PREFACE

There are many excellent finance textbooks for undergraduate and MBA courses. However, to us those textbooks could benefit from offering more economic reasoning and from showing how that reasoning derives from theoretical models. On the other hand, books at the doctoral level can be too detailed and unnecessarily complex. Hence, this textbook attempts to fill a gap by providing rigorous coverage aimed at assisting undergraduate and master's level students to understand better the principles and practical application of financial economic theory. In addition, the book can serve as a supplemental reference for doctoral students in economics and finance, as well as for practitioners who are interested in knowing more about the theory and intuition behind many common practices in finance. The book selectively covers recent research findings and presents them within a structured framework. In short, the book focuses on economic principles and on putting these principles to work in the various fields of finance—financial management, investment management, risk management, and asset and derivatives pricing.

After our introductory chapter sketches the book's approach, we organize our survey in eight parts. The traditional findings of neoclassical financial economics, the subject of Part I, examine finance in a certainty world with a perfect capital market. In Part II we sketch the real-world institutional setting of financial economics, describing the essential elements of a modern financial system and providing a unified theory of how those elements function in relation to each other and to the rest of the economy. Modern financial economics is largely a study of risk management, and Part III examines tools for measuring and coping with risk. Part IV, concerned with portfolio theory and its recent developments, examines the selection and pricing of risky assets, particularly corporate securities. Continuing to examine risk management, Part V is concerned with the nature and pricing of derivative instruments. Research in modern financial economics is progressing well beyond the findings of its original neoclassical perspectives, and in recognition of this progress, Part VI examines the effects of capital market imperfections and limits to arbitrage. Part VII considers capital structure decisions in the presence of capital market imperfections, while the final part of this book, Part VIII, examines the tasks of making capital budgeting decisions under conditions of risk. Background information regarding both institutional aspects of finance and a variety of technical issues is presented in a series of 16 web appendices. Web-Appendix A to P are online only at www.wiley.com/college/fabozzi and referred to as web-Appendix throughout this book.

In order to provide additional detail, we now consider the contents of each of the eight parts. In our presentation of neoclassical financial economics in Part I, we examine the theory of consumer financial decisions, how wealth is created by investing in productive opportunities, how investors value firms, the nature and importance of firms’ financing decisions in a perfect capital market, as well as the nature and importance of firms’ investment decisions in the same neoclassical environment. This part intends particularly to emphasize the great contributions of neoclassical financial analysis, both as intellectual contributions in their own right and as a set of guidelines to financial decision making in the more complex world of market imperfections. Although financial economics is sometimes discussed as if there were on the one hand a theoretical world divorced from reality, and on the other a real world in which actual finance is studied, we contend that the two form a complementary whole. In our view, the road maps provided by neoclassical analysis provide the structure that has and will continue to guide both further research and practical applications.

In our discussion of a modern financial system's institutional nature, Part II, we introduce the notion of financial governance. We present a theory of financial system organization arguing that the three main types of financial governance—financial markets, financial intermediaries, and the internal financial decisions administered by firms—are complementary ways of overseeing financial arrangements. In the complex world beyond the domain of neoclassical economics, all three administrative mechanisms are needed to carry out financial system activity and to monitor that activity effectively. Indeed, recognizing how these mechanisms complement each other is necessary to progress beyond the findings of neoclassical economics to a broader understanding of how applied financial decisions are made in practice, as well as of their implications for the firms and investors who make them.

In our coverage of the tools for coping with risk in Part III, we discuss topics that include the microeconomic foundations of financial economics, the roles of both contingent claims analysis and contingency strategies, the nature of risk and risk management, and the recently burgeoning field of choosing risk measures.

The selection and pricing of risky assets in Part IV begins with the topics of mean-variance portfolio choice and the capital asset pricing model, then turns to the arbitrage pricing theory and factor models. Next, the guiding principles of asset pricing theory are examined, closing with a review of how these theories contribute to our current understanding of pricing corporate securities.

Part V examines the nature and valuation of derivative instruments—both derivatives with linear payoff functions (such as forward and futures contracts) and more complex types of derivatives with nonlinear payoff functions (such as options). We show how both types of contracts can be valued by assuming the absence of arbitrage opportunities. These valuation tasks can either be carried out directly or with the aid of the risk-neutral probabilities that the absence of arbitrage opportunities implies.

