CHAPTER OBJECTIVES

When you have finished this chapter, you should be able to

- Describe the characteristics of the various special life insurance forms discussed in the chapter

- Explain the circumstances in which each of the specialized forms may be used

- Identify the economic conditions that led to the new generation of life insurance contracts

- Identify the advantages and disadvantages of specialized life insurance policies generally

In Chapter 12, we divided available life insurance products into two broad categories: term insurance, which provides pure protection, and cash value life insurance, which combines protection and saving. In addition to this basic distinction, we distinguished between the traditional forms of life insurance (term, whole life, and endowment) and the innovative contracts introduced over the past two decades. In the innovative class, we identified universal life, variable life, and variable universal life as three additional types of contracts that may be considered “basic” today.

In addition to these contracts, life insurance companies offer a wide variety of policies that combine two or more of the basic types into one contract or that provide for an unusual pattern of premium payments. In this chapter, we will examine a few of these specialized contracts that have been developed to fill the particular needs of individuals. The discussion that follows is intended to describe the more important of these special contracts.

![]()

SPECIALIZED LIFE CONTRACTS

![]()

Many life insurance policies have been designed to fit special situations, and while they may or may not offer the same degree of flexibility as the basic contracts, they possess advantages that make them attractive in many situations. The important point to remember is that the forms discussed are combinations or modifications of the three basic types of life insurance, and the manner in which they may be combined is limited only by the imagination of the policy writers.

![]()

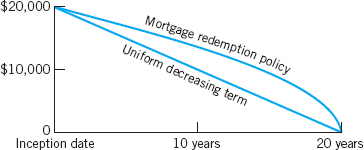

Mortgage Redemption Policy

Actually, we could call any policy mortgage insurance when it was purchased to retire the mortgage if the head of the household dies before it has been paid off. As the term is used in the insurance industry, a mortgage redemption policy (also called a mortgage protection policy) refers to a policy designed to provide protection in some amount sufficient to pay off the mortgage at any given time. Because the amount of the mortgage decreases throughout its term, a policy designed to pay off the mortgage in the event of the death of the head of the family, therefore, may also decrease in face amount over its life. The mortgage redemption policy is written on a decreasing basis for the term of the mortgage. If the policyholder lives to pay off the mortgage, the policy expires without value at the same time the need for protection has disappeared.

Although some insurers refer to nearly any decreasing term policy as their “mortgage redemption policy,” other insurers offer flexible contracts with different time periods and amortization rates that facilitate a close match between the decreasing level of coverage and the amount of the unpaid mortgage. The difference between a mortgage protection policy and a uniform decreasing term policy is illustrated in Figure 16.1. Because the insurance remains at a higher level for a longer period of time under the mortgage protection policy, the premium is higher.

![]()

Joint Mortgage Protection Policy

Another contract that has appeal to young couples is the joint mortgage protection policy, under which decreasing term is written on the lives of two persons, with the insurance payable at the death of the first. Today, married couples often purchase a house based on their joint incomes. In the event that one of the two dies, the remaining spouse would find it difficult, if not impossible, to continue the mortgage payments. One solution is a joint mortgage protection policy. The cost for a joint mortgage protection policy is less than the cost of a separate individual mortgage protection policy on each partner. With one company, for example, a husband and wife, each age 25, would pay about $338 a year for a $100,000 30-year joint mortgage protection policy. Separate policies on the husband and wife would cost $244 and $195, respectively, for a total of $439.

FIGURE 16.1 Mortgage Redemption Policy

![]()

Survivorship Whole Life

Survivorship whole life or the second-to-die policy is a contract that insures two lives with the promise to pay only at the second death. Survivorship life was developed in response to the unlimited marital deduction under the federal estate tax law, under which an individual may leave his or her entire estate to a spouse without estate tax liability. Although the bequest of an individual's estate to his or her spouse avoids the estate tax, a tax will be payable on the death of the beneficiary spouse, resulting in an immense tax liability if the couple have a large estate. Survivorship life insurance is a practical approach to this exposure; it automatically provides life insurance proceeds to cover the estate tax when it occurs, which is at the death of the second spouse. Because survivorship life is not payable until the second death, the premium is lower than the cost of separate policies on the two individuals. One insurer, for example, charges a premium of $7300 for a $250,000 survivorship whole-life policy covering a male age 65 and a female age 62. If separate whole-life policies were purchased, the annual premiums for the husband and wife would be $11,250 and $8025, respectively.1

