240 CHAPTER 10 FUNDING THE BUSINESS

Debt or equity?

Along the way, I have assumed that you will use trade credit as and when it is available.

Your choice for your excess cash requirement is to fund it by borrowing or by increasing

the owners’ capital. The owners might be a sole proprietor, partners or shareholders. The

jargon varies, so from now on I will refer to loan capital as debt and to owners’ capital as

equity. With that out of the way, what difference does it make whether the funding comes

from debt or equity?

COMPARING DEBT AND EQUITY

Debt is repayable

Lenders are very demanding. They are concerned mainly with security and cash flow.

They usually lend to you only if you own more than you owe (so that they can seize your

assets if you default on repayment) and if you can prove that you can definitely afford to

pay it back. The main cost to you is the interest charge.

Equity is not repayable

Shareholders recover their capital in one of two ways. Either the business goes to the

wall and shareholders take the final pickings after all other creditors have been settled.

Or the shareholders unlock value by selling their shares to another investor. We should

assume that you do not want to close your business. The alternative then is to run a suc-

cessful company so that the amount that people are prepared to pay for your shares

increases. Shareholders can then sell their shares at a premium. You usually have to keep

them happy along the way by giving them dividends (sharing out a bit of annual profit as

pseudo interest payments). As shareholders are the owners of the company, those with a

high proportion of the shares usually want a say in how it is run. A shareholder – or group

of shareholders – with a dominant stake can force majority decisions. The cost, then, is

mainly an obligation to be good managers and a loss of ownership and control.

I said that lenders are very demanding. It sounds as if shareholders are worse. The big

difference is in the cash flow.

Debt is a burden – repayments of principle and interest drain your cash

flow. Equity does not necessarily involve parting with any cash – even the

dividends can be deferred until better cash flow days. Moreover, equity

investors accept higher risk in exchange for better returns in the future. This means

that you can persuade backers to swap their cash for your shares when the bankers

are sucking in their breath and shaking their heads. But while the cash flow effect of

equity is far less painful, the overall cost is actually greater than that of debt.

DEBT OR EQUITY? 241

Why is the cost of equity greater than the cost of debt? Follow through these simple

arguments.

1 Your investors are looking for a return on equity that is greater than the rate of

interest that they could earn on a lower-risk investment.

2 Your debt is secured against assets and cash flow, so your debt must be a lower

risk than your equity.

3 Therefore, logically, your equity must produce a higher return than the interest

rate that you pay on your debt. If it did not, shareholders would desert you.

Put another way, you increase the return on equity by leveraging it and using it to help you

borrow at a lower cost.

I do not know about you, but sometimes I find that simple logic can be very demanding.

It gets easier now.

CHOOSING DEBT FROM EQUITY

The relative merits of debt and equity are compared below. To a large extent, the choice

is dictated by circumstances. Figure 10.6 provides a simplistic decision chart. If you have a

good track record, security for a loan, adequate cash flow, and a not-undue burden of exist-

ing debt you might be able to borrow more. Otherwise, you might be forced to look for

equity – especially if you are in a start-up situation with few assets and a higher-risk venture.

Of course, you may also decide that your particular circumstances make equity prefer-

able even if you could justify increasing your debt. In particular, if you sell some of your

own shares you can unlock some of the value that you have created in the business and

treat yourself to a vacation or a new executive jet.

When you increase the proportion of your debt (relative to your equity),

your overall cost of capital falls. If you earn the same profits for a lower

amount of equity capital, the return on equity (profit divided by equity)

must increase.

