IAS 36 IMPAIRMENT OF ASSETS

1 INTRODUCTION AND SCOPE OF IAS 36

IAS 36 contains rules with regard to the impairment and the reversal of impairment losses of specific assets. For the purpose of consolidated financial statements, the scope of IAS 36 mainly comprises items of property, plant, and equipment (IAS 16), intangible assets including any goodwill resulting from a business combination (IAS 38 and IFRS 3), and investment property measured according to the cost model (IAS 40) (IAS 36.2–36.5). The rules of IAS 36 relating to the quantitative impairment test also apply to investments in associates and jointly controlled entities accounted for using the equity method. However, in these cases, a simplified calculation is possible (IAS 28.31–28.34, IAS 31.38, and 31.40).1

An impairment loss is recognized if the carrying amount of an asset (after deduction of depreciation or amortization for the period) exceeds its recoverable amount. The recoverable amount of an asset is the higher of its value in use (present value of the future cash flows expected to be derived by the entity from the asset) and its fair value less costs to sell (amount obtainable from the sale of an asset in an arm's length transaction between knowledgeable, willing parties, less the costs of disposal).

In practice, it is often not possible to determine the future cash inflows generated by an individual asset on a rational basis, which would be necessary for calculating its value in use. For example, entity E produces (among others) product P. The machines and the factory building are employed in the production of P, as well as in the production of other products. It is therefore not possible to state to which extent the cash inflows from the sale of P are generated by each machine, by the factory building, by E's administrative building, etc. However, it is possible to allocate the cash inflows from the sale of P (and of other products) to the group of assets (which consists of the different machines, the buildings, etc.) as a whole. Such a group of assets to which cash inflows can be allocated and for which value in use can consequently be determined is referred to as a cash-generating unit (CGU). According to the Standard, a CGU is the smallest identifiable group of assets that generates cash inflows that are largely independent of the cash inflows from other assets or groups of assets (IAS 36.6. 36.59, 36.66–36.67, and 36.104).

2 WHEN TO TEST FOR IMPAIRMENT

The recoverable amount has to be calculated if there is an indication that an asset or a CGU is impaired (triggering event) (IAS 36.8). Whether such an indication exists is assessed at the end of each reporting period (IAS 36.9). The following are examples of such indications (IAS 36.12–36.16):

- The asset's market value has decreased significantly more than would be expected as a result of the passage of time or normal use.

- Evidence is available of physical damage or obsolescence of an asset.

- Evidence is available from internal reporting which indicates that the economic performance of an asset is, or will be, worse than expected.

The concept of materiality may be helpful in identifying whether the recoverable amount needs to be estimated. For example, if previous calculations show that an asset's or CGU's recoverable amount was significantly greater than its carrying amount, it is not necessary to re-estimate the recoverable amount if no events have occurred that could have eliminated that difference (IAS 36.15–36.16).

Irrespective of whether there is an indication of impairment (i.e. irrespective of whether there are triggering events), the recoverable amount always has to be calculated annually for the following assets or CGUs (IAS 36.10 and 36.90):

- Intangible assets with indefinite useful lives.2

- Intangible assets not yet available for use.

- A CGU to which goodwill (acquired in a business combination)3 has been allocated.

The calculation of the recoverable amount for an intangible asset or for CGUs just described may be performed at any time during an annual period, provided that the test is performed at the same time every year. Different intangible assets or CGUs may be tested for impairment at different times. However, if some or all of the goodwill allocated to a CGU was acquired in a business combination during the current annual period, or if such an intangible asset was initially recognized during the current annual period, the recoverable amount has to be calculated for that CGU or intangible asset before the end of the current annual period (IAS 36.10, 36.90, and 36.96).

3 WHEN TO REVERSE AN IMPAIRMENT LOSS

At the end of each reporting period it is necessary to assess whether there is any indication that an impairment loss recognized in prior periods for an asset (other than goodwill) no longer exists or has decreased. This applies equally to a CGU. If there is such an indication, the recoverable amount has to be calculated (IAS 36.110). The examples of indications in the standard of a possible decrease of an impairment loss (IAS 36.111) mainly mirror the indications of a possible impairment loss in IAS 36.12 (IAS 36.112).