![]()

Family Income Policy

The family income policy utilizes the concept of decreasing term insurance to fit a need for a decreasing amount of insurance. The family income policy is a combination of some form of permanent insurance (e.g., whole life) with decreasing term insurance. The term insurance makes provision for the payment of some stipulated amount per month from the date of the insured's death until some specific date in the future. The sum payable per month is typically 1 percent of the amount of permanent insurance although many companies offer other options. To illustrate how the family income policy works, let us assume the insured in question purchases a $100,000 whole-life policy with a 1 percent family income benefit. The insuring agreement of the family income policy promises to pay $1000 per month to the beneficiary from the date of death of the insured until a date 20 years from the policy's inception. The normal family income period is 20 years although other options such as 10 or 15 years are available. If the insured outlives the period specified as the family income period, the decreasing term portion of the policy ceases. The insured then has the basic amount of permanent insurance on which premiums continue to be paid.

Figure 16.2 illustrates the family income policy graphically. The amount of whole-life insurance in this illustration is $100,000, and a $1000 per month benefit will be paid from the date of the insured's death until the end of the 20th year after the inception date. The $160,000 in decreasing term represents the amount the insurance company must have in policy proceeds at the beginning of the family income period to pay $1000 per month for 20 years. As time goes by, the amount of insurance needed to make the $1000 monthly payments for the remainder of the 20-year period declines. The $1000 family income benefit comes from two sources: One part comes from the decreasing term, and the other part comes from interest on the benefits left with the company. It is common under the family income policy to provide for the payment of the basic policy at the end of the income period. Thus, the interest from the basic policy helps provide the monthly income payments.2 In some instances, the insurance company will permit the beneficiary to take the commutation value of the monthly benefits at the time of the death of the insured. In either case, the amount payable will be reduced by the amount of interest forgone by the insurer.

FIGURE 16.2 Family Income Policy

![]()

Family Income Rider

The family income rider is a variation of the family income policy but with somewhat more flexibility. The family income rider is a decreasing term rider attached to some permanent form of insurance. Some companies will even permit the use of the family income rider with a form of long duration term, such as term to age 65 or term to expectancy.

Although the family income policy and the family income rider may provide for the payment of a specified amount (e.g., $1000 per month), the actual amounts of term insurance required to provide this amount may differ. The determining factor is the time at which the basic policy is payable. As we have seen, it is common under the family income policy to provide for the payment of the basic policy at the end of the income period. In the case of the family income rider, the term insurance is usually sufficient to provide the full amount of the monthly benefit without the interest from the basic policy. This means that the amount of the basic policy may be paid immediately at the death of the insured, it may be left at interest to increase the amount of the monthly benefit above the designated amount, or it may be left to accumulate at interest until the end of the income period.

![]()

Family Protection Policy

The family protection policy is known by many names; almost every insurance company offers it in one form or another, and many refer to it by their own trade name.3 This special form is an attempt to provide insurance on the entire family. The distinguishing characteristic is that insurance in pre-determined proportions is provided for each family member. For example, the unit on the husband may be $5000 on an ordinary life basis, with $1000 term insurance on the wife (the term extending to the time the husband is 65) and $1000 term coverage on each child, with coverage to a designated age such as 21 years. Children born after the inception of the contract are covered automatically without notice to the insurance company on the attainment of a specified age, for example, 14 days. Surrender and loan values are provided, but paid-up insurance is normally provided only on the coverage applicable to the husband. It is customary to permit conversion of the term insurance on the lives of the dependents on the expiration of the specified term. For example, many contracts provide for conversion of the coverage on the children up to as much as $5000 of permanent life insurance for each $1000 of term coverage and without evidence of insurability.

