Chapter 4. The Other Traders

After you have firmly grasped that the market is neither good nor bad but simply a world of opportunity, you must begin to embrace the fact that within this world of opportunity are countless traders seeking to capitalize on the same opportunities as you. Some haven’t a clue what they are doing, but more and more are learning, studying, and utilizing basic trading strategies, such as traditional technical analysis. To remain one step ahead of this crowd, you must not only study the underlying market character, you also need to study the current market players. The sooner you realize you are trading against other traders and not just the stocks or the market, the better off you will be.

Different market environments call for different strategies. Those investors who remain the most flexible have the opportunity to realize the most profits. Although I am a firm believer that over several years the fundamentals of a company will ultimately determine where its stock price goes, most traders live within much shorter time frames. Your goal is not to just take advantage of the fundamental prospects of a company or market, but the anomalies that present themselves day in and day out, from which great profits may be realized. Typically, these anomalies could be recognized and capitalized on through traditional technical analysis. Now, however, you must be familiar enough with traditional methods so that you have the confidence to trade among the traders who sometimes overwhelm a method to the point of failure.

You should look no further than 2009 as a reminder of just how important it is to focus on the actions of others when approaching your trades. Coming off one of the worst annual declines the market had seen in decades, 2009 started off no differently as the market quickly dropped more than 25% within the first two months. Broad complacency over stock prices led to a national panic, at which time investors everywhere sold stocks at any price to secure the little money that was left within their accounts. Looking back, I am not sure whether I will ever see anything like the first two and a half months of 2009. However, the experience throughout the remainder of the year left a lasting impression on me.

After a steep decline to start 2009, it was widely accepted that at some point an oversold bounce would set in. When the March 6th bottom arrived and the bounce began, it was a broad belief that the move up would be nothing more than a dead cat, oversold bounce, that would ultimately either lead to new lows or a significant double bottom, which traders could accept as the final gasp of the bear market. Unfortunately, neither scenario played out, and for the remaining nine months, traders were forced to accept a different paradigm that I believe set the stage for a new style of trading never before seen in our history. Despite net mutual fund withdrawals and an overwhelming shift from stocks to bonds, the S&P 500 finished the year up a staggering 23%. This number is even more impressive considering that at one point in the year the market was down more than 25%. You might assume that this meteoric rise gave way to vast fortunes within the trading world, when in reality this is far from the truth. Of the traders who used traditional technical analysis to move them out of the market before the 2008 decline, very few capitalized in the manner the market moved in 2009. Investors who did capitalize on the returns of 2009 were more often than not passive. They were investors who had also suffered incredible losses in 2008 and were simply returning to a level their accounts had been at halfway through the decline itself. When 2009 came to an end, most traders expressed that they were too cautious and not willing to embrace higher prices. I doubt many went any further to study the character of the market at that time, which led to this general theme of extreme caution. I would argue that despite any hind-sight resolutions, if 2009 were to repeat itself in the same manner, most traders would adhere to the same caution, struggling to embrace the move just as before. I believe this is because few investors will ever understand the true nature in which the move itself transpired.

One of the basic tenets of technical analysis is its attempt to study the footprint of institutions so that you may actually see what the larger mutual funds’ money is doing as they move in and out of stocks. Traditionally, through this study, you could learn enough about money flow to hop along for the ride. Looking back over 2009, you must ask the question how such a steep rise was possible, when there were actually net mutual fund redemptions. Meaning how is it possible for a market to advance more than 20% when more money moved out of the market than in?

While the return was impressive within itself, the character of the ascent along with the characteristics of the traders must be studied because the move transpired in a technical manner that had never been seen before.

Most traders would agree that throughout 2009, there weren’t many significant pullbacks, yet those that arrived developed in such a way as to infer lower prices were on the horizon and, as a result, these were incredibly challenging to accept as prudent points of entry for going long. A basic tenet of a sound technical trading strategy is to study the character of the consolidation or reversal when a broad move pauses. A healthy consolidation, whereby longer-term investors replace shorter-term traders, can be seen through a methodical “backing and filling” (or a pattern that looks like a staircase with a rise higher followed by a small retreat). It is through this consolidation that various stocks begin to develop new bullish patterns, offering new trading opportunities to the astute observer. Under this traditional premise, you might assume that 2009’s 23% rise had its fair share of healthy pullbacks and subsequent bullish setups. However, this assumption based on basic technical analysis would be incorrect.

