140 CHAPTER 7 ABOUT THESE NUMBERS

Varying views of the same numbers

THREE VIEWS OF FINANCIAL TRANSACTIONS

You were promised a gentle start. So let me begin by stating the obvious. You are inter-

ested in the following three types of transactions.

1 Sales

In fact, you should be obsessed with sales volumes, selling prices and the direct cost of

buying, developing or producing the items that you sell. This is what business is all about.

2 Capital outlays

These are primarily spending on productive assets with a life of more than one year; the

secret to future income. I will talk mainly about fixed assets (such as plant, machinery

and equipment), but the same considerations apply to any investment spending (such as

when you take over another company).

Rightly or wrongly – usually wrongly – the numbers in the financial plan

take on a spurious air of accuracy and importance. They usually become key

targets for measuring performance. Retain a healthy scepticism. The numbers

are only best guesses. We are going to see how the same numbers can be made to tell

different stories and how you can help your readers to understand your message.

t

The fast track to financial basics

1 Start by remembering that business professionals are familiar with three

types of financial transactions – those relating to sales, operating costs and

capital spending.

2 Review the way that the three types of transactions relate to the three

financial statements – the balance sheet, profit and loss account and cash

flow statement.

3 Remember that you are dealing with the past, present and future. You

usually have incomplete information for the present – such as when you are

preparing next year’s business plan during the current financial year.

4 Before going on to start analysing sales and costs, make sure that you

understand some basic accounting principles.

5 Finally, take a look at the way that you can use computer spreadsheets to

simplify your work.

VARYING VIEWS OF THE SAME NUMBERS 141

3 Operating costs

This is all other expenditure – salaries, wages, stationery, telecommunications – the pain-

ful daily costs of running the business.

These figures are not too hard to pull together, as discussed in Chapters 8 and 9.

THREE FINANCIAL STATEMENTS

By themselves, the three types of transactions just mentioned are interesting. They take

on special meaning when reclassified into three key financial statements. This is a simple

matter of mechanical arithmetic. The three statements are as follows and their relation-

ships are shown in Figure 7.1.

1 The balance sheet

Think of this as a snapshot of your finances at one moment in time, say, midnight on 31

December. The balance sheet shows, in financial terms and to the best of the accounting

world’s ability, the sum total of what you have done in the past and where you are today.

See Figure 7.2 and Balance sheet basics on page 143.

2 The income or profit and loss (P&L) account

This shows the very important bottom line – net income (American usage) or the net

profit or net loss (British usage). US readers will know this as an income statement even

though it includes expenditure. For the sake of avoiding ambiguity I’ll generally refer to

it as the profit and loss account. It records financial flows relating to a specific period,

perhaps a month or a year. The flows are essentially sales income less production costs

and operating costs. The difference is net profit (or loss). Transactions are recorded in the

period to which they relate. For example, rent for May is entered in the accounts for May

even if it was actually paid in advance in April.

3 The cash flow statement

This shows financial flows as and when they actually happen (rent for May paid in

advance in April is recorded in April). It is not unusual for the profit and loss account to

look very healthy at the precise moment that negative cash flow (a big borrowing require-

ment) is strangling the business.

If you are relatively new to all this, you might find it useful to review the

components of various financial statements and see how they fit together.

You could take a look at the balance sheet in Figure 10.2, profit and loss

account in Figure 9.7 and cash flow in Figure 10.3.

t

142 CHAPTER 7 ABOUT THESE NUMBERS

THREE TIME PERIODS

The familiar transactions in the first list above (sales, operating costs) – and therefore the

financial statements in the second list (balance sheet, P&L, cash flow) – apply to three

time periods:

the past – historical data from your records;

the present (approximately) – where it is usually necessary to make some

estimations;

the future – which you are about to try to predict.

This might seem painfully obvious. I mention it to draw your attention to the fact that

rarely do you have complete information for the current period. You might begin your

planning in August. Obviously, at that time final figures for the current calendar year are

not available. The usual practice is to estimate them before starting the forecast for the

year ahead.

