The valuation of your inventory must appear on your balance sheet accounts at the end of a fiscal year. The system can calculate the inventory valuation using different costing methods and can post it to the general ledger automatically, so that you do not have to worry about it. Due to performance issues, though, the inventory valuation is usually set up, so that posting to the general ledger is done manually.

Dynamics NAV can calculate the valuation of your inventory according to five different costing methods: They are as follows:

- First In First Out (FIFO): It assumes that the first units to be received in your stock will also be the first ones that will leave it. The inventory valuation will be based on the cost of the last received units.

- Last In First Out (LIFO): It assumes that the last units to be received in your stock will be the first ones that will leave it. The inventory valuation will be based on the cost of the first received units.

- Average: The inventory valuation will be based on the average cost of all received units.

- Specific: This costing method can only be used when specific serial number tracking is done over the stock of the items. The inventory valuation will be based on the exact units that are in stock.

- Standard: This costing method does a FIFO calculation. The difference with FIFO is the way it takes incoming costs, which are based on an estimated cost that you set up on the item. This costing method is usually used for items that are manufactured.

The costing method is chosen at item level, so different items may use different costing methods.

Actually, you don't have to calculate anything. The system will do it for you. However, it is important to understand how costs are assigned to item entries.

The system assigns a cost to every single item entry. This is how different entry types get their cost:

- Purchases: They first get an expected cost when the purchase receipt is posted. The expected cost is taken from the purchase order. When the invoice is posted, they get their real cost from the invoice.

- Positive adjustments: They have the cost that was specified on the item journal. By default, they get the actual average cost of the item, but can be changed by the user if needed.

- Outputs of a manufacturing process:

- Standard costing method: They get the estimated cost defined on the item card

- Other costing methods: Their cost is calculated as the sum of the costs of their components plus the cost of manufacturing the item

The costing method used here determines how costs are assigned to outbound entries. They are always based on the costing of inbound entries for the same item, though.

This is not a complete list. There are other possibilities (such as an inbound entry as the result of a sales return) and different choices that can be made when manufacturing, for instance. We have just taken a look at the most common entries.

The costs in outbound entries are always based on the costs of inbound entries. What happens if the cost of the inbound entry changes after the cost has been assigned to the outbound entry? No problem, the cost in the outbound entry will be updated later on. This is actually done by a batch process called Adjust Cost - Item Entries that can be found by navigating to Financial Management/Inventory. You should run this process periodically to have your item costs up-to-date.

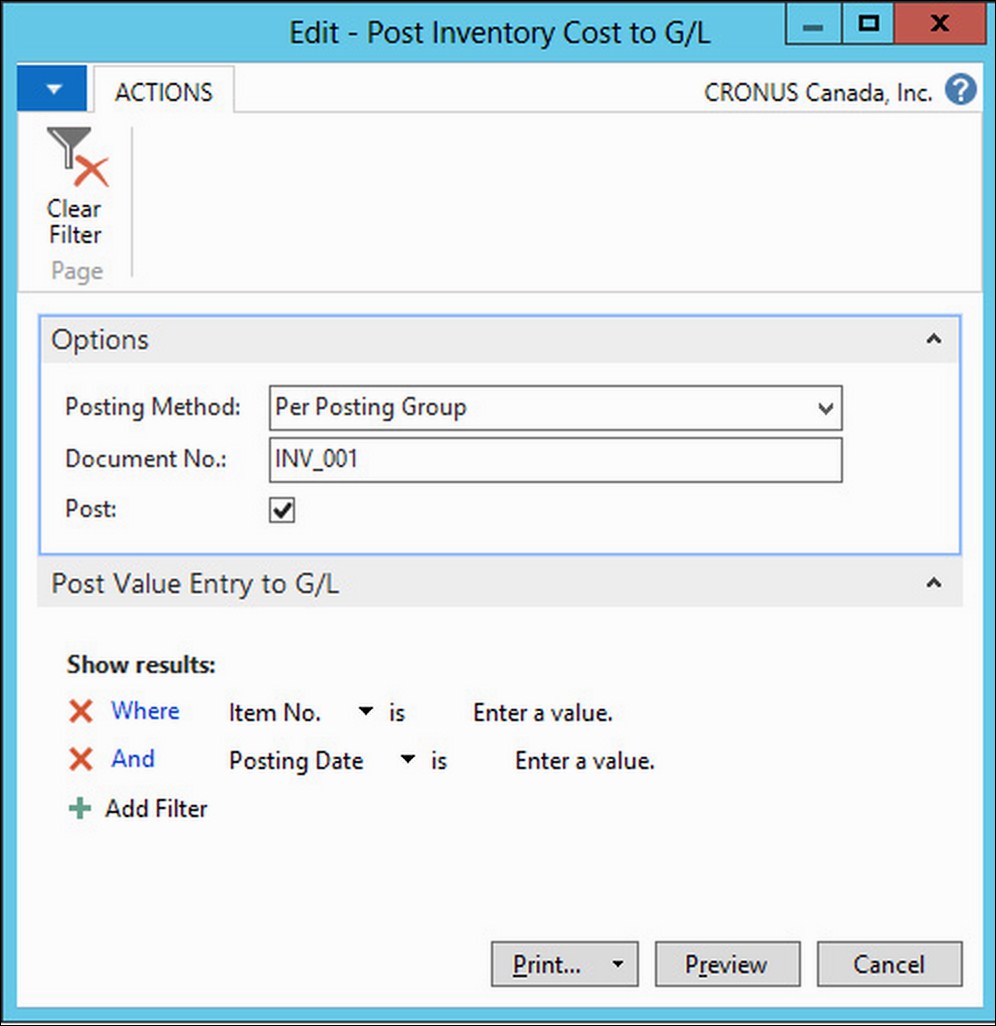

Posting the inventory valuation to the general ledger will transfer the calculated item costs to the corresponding balance sheet account. To do so, we use the following steps:

- Navigate to Financial Management | Inventory and select Post Inventory Cost to G/L.

- Choose Posting Method, Document No., and place a checkmark on Post as shown in the following screenshot:

- Click on Preview.

- A report containing the posted costs will be shown.

If you want to know your inventory valuation at a certain date, you have to run the Inventory Valuation report that can be found by navigating to Financial Management/Inventory. On this report, you can choose whether you want to include expected costs or not. Expected costs are those for item entries that have not yet been invoiced.

The printed report groups entries by inventory posting groups. The Inventory Valuation for January 2016 looks similar to the following screenshot:

For each item, the report prints five groups of columns that shows the following information:

|

Description | |

|

|

This shows the quantity and value of the stock the day before the starting date is selected when running the period. |

|

|

This shows the quantity and value of the increases of stock for the given period. This includes purchases, positive adjustments, sale returns, manufactured items, and so on. |

|

|

This shows the quantity and value of the decreases of stock for the given period. This includes sales, positive adjustments, purchase returns, consumed items, and so on. |

|

|

This shows the quantity and value of the stock at the end of the period. |

|

|

This shows the cost that has already been posted to the general ledger. |