4 DETERMINING THE RECOVERABLE AMOUNT FOR AN INDIVIDUAL ASSET OR FOR AN ASSET'S CGU?

The recoverable amount has to be calculated for an individual asset, if possible. The recoverable amount cannot be determined for the individual asset if both of the following criteria are met (IAS 36.22 and 36.66–67):

- The asset's value in use cannot be estimated to be close to its fair value less costs to sell.

- The asset does not generate cash inflows that are largely independent of those from other assets.4

In such cases, value in use and thus the recoverable amount, can be determined only for the asset's CGU, unless the asset's fair value less costs to sell exceeds its carrying amount (IAS 36.22 and 36.66–67). In the latter case, the asset is not impaired (IAS 36.19).

In most cases, an asset is only able to generate cash inflows together with other assets.5 Consequently, impairment tests are normally conducted on the level of CGUs and not on the level of individual assets. In the case of assets rented to others, impairment tests are possible for the individual assets.

A CGU is the smallest identifiable group of assets that generates cash inflows that are largely independent of the cash inflows from other assets or groups of assets (IAS 36.6). Cash inflows are inflows of cash and cash equivalents received from parties external to the reporting entity. In determining whether cash inflows from an asset (or group of assets) are largely independent of the cash inflows from other assets (or groups of assets), various factors are considered, including the following (IAS 36.69):

- How management monitors the entity's operations (such as by product lines or geographic criteria).

- How management makes decisions about continuing or disposing of the entity's assets and operations.

A CGU may be a product line, a plant, a business operation, a geographical area, or a reportable segment as defined in IFRS 8 (IAS 36.130d).

If an active market exists for the output produced by an asset or by a group of assets, it is likely that that asset or group is a CGU. This applies even if some or all of the output (e.g. products at an intermediate stage of a production process) is used internally. Consequently, what is critical is regularly the existence of an active market for the output, irrespective of whether this output is actually sold there (IAS 36.70–36.71, 36.IE6, and 36.IE12). An active market is a market that meets all the following criteria (IAS 36.6):

- The items traded within the market are homogeneous.

- Willing sellers and buyers can normally be found at any time.

- Prices are available to the public.

5 DETERMINING THE RECOVERABLE AMOUNT

5.1 General Aspects

It is not always necessary to determine both an asset's or CGU's fair value less costs to sell and its value in use. If either of these amounts exceeds the asset's or CGU's carrying amount, the asset or CGU is not impaired and it is not necessary to estimate the other amount (IAS 36.19).

If it is not possible to determine fair value less costs to sell, value in use may be used as the recoverable amount (IAS 36.20). However, fair value less costs to sell can only be used as the recoverable amount if it is appropriate to assume that value in use does not significantly exceed fair value less costs to sell (IAS 36.21–36.22 and 36.67).

In some cases, estimates, averages, and computational short cuts may provide reasonable approximations of the detailed computations illustrated in IAS 36 for determining value in use or fair value less costs to sell (IAS 36.23).

5.2 Fair Value Less Costs to Sell

Fair value less costs to sell is the amount obtainable from the sale of an asset or of a CGU in an arm's length transaction between knowledgeable, willing parties, less the costs of disposal. The costs of disposal are incremental costs directly attributable to the disposal of an asset or of a CGU, excluding income tax expense and finance costs. However, costs of disposal recognized as a liability are not deducted in determining fair value less costs to sell (IAS 36.6 and 36.28).

IAS 36 specifies a measurement hierarchy for determining fair value less costs to sell (IAS 36.25–36.27):

- The best evidence of fair value less costs to sell is a price in a binding sale agreement in an arm's length transaction.

- If there is no binding sale agreement but an asset is traded in an active market, fair value is the asset's market price on that market. When current bid prices are unavailable, the price of the most recent transaction may provide a basis from which to estimate fair value.

- If there is no binding sale agreement or active market, fair value less costs to sell is based on the best information available. In determining fair value in such situations, the outcome of recent transactions for similar assets within the same industry is considered. Fair value less costs to sell does not reflect a forced sale unless the entity is compelled to sell immediately (IAS 36.27). If fair value less costs to sell is determined using discounted cash flow projections, additional disclosures are necessary under certain circumstances (IAS 36.134e). It is important to note that fair value reflects the market's expectation and not the entity's expectation of the present value of the future cash flows (IAS 36.BCZ11).

- Replacement cost techniques must not be applied when measuring fair value less costs to sell according to IAS 36 (IAS 36.BCZ29).