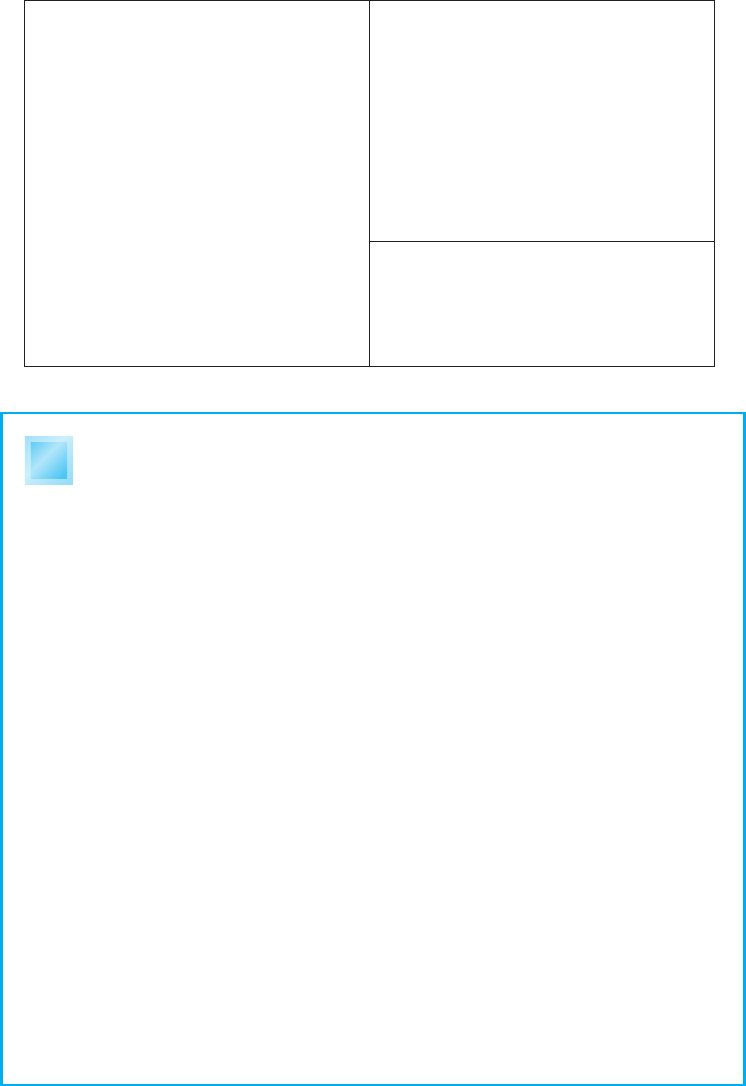

These figures Create these

statements

For these time

periods

Sales projections

Operating costs

Capital spending

Profit and loss

Balance sheet

Cash flow

Historical

Current

(may have to be estimated)

Forecast

Figure 7.1 Basic relationships

Most people understand profit and loss accounts. The concepts behind the

critical cash flow projection are easy enough to grasp. Balance sheets have

managed to take on an unnecessary air of mystery. For this reason, I think it

is useful to spend a few moments unravelling them. Take a look at Figure 7.2 and the

following text that illustrates the basics.

VARYING VIEWS OF THE SAME NUMBERS 143

Assets

Amounts owned or owed to you

Uses of funds

Debit balances

An increase (a debit)

shows use of funds

Liabilities

Amounts you owe

Sources of funds

Credit balances

An increase (a credit)

shows source of funds

Owners' equity

Capital and retained earnings

What the stakeholders have put in and left in

Figure 7.2 The three sections of a balance sheet

Balance sheet basics

I recall attending a meeting with the general manager of one of the world’s top

200 banks. Just before we entered his office, a senior executive of the bank told me

‘forget the balance sheet, nobody understands them’. This is largely true. Balance

sheets are the least understood of all financial statements.

However, most venture capital providers and most bankers are pretty hot

cookies when it comes to reading balance sheets. The discussion in the following

pages will help you stay at least one jump ahead. I will show you how the balance

sheet reveals if you have enough liquidity – and whether you could sell enough

assets to cover your debts if the crunch came.

The company bean counter buries all manner of interesting information in

balance sheets. They provide a snapshot of the financial health of a business at a

single moment in time. They show what is owned and what is owed. The entries can

be classified under the following three headings.

1 Assets. There are things you own, such as equipment and cash in the bank, and

money that is owed to you by your debtors. You are halfway there if you have

spotted the fact that the bank is actually one of your debtors when you have

funds on deposit.

2 Liabilities. These might seem unwelcome at first glance – amounts that you owe

to your creditors, such as bank loans to you and accounts payable by you. In fact,

these are the funds that help you build your business.

t

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.