Although the first five parts of the book acknowledge and sketch out the roles of market imperfections, they recognize imperfections largely as requiring extensions and modifications of the neoclassical theory. Part VI turns explicitly to a more detailed recognition of capital market imperfections, the limits to arbitrage, and the detailed consequences of recognizing these complications.

The themes of recognizing and understanding complications presented by market imperfections are continued in Part VII. Here we consider why market imperfections mean that capital structure decisions matter, and the kinds of decisions that are needed to cope with these complications. In addition, we consider the implications of making financing decisions in practice, as contrasted with their implications in a neoclassical environmment. Finally, we examine the importance of financial contracting and contract terms for coping with different kinds of market imperfections. In its early days, neoclassical analysis assumed away these complications in order to develop an initial understanding of the complex financial world with which practice contends. In those earlier days, financial economics was necessarily concerned with getting the large-scale maps of the territory correct. Once those tasks had been accomplished, it became possible to grapple systematically with the effects of imperfections and hence to fill in the details of smaller-scale maps that fitted within the large-scale context.

Part VIII is a parallel to Part VII, focused this time on capital budgeting decisions rather than on capital structure issues. We consider capital expenditure plans in a risky world and the implications for capital budgeting decisions of recognizing project risk.

The web appendices provide both institutional and technical information. The first 10 appendices, Web-Appendices A through J, are concerned with institutional complications that arise in the practice of finance, and the remaining six appendices (Web-Appendices K through P) are concerned with topics of a mathematical background nature. All of the appendices are intended to provide supplementary information where we think it would be helpful, and to provide it in a form that does not distract the reader from the main presentation.

Most of the chapters in this book were written to be readily accessible to undergraduate students, and we believe that the remaining chapters are also accessible to those readers if they are willing to take on modest challenges. To us, the more challenging chapters are 12, 16, 24, and 25. We have included this material not only for the sake of completeness but also to give students a perspective on where we see the field of financial economics currently moving forward.

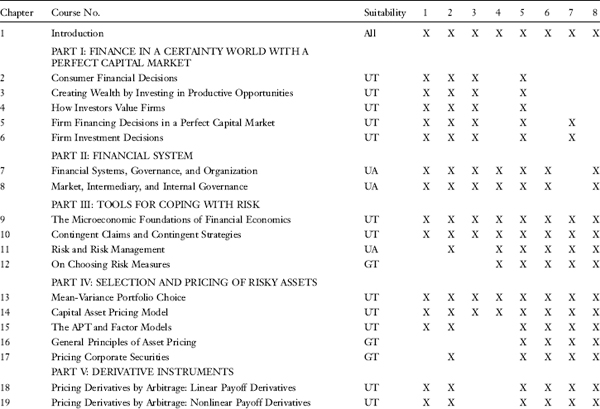

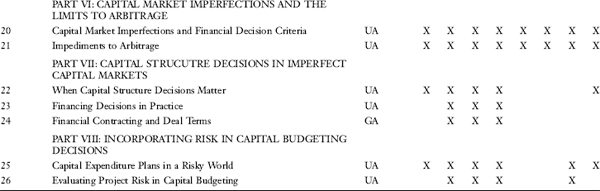

The material in the book lends itself to a number of different presentations. We provide the suitability of chapters for undergraduates and graduate students on the next page. Also provided is a list of selected chapters that can be used for various courses.

| Suitability | |

| UT | Theory suitable for undergraduates |

| UA | Applications suitable for undergraduates |

| GT | Theory suitable for graduates |

| GA | Applications suitable for graduates |

| Course | |

| 1 | One semester undergraduate or introductory graduate course in financial economics |

| 2 | Two semester undergraduate course in financial economics |

| 3 | One semester undergraduate or introductory graduate course focusing on financial management |

| 4* | One semester advanced undergraduate or advanced graduate course focusing on financial management |

| 5 | One semester undergraduate or introductory graduate course focusing on asset pricing and derivatives pricing |

| 6* | One semester advanced undergraduate or advanced graduate course focusing on asset pricing and derivatives pricing fundamentals |

| 7* | One semester quantitative finance course |

| 8* | Introductory doctoral finance course |

* Assumes students are familiar with the fundamentals