The premium on this form of insurance is based on the age of the husband, with an adjustment made for the additional risk the company accepts. The basic premium computation assumes the wife is the same age as the husband. If she is not, the face amount of the term insurance covering her is adjusted. The younger the wife relative to her husband, the greater the amount of insurance coverage on her life.4 The older the wife, the less her coverage. For example, if the standard program provides $1000 coverage on the wife and that particular wife is one year older than her husband, her coverage might be reduced to $900. If she is one year younger than the husband, it would be adjusted to $1100.

All members of the family must be insurable if the contract is to be issued. If the husband or wife should be uninsurable, the contract cannot be issued at all.5 The only exception involves the children. If one child is uninsurable, the family protection policy may be issued but with that child excluded from coverage.

The family protection policy is popular with young married couples since it provides some insurance on every family member. It can be, and often is, written with a family income rider that provides 1 percent of the amount of coverage on the father as monthly income during the family income period. One of the more attractive features of the policy is that it guarantees the insurability of the children in the family. In the event that a child should become uninsurable before reaching the conversion age or if a child who is uninsurable is born to the marriage, this contract would guarantee the child would be able to purchase at least some minimum amount of permanent insurance on reaching the conversion age.

![]()

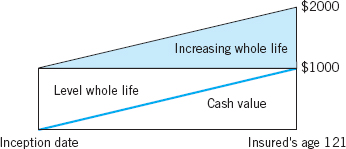

Return-of-Premium and Return-of-Cash-Value Policy

Some individuals who lack an understanding of the level-premium concept think the insurance company should pay the face amount of the policy when the insured dies plus the cash value. They reason that since the cash value is the insured's savings fund, it is inequitable to pay this to the beneficiary and call it a part of the death benefit. Insurance companies attempt to create a salable product, and if people want a policy that pays the face amount plus the cash value, they are going to get it. Policies have been issued that purport to pay, in addition to the policy's face amount, the cash surrender value at the time of death. From what we have learned about the cash value and its relationship to the level premium, we know this is impossible unless an additional premium is charged. The policies that agree to pay the cash value plus the face amount of the policy are nothing more than a combination of two whole-life contracts. As Figure 16.3 indicates, two amounts of insurance are in force at all times. The basic amount is level, being equal to the policy's face amount that the insured has purchased. The second portion, for which the insured pays an additional premium, is always sufficient to pay an amount equal to the basic policy's cash value.

FIGURE 16.3 Return-of-Cash-Value Policy

FIGURE 16.4 Return-of-Premium Policy

A variation of this idea is found in the return-of-premium policy (Figure 16.4). Most individuals like to think they are getting something for nothing. The return-of-premium policy purports to pay the policy's face amount at the death of the insured, plus all the premiums that have been paid, provided the insured dies within a certain period of time. Like the return-of-cash-value policy, the return-of-premium policy is composed of two amounts of insurance. The basic policy is whole life or some other form of permanent insurance. The second portion is increasing term insurance, with a face amount always sufficient to pay the total amount of premiums paid for both portions. The insured must die within a certain period (normally 20 years) if the beneficiary is to receive the face amount and the premiums paid. If the insured does not die until after the 20-year period has passed, the beneficiary will receive only the face amount of the basic policy, and the term portion of the policy expires without value.

![]()

Modified Whole Life

The distinguishing characteristic of modified whole life is its premium arrangement. The premium for the first three or five years is slightly more than that on the same amount of term insurance. After the end of the three-year or five-year period, the premium increases to a level more than the whole-life premium at the age at which the policy was taken out but less than the premium on permanent insurance at the attained age of the insured. One company quotes the following rates for five-year term, whole life, and modified whole life:

This policy is attractive to college students and other individuals who think their income will increase within a short time. They would like to purchase permanent insurance at their current age but cannot afford to do so. If they wait until they can afford it, or if they purchase convertible term, the premium on the permanent insurance will be based on their age at conversion. The modified whole-life policy helps solve this problem. If the insured knows he or she will be converting to permanent insurance within a short period of time, the premium outlay will be lower over the long term if modified whole life is purchased instead of convertible term.

Actually, modified whole life is equivalent to automatically convertible term. As in the case of term, during the first three to five years, there is rarely a cash value. Although a separate type of policy is designated automatic convertible term, it is almost identical with modified life.