242 CHAPTER 10 FUNDING THE BUSINESS

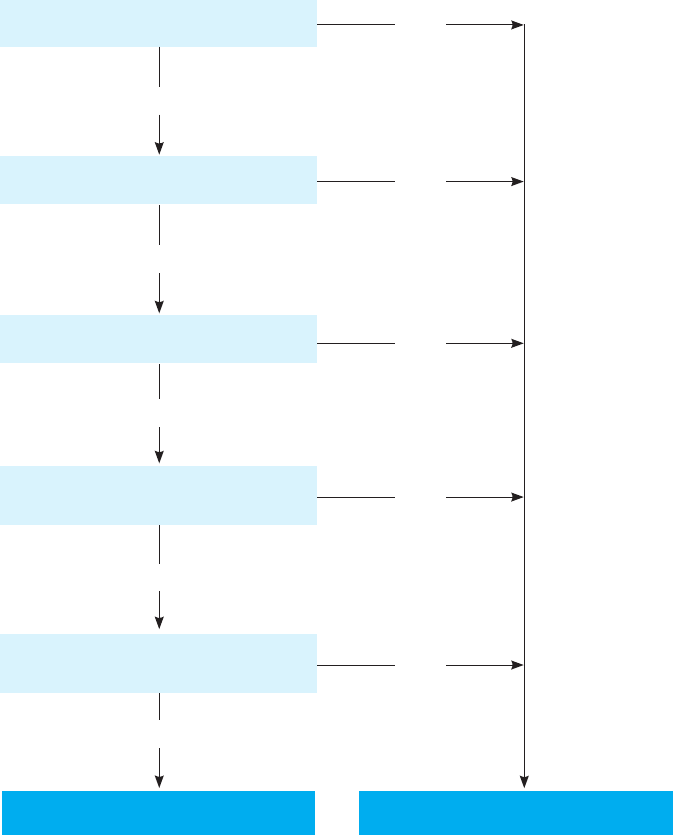

Figure 10.6 Choosing debt from equity

Are you starting a new business?

Do you already have a high proportion of

borrowing relative to equity?

Is repayment of the funding dependent on

the success of a high-risk undertaking?

You will probably be able to borrow You should be looking for equity

NO

NO

NO

YES

YES

YES

YES

YES

Do you have, or will you have,

unencumbered fixed assets with a value

that exceeds the required funding?

NO

Do you have, or will you have,

clearly identifiable cash flow

that will repay the funding?

NO

DEBT OR EQUITY? 243

FINDING FUNDING

Having decided whether you need debt or equity funding, where do you look for it?

Figure 10.7 shows common sources with a crude indication of the likelihood of extracting

the required funds from each, depending on your stage of development. These stages –

start-up, early operations, growth, maturity and recovery from crisis – equate very loosely

with the amount of risk for the provider of funds. The earlier and late stages tend to be

riskier. The table also has an even more tongue-in-cheek identification of the associated

quality of assets – start-ups tend to have fewer tangible assets than mature companies.

Start-up equity

The indications of the likelihood of receiving backing from these sources are also tainted

by my cynicism – based on experience.

For example, venture capital providers are supposed to exist to pour equity into

start-up situations, but their definition of start-up seems to be ‘a well-developed

product and full order book’.

Business partners – including big companies that would benefit from your

invention – are also remarkably inept at grasping opportunities.

In my opinion, you are more likely to find pure start-up capital from working

partners and angels. Angels (sometimes known as the Three Fs – family, friends

and fools) are people you can persuade to invest their spare cash in your business.

The term ‘Angels’ comes from the original sponsors of Broadway shows.

Debt and equity compared

Debt Equity

Lenders are risk averse Equity investors accept higher risk

No loss of ownership Involves giving up some ownership

No explicit loss of control May reduce control

Has to be repaid Does not have to be repaid

Increases demands on cash flow Exerts smaller demands on cash flow

Reduces cost of capital Increases cost of capital

Increases return on equity Reduces return on equity

244 CHAPTER 10 FUNDING THE BUSINESS

Figure 10.7 Sources of funds

Quality of assets

Mainly intellectual Mainly fixed

Risk

High Low High

Stage of growth

Start-up Early days Growth Maturity Recovery

Equity

Family and friends

Angels

Venture capital

Fellow directors

Joint ventures

Misc corporate

Suppliers

Channels to market

Institutional investors

Investment companies

Public offerings

Takeovers

Debt

Family and friends

Angels

BS/S&L

MBO

Commercial credit co’s

Factors

Government agencies

Banks

Institutional investors

Investment companies

Public offerings

Leasing

Other

Research grants

Private foundations

Licensing

Source of funds

Any existing funding mainly equity No existing funding, or mainly debt

Lower-risk activities

Higher-risk activities

Will they provide funds?

BS/S&L = building societies/savings and loans associations; MBO = management buyouts

Unlikely Possible Likely

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.