CHAPTER OBJECTIVES

When you have finished this chapter, you should be able to

- Describe the purpose and uses of the monoline dwelling forms

- Explain how coverage under the mobilehome program differs from coverage on dwellings under the homeowners program

- Identify the coverage limits on residential property available under the National Flood Insurance Program

- Explain the reasons that an individual might choose to purchase scheduled coverage under an inland marine floater

- Identify the classes of property that may be insured under the scheduled coverage endorsement to the homeowners forms

- Explain the coverage features of watercraft policies

Although the homeowners policy does an adequate job of protecting the assets of persons eligible for coverage, some properties are ineligible for a homeowners policy. In addition, although the homeowners policy protects many types of personal property owned by individuals, some property is excluded, and the coverage on other classes is limited. Finally, while the homeowners policy protects against a wide range of perils, it does not cover flood, and protection against this peril must be obtained separately. For these reasons, additional forms of coverage are often needed by persons with specialized exposure.

In this chapter, we conclude our discussion of property insurance for the individual and the family with a brief look at several additional forms of protection. The specific coverages that remain to be considered include the monoline dwelling policies, the Mobilehome Policy, the National Flood Insurance Program, and inland marine coverages designed for personal exposures. In addition, we will briefly discuss title insurance. Although title insurance is a different form of insurance coverage from those we have encountered, it represents an important part of the property owner's protection and is appropriate to include in this section. Finally, we will examine the process of purchasing property insurance and provide some additional guidelines in this area, applying the principles originally encountered in Chapter 3.

![]()

MONOLINE FIRE DWELLING PROGRAM

![]()

Although the homeowners forms represent the most attractive approach to insuring residences and their contents, many dwellings are ineligible for coverage under one of these forms. Such properties must be insured under monoline forms, which have less demanding eligibility requirements. The monoline forms used to insure residential property are referred to as dwelling forms. As monoline forms, the dwelling policies have traditionally differed from the homeowners policies in that they do not provide personal liability insurance or personal theft coverage. (Theft coverage and personal liability coverage are available under the dwelling policies by endorsement.) Although the coverage of the dwelling policies is somewhat narrower than that of the homeowners policies, the dwelling policies provide an alternative for those property owners whose buildings are ineligible for one of the homeowners forms.1

![]()

Current Dwelling Program

There are three forms in the Dwelling 2002 program, designated the Dwelling Property 1 Basic Form (DP 00 01), Dwelling Property 2 Broad Form (DP 00 02), and the Dwelling Property 3 Special Form (DP 00 03). The principal difference among the forms is with respect to the covered causes of loss. As its title indicates, the Basic Form provides the most limited coverage available on dwellings and their contents. The form makes provision for three coverage levels. The first level consists of coverage for loss by fire, lightning, and internal explosion. For an additional premium, coverage may be extended to include eight additional perils (windstorm and hail, explosion, riot or civil commotion, aircraft, vehicles, smoke, and volcanic eruption). For an additional premium, coverage is extended to include vandalism and malicious mischief. The Broad Form includes the perils of the Basic Form, plus additional named perils. The Special Form insures the dwelling and other structures on an open-perils basis and insures personal property for the same perils as the Broad Form. All three forms may be endorsed to include coverage for loss by theft. In addition, personal liability coverage may be added by endorsement.

![]()

Eligibility

The dwelling forms may be used to insure most dwelling property, including dwellings in the course of construction, whether or not owner-occupied. The dwelling program is not intended to be used for insuring farm property but may be written to cover a wide variety of other dwellings. Even trailer homes may be insured, provided they are at a fixed location and meet other eligibility requirements.2

![]()

Coverages under the Dwelling Program

![]()

There are five insuring agreements used in the Dwelling '89 policies:

| Coverage A | Dwelling |

| Coverage B | Other Structures |

| Coverage C | Personal Property |

| Coverage D | Rental Value |

| Coverage E | Additional Living Expense |

All forms include coverages A, B, C, and D, and the terminology affecting these coverages is identical under all three forms. Coverage E (Additional Living Expense) is included only in the Broad and Special Forms but is available by endorsement to the Basic Form. In addition to these coverages, each of the forms contains extensions entitled Other Coverages, which parallel the additional coverages of homeowners policies.

Differences between Dwelling Forms and Homeowners Forms Our previous analysis of the homeowners program and the forms that are contained in that program permit a somewhat briefer discussion of the dwelling program forms. In general, each of the three dwelling forms parallels the homeowners form with the same designation, subject to the following six exceptions.

- The dwelling forms do not include the peril of theft of personal property. Coverage for loss by theft is available by endorsement.

- The dwelling forms do not include personal liability coverage (as provided under Section II of the homeowners policy). Personal liability coverage is available as an option for an additional premium.

- Coverage on property away from the insured premises is limited to 10 percent of the on-premises limit under all three forms.

- In addition to the classes of personal property excluded under the homeowners forms, the Dwelling Basic Coverage Form excludes boats other than rowboats and canoes.

- The dwelling forms do not provide coverage on money or valuable papers.

- The dwelling forms do not contain the special liability limits for certain types of personal property (money, watercraft, trailers, jewelry, firearms, silverware) that are found on homeowners forms.

A special provision in the definition of personal property provides automatic transfer of coverage for 30 days at a new location, which is to be used as the insured's residence. Coverage applies at the new location and ceases to apply at the older location. During the removal period, the property at each location is covered on a pro rata basis. Property in transit is covered only to the extent of the 10 percent off-premises extension.

![]()

Endorsements to the Dwelling Program Forms

Various endorsements are available to modify the Dwelling 2002 forms. They include Automatic Increase in Insurance Endorsement, Sinkhole Collapse Endorsement, Dwelling Under Construction Endorsement, Condominium Unit-Owners Coverage Endorsement, and a Loss Assessment Endorsement, whose coverage parallels the coverage under the homeowners program.

Modified Loss Settlement Endorsement (DP 00 08) The Modified Loss Settlement Endorsement (DP 00 08) is used only with the Dwelling Property 1 Basic Form to provide coverage equivalent to Form DP-8, which was withdrawn in the 1989 revision. It modifies the loss-settlement provisions of the Basic Form to coincide with those of the Homeowners 8 Modified Coverage Form. In the event of a partial loss, payment is made on a functional cost basis, that is, the cost to replace the damaged property using common construction methods and materials. In the event of a total loss, coverage is limited to the lesser of the cost to repair the property or the market value of the property exclusive of land.

Dwelling Program Theft Endorsements A dwelling policy does not automatically include coverage for theft, but the policy may be endorsed to cover it. Coverage is available on a limited or broad-form basis.

Broad-Form Theft Coverage Endorsement The Broad-Form Theft Coverage Endorsement (DP 04 72) may be used with any dwelling policy written on a dwelling, co-op, or condominium unit that is owner-occupied. In addition, the endorsement may be written for a named insured who is a tenant in an apartment. The insured may elect on-premises coverage only or on-premises and off-premises coverage, but off-premises coverage is unavailable alone. The minimum limit for on-premises or off-premises coverage is $1000.