![]()

Graded-Premium Whole Life

Another contract closely related to modified whole life is graded-premium whole life. Graded-premium whole life is a contract in which the initial premium is low (say, $2 per $1000 at age 21) but increases yearly until it levels off sometime between the tenth and twentieth years. Cash values are generally unavailable until year 10, and even by year 20, the cash values are low.

![]()

Single-Premium Life

As its name suggests, a single-premium life policy is one in which there is a single premium; generally, the minimum premium is $5000 or more. This premium creates an immediate cash value in the policy. This cash value and the investment income earned on it are sufficient to pay the cost of the policy's benefits, which, to comply with the requirements of the Internal Revenue Code (IRC) must be 100 percent to 250 percent of the cash value, depending on the age of the insured. Single-premium life insurance is written on a traditional whole-life and variable basis.

The rate of return on a single-premium whole-life policy is usually guaranteed for a period of from one to five years. Thereafter, the rate is adjusted at the discretion of the insurer or according to a formula but does not fall below a guaranteed minimum (e.g., 4 percent or 5 percent). The earnings on the cash value accumulate tax free until the policy is cashed in, at which time the earnings are taxable. Unlike traditional forms of life insurance, single-premium life does not usually have a front-end “load.” Although a commission is paid to the agent, the amount of the commission is not deducted from the premium in creating the policy's cash value. Instead, the policy is subject to a surrender charge, generally in the range of 5 to 10 percent, which is levied if the policy is cashed in during a specified period of time, usually 7 to 10 years. The surrender charge diminishes and disappears after 7 to 10 years.

Modified Endowment Contracts Following the elimination of many traditional tax shelters by the Tax Reform Act of 1986 (TRA-86), sale of single-premium life insurance mushroomed. In 1987, the sale of single-premium life insurance soared to about $10 million, more than double the level the previous year. Ironically, this rapid growth served as the motivation for congressional action to modify its status under the tax laws. Because single-premium life policies were treated the same as any other contract that met the IRC definition of life insurance, many buyers found them to be attractive investment shelters. As with other forms of life insurance, the cash value buildup is tax free until the policy is terminated. As with other forms of life insurance, the insured could borrow from the cash value without tax liability, as long as the loans did not exceed his or her basis in the contract. This meant that large sums invested in single-premium life insurance could generate tax-sheltered investment income.

Although single-premium life insurance and certain other contracts with a high investment element met the standards established by the 1984 act, Congress considered the tax treatment of these contracts to be a loophole, which it acted to close in the Technical and Miscellaneous Revenue Act of 1988 (TAMRA). In this law, Congress instituted a new test, designed to further discourage the use of life insurance contracts with high premiums as an investment. TAMRA classifies any contract sold after June 21, 1988, that fails the test as a modified endowment contract (MEC). It then makes modified endowment contracts subject to a penalty if investment earnings are withdrawn by a cash surrender or loan before age 59½. The test, called the seven-pay test, compares the premiums paid for the policy during the first seven years with seven annual net level premiums for a seven-pay policy. The net level premium for a seven-pay policy is an artificial standard constructed by the Internal Revenue Service (IRS) based on the guideline level-premium concept introduced in the 1984 tax act.

Modified endowment contracts are subject to two important provisions. First, funds withdrawn from such contracts are subject to a last-in first-out (LIFO) treatment. This assumes the investment income is withdrawn from the policy before the insured's basis. In addition to the LIFO treatment, MECs are subject to a 10 percent penalty on any taxable gains withdrawn before age 59½. As with an annuity, the cash value buildup accumulates tax free unless it is withdrawn.

![]()

Juvenile Insurance

Historically, the primary purpose of most juvenile policies was thrift, and many policies were purchased to accumulate funds for the child's college education. Prior to the Deficit Reduction Act of 1984, the most popular forms of juvenile insurance were a 20-year endowment and an educational endowment at age 18, but these contracts have disappeared because of their inability to satisfy the cash value-corridor test. The most popular forms of juvenile insurance today are term contracts that automatically convert to whole life without evidence of insurability when the child reaches a stipulated age (such as 25) and whole-life policies with a guaranteed insurability option. Some policies combine the features of automatically convertible term with a guaranteed insurability option that permits the insured to incrementally increase the amount of insurance at specified ages.6

The major appeal of juvenile insurance is that it protects the child's insurability. Should the child become uninsurable, a whole-life contract (or a convertible-term policy) with the guaranteed insurability option would ensure at least some minimum level of lifetime protection.

