OPTIONS1

IFRS 2 specifies the financial reporting of share-based payment transactions. In practice, the most important types of share-based payment transactions are:

- contributions in kind in which the entity acquires goods and settles the transaction by issuing equity instruments, and

- employee share options in which the entity receives employee services and gives the employees the right (or the virtual right) to acquire equity instruments below their market price.

A share option is a contract that gives its holder the right, but not the obligation, to subscribe to the entity's shares at a fixed or determinable price. The vast majority of options are either European or American (style) options. A European option can be exercised only at the expiry date of the option, i.e. at a single pre-defined date. By contrast, an American option may be exercised on any trading day on or before expiry.

When measuring options, fair value is of particular importance. Fair value is the amount for which an asset could be exchanged, a liability settled, or an equity instrument granted could be exchanged between knowledgeable, willing parties in an arm's length transaction. Fair value of a share option consists of the following components:

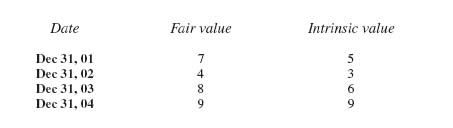

- Intrinsic value: Intrinsic value of an option to acquire one share is the positive difference between fair value of the share and the price that has to be paid to acquire this share under the option (exercise price). In this case, the option is “in the money.” For example, if fair value of the share amounts to CU 3 and the exercise price is CU 2, intrinsic value of the option to purchase the share is CU 1. Intrinsic value of this option cannot be negative because the holder of the option would not exercise it if its exercise price exceeded fair value of the share.

- Time value: The time value of an option is the difference between its fair value and its intrinsic value. It reflects the probability that the intrinsic value of the option will increase or that the option will become profitable to exercise before it expires. Time value depends on the remaining maturity and on the expected volatility of the underlying (e.g. of the shares that can be acquired under the option).

The right to exercise an option may be subject to various conditions. The following chart shows the classification of such conditions:

In the case of employee share options, different forms of vesting conditions may be stipulated:

- Service conditions require the employee to complete a specified period of service in order to be able to exercise the option.

- Performance conditions require specified performance targets to be met by the entity or the employee (e.g. a specified increase in the entity's sales or profit).

A performance condition might include a market condition. In the case of a market condition, the performance target is related to the market price of the entity's equity instruments. Examples of such performance targets are attaining a specified share price or a specified amount of intrinsic value of a share option. However, if the right to exercise the option depends on a specified increase in sales or profit instead of the market price of the entity's equity instruments, this is not a market condition.

The vesting period is the period of time during which all the specified vesting conditions are to be satisfied. The vesting date is the date on which the vesting conditions are satisfied, whereby the employee effectively becomes the holder of the option. Also, the expression “to vest” has the same meaning. The exercise date is the date on which the share option is exercised by the employee.

The ability to exercise the option may not only depend on vesting conditions, but also on non-vesting conditions. The latter do not constitute service conditions or performance conditions. Meeting non-vesting conditions is in the discretion of:

- none of the contracting parties (e.g. if meeting the condition depends on the development of an index),

- the employee (e.g. paying in a specified amount during the vesting period), or

- the entity (e.g. if cessation of the share-based payment is possible at any time).

2 SCOPE OF IFRS 2

The separate acquisition of financial assets by issuing equity instruments is not within the scope of IFRS 2 because financial instruments are not goods within the meaning of the standard (IFRS 2.5). The acquisition of goods as part of the net assets acquired in a business combination, to which IFRS 3 applies, is excluded from the scope of IFRS 2 (IFRS 2.5). However, a business combination may involve aspects that are subject to IFRS 2.

In the absence of specifically identifiable goods or services, other circumstances may indicate that goods or services have been (or will be) received, in which case IFRS 2 applies (IFRS 2.2).

3 THE ACCOUNTING OF EMPLOYEE SHARE OPTIONS

3.1 Introduction

Section 3 only deals with employee share options, i.e. only with situations in which the entity receives employee services as consideration for the granting of share options to employees. The receipt of employee services for the granting of share options usually does not result in the receipt of an asset that is recognized in the statement of financial position. Consequently, the employee services are recognized in profit or loss as employee benefits expenses (IFRS 2.7–2.8). The credit entry and the subsequent accounting depend on whether the employee options are part of an equity-settled share-based payment transaction (see Section 3.2) or of a cash-settled share-based payment transaction (see Section 3.3) (IFRS 2. Appendix A):

- Equity-settled transactions: The entity receives employee services as consideration for options to purchase shares of the entity. Consequently, when the share options are exercised, the entity either issues new shares or reacquires its own shares (treasury shares)2.

- Cash-settled transactions: The entity receives employee services by incurring a liability to transfer cash or other assets to the employee for amounts that are based on the price (or value) of the entity's shares. For example, entity E may incur a liability to make a payment to its CEO for an amount that depends upon the development of the value of the E's shares during a specified period of time. However, E will neither issue shares nor reacquire its own shares.