The Broad-Form Theft Coverage Endorsement provides essentially the same theft coverage as does the Homeowners Broad Form (HO-2). The endorsement contains its own definition of insured property. It excludes some property classes,3 and imposes dollar limits on some classes.4

Limited Theft Coverage Endorsement The Limited Theft Coverage Endorsement (DP 04 73) is designed to insure personal property of landlords located in dwellings, co-ops, condominiums, or apartments occupied by others. Coverage is limited to property owned or used by the insured or spouse, and applies only on premises. In addition to those items excluded under the Broad Form, the Limited Form excludes money and valuable papers, jewelry and furs, and silverware. The Limited Form includes the same dollar limits as the Broad Form on watercraft and their trailers, other trailers, and firearms. Finally, the Limited Theft Endorsement excludes losses caused by a tenant, roomer or boarder, members of the tenant's household, or employees of any of these persons.

Personal Liability Supplement to Dwelling Policies Unlike the homeowners policy, a dwelling policy does not automatically include liability coverage. The policy may be endorsed, however, to provide personal liability coverage.

![]()

MOBILEHOME PROGRAM

![]()

Coverage for mobilehomes may be provided by endorsement to a homeowners policy.5 The rules allow combining a Homeowners 2 Broad Form or Homeowners 3 Special Form with Mobilehome Endorsement MH 04 01. The Mobilehome Endorsement tailors the homeowners forms to accommodate the needs of mobilehome owners. This provides the same coverage for mobile homes as for conventional dwellings, modified as appropriate. In addition, the endorsement may be used with the Homeowners 4 Contents Broad Form for a mobilehome tenant.

![]()

Eligibility

A Mobilehome Policy may be written on a mobilehome designed for portability and year-round living and that is not less than 10 feet wide and 40 feet in length. These requirements are imposed to eliminate from eligibility the small trailers of a camper type that may be pulled by private passenger automobiles. Such trailers are insured under the auto policy. To be eligible for coverage under the Mobilehome Policy, the unit must be a trailer; that is, it must be a portable unit, designed and built to be towed on its own chassis, comprising a frame and wheels, and must be designed for year-round living.

![]()

Coverage on the Mobilehome

Coverage A provides protection on the mobilehome described in the declarations. The Mobilehome Endorsement amends Coverage A to include utility tanks attached to the mobilehome and permanently installed floor coverings, appliances, dressers and cabinets, and other built-in or attached items of a similar nature. When coverage is written for at least 80 percent of replacement cost value, coverage applies on a replacement cost basis. The policy can be endorsed to provide coverage on an actual cash value basis. The mobilehome endorsement adds a provision deleting the ordinance or law additional coverage of the homeowners policy to which the endorsement is attached.

A special provision related to loss settlement has been added, reflecting the difficulties that can arise in repairing a mobilehome when part of a series of panels used in the unit's construction is damaged. In the event of damage to pieces or panels of the mobilehome, the insurer agrees to pay the reasonable cost to do the following:

- Repair or replace the damaged part to match the remainder as closely as possible

- Provide an acceptable decorative effect or use as conditions warrant

So, if the repairs to the unit result in a mismatch (appearance damage), the insurer will pay for recovering (or perhaps painting?) the unit.

Coverage on Personal Property The basic limit of personal property coverage under the mobilehome program is 40 percent of the limit on the mobilehome rather than the standard 50 percent under other homeowners forms. The justification for the reduced limit of contents coverage is that a substantial number of normal contents items are “built in” in mobilehomes. The coverage on contents may be increased if the need exists.

Loss of Use Loss of Use coverage is 20 percent of the Coverage A limit.

Property Removal The Property Removal coverage is expanded to cover the expense of moving the mobile home when such movement is required to escape damage from an insured peril. The endorsement provides up to $500 for this expense, but the limit may be increased (up to $2500) for an additional premium.

Transportation/Moving Endorsement Coverage for damage to the mobilehome while being moved is covered under the Transportation/Moving Endorsement (MH 04 03). This endorsement extends the policy for 30 days to cover collision, upset, stranding, or sinking while being moved to a new location. An additional premium is required.

Lienholders Single Interest Endorsement When the mobilehome is financed by a dealer on a time-payment basis or when a lienholder is interested in the unit, special coverage protecting the interest of such parties may be provided under the Lienholders Single Interest Endorsement (MH 04 04). This endorsement, which insures the interest of the vendor or lienholder only, provides protection against loss resulting from collision, conversion, embezzlement, or secretion of the mobilehome by the insured.

![]()

FLOOD INSURANCE

![]()

Until enactment of the Housing and Urban Development Act (HUD) of 1968, which initiated the National Flood Insurance Program (NFIP), flood insurance on fixed-location property was available only on a limited basis. The HUD Act of 1968 created a federally subsidized flood insurance program, with which flood insurance became available to individuals and businesses.

![]()

General Nature of the Program

The National Flood Insurance Program (NFIP) is under the jurisdiction of the Federal Insurance and Mitigation Administration in the Federal Emergency Management Agency (FEMA). Flood policies are issued by the NFIP and private insurers, participating in the cooperative program referred to as the Write-Your-Own Program. Private insurers issue flood insurance policies on behalf of the NFIP and are reinsured 100 percent against loss. The NFIP reimburses private insurers participating in the Write-Your-Own Program for losses that are not covered by premiums and the investment income on those premiums. Coverage written by the private insurers and the federal government is sold by private insurance agents who are paid a commission for the coverage sold.

Eligible Communities The NFIP is open to any community that pledges to adopt and enforce land control measures designed to guide the community's future development away from flood-prone areas. Cities, counties, or other governmental units seeking approval for the sale of flood insurance must take the initiative and submit an official statement to FEMA indicating a need for the insurance and a desire to participate in the program. To become eligible for the insurance, the community must agree to adopt certain land use and flood control measures, including zoning ordinances that prohibit new construction in areas where there is more than a 1 percent chance of flooding each year.

TABLE 26.1 Limits on Residential Property under Federal Flood Insurance Program

Once the community has agreed to adopt the specified controls, it becomes eligible for the Emergency Program. Under this program, coverage is available on eligible properties, up to specified limits, at subsidized rates. Although the program originally provided coverage only for residential property, the eligibility has been expanded. Today, nearly all residential, industrial, commercial, agricultural, and public buildings are eligible for coverage. Subsidized coverage is available under the Emergency Program for up to $35,000 on single-family dwellings and up to $100,000 on other eligible structures, and up to $10,000 on residential contents and $100,000 on nonresidential contents. A community enters the Regular Program when the detailed flood risk study has been completed (or waived by FEMA), and the community adopts floodplain management ordinances. Increased amounts of coverage are available once the community enters the Regular Program, and the rates vary with the areas' loss probability. An individual in an area with a low risk of flooding and no prior loss experience is eligible for a Preferred Risk Policy with premiums that start at $129 per year. Rates under the Regular Program are actuarially determined. The amounts of coverage under the Emergency Program and the Regular Program are summarized in Table 26.1.

Rate Maps The additional amounts of insurance available under the Regular Program are not at subsidized rates but are actuarial rates calculated to consider the loss probability in the community. Maps of participating communities indicate the flood hazard degree so actuarial premium rates can be assigned on properties. The initial map of a community is known as the Flood Hazard Boundary Map, and the official map detailing the actuarial risk for the community is called the Flood Insurance Rate Map (FIRM).

