228 CHAPTER 10 FUNDING THE BUSINESS

Balance sheet headings

You have just looked at methods of producing balance sheets and cash flow from your

expenditure forecasts. Now is a good time to take a look at the entries that appear in bal-

ance sheets. You could, if you wanted, do the opposite and work through the balance

sheet pulling in entries from the transaction accounts and churning out the cash flow on

the side. Figure 10.1 shows the main headings on a balance sheet. To make sure that you

are familiar with them, I will run through each in turn. But first how long is long?

HOW LONG IS LONG?

Unlike other professionals, accountants consider the long term to be anything that is not

going to happen before their next pay review.

Current assets and liabilities are those which relate to the current year.

Long-term assets and liabilities relate to payments and consumption that will

take place after the end of the current year or operating cycle.

Jun Jul Aug Sep

Balance sheet, end month

Assets: prepaid rents 0 3000 2000 1000 0

Memo: change in month … +3000 –1000 –1000 –10000

Expenditure account, whole month

Salaries 12,000 12,000 12,000 12,000

Office rental payments … 1000 1000 1000

Other expenses 100,000 100,000 100,000 100,000

Total (including expenses not shown) 112,000 113,000 113,000 113,000

Cash flow related to expenditure,

whole month

Total expenditure brought forward –112,000 –113,000 –113,000 –113,000

Adjustment for rental payments – 3000 +1000 +1000 +1000

Net cash flow requirement –115,000 –112,000 –112,000 –112,000

BALANCE SHEET HEADINGS 229

CURRENT ASSETS

Current assets are those which will be converted into cash, sold or consumed within one

year. There are four categories:

1 cash at bank;

2 accounts receivable;

3 inventory/stock;

4 miscellaneous.

Cash at bank

This includes currency, demand deposits, certificates of deposits and other deposits

maturing within 90 days. You probably want to avoid forecasting this total until you have

developed your cash flow projections. Generally, you should aim to keep it as small as

possible, while providing adequate working balances. Cash in the bank is not generating

income in the normal course of your business.

Accounts receivable

This is revenue recognised in your profit and loss accounts, where cash has not yet been

received (you will have to deduct an allowance for bad debts). Essentially, the total bal-

ance on accounts receivable reflects the length of time that passes between recognising

sales and collecting payment.

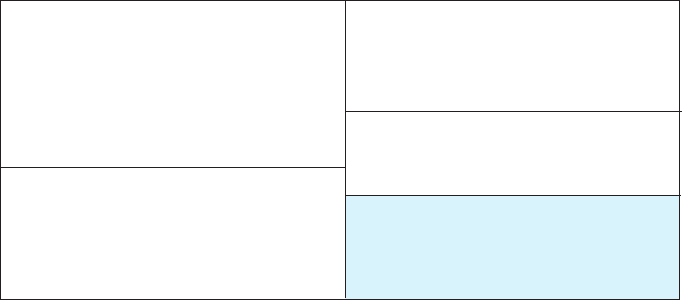

Figure 10.1 A snapshot of the balance sheet

Current assets

Cash

Inventory/stock

Accounts receivable

Other (prepaid expenses, deposits paid …)

The left-hand side always equals the right-hand side: assets = liabilities plus owners’ equity

Current liabilities

Short-term loans

Maturing long-term loans

Accounts payable

Other (accrued expenses, taxes due …)

Non-current liabilities

Long-term loans and other borrowing

Pension fund

Non-current assets

Investments Owners’ equity

Fixed assets (plant, machinery …) Paid-in share capital

Natural resources Retained earnings

Intangible assets (patents, goodwill …)

230 CHAPTER 10 FUNDING THE BUSINESS

Inventory/stock

These are your holdings of raw materials, work-in-progress and finished products that will

be sold. You produced a forecast of these in Chapter 8.

Miscellaneous

This category is usually small, but it can be significant for a new business. It usually rep-

resents cash tied up in payments that you would rather not have made. Try to minimise

them. Two such categories, already discussed, are:

Prepayments. These are advance payments for goods and services – rent,

insurance, subscriptions. Although classified as current assets, they are often

ignored by bankers and others appraising your balance sheet because they are

generally unrecoverable.

Deposits paid. These are (supposedly) returnable sums payable when renting

premises, machinery, vehicles, etc. Beware that sometimes, especially in less

developed countries, it can be remarkably difficult to recover deposits.

LONGTERM OR NONCURRENT ASSETS

There are four main categories of long-term assets. It is common to hear all of these

referred to as ‘fixed assets’:

1 investments;

2 fixed assets;

3 natural resources;

4 intangible assets.

Investments

This is where you show your long-term minority shareholdings in other companies. Minority

is used loosely in this context. The opposite is where you exert a dominant influence over

another company (usually but not always through a majority shareholding) – in which case

the investment is not shown here. Instead, you will consolidate the accounts and have a con-

solidated balance sheet showing the total value of combined assets and liabilities.

BALANCE SHEET HEADINGS 231

Fixed assets

These are holdings of property, plant, machinery, equipment, etc. which were more-or-

less discussed to death in Chapter 9 (along with natural resources and intangibles). They

are shown at cost and also at their net value after deducting accumulated depreciation.

You bring in the totals for these amounts from your forecast of capital outlays.

Natural resources

The treatment of these was considered with our discussions of fixed assets (see above).

Intangible assets

These include R&D costs, patents, copyrights, licences and goodwill. Again, the treatment

of these was considered with fixed assets (see above).

CURRENT LIABILITIES

Current liabilities represent payments that you will have to make within one year.

1 Accounts payable (trade payables/trade credit). This reflects the grace period

that you can win between buying and paying for inventory, supplies and other

materials. Extend it as much as you can.

2 Short-term loans (bank loans, notes payable). These are short-term borrowing –

usually secured against inventory or accounts receivable – from banks and trade

creditors.

3 Long-term debt maturing in the current period. This reflects the obligations of

past borrowing coming home to roost.

4 Miscellaneous. As with assets, the miscellaneous category is not always as

‘unimportant’ as it might sound. It mostly covers payments that you know you have

to make, but which have not hit your cash flow yet. Three headings are as follows.

– Accrued expenses payable. This is recognition of expenses due but not yet paid

– discussed under accruals accounting in Chapter 7. Note that long-term accruals

such as those related to pensions belong – obviously – with long-term liabilities.

– Provision for taxation. The tax collector usually grabs your money as fast as

possible, but you tend to know ahead of time that you will have to pay up, and

you should make provision here.

– Deposit received. If you take returnable cash payments from customers, show

them here. Financial institutions take deposits in a different sense and have

special categories for deposits.

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.