3.2 Equity-settled Transactions

In the case of equity-settled transactions, the employee services received by the entity are generally recognized by means of the entry “Dr Employee benefits expense Cr Equity” because usually the employee services do not result in the receipt of an asset that is recognized in the statement of financial position. IFRS 2 does not specify where in equity the credit entry should be made. In this regard, it may be necessary to take legal advice in order to comply with local legislation. In the examples in this section of the book, the credit entry is effected in a separate component of equity.

The fair value of the equity instruments granted represents the value of the employee services received by the entity. The fair value is measured at the grant date (IFRS 2.11–2.12). The grant date is the date on which the entity and the employee agree to a share-based payment arrangement. If the agreement is subject to an approval process (e.g. by shareholders), the grant date is the date when that approval is obtained (IFRS 2. Appendix A).

The fair value of the equity instruments granted is determined on the basis of market prices, if available. If market prices are not available, a valuation technique is applied. Such valuation techniques have to comply with certain requirements (IFRS 2.16–2.18 and IFRS 2. Appendix B). Normally, fair value can be estimated reliably (IFRS 2.24).

Two different cases have to be distinguished (IFRS 2.14–2.15):

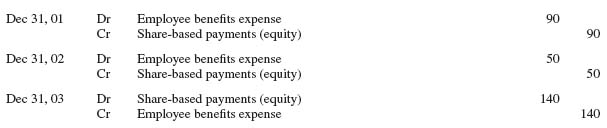

- The equity instruments granted vest immediately: In this situation the entity presumes – in the absence of evidence to the contrary – that the employee services have already been received. In this case, the services received by the entity are recognized in full on the grant date (“Dr Employee benefits expense 100% Cr Equity 100%”).

- The equity instruments granted do not vest until the employee completes a specified period of service: In this case, the entity presumes that it will receive the services to be rendered by the employee in the future, i.e. during the vesting period. The entity accounts for those services as they are rendered by the employee during the vesting period. This means that the entry “Dr Employee benefits expense 50% Cr Equity 50%” is made in each year of the vesting period if the vesting period is two years.

Vesting conditions which are not market conditions are (IFRS 2.19–2.20):

- not taken into account when estimating the fair value at the measurement date;

- taken into account by adjusting the number of equity instruments that are expected to vest in the future. For example, it may be expected after the second year of the vesting period that in total 20 equity instruments will not vest because of employees who already left or will leave the entity early. In this case, no employee services are recognized for these 20 equity instruments. If expectations change in this regard, the number of equity instruments that are expected to vest is changed.

Vesting conditions that are market conditions (e.g. achieving a target share price) have to be taken into account in determining fair value of the equity instruments granted. The employee services received by the entity have to be recognized irrespective of whether a market condition is expected to be met if it is expected that all other vesting conditions, which do not represent market conditions, will be satisfied (IFRS 2.21).

After the vesting date the amount recognized for employee services is not reversed if employee share options are not exercised. However, this does not preclude the entity from recognizing a transfer within equity, i.e. a transfer from component of equity to another (IFRS 2.23).

When an employee exercises his options, he receives shares of the entity. Therefore, the entity has to issue shares or reacquire its own shares (treasury shares) (IAS 32.33 and 32.AG36)3.

3.3 Cash-settled Transactions

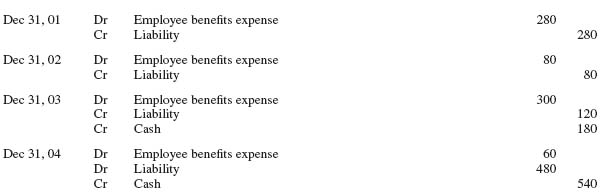

In the case of cash-settled transactions, the employee services received and the liability incurred are measured at the fair value of the liability. Until the liability is settled, fair value is remeasured at the end of each reporting period and at the date of settlement. Changes in fair value are recognized in profit or loss (IFRS 2.30–2.31).

The employee services received and the liability to pay for these services are recognized as the employees render service (IFRS 2.32). For example, entity E grants share appreciation rights to its employees on Jan 01, 01. The vesting period is three years. On Dec 31, 01 fair value of the share appreciation rights is CU 3. Consequently, on Dec 31, 01, a liability of CU 1 is recognized.

The employee services received and the liability are recognized immediately if the share options are granted for employee services that have already been received by the entity (IFRS 2.32).

4 EXAMPLES WITH SOLUTIONS

1See IFRS 2. Appendix A with regard to the definitions of the technical terms.

2See the chapter on IAS 32, Section 5 regarding treasury shares.

3See the chapter on IAS 32, Section 5 regarding treasury shares.