Other Important Provisions Over the years, Congress has made several attempts to encourage individuals to purchase flood insurance. In 1973, amendments to the National Flood Insurance Act required individuals in Special Flood Hazard Areas to purchase flood insurance as a condition of receiving any federal financial assistance for acquisition or construction.6 This means that property owners in those communities where flood insurance is available and whose property is located in a Flood Hazard Area must purchase flood insurance to qualify for federal loans or for federally assisted or insured loans (VA, FHA, and so on).

Following the floods of 1993, when many homeowners were found lacking flood insurance, the National Flood Insurance Reform Act of 1994 gave lenders the responsibility of ensuring flood insurance was purchased. Federally regulated lenders and federal agency lenders must require flood insurance on properties in Special Flood Hazard Areas when making, increasing, extending, or renewing a loan, and the coverage must be maintained for the loan's term. More recently, the Flood Insurance Reform Act of 2012 (discussed later) increased the civil penalties on lenders that fail to require flood insurance.

![]()

The Flood Insurance Policy

The Dwelling Form of the Standard Flood Insurance Policy is designed for one-family to four-family noncondominium residential dwellings and for a single-family unit in a condominium building. It is a simplified language form that generally follows the format of contracts used by private insurers for property insurance coverage. A number of significant differences, outlined next, are dictated by the nature of the flood peril.

Protection under the flood insurance policy is provided under four items, designated Coverages A, B, C, and D, which insure the dwelling, personal property, debris removal, and other loss avoidance measures, and increased cost of compliance due to a state or local floodplain management law or ordinance. The debris removal coverage is included in the coverage limit applicable to the property insured although it is set forth in a separate insurance agreement.

Insurance Agreement The dwelling flood policy provides coverage for “direct physical loss by or from flood” as defined in the contract. Flood is defined in the policy as the following:

- A general and temporary condition of partial or complete inundation of two or more acres of normally dry land area or of two or more properties (at least one of which is your property) from the following:

- Overflow of inland or tidal waters

- Unusual and rapid accumulation or runoff of surface waters from any source

- Mudflow

- Collapse or other subsidence of land along the shore of a lake or similar body of water as a result of erosion or undermining caused by waves or currents of water exceeding anticipated cyclical levels that result in a flood as defined in (1.a) above.

Flood must be a general condition. This is reinforced by specific water damage exclusions that are substantially confined to the dwelling or within the insured's control. The policy also excludes water that backs up through sewers or drains, comes from a sump pump, or seeps through covered property, unless caused by a flood. This means the policy will not cover as flood damage inundations from a broken or stopped-up sewer or a faulty sump pump in the insured's basement.

The policy covers direct physical loss only. There is no coverage or loss of revenue or profits, business interruption, additional living expense, or any other economic loss.

Building Coverage The dwelling is covered, as are certain dwelling additions and extensions. In addition to the dwelling, a 10 percent extension covers a detached garage on the premises, but it does not provide an additional amount of coverage. A special provision applies if the dwelling is a manufactured (or mobile) home or travel trailer in a Special Flood Hazard Area. In that case, the dwelling must be anchored to the ground.7 The policy contains an extensive list intended to clarify which property is to be covered under Coverage A, rather than B. This includes such things as awnings and canopies, built-in dishwashers, central air conditioners, outdoor antennas, refrigerators, and permanently installed wall mirrors.

There is a specific exclusion of land values, lawns, trees, shrubs, and plants. Fences, outdoor swimming pools, and waterfront structures (e.g., docks and wharves) are excluded, as are walks, driveways, or other paved surfaces outside the building. Underground structures (like wells), hot tubs and spas that are not bathroom fixtures, and swimming pools are excluded.

Coverage for basement property is limited to specific property classes. Coverage is provided for such items as central air conditioners, sump pumps, furnaces, fuel tanks, and nonflammable insulation. The items must be installed in their functioning locations and, if necessary for their operation, connected to a power source.

Finally, flood policies exclude buildings and their contents if more than 49 percent of the building's cash value is below ground unless the lowest level is above the one in 100-year floodplain and the property is below ground for energy efficiency reasons.

Like the homeowners form, the Replacement Cost coverage under the Dwelling Flood Insurance Policy requires the structure be insured for 80 percent of its replacement cost. Replacement cost is available only for a principal residence and not for a vacation home.8

Personal Property When dwelling contents are insured under the flood policy, the coverage applies to personal property the insured or family members own. At the policyholder's option, the coverage may be extended to cover the property of guests or servants on the premises. Perhaps the most important provision in this coverage is the stipulation that contents are covered against loss by flood only while inside a fully enclosed building on the premises. There is no off-premises extension.

The policy imposes a $2500 aggregate limit on artwork and collectibles, rare books or autographed items, jewelry, furs, and business personal property. There is no coverage for recreational vehicles; currency, stamps, manuscripts, etc.; and aircraft and watercraft. Self-propelled vehicles other than those used to service the location or assist the handicapped are covered while they are located inside a building on the insured location. As with the building coverage, coverage for personal property in a basement is limited. Coverage is provided for airconditioning units, clothes washers and dryers, and freezers and food in a freezer, if they are installed in the functioning locations and connected to a power source.

Tenant's improvements and betterments are covered up to 10 percent of the coverage amount on the contents, but as with the garage extension, this is not an additional amount of insurance.

Debris Removal and Other Coverages Coverage C provides coverage for debris removal, loss avoidance measures, and condominium loss assessments. The debris removal provision pays for expense incurred to remove nonowned debris on or in insured property and owned debris anywhere. This is an important limitation. The property owner may incur significant expense in clearing away debris after a flood, but the cost is covered only to the extent of removing the covered property debris or removing other debris from the covered property. Reimbursement for debris removal is a part of, and not in addition to, the coverage provided on the dwelling or personal property.

Coverage for loss avoidance measures, such as sandbags, pumps, and labor, is limited to $1000. Coverage applies only if damage to the insured property by flood is imminent. In addition, the coverage provides up to $1000 for reasonable expenses to move insured property to protect it from flood. The policy will cover the insured property at a new location for 45 days, but the property must be inside a fully enclosed building or otherwise protected from the elements. Both of these limits are included in the limits of liability for Coverages A and B. Finally, coverage is provided, up to the Coverage A limit, for the insured's share of loss assessment charged by a condominium association as a result of direct physical loss by flood to the building's common elements.

Increased Cost of Compliance Finally, the policy provides up to $30,000 for increased costs of compliance due to a state or local floodplain management law or ordinance that affects the repair of a structure that has suffered flood damage and is insured under Coverage A. Certain eligibility requirements apply. The building must be a repetitive loss structure or have had flood damage exceeding 50 percent of the building's market value.9 The $30,000 is in addition to the Coverage A limits.

Inception of Coverage and Cancellation Provision There is a 30-day waiting period, after application and the payment of the premium, before a flood insurance policy becomes effective. This waiting period is subject to two exceptions. The waiting period does not apply to the initial purchase of flood insurance in connection with making, increasing, extending, or renewing a loan. The waiting period also does not apply to the initial purchase of flood insurance if the purchase occurs during the 13-month period following the revision or update of a Flood Insurance Rate Map (FIRM).