5.3 Value in Use

5.3.1 Introduction

Value in use of an asset or of a CGU is calculated by discounting the future cash inflows and outflows from continuing use and from the ultimate disposal with the appropriate discount rate (IAS 36.31). The following elements are reflected in the calculation of value in use (IAS 36.30 and 36.A1):

There are two approaches to computing value in use (IAS 36.A2):

- Traditional approach: Adjustments for factors (b) to (e) are embedded in the discount rate.

- Expected cash flow approach: Factors (b), (d), and (e) cause adjustments in arriving at risk-adjusted expected cash flows.

It is important to note that interest rates used to discount cash flows have to reflect assumptions that are consistent with those inherent in the estimated cash flows. This means that interest rates must not reflect risks for which the cash flows have been adjusted. Otherwise, the effect of some presumptions would be double-counted (IAS 36.56, 36.A3, and 36.A15).

5.3.2 Estimating the Future Cash Flows

Cash flow projections have to be based on reasonable and supportable presumptions, whereby greater weight has to be given to external evidence (IAS 36.33a and 36.34). Moreover, cash flow projections have to be based on the most recent financial budgets/forecasts approved by management. Projections based on these budgets/forecasts have to cover a maximum period of five years, unless a longer period can be justified (IAS 36.33b and 36.35). Cash flows beyond the period covered by the most recent budgets/forecasts have to be determined by extrapolating the projections based on the budgets/forecasts. In doing so, a steady or declining growth rate is used unless an increasing rate can be justified (IAS 36.33c, 36.36, and 36.37).

The future cash flows include (IAS 36.39, 36.41, 36.51, and 36.52):

- cash inflows from continuing use of the asset or CGU,

- cash outflows necessary to generate these cash inflows (including overheads that can be directly attributed, or allocated on a reasonable and consistent basis, to the use of the asset or CGU), and

- net cash flows, if any, to be received (or paid) for the disposal of the asset or CGU at the end of its useful life.

To avoid double-counting, cash flows do not include cash outflows that relate to obligations that have been recognized as liabilities (e.g. pensions) (IAS 36.43b).

Cash outflows include those for the day-to-day servicing of the asset or CGU that are necessary to maintain the level of economic benefits expected to arise from the asset or CGU in its current condition from continuing use (IAS 36.39b, 36.41, and 36.49).

The cash flows are estimated for the asset or CGU in its current condition. Hence, they do not include estimated future cash flows from future restructuring (to which the entity is not yet committed according to IAS 37) or improving or enhancing the performance of the asset or CGU. However, when the cash outflows that improve or enhance performance have already been incurred, the resulting future cash inflows are included in the cash flows. Once the entity is committed to a restructuring, the cash flows for the purpose of determining value in use (IAS 36.33b, IAS 36.44-36.48, and 36.IE44-36.IE61):

- reflect the cost savings and other benefits from the restructuring, but

- do not include the future cash outflows for the restructuring because these are already included in a restructuring provision according to IAS 37.

When a single asset consists of components with different useful lives, the replacement of components with shorter lives is part of the day-to-day servicing of the asset when estimating the future cash flows (IAS 36.49).

When a CGU consists of assets with different useful lives, all of which are essential to the ongoing operation of the CGU, the replacement of assets with shorter lives is part of the day-to-day servicing of the unit when estimating the future cash flows (IAS 36.49).

When the carrying amount of an asset does not yet include all the cash outflows to be incurred before it is ready for use (e.g. a building under construction), any further cash outflow that is expected to be incurred before the asset is ready for use is included when determining value in use (IAS 36.39b and 36.42).

Estimates of future cash flows must not include cash inflows or outflows from financing activities and income tax receipts or payments (IAS 36.50).

In estimating cash flows the effects of internal transfer prices that do not correspond to future prices that could be achieved in arm's length transactions have to be eliminated (IAS 36.70–36.71).

5.3.3 Determining the Discount Rate

When an asset-specific rate is not directly available from the market, surrogates are used in order to estimate the discount rate (IAS 36.57 and 36.A16). The following rates might be taken into account as a starting point in making such an estimate (IAS 36A17):

- The entity's weighted average cost of capital (WACC) determined using techniques such as the capital asset pricing model (CAPM).

- The entity's incremental borrowing rate.

- Other market borrowing rates.