It is common in the case of juvenile policies to include a policy provision called the payor clause, which specifies that all future premiums under the policy will be waived if the premium payer, who is named in the endorsement attaching the payor clause, should die or become disabled. This provision guarantees the payment's completion on the child's policy if the payer should die or become disabled.

Juvenile insurance is a specialized form of protection. In many cases, it is misused. Too many individuals purchase this kind of life insurance when they are inadequately protected. In most cases, the premium dollars used to purchase insurance on children would be better spent in providing protection on the head of the family. Although a child's death is a tragedy, it does not bring with it the grave consequences for the family that the breadwinner's death brings. Dollars spent to provide educational funds for the child can accomplish this purpose almost as well when they purchase insurance on the father's life.

![]()

Indeterminate Premium Policies

The years from 1976 to 1985 marked a period in which interest rates climbed to unprecedented levels. These record rates combined with diversification strategies of firms in the financial services market to create a backdrop for a revolution in life insurance products. One of these was the universal life policy, but there were others as well.

As interest rates rose in the late 1970s, the insurance-buying public recognized the investment elements in their cash value insurance policies were not earning competitive yields. (It was common during this time for traditional life insurance products to yield 3 to 5 percent on the investment element when alternative investments were returning 12 to 14 percent.) Often, especially when the guaranteed policy loan rate was low, policyholders borrowed their policy cash values at 5 percent to invest them at 12 percent. Other insureds went further and cashed their policies in, purchasing newer policies with lower premiums or higher yields or they converted to term insurance and a separate investment. As a result, there was a significant turnover of policyholders for many companies, and old policies were replaced with new ones. As interest rates rose, insurers found it difficult to meet the competition from universal life policies using traditional participating policies. What was needed, and what some insurers devised, was a mechanism whereby insurers could adjust the premiums on existing policies to reflect changes in investment income; this led to the indeterminate premium policy.

The benefit structure of the indeterminate premium policy is the same as that for other policies, but the premium structure differs. Indeterminate premium policies have maximum guaranteed premium rates specified in the policy, but initial premiums are generally set at a level well below the maxima. The issuing company then reserves the right to change the initial premium up or down, subject to the specified maximum. The low initial premium is guaranteed for a specified time period, usually ranging from 2 to 10 years. Generally, the longer the period for which the initial premium is guaranteed, the higher the initial premium. Although the earliest indeterminate premium policies were whole-life policies, indeterminate term soon followed. Indeterminate premium policies are also known as variable premium life insurance.

Interest-Sensitive Whole Life Interest-sensitive whole life, which is also called current assumption whole life (CAWL), insurance is an indeterminate premium policy in which the policy's cash value is variable, based on changes in the premium. Interest-sensitive policies include a redetermination provision under which the insurer can, after an initial guarantee period, increase or decrease the premiums based on current interest and mortality. If the current assumption produces a lower premium, the insured can pay the lower premium or continue to pay the old higher premium and, thereby, increase the cash value. Subject to evidence of insurability, the insured can use the difference between the old and new premiums to increase the death benefit. If the new premium is higher than the previous premium, the insured can pay the new premium, reduce the face amount of the policy, or use a part of the cash value to cover the difference.

Participating Policy Innovations The same competitive forces that prompted creation of indeterminate premium policies and interest-sensitive policies prompted insurers selling participating policies to create new approaches in allocating dividends. These new approaches that have been adopted are collectively called the investment generation method (IGM), a term broadly used in reference to any allocation procedure that recognizes the year (or generation of policies) during which money was invested by the policyholder in determining the dividend.