The policy may be canceled by the insurer only for nonpayment of premium, and even in this case, a 20 days' written cancellation notice is required. The policy may be dropped by the insured at any time, but if the insured retains title to the property, the premium for the current term is considered fully earned and there is no premium refund. If the insured disposes of the property, the return premium is calculated on a short-rate basis. Finally, if the community in which the insured property is located ceases participation in the NFIP during the term of the policy, the policy is deemed voided effective at the end of the policy year in which the cessation occurred and will not be renewed.

The Flood Insurance Reform Act of 2012 In 2012, Congress enacted major reforms to the NFIP in response to growing concern about its financial condition. The reforms were, in part, the result of lessons learned from Hurricanes Katrina and Rita, which struck the Gulf Coast in 2005 and caused over 240,000 NFIP claims. Following the hurricanes, the NFIP did not have adequate funds to cover the losses, and Congress was forced to authorize the program to borrow $20.8 billion from the U.S. Treasury.

A review of the properties insured and losses incurred under the program increased recognition of the subsidies that were being provided. The U.S. Government Accountability Office (GAO) estimated that roughly 29 percent of all properties insured by the NFIP in 2003 had subsidized premiums, with subsidies for residential dwellings averaging 60 to 65 percent of the actuarially fair premium.10 Critics pointed out that many of these subsidized properties were vacation homes in coastal areas, likely owned by relatively affluent individuals.

A second concern was the existence of repetitive loss properties, properties that had more than one loss covered by the NFIP. The GAO estimated that, in 2004, there were 49,000 repetitive loss properties among 4.4 million buildings insured by NFIP. Although only about 1 percent of properties have repetitive losses, they have historically accounted for 25 percent to 30 percent of total losses in the program.

Unfortunately, for many years, the Congress was unable to agree on a package of reforms. When the National Flood Insurance Act expired in 2008, it was temporarily extended, and between 2008 and 2012, the Congress passed 17 temporary extensions. Finally, in July 2012, President Obama signed the Flood Insurance Reform Act of 2012.

The 2012 Act extends the NFIP for five years, through September 30, 2017, and makes significant changes to address the program's solvency. Reforms specifically target premium subsidies for properties, phasing them out for second homes, business properties, severe repetitive loss properties, properties where flood losses have exceeded the property value, and substantially improved or damaged properties. Rates for these properties will increase 25 percent per year until they reach the full actuarial cost. For other properties, the annual cap on premium increases is raised from 10 percent to 20 percent. If a homeowner refuses an offer of mitigation assistance following a major disaster, full actuarial rates must be charged. In addition, premiums for policies written on previously uninsured or lapsed policies must be based on actuarial rates.

Also aimed at strengthening the financial condition of the program are requirements that NFIP premiums reflect losses in catastrophic loss years when setting premiums and that FEMA establish a reserve fund to cover high loss years. FEMA must develop detailed reporting and repayment plans whenever it borrows from the U.S. Treasury to pay NFIP losses.

One element of the program is aimed at resolving coverage disputes that were common in 2005: the so-called “slab cases,” in which the only thing left after the hurricane was the cement slab on which the house had previously stood. In such cases, it was often difficult to determine which damage was caused by the hurricane's wind (typically covered by the homeowner's policy) and which was caused by the resulting flood (covered by the flood insurance policy). Under the Consumer Option for an Alternative System to Allocate Losses (COASTAL) Act, part of the 2012 reforms, FEMA must create a system for allocating losses between wind and water in indeterminate (slab) cases, using data gathered from public and private sources by the National Oceanographic and Atmospheric Administration (NOAA).

Among the other changes, the 2012 Act clarifies that residential properties designed for five or more families, calls for updating flood insurance maps and created a Technical Mapping Advisory Council to address map modernization issues, specifies a five-year phase-in for premium increases resulting from updated flood maps, increases penalties on lenders that failed to comply with flood insurance purchase requirements, allows private insurance to meet flood insurance purchase requirements, sets minimum deductibles ranging from $1000 to $2000 depending on the property, and mandates a number of studies that may result in future changes to the program.

In spite of the significant changes, the NFIPs financial challenges are expected to continue. In October 2012, when the NFIP owed the U.S. Treasury approximately $18 billion, Hurricane Sandy hit northeastern United States, generating over 100,000 new claims. In January 2013, facing urgent warnings the program would run out of money, the Congress increased the NFIP borrowing authority by another $9.7 billion, to a total of $30.5 billion. House Financial Services Committee chairman Jeb Hensarling (R-Texas) has vowed to once again take up legislation to reform the program.

![]()

INLAND MARINE COVERAGE FOR THE INDIVIDUAL

![]()

Although the homeowners forms do an adequate job of insuring an individual's personal property, in some cases it may be desirable to specifically insure certain items of personal property under the Inland Marine Forms. Obvious examples would include items of property that are specifically excluded under the homeowners insurance, such as automobiles and recreational motor vehicles or items on which the coverage afforded under the home-owners policy is limited. For example, coverage on boats and trailers is limited to $1500, and the theft peril does not apply away from the premises. Theft coverage on jewelry and furs under the homeowners forms is limited to $1500 per loss. Perhaps not so obvious is the need for broader coverage on certain property classes than that afforded under the named-peril coverage of the homeowners or for valued coverage in the case of fine art or antiques. In this section, we will examine some of the Inland Marine Forms used as supplements to the homeowners forms in providing coverage on the property of the individual or family. In addition to the various inland marine floater forms, we will examine insurance for watercraft.

![]()

Personal Inland Marine Floaters

The term floater originally suggested a coverage that protected property while away from the insured's premises. Prior to the introduction of the home-owners forms, coverage on personal effects was provided under monoline dwelling forms, which offered only limited coverage on property away from the premises. With the introduction of the worldwide coverage of the homeowners forms, the term floater has lost some of its original significance since the coverage on personal property under the homeowners forms “floats;” that is, it provides coverage on the premises and off the premises. Nevertheless, the term floater retains its original meaning of an Inland Marine Form that provides coverage on property that by its nature is mobile.

In addition to inland marine policies being originally designed to cover property away from the insured's premises, a second feature of these forms is they generally provide coverage on an open-peril basis. This is an attractive feature since it permits the insured to obtain broad coverage on valuable items. Today, floater coverage on personal property is provided under Inland Marine Forms purchased as a separate Personal Articles Floater or by endorsement to the homeowners policy. We will not attempt to discuss all the personal floater policies available but will limit our discussion primarily to those coverages that may be included in the Homeowners Scheduled Personal Property Endorsement.

![]()

Scheduled Personal Property Endorsement

The Homeowners Scheduled Personal Property Endorsement provides open-peril coverage on nine property classes under the same terms as if separate contracts were purchased for each property type.11 Regardless of whether the coverage is purchased as a separate floater policy or by endorsement to the homeowners form, it is broad and provides an attractive means of insuring valuable personal property. The following discussion is based on the coverage under the Homeowners Scheduled Personal Property Endorsement. Coverage under this form is nearly identical with the coverage on the same items under a separate Personal Articles floater.

Valuation Options There are two versions of the Scheduled Personal Property Endorsement: one that provides coverage on a valued basis and one that provides coverage on a cash value basis or on a replacement cost basis. Under the valued basis endorsement, the amount for which an item is insured is agreed to be the item's value for loss settlement purposes.