The discount rate has to reflect current market assessments of the time value of money (represented by the risk-free rate of interest) and the risks specific to the asset or CGU for which the future cash flows have not been adjusted (IAS 36.55, 36.A1, 36.A16, and 36.A18).

The discount rate is independent of the entity's capital structure and of the way the entity financed the acquisition of the asset or CGU (IAS 36.A19). The discount rate used has to be a pre-tax rate (IAS 36.55 and 36.A20). Normally, a single discount rate is used. However, separate discount rates have to be used for different future periods where value in use is sensitive to a difference in risks for different periods or to the term structure of interest rates (IAS 36.A21).

6 DETERMINING THE CARRYING AMOUNT OF A CGU

The carrying amount of a CGU has to be determined on a basis consistent with the way the recoverable amount of the CGU is determined (IAS 36.75). The carrying amount of a CGU includes the carrying amount of the assets that can be attributed directly, or allocated on a reasonable and consistent basis to the CGU and will generate the future cash inflows used in determining the CGU's value in use. The carrying amount of a CGU does not include the carrying amount of any recognized liability unless the recoverable amount of the CGU cannot be determined without consideration of this liability. The latter situation may occur if the disposal of a CGU would require the buyer to assume the liability (IAS 36.76–36.78).

For practical reasons, the recoverable amount of a CGU is sometimes determined after consideration of assets that are not part of the CGU (e.g. financial assets) or liabilities that have been recognized. In such cases, the CGU's carrying amount is increased by the carrying amount of those assets and decreased by the carrying amount of those liabilities (IAS 36.79). However, to begin with, the assets and liabilities outside the scope of IAS 36 are measured according to the applicable standards. For example, at first inventories are written down to their net realizable value (if net realizable value is below cost) before they are added to the carrying amount of the CGU (IAS 2.9).

7 GOODWILL

7.1 Allocating Goodwill to CGUs

For the purpose of impairment testing, goodwill acquired in a business combination6 has to be allocated to each of the acquirer's CGUs or groups of CGUs that is expected to benefit from the synergies of the business combination (IAS 36.80). Consequently, the quantified synergies are used as the basis for allocating goodwill. Goodwill may also be allocated on the basis of fair values, EBIT, EBITDA, etc., if they reflect synergies approximately.

Each CGU or group of CGUs to which the goodwill is allocated as described above (IAS 36.80–36.83):

- has to represent the lowest level within the entity at which the goodwill is monitored for internal management purposes, and

- must not be larger than an operating segment (as defined by IFRS 8.5 before aggregation).

7.2 Multi-level Impairment Test

In some cases, a multi-level impairment test is necessary (IAS 36.97–36.98):

- If the assets of a CGU to which goodwill has been allocated are tested for impairment at the same time as that CGU, they have to be tested for impairment first and any impairment loss is recognized. Afterwards, the CGU to which goodwill has been allocated is tested for impairment.

- Similarly, if the CGUs constituting a group of CGUs to which goodwill has been allocated are tested for impairment at the same time as that group of CGUs, the individual CGUs have to be tested for impairment first and any impairment loss is recognized. Afterwards, the group of CGUs containing the goodwill is tested for impairment.

8 CORPORATE ASSETS

Corporate assets are assets other than goodwill that contribute to the future cash flows of at least two CGUs (IAS 36.6). Whether an asset meets the definition of a corporate asset depends on the structure of the entity. Typical examples of corporate assets are the building of a headquarters or of a division, EDP equipment or a research center (IAS 36.100). Normally, the recoverable amount of an individual corporate asset cannot be determined (IAS 36.101).

When testing a CGU for impairment, all the corporate assets that relate to the CGU have to be identified. If allocation of a portion of the carrying amount of a corporate asset to the CGU on a reasonable and consistent basis (IAS 36.102):

- Is possible, the carrying amount of the CGU (including the pro rata carrying amount of the corporate asset) is compared with its recoverable amount. Any impairment loss is recognized.

- Is not possible, at first, the carrying amount of the CGU (excluding the corporate asset) is compared with its recoverable amount. Afterwards, the smallest group of CGUs, which includes the CGU under review and to which a portion of the carrying amount of the corporate asset can be allocated on a reasonable and consistent basis, is identified. Finally, the carrying amount of the group of CGUs (including the pro rata carrying amount of the corporate asset) is compared with its recoverable amount. Any impairment loss is recognized.