Under the traditional dividend allocation method (called the portfolio average method), excess investment earnings to be included in dividends are allocated to all policies, old and new, at a single rate, regardless of the pattern of premium payments over the years. Because a life insurer has an investment portfolio with different inceptions, maturities, and rates, funds invested at different times earn different returns. The portfolio average method, as the name implies, produces an average return allocated to all policies. During periods of high interest rates, the average allocation produces a lower rate on new funds than is available elsewhere. To meet the competition from other interest-sensitive products, many companies switched from the portfolio average method of dividend allocation to IGM. There are two distinct types of IGM. They are referred to as partitioned-portfolio IGM and policybased IGM. The partitioned-portfolio approach establishes policy groupings (partitions) by issue year (e.g., prior to 1979, 1980 to 1983, 1984 and later) and calculates a separate average rate of return for each partition. Conceptually, this approach breaks the insurer's policyholders into several small companies corresponding to the issue-year groups. The portfolio average interest rate for each group is calculated from the earnings on the group's net cash flow over the years. Thus, the generation of policies issued from 1980 through 1983 would have a higher rate than would the generation of policies issued prior to 1980.

The policy-based IGM works differently. Each individual policy receives excess interest at rates reflecting the timing of deposits (such as premium payments) made in that policy. More specifically, generations of one or more years are defined, and the increase in policy reserve during each generation receives the rate earned on investments made during those years.7

![]()

Low-Load and No-Load Life Insurance

Low-load and no-load life insurance products are available from a limited number of insurers. The term low-load refers to a contract in which the commission for the first and subsequent years is lower than the traditional commission rates. A no-load policy is one on which no commission is payable.

Initially, low-compensation products were offered only by insurers that do not have a conventional distribution system (such as TIAA-CREF and mail-order insurers). Increasingly, however, low-load and no-load life insurance have become available through specialty agents or brokers who charge a fee for placement. Most companies offering low-load and no-load products limit the market for these products through restrictions such as high minimum face amounts and high minimum premiums so their traditional agents can coexist with the new products.

The interest in no-load and low-load life insurance products parallels the popularity of no-load mutual funds. Other things being equal, a product with a reduced load or no load should be less expensive than a fully loaded product. However, no-load and low-load policies sometimes carry backend loads (surrender charges) similar to those discussed in connection with the single-premium deferred annuity.

![]()

ADVANTAGES AND DISADVANTAGES OF SPECIAL FORMS

![]()

The special policy forms examined in this chapter have certain advantages and disadvantages, both of which arise from these policies being designed to meet special needs. Because they are narrowly designed, these special forms meet those needs better than other policies; by the same token, they are often inflexible and meet other needs poorly. Each individual faces different circumstances, and the danger exists that one of the special policy forms may be used inappropriately. Of course, some needs are almost universal. There is little chance that the family income policy will be misused because of the general need for protection during the child-raising years. However, the juvenile insurance policies are often misused, eating up the premium dollars that would better be spent on the head of the family.

In addition to the special policy forms discussed in this chapter, there are a number of other, even more specialized contracts. The variety and type of special policies are limited only by the imagination of the marketing directors of the insurance companies. When properly used, the special policy forms are useful tools for protecting the insured's family members against the financial consequences of premature death or for accumulating a fund for some specific future need such as retirement or education.

IMPORTANT CONCEPTS TO REMEMBER

mortgage redemption policy

joint mortgage protection policy

family income policy

family income rider

protection policy

modified whole-life policy

return-of-premium policy

return-of-cash-value policy

graded-premium whole-life insurance

juvenile insurance

payor clause

indeterminate premium policy

interest-sensitive whole life

indexed whole-life insurance

single-premium life

single-premium deferred annuity

investment generation method

portfolio average method

low-load insurance policy

no-load insurance policy

QUESTIONS FOR REVIEW

1. Explain the difference between the family income policy and the family income rider. How would you expect their rates to differ and why?

2. Briefly describe the specialized policies that have been created to address the needs associated with mortgages.

3. The family income policy is a combination of whole-life insurance and decreasing term insurance. Explain.

4. Briefly explain the nature of the family protection policy, identifying the various components by type of protection.

5. Describe the situation for which survivorship wholelife or the second-to-die policy was developed. Are there any other situations for which it would be appropriate?

6. Explain why the economic environment of the late 1970s and early 1980s led to the creation of new types of life insurance policies.