Scope of Coverage All property is covered on an open-peril basis anywhere in the world, with exclusions for different property that reflect the nature of the property. Generally, each item insured is scheduled, with an amount of insurance applicable to each. Insurers often require an appraisal of each article before it is insured; however, the sales slip on a recently purchased garment is sufficient to establish a value.

For some property classes (jewelry, furs, cameras, and musical instruments), newly acquired property of that insured class is covered automatically, subject to a limitation of 25 percent of the insurance amount scheduled or $10,000, whichever is less, and with the requirement that the acquisitions be reported within 30 days and an additional premium paid. However, the automatic coverage applies only to the specific property classes insured at the time the property is acquired.

Personal Furs Items eligible for coverage under the insuring agreement for furs include garments made of fur or trimmed with fur. It must be an animal's dressed pelt and not a manmade fabric. As in the case of other scheduled property, an appraisal or recent sales slip is usually required, and each garment is insured for a stated value. Coverage may be written on a cash value basis, for replacement cost, or on a valued basis, depending on which of the two Scheduled Personal Property Endorsements is used.

Coverage on personal furs typifies the coverage on property insured under the Scheduled Personal Property endorsement. The breadth of the coverage is indicated by there being only four exclusions. The first eliminates loss caused by wear and tear, gradual deterioration, or inherent vice (a quality within a good that causes it to destroy itself); the second excludes loss from insects or vermin; the third excludes war; and the last excludes nuclear radiation or nuclear contamination. As indicated earlier, there is some automatic coverage for newly acquired furs, provided the insured has existing coverage for furs.

Personal Jewelry Personal jewelry is covered on a similar basis as furs. Each item must be scheduled with an amount of insurance applicable to each and the indemnity may be on its cash value, replacement cost basis, or on a valued basis. Again, an appraisal is usually mandatory, or at least some verification of the cost price must be established.

As in the case of the coverage on furs, there is a limited amount of coverage for 30 days for newly acquired property.

Silverware Another property class that may be insured under the Homeowners Scheduled Personal Property Endorsement or under a separate Inland Marine Floater is silverware. Coverage is provided on valuable silverware, silver-plated ware, and the like. The coverage is similar to that provided for jewelry as described previously. The major difference is there is no automatic coverage on additionally acquired items.

Golfer's Equipment Golfer's equipment may be insured under a separate policy, or it may be covered under the Homeowners Scheduled Personal Property Endorsement. Either form provides coverage for golfing equipment, including clubs, golf clothing (but excluding watches and jewelry), and other clothing that is contained in a locker in a clubhouse or other building used in connection with the game of golf. The description of eligible property is broad and could include a motor-driven golf cart. The coverage is on an open-peril basis for most items of property and most is written on a blanket basis. However, the coverage for golf balls is not open peril but is limited to the perils of fire and burglary.

Cameras Eligible equipment under the cameras insuring agreement includes cameras, projection machines, movable sound equipment, films, binoculars, and telescopes. As usual, the various items are scheduled and a blanket item may be included to provide coverage for miscellaneous articles such as sunshades, filters, and so on. Newly acquired property is insured automatically for 30 days but subject to a limit of 25 percent of the amount of insurance or $10,000, whichever is less. The only exclusions are those of the wear and tear variety, war, and radioactive contamination.

Fine Art and Antiques Coverage under the Fine Arts and Antiques insuring agreement is written to protect art objects, such as paintings, statuary, rare manuscripts, and antiques. The coverage is open peril with the usual exceptions. In addition to the standard open-peril exclusions of wear and tear, gradual deterioration or inherent vice, and insects or vermin, coverage on fine arts and antiques is subject to three additional exclusions: the first excludes damage caused by repairing, restoration, or retouching process; the second excludes breakage of certain fragile articles, unless the breakage is caused by specifically named perils. Fragile articles specifically listed in the contract to which the breakage exclusion applies include art glass windows, glassware, statuary, marble, bric-a-brac, and porcelains. The exclusion is not limited to these and can apply to other similar fragile articles. The specifically named perils for which coverage by breakage is provided are fire and lightning, explosion, aircraft, collision, windstorm, earthquake, flood, malicious damage or theft, and derailment of a conveyance. Coverage for breakage from causes other than these named perils is available for an additional premium. When the insured wishes to eliminate the exclusion of breakage, an entry is made in the declarations section of the endorsement.

The final exclusion applicable to antiques and fine art eliminates coverage for loss by any cause to property on exhibition at fair grounds or premises of national or international expositions unless the policy covers the premises. The purpose of this exclusion is to alert the insurer to situations in which an unexpected concentration of insured values might occur. The exclusion requires the insured to notify the insurer when property will be exposed to loss at such locations.

It is customary to insure antiques and fine arts on a valued rather than a cash value basis. Since this means the insurance company agrees to the value of each item insured and this is the value paid in the event of a loss, appraisals are usually mandatory. Some insurance companies retain art appraisers to advise them on values. Each insured item is scheduled with an applicable insurance amount. Newly acquired property is covered automatically but subject to a limit of 25 percent relative to the aggregate amount of the schedule. However, reports of additional items must be made within 90 days and the proper pro rata additional premium paid.

Postage Stamps and Rare and Current Coins The property eligible for coverage under the stamp and coin insuring agreement consists of postage stamps including due, envelope, official, revenue, match and medicine, covers, locals, reprints, essays, proofs, and other philatelic property owned by or in the custody or control of the insured, including the books, pages, or mountings. The eligible coins include rare and current coins, medals, paper money, bank notes, tokens of money, and other numismatic property owned by or in the custody or control of the insured, including coin albums, containers, frames, cards, and display cabinets in use with such collection. The property in both cases may be insured on a schedule or on a blanket basis. There are no automatic coverages of newly acquired property.

In addition to the customary exclusions, several are unique to this contract. For example, damage resulting from fading, creasing, denting, scratching, tearing, thinning, transfer of colors, or damage arising while the property is being worked on is excluded. The policy excludes any mysterious disappearance of individual stamps unless the item has been specifically scheduled or unless mounted in a volume and the page to which the stamp is attached is lost. Loss caused by shipping by mail is excluded unless it is registered mail. The policy contains a limit of no more than $250 on any unscheduled stamp, coin, pair, block, or series, and $1000 on an unscheduled coin collection. Failure on the part of the insured to schedule high-valued items can result in a significant gap in coverage.

Musical Instruments Musical instruments may be scheduled under the Homeowners Scheduled Personal Property Endorsement or insured under a separate contract, with either approach providing open-peril coverage. The only unusual condition in this coverage involves an agreement by the insured that he or she will not perform for pay unless permitted by endorsement and the payment of an additional premium. The purpose of this condition is to separate amateur and professional musicians for rating purposes. Experience indicates that the loss experience of professional musicians is worse than that of individuals who are not engaged in performing for hire.

As in the case of the fur floater, jewelry floater, and camera floater, additionally acquired property is automatically covered up to 25 percent of the amount of insurance or $10,000, whichever is less. The acquisitions must be reported within 30 days and an additional premium paid.

