IAS 29 FINANCIAL REPORTING IN HYPERINFLATIONARY ECONOMIES1

1 INTRODUCTION

IAS 29 comprises rules relating to financial reporting in hyperinflationary countries. In such countries money loses purchasing power at such a rate that comparison of amounts from transactions and other events that have occurred at different times even within the same accounting period would be misleading (IAS 29.2). For most entities, the rules of IAS 29 are only relevant to their foreign operations (subsidiaries, associates or jointly controlled entities) whose functional currency is hyperinflationary. In such cases, the investee's financial statements should be adjusted before being translated and included in the investor's consolidated financial statements.

2 APPLICATION OF IAS 29 RELATING TO FOREIGN OPERATIONS: THE “7-STEP-APPROACH”

Step 1: Does hyperinflation exist?

The application of IAS 29 presupposes that there is hyperinflation. A cumulative inflation rate over three years that is approaching or exceeds 100% is the strongest indicator of hyperinflation (IAS 29.3e). An inflation rate of over 50% that is increasing massively can also be an indicator of hyperinflation.

Step 2: Determining the appropriate price index

A general price index is used with regard to the inflation adjustment. If there is more than one price index (e.g. a consumer price index (CPI) and a producer or wholesale price index (PPI or WPI)), determining the appropriate index is a matter of proper judgment (IAS 29.11 and 29.17).

Step 3: Adjustment of non-monetary items

With regard to the distinction between monetary items and non-monetary items, we refer to the chapter on IAS 21 (Section 2). Non-monetary items (e.g. inventories, property, plant, and equipment, and intangible assets including goodwill) measured on the basis of historical cost are adjusted by applying the price index to the costs of purchase or conversion (and to cumulative depreciation, amortization, and impairment losses). It is important to note that the change in the price index from the date of acquisition to the end of the reporting period is relevant and not the change in the index within the reporting period (IAS 29.15). By contrast, monetary items (e.g. cash and trade payables) are not adjusted.

Step 4: Adjustment of the statement of comprehensive income

All items in the statement of comprehensive income are expressed in terms of the purchasing power at the end of the reporting period (IAS 29.26). In the case of income and expenses that occur on a relatively regular basis during the period (this may be the case if there is no seasonal business), and an inflation rate that develops rather consistently during the period, the adjustment from the transaction date to the end of the reporting period might be possible by applying half of the inflation rate for the year.

Step 5: Gain or loss on the net monetary position

In a period of inflation, an entity holding an excess of monetary assets over monetary liabilities loses purchasing power, whereas an entity with an excess of monetary liabilities over monetary assets gains purchasing power to the extent the assets and liabilities are not linked to a price level. The gain or loss on the net monetary position is recognized in profit or loss (IAS 29.27–29.28).

In the system of double-entry book-keeping, the gain or loss on the net monetary position can be determined via a so-called “purchasing power account.” That account comprises the adjustment of all initial balances of and additions to non-monetary items and of certain items of the statement of comprehensive income (e.g. sales revenue). The account balance is the gain or loss on the net monetary position that becomes part of the statement of comprehensive income and therefore also of the statement of financial position. The balance of the purchasing power account should equal approximately the gain or loss on the net monetary position calculated by dividing the change in the net monetary position during the period by two.

Step 6: Determining the comparative figures

When the results and financial position of an entity whose functional currency is hyperinflationary are translated into a non-hyperinflationary presentation currency, comparative amounts are those that were presented as current year amounts in the relevant prior year financial statements (i.e. not adjusted for subsequent changes in exchange rates or subsequent changes in the price level) (IAS 29.34 and IAS 21.42–21.43).

Step 7: Translation into the presentation currency

After inflation adjustment, translation into the presentation currency of the group is effected according to the normal rules for foreign currency translation (IAS 29.35).

3 REPORTING PERIOD IN WHICH AN ENTITY IDENTIFIES HYPERINFLATION WHEN THE CURRENCY WAS NOT HYPERINFLATIONARY IN THE PRIOR PERIOD

In the reporting period during which an entity identifies the existence of hyperinflation in the country of its functional currency that was not hyperinflationary in the prior period, IAS 29 is applied as if the economy had always been hyperinflationary. Therefore, in relation to non-monetary items measured on the basis of historical cost, the opening statement of financial position at the beginning of the earliest period presented is restated to reflect the effect of inflation from the date the assets were acquired and the liabilities were incurred or assumed until the end of the reporting period (IFRIC 7.3).

4 EXAMPLE WITH SOLUTION2

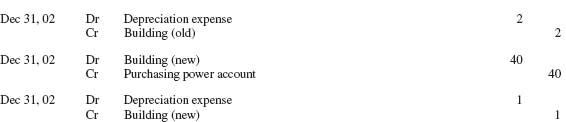

- The old building (remaining useful life: three years) is depreciated by the amount of CU 2 (on the basis of the amount indexed as at Dec 31, 01).3

- A new building (useful life: 20 years) is acquired on Jul 01, 02 for CU 80. Depreciation of CU 2 is recognized for that building.

- All of the old merchandise is sold in 02.

- On Jul 01, 02, new merchandise is acquired for CU 80. Half of the new merchandise is sold in 02.

| Separate income statement for 02 | |

| Sales revenue | 110 |

| Old merchandise sold | –30 |

| New merchandise sold | –40 |

| Depreciation expense (old building) | –2 |

| Depreciation expense (new building) | –2 |

| Other expenses | –16 |

| Profit for 02 | 20 |

- The monetary items (i.e. H's trade receivables, H's cash, and H's loan payable) are not adjusted.

- The share capital and the retained earnings as at Dec 31, 01 are multiplied by 2.

- The adjustment of the merchandise and of the buildings is explained below.

| Historical values/old index | Index as at Dec 31, 02 | |

| Balance as at Jan 01, 02 | 30 | 60 |

| + Acquisition on Jul 01, 02 | 80 | 120 |

| – Balance as at Dec 31, 02 | 40 | 60 |

| = Cost of the merchandise sold in 02 | 70 | 120 |

1 See Lüdenbach/Hoffmann, IFRS Commentary, 9th edition, 2011, Section 27, Chapter 4 with regard to the explanations and the example in this chapter of the book. The commentary cited is published in the German language.

2 In this example, the presentation specifications of IAS 1 are ignored.

3 In this example, the term CU is used to denote the currency units of the hyperinflationary currency.

4 CU 70 = CU 30 (balance as at Jan 01, 02) + CU 40 (acquisition on Jul 01, 02).

5 The unadjusted values are shown on the left.