7. Explain how indeterminate premium whole-life policies differ from traditional whole-life policies.

8. In what way does the treatment of acquisition expense under single-premium life insurance differ from that of other life insurance policies?

9. What are the principal uses of juvenile life insurance?

10. Explain how the investment generation method of determining dividends differs from the traditional portfolio average method.

QUESTIONS FOR DISCUSSION

1. Taking any combination of the basic forms of insurance from which special policy combinations studied in this chapter are constructed, invent a new policy not discussed in the text and explain the circumstances under which it would be useful.

2. Many products are brought to the market because, in the words of the seller, “the consumer demanded it.” Do you think that the return-of-premium policy or the return of-cash-value policy were the response of the insurance industry to consumer demands, or do you feel they were developed for competitive reasons? What is your opinion of these two policies?

3. During the high interest-rate environment of the 1980s, many policyholders purchased vanishing-premium policies. Because interest rates dropped in subsequent years, premiums have not vanished as originally projected, and many consumers are dissatisfied. Some observers have proposed requiring that insurance companies and agents make projections only on the basis of the minimum guarantees in the policy. Do you agree or disagree with this proposal? Explain.

4. Although the family protection policy attempts to provide protection on the entire family, the insurance on the wife is generally low relative to that on the husband. In addition, the coverage on the wife is term insurance, and only the husband's coverage accumulates cash value. Design a policy that would provide maximum protection on the husband and wife during the child-raising years, with cash values at retirement that vary depending on whether the husband and wife are alive or only one survives. Indicate the specific types of coverage you would use.

5. John Jones travels considerably in his occupation. Although he thinks he needs more life insurance, he does not think he can afford it. However, he is considering a $100,000 travel accident policy on the grounds that it will provide at least some additional protection. How would you advise him?

SUGGESTIONS FOR ADDITIONAL READING

Black, Kenneth Black, Jr., Harold D. Skipper, and Kenneth Black III Life and Health Insurance, 14th ed., Lucretian, LLC, 2013.

Graves, Edward E. McGill's Life Insurance, 8th ed. Bryn Mawr, Pa.: The American College, 2011.

Schaeffer, Karen P. “Second-to-Die Plans: Why the Avalanche?” Best's Review (August 1990).

Skipper, Harold D. and FSA Wayne Tonning The Advisor's Guide to Life Insurance, American Bar Association, 2013.

WEB SITES TO EXPLORE

| American Council of Life Insurance | www.acli.com |

| Life Insurance Management Association (LOMA) | www.loma.org |

| Life Insurance Marketing and Research Association | www.limra.org |

| Society of Financial Service Professionals | www.financialpro.org |

![]()

1Special measures may be required with respect to the ownership of second-to-die policies if the incidents of ownership that will result in inclusion of policy proceeds in the insured's estate are to be avoided. Given the uncertainty as to which spouse will die first, the most logical plan is to have one of the couple's other heirs serve as the policy owner. This will avoid incidents of ownership and the inclusion of the policy proceeds in the estate of the second spouse to die. If this is impractical for some reason, the policy may be owned by a trust.

2To provide funds for funeral expenses and the costs of the last illness, some family income policies allow the payment of a certain amount at the death of the insured if it should occur during the income period. In some contracts, this amount would be $200 per $1000 of the face amount.

3Some insurers create ad hoc family protection policies through the use of riders that add a spouse or children to an individual policy.

4Although this is the standard approach, some insurers leave the amount of insurance on the wife at the standard $1000 and adjust the premium based on her age.

5With some insurers, a parent's policy, covering one parent and the insurable children may be employed.

6These policies are similar to a policy form known as jumping juvenile that was popular prior to the introduction of the modified endowment contract (MEC) penalty in the IRC. Jumping juvenile policies were whole-life contracts that automatically increased to some multiple of the face amount (usually five times) when the child reached age 21.

7Although the newer dividend formulas are effective tools for competition, during periods of rising interest rates, they may be viewed negatively by older policyholders who are receiving dividends based on the lowest dividend interest rate. This can lead to further replacement activity. The question of which method of allocating dividends is proper is a matter of judgment, subject to honest differences of opinion. While equity is an important factor in setting the method of allocating investment income, the motivating force that led to IGM was competition.