![]()

Insurance on Watercraft

Although homeowners policies provide some coverage on watercraft and their equipment, this coverage is limited to $1500 and excludes coverage for loss by theft away from the premises. Because of this $1500 limit, and to a lesser degree because of the theft exclusion, many boat owners will need specific coverage on their boats. In addition, boat owners need coverage for liability because of watercraft operation. Although Section II of the homeowners forms provides coverage for some liability arising out of watercraft use, the coverage is limited and applies only to smaller watercraft. Liability coverage for other watercraft must be extended by endorsement on the homeowners policy or be specifically insured under a separate contract.

Policies used to insure boats are not standardized, but they fall into two general classes: yacht policies, which are used to insure larger vessels, and boat-owners policies. The distinction between the two has blurred, but yacht policies are considered to be ocean marine coverages, whereas the Boatowners Policy was developed by combining liability coverage with an Inland Marine Form, Outboard Motor and Boat Policy.12 The complex nature of ocean marine policies in general is beyond the scope of this course, so we will focus primarily on the Boat-owners Policy.

The Boatowners Policy The Boatowners Policy is a package contract that, similar to an auto policy, provides coverage for liability, physical damage, medical payments, and uninsured watercraft. The Boatowners Policy sold by most companies includes two sections:

| Section I | Physical Damage Coverages |

| Section II | Liability Coverages |

Section I coverage includes a Perils Insured section, exclusions, and conditions applicable to Section I only. Section II includes separate insuring agreements for watercraft liability, medical expenses, and uninsured boaters.

Section I: Physical Damage Coverages Physical damage coverage on the boat is designated Coverage A in the Boatowners Policy. It includes coverage for the cash value of the described boat and motors, equipment and accessories manufactured for marine use, and any trailer described in the declarations. Coverage is on an open-peril basis, subject to the usual exclusions of wear and tear, gradual deterioration, inherent vice, and mechanical breakdown. Some policies exclude loss when the boat is used to carry persons or property for a fee, while the boat is rented to others, or while a boat (other than a sailboat) is being operated in an official race or speed contest.

Some companies include special valuation provisions. The coverage may be written on an agreed-value basis, under which the face amount of insurance is payable in the event of a total loss. Other insurers offer replacement cost coverage, similar to the replacement cost option on contents under the homeowners forms.

Section II: Liability Coverages The Section II coverages of the Boatowners Policy parallel the coverages of the Personal Auto Policy. They include the following:

- Watercraft liability

- Medical payments

- Uninsured boaters

Watercraft Liability Watercraft liability coverage provides protection up to a specified limit for claims or suits against an insured for damages because of bodily injury or property damage caused by a watercraft occurrence. The term insured under liability coverage is broadly defined and usually includes family members and other persons while operating the insured watercraft with the insured's permission.

The liability coverage excludes (1) bodily injury or property damage that is expected or intended by the insured, (2) liability of any person using a watercraft without permission, (3) damage to property owned by or in the care, custody, and control of the insured, (4) injury to persons eligible for workers compensation benefits, and (5) liability of a person engaged in the business of selling, repairing, storing, or moving watercraft. Some policies exclude liability arising out of any watercraft, other than a sailboat, while being used in any official race or speed test. Finally, the policy includes the standard war and nuclear exclusions.

Medical Payments Coverage Most boat policies include medical payments. This coverage pays for medical expenses resulting from boating accidents when a person (including the named insured and family members) is injured “in, upon, getting into or out of the insured watercraft.” The broadest policies include medical payments coverage for persons who are waterskiing.

Uninsured Boaters Coverage Uninsured watercraft coverage is a special form of accident insurance available under the Boatowners Policy as an option. It provides payment up to a specified limit, usually $10,000, when the insured or a family member suffers bodily injury caused by an uninsured boater.13

Navigation and Territorial Definitions Most policies limit usage of the insured watercraft to a specified territory. The broadest policies cover the watercraft while being operated on any inland body of water within the continental United States, Canada, and coastal waters of the same areas, up to a limit of from 10 to 25 miles. The most restrictive policies provide coverage only on a specified body of water and within a narrow perimeter around that area. Between these extremes, some policies provide coverage only in inland lakes or only in certain states, and some provide coverage options to extend coverage to areas such as the Bahamas. Many policies provide no coverage for offshore waters, such as the Gulf of Mexico.

![]()

BUYING PROPERTY INSURANCE FOR THE INDIVIDUAL

![]()

Pricing and Cost Considerations

Before discussing property insurance purchases for the individual or family, a brief review of the factors that affect the cost of such insurance seems in order. Aside from the differences in prices among companies, differences exist in cost based on the characteristics of the individual exposure.

As the reader will recall, the rate is the cost per unit of insurance. In the property field, rates are generally stated as the cost per $100 or $1000 of coverage. The premium is determined by multiplying the amount of insurance purchased by the rate. The rate varies with the scope of the perils insured against and the loss potential carried by those perils. The loss potential (i.e., the likelihood that a loss will occur and the extent of damage if one does) is a function of the property and is measured in part by the item's characteristics. For example, the type of construction is an important consideration in some perils: The rate for fire insurance is lower on a brick or masonry building than on a wood building. Rates vary with the loss experience of each locality. Again, in the case of fire insurance, rates vary with the fire protection provided by the city. Cities and towns are evaluated on certain critical factors such as the fire department and water supply and are placed in 1 of 10 classifications, numbered 1 through 10, with class-1 towns being the lowest rated and class-10 towns the highest.14 The rates for other coverages vary by locality: Extended coverage rates are higher in those areas subject to severe loss experience (e.g., from windstorms), just as crime rates are usually higher in large cities, reflecting the greater incidence of crime.

Homeowners' rates are based on three major factors: construction type, number of families, and fire protection.15 Other factors are also used, such as prior loss experience, the insured's age, and credit history. Homeowners policies use an indivisible premium concept, in which the premium is the entire package's cost, without allocation of parts of the premium to the different sections of coverage.

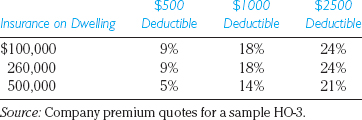

TABLE 26.2 Homeowners Deductible Premium Credits

![]()

Choosing the Form

If the residence is eligible, the building and personal property should be purchased under a homeowners policy. The choice of a particular form to be purchased is more complicated and could be subject to debate. The difference in cost between Forms 2 and 3 is so small that the choice of a Form 2 seems like false economy. Form 3 is slightly more costly than Form 2, but it provides open-peril coverage on the dwelling. If the higher cost of Form 3 is a problem, the insured might consider a higher deductible. Table 26.2 indicates the premium credits available for increased deductibles for three sample policies. The choice of a Form 3 with a $500 deductible in preference to a Form 2 with a $250 deductible follows the principles of risk management. Because each additional peril insured against reduces the possibility of an uninsured catastrophe, the insured should prefer broader coverage with a high deductible to narrower coverage with a low deductible. The insured should review the policy's deductibles to avoid surprises after a loss. Earthquake deductibles and, in hurricane-prone areas, hurricane deductibles, are likely to be expressed as a percentage of the value of the property insured.

