IAS 40 INVESTMENT PROPERTY

1 THE CONCEPT OF “INVESTMENT PROPERTY”

Investment property is property (i.e. land or a building – or part of a building – or both) held (by its owner or by the lessee under a finance lease) to earn rentals or for capital appreciation or both (IAS 40.5).

Properties held for sale in the ordinary course of business are inventories and not investment property (IAS 40.5 and IAS 2.6). The business model of an entity (i.e. the entity's intentions regarding that property) is the primary criterion for classifying a property as inventory or as investment property.1

Investment property also has to be distinguished from owner-occupied property. Owner-occupied property is held (by the owner or by the lessee under a finance lease) for use in the production or supply of goods or services or for administrative purposes. If owner-occupied property is expected to be used during more than one period, it meets the definition of property, plant, and equipment (IAS 40.5 and IAS 16.6).

Property being constructed or developed on behalf of third parties does not represent investment property. Instead, revenue is recognized according to IAS 11 if the buyer is able to specify the major structural elements of the design of the real estate, and otherwise according to IAS 18 (IAS 40.9b, IAS 11.3, and IFRIC 15).

A building owned by the entity or held by the entity under a finance lease and leased out under one or more operating leases is an example of investment property (IAS 40.8c). However, if the building is leased out under a finance lease it is not investment property because, in this case, the building is no longer recognized in the lessor's statement of financial position (IAS 40.9e).

Property that is being constructed or developed for future use as investment property represents investment property (IAS 40.8e).

In the case of dual-use property, part of the property is owner-occupied property and the other part is used as an investment property. If these parts could be sold separately (or leased out separately under a finance lease) they are accounted for separately. Otherwise, the entire property represents investment property only if an insignificant portion is owner-occupied (IAS 40.10).

An entity may provide ancillary services to the occupants of a property it holds. Such a property is treated as investment property if the services are insignificant to the arrangement as a whole (IAS 40.11–40.13).

In certain cases an entity owns property that is leased to, and occupied by, its parent or another subsidiary. In the individual financial statements of the lessor the property is investment property if the criteria for investment property are met. However, the property does not qualify as investment property in the consolidated financial statements since it is owner-occupied from the group perspective (IAS 40.15).

2 RECOGNITION

The recognition criteria for the initial and subsequent cost of investment property correspond with the criteria for property, plant, and equipment in IAS 16.2

3 MEASUREMENT AT RECOGNITION

An investment property is initially measured at its cost. The cost of a purchased investment property includes its purchase price and any directly attributable expenditure (IAS 40.20–40.21).

Similar to IAS 16, the costs of purchase of investment property also include the initial estimate of the costs of dismantling and removing the item and restoring the site on which it is located, the obligation for which the entity incurs when the item is acquired (IAS 16.16c, 16.18, and 16.BC15). These costs are normally included on the basis of their present value (IAS 16.18 and IAS 37.45).

The costs of purchase of a property leased under a finance lease which is an investment property are recognized as an asset at the lower of the following amounts (IAS 40.25 and IAS 17.20):

- Fair value of the property.

- Present value of the minimum lease payments.

4 MEASUREMENT AFTER RECOGNITION

4.1 Introduction

An entity has to choose either the fair value model3 or the cost model4 as its accounting policy and the entity generally has to apply that policy to all of its investment property (IAS 40.30 and IAS 40.32A–40.32C).

The standard states that it is highly unlikely that a change from the fair value model to the cost model will result in the financial statements providing more relevant information (IAS 40.31). Therefore, normally, it is not possible to change from the fair value model to the cost model. However, a change from the cost model to the fair value model is generally possible.

4.2 Fair Value Model

An entity that chooses the fair value model generally has to measure all of its investment property at fair value after initial recognition (IAS 40.32A, 40.33, and 40.53–40.55). Fair value is the amount for which an asset could be exchanged between knowledgeable, willing parties in an arm's length transaction (IAS 40.5).

A gain or loss arising from a change in fair value is recognized in profit or loss (IAS 40.35). According to the fair value model no depreciation is recognized.

The procedure just described distinguishes the fair value model as set out in IAS 40 from the revaluation model according to IAS 16 (property, plant, and equipment)5 and IAS 38 (intangible assets).6 That is to say, according to the revaluation model, fair value changes are recognized in other comprehensive income in some situations and in profit or loss in other situations. Moreover, depreciation or amortization is generally recognized according to the revaluation model.

Fair value of an investment property is the amount for which a property could be exchanged between knowledgeable, willing parties in an arm's length transaction (IAS 40.5). Fair value is determined without any deduction for transaction costs the entity may incur on sale or other disposal (IAS 40.37).

The standard contains a hierarchy for the methods to determine fair value of an investment property.

- the items traded within the market are homogeneous;

- willing buyers and sellers can normally be found at any time; and

- prices are available to the public.”

It is recommended but not required to determine fair value on the basis of the valuation by an independent appraiser (IAS 40.32).