9 RECOGNIZING AND REVERSING AN IMPAIRMENT LOSS7

In the case of a reversal of an impairment loss of an individual asset, the carrying amount of the asset must not be increased above the fictitious carrying amount (which is the carrying amount that would have been determined had no impairment loss been recognized for the asset in prior years) (IAS 36.117).

An impairment loss recognized for goodwill must not be reversed in a subsequent period (IAS 36.124–36.125). Even if the impairment loss was recognized in respect of goodwill in an interim financial statement, the recognition of a reversal of the impairment loss is prohibited in the following interim financial statements as well as in the annual financial statements (IFRIC 10.8).

An impairment loss determined for a CGU or group of CGUs has to be allocated to reduce the carrying amount of the assets of the unit (group of units). At first, the carrying amount of goodwill allocated to the unit (group of units) is reduced. Afterwards, the remaining impairment loss is allocated to the other assets of the unit (group of units) pro rata on the basis of the carrying amount of each asset in the unit (group of units) (IAS 36.104). Thereby, the carrying amount of an asset must not be reduced below the highest of the following amounts (floor) (IAS 36.105):

- Its fair value less costs to sell (if determinable).

- Its value in use (if determinable).

- Zero.

The amount of the impairment loss that would have been recognized as described above in the absence of the floor has to be allocated pro rata to the other assets of the unit (group of units) on the basis of their carrying amounts (IAS 36.105).

These reductions in carrying amounts are treated and recognized as impairment losses on individual assets (IAS 36.104). After the requirements described above (IAS 36.104 and 36.105) have been applied, a liability is recognized for any remaining amount of an impairment loss for a CGU only if this is required by another standard (IAS 36.108).

A reversal of an impairment loss for a CGU has to be allocated to the assets of the unit, except for goodwill, pro rata with the carrying amounts of those assets. These increases in carrying amounts are treated and recognized as reversals of impairment losses for individual assets (IAS 36.122). In allocating a reversal of an impairment loss for a CGU, the carrying amount of an asset must not be increased above the lower of the following amounts (cap) (IAS 36.123):

- Its recoverable amount (if determinable).

- The fictitious carrying amount, i.e. the carrying amount that would have been determined had no impairment loss been recognized for the asset in prior periods.

The amount of the reversal of the impairment loss that would have been allocated to one or more assets in the absence of the cap has to be allocated pro rata to the other assets of the CGU, except for goodwill (IAS 36.123).

10 NON-CONTROLLING INTERESTS

For each business combination, the acquirer generally measures any non-controlling interest in the acquiree on acquisition date either (a) at its fair value or (b) at the non-controlling interest's proportionate share in the recognized amounts of the acquiree's identifiable net assets (IFRS 3.19), which also affects goodwill (goodwill option).8

If a subsidiary with a non-controlling interest is itself a CGU, the impairment loss is allocated between the parent and the non-controlling interest on the same basis as that on which profit or loss is allocated (IAS 36.C6).

If a non-controlling interest is measured at its proportionate share of the acquiree's identifiable net assets (see above), goodwill attributable to the non-controlling interest is not recognized in the parent's consolidated financial statements. However, it is included in the recoverable amount of the related CGU. Consequently, the carrying amount of the CGU is increased (only for the purpose of impairment testing) by the goodwill attributable to the non-controlling interest. This adjusted carrying amount is then compared with the recoverable amount of the CGU (IAS 36.C4 and 36.IE65). If an impairment loss attributable to a non-controlling interest relates to goodwill that is not recognized in the parent's consolidated financial statements, that impairment loss is not recognized (IAS 36.C8).

11 EXAMPLES WITH SOLUTIONS

| Carrying amount as at Dec 31, 01 | 39 |

| Depreciation for 02 | −13 |

| Modification of the machine (Dec 28, 02) | 10 |

| (Preliminary) carrying amount as at Dec 31, 02 | 36 |

| Carrying amount as at Dec 31, 00 | 60 |

| Depreciation for 01 | −15 |

| Depreciation for 02 (fictitious) | −15 |

| Modification of the machine in 02 | 10 |

| Fictitious carrying amount as at Dec 31, 02 | 40 |

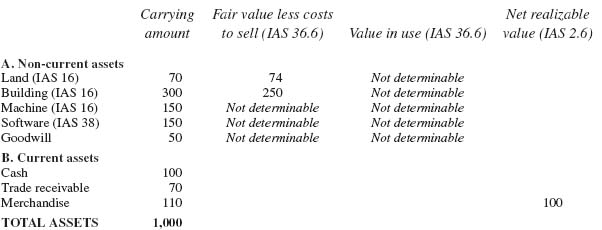

- Cash is not written down because of its nature.