![]()

Tailoring the Coverage under the Homeowners Policy

The greatest errors in purchasing insurance on the dwelling and its contents are usually in the insurance amount. As we have noted, the dwelling should be valued on its replacement cost. If the dwelling is relatively new, determining the replacement cost should not pose a great problem. Original cost may be inflated to current replacement cost using a construction price index. In the case of older dwelling properties, replacement cost may be calculated with the aid of a replacement cost estimator, available from many insurance agents and companies. These replacement cost estimators are simple to use and permit a reasonable approximation of a person's dwelling value by the application of stated cost factors to the various items of construction. In most cases, the cost estimators make provision for differing construction types and regional differences in cost, resulting in a fairly accurate estimate.

Even though the replacement cost condition requires that the dwelling insurance amount be 80 percent of the full replacement cost value, it is good practice to insure for 100 percent of the replacement cost value. This cushion, plus the Inflation Guard Endorsement, should prevent possible underinsurance from inflation and increases in the construction cost. A more attractive option is the guaranteed replacement cost coverage.

The homeowners forms provide coverage on the contents equal to 50 percent of the dwelling value. Yet, there is no reason to think that the value of contents will be this amount, and the insurance buyer should estimate his or her personal property value to avoid underinsurance. The problem of estimating insurable value of contents is more difficult than estimating building replacement cost. It requires an inventory of personal property, with the replacement cost value of each item. Although personal property is insured on a cash value basis under the homeowners forms, replacement cost coverage is a highly desirable option, and the policy should be endorsed to provide this coverage. Although replacement cost coverage on contents is not an essential coverage, it certainly ranks as important.

The inventory of personal property compiled in estimating the contents' value should note any valuable jewelry and furs or other items on which open-peril scheduled coverage is needed. Specific insurance should be purchased on those personal property items not covered under the homeowners policy (such as snowmobiles and golf carts) or on property with a higher value than the limits under the homeowners policy (e.g., boats or trailers valued at more than $1500).

Finally, the insured should consider adding other perils or broadening those included under the form selected. For example, the earthquake peril should be added to the homeowners form through the use of the Earthquake Damage Assumption Endorsement. It protects against a potentially catastrophic loss at a reasonable premium in most areas.

![]()

Flood Insurance

Property owners in special flood hazard areas may have no choice in the purchase of federal flood insurance. If the real estate is financed through one of the specified lending institution types, flood insurance will be required as a condition of the loan. When the property is not in a flood hazard area, the purchase of the coverage is optional with the property owner. However, nearly 20 percent of flood insurance losses occur in low-risk to moderate-risk flood zones. Even for properties not located in a high-risk area, flood insurance seems like a sound way to protect a substantial investment.

![]()

TITLE INSURANCE

![]()

Before leaving the subject of home insurance, we should briefly mention title insurance, which is a form of property insurance designed to protect against losses resulting from a defective title to land and improvements. The legal principles in the transfer of title to real estate are complicated, and because of the technicalities, it is possible for a defective title to be transferred in a real estate transaction. A person may purchase a home and after many years find that the one who conveyed the title to him or her was not the rightful owner and did not have the right to transfer the title. If a person with a superior claim to the land comes forward to exert this right, the purchaser who received the defective title may suffer.

Defects in a title may result from a number of causes, including forgery of titles, forgery of public records, invalid or undiscovered wills, or liens and encumbrances. All rights in real property, such as encumbrances, liens, and easements are generally recorded in the public records of the jurisdiction where the real estate is located. One approach to dealing with the risk of defective titles is examining these public records. When buying real estate one may protect oneself by procuring a title abstract, which is a summarized report of the title history as shown by the records, together with a report of judgments, mortgages, and similar recorded claims against the property. An attorney is generally retained to render an opinion on the abstract's accuracy and validity. The major shortcoming of this procedure is that it partially reduces the possibility of loss. Even if the abstractor or attorney is careful in the examination, defects may go undiscovered, such as a right to the property granted in a lost will or a forged transfer document that appears genuine. If the abstractor or lawyer is free from negligence, he or she cannot be held liable even if it is later determined the title was defective.16

If no other alternative is available, an examination of the abstract and a title search serve as a means of loss prevention. However, in some areas, title insurance may be available as a more attractive alternative. Title insurance companies generally insure titles only within a limited territory, a natural result of the nature of title insurance. The basic asset of the title insurance company is the abstract plant, which consists of an index of the various plots of land and their history. All transactions and transfers that affect the property's title are noted in the records of the company on a day-to-day basis, so when an application for insurance is received, most of the information regarding the property's title is on hand. When an application is received, the title insurance company engages in a title search, attempting to determine title's validity. Any defects in the title discovered by the title insurance company in its research are listed in a schedule included in the policy. A contract is then issued under which the title insurance company agrees to indemnify the insured for any loss arising out of undiscovered defects in the title. Those defects scheduled in the policy are excluded from coverage.

This guarantee by the insurer differs from most other lines of insurance in that it relates to past occurrences rather than in the future. If an undiscovered defect later causes financial loss to the insured, the insurer will pay an indemnity. The remedy to the insured in the event of a defective title is a dollar indemnification and not possession of the property. In addition, the insurer agrees to defend the buyer in the event of legal action against him or her in connection with losses included under the policy.

A single premium is payable for the title insurance policy, and it is fully earned once it is paid. The policy term is indefinite, terminating only when the property is again sold. For obvious reasons, title insurance may not be transferred to a new purchaser, but the latter may obtain a policy at a reduced reissue rate if purchase is within a short period after the previous policy was issued.

![]()

Torrens System

We will briefly mention an alternative to the system of title insurance described, the Torrens system, originally developed in Australia by Robert Torrens. It provides that title to the property is vested in the purchaser. Fees are collected at the time the title is registered and are deposited in an insurance fund. If someone can later show a property claim, the claimant is reimbursed for his or her loss out of the fund, and the title remains with the person who has registered. Many persons feel this system is superior to the alternatives discussed earlier because the purchaser of the property is granted a clear title. Torrens laws, which provide for the operations of the funds and establish the statutory basis on which they can operate, were adopted by nearly half of the states in the early part of the last century. However, few of those states implemented Torrens funds, and a number of states have since repealed their laws. By 2007, only ten states had Torrens laws, and those systems were optional.17

IMPORTANT CONCEPTS TO REMEMBER

monoline forms

Dwelling Property Basic Form

Dwelling Property Broad Form

Dwelling Property Special Form

Mobilehome Endorsement

Collision Endorsement

Lienholder's Single Interest Endorsement

golfer's floater

Scheduled Personal Property Endorsement

personal furs floater

personal jewelry floater

silverware floater

camera floater

fine arts and antiques floater

stamp and coin collection floater

musical instrument floater

personal property floater

title insurance

abstract of title

reissue rate

Torrens system

QUESTIONS FOR REVIEW

1. Briefly describe the difference in coverage on the insured's own property under Section I of the homeowners forms and the coverage on that property under the equivalent monoline dwelling forms.

2. Under what circumstances might dwelling property be insured under one of the monoline dwelling forms rather than under one of the homeowners forms?

3. Briefly describe the provisions of the flood insurance policy relating to inception of coverage and cancellation.

4. What limits of coverage are currently available to residential applicants under the National Flood Insurance Program (NFIP)?

5. In what fundamental respect is the coverage on personal property owned by the insured under the mobilehome policy different from the coverage under the homeowners policies?

6. Describe the general nature of the Lienholder's Single Interest Conversion Endorsement. Why would a mobilehome owner elect this coverage?