If an entity that applies the fair value model has previously measured an investment property at fair value, it has to continue to measure this property at fair value until disposal (or until the property becomes owner-occupied property or the entity begins to develop the property for subsequent sale as inventory) (IAS 40.55).

When the fair value model is applied, investment property under construction is also measured at fair value unless its fair value cannot be determined reliably. In the latter case, investment property under construction is measured at cost according to the cost model of IAS 16 (IAS 40.8e and 40.53).

The entity's statement of financial position may include a decommissioning, restoration, or similar provision for a particular investment property. If the amount of the provision were deducted from the fair value of the investment property, the obligation would be taken into account twice in the statement of financial position. Consequently, the obligation must not be taken into account, when determining fair value of the investment property. Changes in such provisions are treated in the following way when applying the fair value model:

- The periodic unwinding of the discount is recognized in profit or loss as a finance cost.

- If the change in measurement is due to a change in the discount rate, it is recognized as a finance expense or as finance income. If the change of the provision is due to a change in the estimated timing or amount of the outflow of resources, it is presented in the line item other operating expenses or other operating income.

4.3 Cost Model

If the entity measures its investment properties after recognition according to the cost model, the rules of IAS 16 apply (IAS 40.56) and consequently also the rules of IAS 36 for impairment testing (IAS 16.63). However, investment properties that are classified as held for sale (or are included in a disposal group that is classified as held for sale) in accordance with IFRS 5 have to be measured according to that standard (IAS 40.56).

Changes in existing decommissioning, restoration, and similar liabilities in respect of an investment property measured according to the cost model are treated in the same way as in the case of property, plant, and equipment measured according to the cost model.7

According to the cost model it is necessary to determine fair values in order to comply with the disclosure requirements of IAS 40. If it is not possible to determine fair values reliably, other disclosures are required (IAS 40.32, 40.53, and 40.79e).

5 DERECOGNITION

An investment property has to be derecognized on disposal. Disposal may be achieved through sale or by entering into a finance lease. An investment property is also derecognized when the investment property is permanently withdrawn from use and no future economic benefits are expected from its disposal (IAS 40.66–40.67). The difference between the net disposal proceeds and the carrying amount of the asset is recognized in profit or loss unless IAS 17 requires otherwise on a sale and leaseback8 (IAS 40.69).

6 PRESENTATION

Gains and losses on disposal are presented on a net basis in the statement of comprehensive income, which means that the net disposal proceeds and the carrying amount of the asset are offset (IAS 1.34a and IAS 40.69).

When the fair value model is applied, gains from fair value adjustments (fair value gains) are not offset with fair value losses in the statement of comprehensive income if these gains and losses are material. In a similar way, gains on disposal are not offset with losses on disposal (IAS 1.35).

7 EXAMPLES WITH SOLUTIONS

References to Other Chapters

Examples relating to the cost model and to impairment when the cost model is applied are illustrated in the chapters on IAS 16 and IAS 36. Regarding the accounting treatment of decommissioning, restoration, and similar liabilities under the cost model, we refer to the chapter on IAS 16 (Sections 3 and 4.4, as well as Example 4).

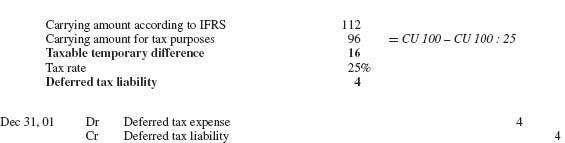

| Dec 31, 01 | 112 |

| Dec 31, 02 | 112 |

| Dec 31, 03 | 96 |

| Dec 31, 01 | 450 |

| Dec 31, 02 | 300 |

| Dec 31, 03 | 150 |

| Dec 31, 04 | 0 |

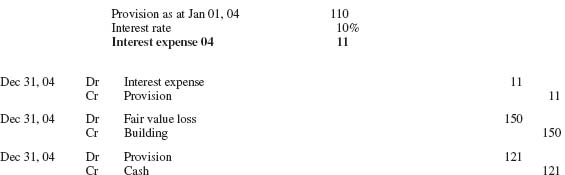

| Provision as at Dec 31, 03 (CU 146.41) | 133.1 | CU 100 · 1.13 or CU 146.41 : 1.1 |

| Provision as at Dec 31, 03 (CU 121) | 110.0 | CU 121 : 1.1 |

| Reduction in the provision | 23.1 |

1 See also KPMG, Insights into IFRS, 6th edition, 3.4.60.30.

2 See the chapter on IAS 16, Section 2.

3 See Section 4.2.

4 See Section 4.3.

5 See the chapter on IAS 16, Section 4.1.

6 See the chapter on IAS 38, Section 5.1.

7 See the chapter on IAS 16, Section 4.4.

8 See the chapter on IAS 17, Section 6.

9 See KPMG, Insights into IFRS, 7th edition, 3.4.60.30.

10 See the chapter on IAS 12 regarding deferred tax.

11 See the chapter on IAS 12, Section 3.1.