- In this example it is assumed that the trade receivable is not impaired (IFRS 9.5.2.2, IAS 39.58, and 39.59) (see previous).

- The inventories are written down to net realizable value (IAS 2.9, 2.34, and IAS 1.103):

| Total assets | 1,000 |

| Provisions | −100 |

| Other liabilities | −300 |

| Net assets (preliminary) | 600 |

| Write–down of inventories | −10 |

| Net assets | 590 |

| Recoverable amount | 340 |

| Impairment loss on the CGU | 250 |

- At first, the carrying amount of goodwill is reduced from CU 50 to zero (IAS 36.104a).

- The remaining part of the impairment loss on the CGU of CU 200 (= CU 250 – CU 50) is allocated to the other assets that are within the scope of IAS 36 pro rata on the basis of their carrying amounts (IAS 36.104b). However, no impairment loss is allocated to the land because its fair value less costs to sell exceeds its carrying amount (IAS 36.19, 36.22, and 36.105).

- Its fair value less costs to sell (if determinable).

- Its value in use (if determinable).

- Zero.

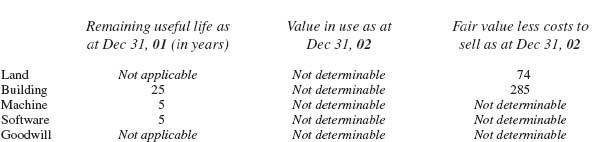

| Total of the carrying amounts from the table above | 430 |

| Cash | 100 |

| Trade receivable | 70 |

| Merchandise (after the write-down in 01) | 100 |

| Total assets | 700 |

| Provisions | −100 |

| Other liabilities | −300 |

| Net assets | 300 |

| Recoverable amount | 480 |

| Reduction in the impairment loss on the CGU | 180 |

- The recoverable amount of the asset (if determinable).

- The fictitious carrying amount, i.e. the carrying amount that would have been determined had no impairment loss been recognized for the asset in prior periods.

| CGU 1 | CGU 2 | |

| Carrying amount | 40 | 38 |

| Recoverable amount | 42 | 33 |

| Consideration transferred | 90 |

| Non-controlling interest (measured at the NCI's proportionate share of S's net assets) (20% of CU 100) | 20 |

| Value of the acquiree | 110 |

| Net assets of S (measured according to IFRS 3) | 100 |

| Goodwill recognized in the statement of financial position | 10 |

| Part of this goodwill allocated to CGU S (50%) | 5 |

| Consideration transferred | 90 |

| Non-controlling interest (fair value) | 22 |

| Value of the acquiree | 112 |

| Net assets of S (measured according to IFRS 3) | 100 |

| Goodwill | 12 |

| Goodwill allocated to CGU S | 7 |

| Goodwill allocated to other CGUs | 5 |

1 See the chapter on IAS 28, Section 2.2.2.

2 See the chapter on IAS 38, Section 5.3.

3 See the chapter on IFRS 3, Section 6.1.

4 See Section 1.

5 See Section 1.

6 See the chapter on IFRS 3, Section 6.1.

7 This section does not deal with the rules that are effective when the revaluation model of IAS 16 or IAS 38 is applied. This is due to the fact that the revaluation model is seldom applied in practice (see the chapter on IAS 16, Section 4.1 and the chapter on IAS 38, Section 5.1).

8 See the chapter on IFRS 3, Section 6.3.

9 Case (a) is based on IAS 36.67 and PwC, Manual of Accounting, IFRS 2011, 18.99.

10 Case (c) is based on IAS 36.68.

11 For simplification purposes this example only includes a small number of assets.

12 Allocation on the basis of the original carrying amounts of the machine and of the software (CU 150 each) leads to the same result as allocation on the basis of the reduced carrying amounts (CU 100 each).

13 Allocation on the basis of the original carrying amounts of the machine and of the software (CU 60 each) leads to the same result as allocation on the basis of the increased carrying amounts (CU 90 each).

14 See the chapter on IFRS 3 (Sections 6.1 and 6.3) with regard to non-controlling interests.