7. What factors, other than the value of the property insured, determine the coverage cost under the monoline dwelling policies and the homeowners forms?

8. Is an examination of the abstract of title an adequate substitute for title insurance? Why or why not?

9. List and briefly describe the coverages that may be included in the Boatowners Policy.

10. For what reasons might an individual decide to insure property under the homeowners Scheduled Personal Property Endorsement?

QUESTIONS FOR DISCUSSION

1. Most people elect the standard percentage of coverage on contents when purchasing a homeowners policy, yet there is no reason to suppose the value of contents for a given family will be equal to 50 percent of that of the dwelling. Unfortunately, few people have any idea of the true value of their contents. How do you believe one should go about determining the amount of contents coverage to be purchased? What additional benefits might be derived from the technique you recommend?

2. The cancellation provisions of the NFIP differ from those of any contracts previously encountered in the text. In what ways do these provisions seem necessary for the protection of (1) the insured and (2) the insurer?

3. Do you believe that persons owning property in the city in which you live should purchase the Earthquake Assumption Endorsement to their homeowners policies? Why or why not?

4. If you lived in an area where title insurance and a Torrens system were available, which would you elect? Why?

5. The open-peril coverage of inland marine policies is generally subject to exclusions of damage caused by wear and tear, gradual deterioration, insects, vermin, and inherent vice. For what reason are these causes of loss excluded? Are these causes of loss uninsurable or, in your opinion, are they excluded for some other reason?

SUGGESTIONS FOR ADDITIONAL READING

Abraham, Kenneth S. “The Hurricane Katrina Insurance Claims,” 93 Va. L. Rev. In Brief 157, 2007. http://www.virginialawreview.org/inbrief/2007/08/08/abraham.pdf.

Cook, Mary Ann. Personal Risk Management and Property-Casualty Insurance, Malvern, Pa.: American Institute for Chartered Property Casualty Underwriters/Insurance Institute of America, 2010.

CPCU Society's Connecticut Chapter. “Flood Insurance and Hurricane Katrina: Evaluation of the National Flood Insurance Program and Overview of the Proposed Solutions.” CPCU EJournal, September 2006.

Dumm, Randy E., David A. Macpherson, and G. Stacy Sirmans. “The Title Insurance Industry: Examining a Decade of Growth.” Journal of Insurance Regulation, Vol. 24, Issue 4 (Summer 2007).

Hull, Rabley, Monacelli, and Ewan. The Earthen Vessel: Land Records in the United States, 2010. Available at grm:thompsonreuters.com/media/14621/earthen_vessel_final.

Kunreuther, Howard. “Disaster Mitigation and Insurance: Learning from Katrina.” The Annals of the American Academy of Political and Social Science 604(1), 2006.

U.S. Government Accountability Office. Flood Insurance: Public Policy Goals Provide a Framework for Reform, GAO-11-670T, June 23, 2011.

WEB SITES TO EXPLORE

| Best's Review | www.bestreview.com |

| FloodSmart | www.floodsmart.gov/floodsmart |

| Information Information Institute | www.iii.org |

| International Risk Management Institute | www.irmi.com |

![]()

1Residential property may be ineligible for coverage under the homeowners program for various reasons. One major class of dwellings that is ineligible for homeowners coverage consists of rental property. All jurisdictions require that dwellings insured under homeowners forms must be owner occupied. Another class of ineligible dwellings consists of rooming and boarding houses. The homeowners program permits no more than two roomers or boarders per family. A residence insured under the dwelling program may have up to five roomers or boarders. Finally, many low-valued dwellings and older structures that do not meet the strict underwriting requirements of the home-owners program may be insured under the dwelling policies.

2More specifically, a dwelling policy may be used to insure a dwelling building used exclusively for dwelling purposes (except permitted incidental occupancies) with no more than four apartments and with no more than five roomers or boarders in total. Incidental occupancies permitted include business or professional occupancies and other occupancies, such as barber shops, beauty parlors, and photographers' studios, with not more than two persons at work at any one time.

3The excluded property classes are aircraft, hovercraft, motor vehicles, their equipment and accessories, property held as a sample or for sale or delivery after sale, business property, animals, birds, fish, and property of tenants who are not related to an insured. There is also an exclusion of credit cards or fund transfer cards and property separately described and specifically insured by other insurance. Some property is excluded only while away from the premises, such as property at a location owned, rented to or occupied by an insured, except while the insured is residing there, property in the custody of a laundry, cleaner, tailor, presser or dryer, and property in the mail.

4The property classes and the dollar limits are the following: $1500 on watercraft, their trailers, furnishings, equipment and outboard motors; $1500 on other trailers; $2500 on firearms; $200 on money, bank notes and precious metals; $1500 on securities and valuable papers; $1500 on jewelry, watches, and furs; and $2500 on silverware, silver-plated ware, goldware, gold-plated ware, and pewterware.

5Standard approaches to insuring mobilehomes have existed since the 1960s. In the early forms, coverage was provided for named perils based on the Homeowners Broad Form but otherwise followed the approach used in providing auto physical damage insurance. This automobile approach to insuring mobilehomes based the premium on the age and original price of the mobilehome structure. As a corollary, loss settlement was based on the structure's actual cash value at the time of loss, and losses were settled in much the same way as auto physical damage claims. ISO introduced a homeowners underwriting approach for mobilehomes in 1984. The change from the automobile approach to insuring mobilehomes to the homeowners approach rests on the premise that modern mobilehomes tend to increase in value over time, as do conventional homes, rather than depreciate, as cars do.

6A Special Flood Hazard Area is specifically designated land within a community that has at least a 1 percent chance of flooding in a year.

7There is an exception if the dwelling has been continuously insured by the NFIP at the same location since September 30, 1982.

8For a mobilehome or travel trailer that is totally destroyed, the NFIP will pay the lesser of its replacement cost or 1.5 times the cash value.

9A repetitive loss structure is one that has had previous covered flood damage during the prior 10 years, and the cost to repair the flood damage equaled or exceeded 25 percent of the building's market value at the time of each loss. The state community must have a cumulative substantial damage provision or repetitive loss provision in its floodplain management law.

10Premium subsidies are granted for properties built before 1973.

11Jewelry, furs, cameras, musical instruments, silverware, golfers' equipment, fine art (including antiques), stamp collections, and coin collections.

12When watercraft liability is insured under the homeowners policy, the boatowner may obtain broader physical damage coverage on boatsunder an inland marine Outboard Motor and Boat Policy, which provides open-peril coverage on boats and their trailers.

13Uninsured Boaters coverage is patterned after the automobile insurance coverage, uninsured motorists coverage, which is discussed in Chapter 29.

14These classifications are assigned by the Insurance Services Office (ISO).

15There are four factors used in the determination of fire rates: construction, occupancy, protection, and exposure. The fourth, exposure, which reflects the hazard created by neighboring property, is used in the rate structure for nonresidential property.

16If the abstractor or attorney was negligent, the property “owner” who suffered the loss would have a right of action and could sue for damages.

17Colorado, Georgia, Hawaii, Massachusetts, Minnesota, New York, North Carolina, Ohio, Virginia, and Washington. The Torrens system is used in the United Kingdom, Australia, and Canada.