From the very beginning of the rise, it almost seemed as if the disbelief of the investing community was, in fact, the catalyst behind the rise itself. Although this is true in part for any reversal, where short covering provides the initial force behind higher prices, sustained moves higher are known to be followed by actual demand for stocks rather than bearish investors reversing their positions. It is at this time that institutions provide notable volume, scooping up select stocks becoming new market leaders and letting even the casual observers know that an advance is widely supported. Even though a wall of worry or a market that moves higher based on pessimism rather than optimism is a common, short-term investing theme, 2009 was much different. Not a single text I have ever read says that any sustained rally may come from a continuous stream of pessimistic investors seeking to capitalize on a reversal, thereby setting the stage for repeated and continuous short squeezes higher. From my vantage point, this is what happened throughout 2009. The ease with which retail investors could short stocks through inverse ETFs (exchange traded funds), in combination with the vast amount of traders who understand and attempted to apply basic technical analysis, along with the broad pessimism surrounding the economy, created an environment prone to short squeeze after short squeeze, sending the market higher with very few participating.

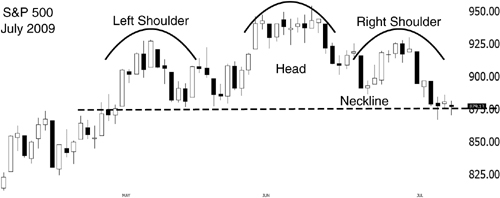

For example, you didn’t have to be a technical analysis guru to be aware of the head and shoulders pattern that had developed on the S&P 500 around July of that year, shown in Figure 4.1. This historically bearish pattern, where the movement of a stock or market takes on the look from which it is named, received unprecedented attention in not only trading circles but also in the mainstream financial media. I would argue that this very notoriety was the primary reason the pattern was doomed to fail, simply because of the number of traders looking to play it. When the pattern didn’t result in lower prices as traditional technical analysis would suggest, it set the stage for one of the biggest short squeezes in the history of the market, as shown in Figure 4.2.

Figure 4.1 In July 2009, the market had carved out one of the most widely discussed head and shoulder topping patterns in history.

Chart courtesy of Worden—www.Worden.com.

Figure 4.2 In July 2009, the head and shoulders pattern failed to break down, resulting in a dramatic short covering rally higher.

Chart courtesy of Worden—www.Worden.com.

From that point forward, not a single market drop looked like healthy consolidation from a traditional sense and was therefore embraced by the general trading world as the top. Opportunistic traders sought to capitalize on this, positioning on the short side only to be squeezed time and again. As the masses moved in to short, the trade quickly became overcrowded and did not work. As these traders reversed their positions, it resulted in an incredible move higher, altering the technical picture from looking rather bearish to new highs in the blink of an eye. This played out time and again to the point where a “bearish pattern, turned bullish break” became the norm. Although I didn’t trade the pattern as often as I should have, one of the most successful long side trades of 2009 was buying what is traditionally called a bearish wedge, a pattern that would normally be shorted. True to its name, the bearish wedge is a consolidation pattern insinuating lower prices in the future. Bearish wedges were common in 2009 after a decline. However, because many investors attempted to capitalize on these patterns to the short side, the patterns no longer played out as they traditionally would. Instead of shorting these traditionally bearish patterns, the profitable trade became buying them, throwing conventional technical analysis out the window. It became so successful that traders jokingly dubbed the pattern the “bullish cliff,” stating that the steeper the decline before the consolidation, the more leverage to use going long. It was humorous at the time, but little did we know how much foresight it actually contained.

To understand 2009, you must understand the general investor mindset leading up to that year. The incredible decline of 2008 led many on a quest to not just understand how to avoid such a drop but to profit from it. Few strategies, outside of technical analysis, protected traders from the bear market of 2008 while also allowing them to profit from it. When the decline was over and the damage done, the frustrated masses flocked to technical analysis, seeking to understand more about the strategy and use it to their advantage. Of course, once again, the crowd was simply setting themselves up for disappointment. The untold masses seeking to utilize basic technical analysis led to the direct opposite outcome from what most were hoping for. Time and again, these strategies failed in 2009. You would be wise to remember that when so many are utilizing the same strategy, it will rarely work.

In 2009, basic technical analysis was thrown out the window, and simply doing the opposite would have netted the investor a hefty profit. Can you then conclude that traditional technical analysis is dead, never to be successful again? I believe that conclusion is foolish. However, I will argue that the successful trader’s strategy will account for the ever-changing landscape that is made up of other traders. Rather than being held to a specific set of rules or style, what we learn from 2009 is that you must be willing to adapt to what other traders are doing, seeking not just to capitalize on the market itself, but also on the actions of others you are trading against. Most will review the rise off the March 2009 bottom and simply conclude that next time they will buy into the weakness and hold longer, capitalizing on higher prices. If this is their only takeaway from 2009, most traders will completely miss some of the most important lessons presented. The real lesson is that you must not only observe the market, but you must also observe the market participants. When the masses have moved to using traditional methods, such as technical analysis, you must be willing to trade on the failure of these patterns to exploit the crowd’s movement for your own benefit.