Understanding the Financial Management Process

Organizations have to be able to manage their finances, but it is a complex process used across an entire organization. It is normally owned by a very senior executive and managed as a separate business function. It is an extremely important area that allows organizations to manage resources and ensure that their objectives are being achieved.

The IT service provider, as part of the overall organization, must be involved in the financial management process. It is important to make sure that all financial practices are aligned; even though a separate process may be used, it should follow the overall organizational principles and requirements.

Purpose of Financial Management

To design, develop, and deliver the services that meet the organizational requirements, you must secure an appropriate level of funding. This is the main purpose of financial management for IT services. At the same time, the financial management process should act as a gatekeeper for the expenditure on IT services to ensure that the service provider is not over-extended financially for the services that the service provider is required to deliver. Obviously, this will require a balance between the cost and quality of the service, in line with the balance of supply and demand between the service provider and their customers.

Cost and quality are key factors in the provision of services, and the only way you can allocate and understand the cost of service provision is through sound financial practices.

Objectives of Financial Management

The following are the objectives of the financial management process:

- Defining and maintaining a financial framework that allows the service provider to identify, manage, and communicate the actual cost of service delivery.

- Understanding and evaluating the financial impact and implications of any new or changed organizational strategies on the service provider.

- Securing the funding that is required for providing the services. This will require significant input from the business and will naturally depend on the overall approach to financial management and cross charging within the organization.

- Working with the service asset and configuration management process (covered in Chapter 9) to ensure service and customer assets are being properly maintained and all associated costs are recorded.

- Performing basic financial accounting in respect of the relationship between expenses and income and ensuring they are balanced according to the overall organizational requirements.

- Reporting on and managing expenditure for service provision, on behalf of the stakeholders.

- Management and execution of the organization’s policies and practices relating to financial controls.

- Ensuring that financial controls and accounting practices are applied to the creation, delivery, and support of services.

- Understanding the future financial requirements of the organization and providing financial forecasts for the service commitments and any required compliance for legislative and regulatory controls.

- If appropriate, defining a framework that allows for recovering the costs of service provision from the customer.

Scope of Financial Management

Financial management is normally a well-recognized activity in any organization, but the specific requirement to manage funding related to the provision of IT services may not be so well established.

It is important to understand the strategic approach that is adopted in relation to IT service provision. How will it be managed; is it internally or externally sourced? If it’s internal, is there a requirement to cross charge for services, or is there some other mechanism of cost recovery in place?

In the majority of organizations, there will be qualified accountants in charge of the corporate finances, usually as part of the finance department. They will set the policies, standards, and accounting practices for the business. The strategy relating to IT funding will be part of the overall accounting approach, but the specifics may be managed locally as part of the IT department.

Those engaged in financial management for IT services must ensure that the practices are consistent with existing corporate controls and that reporting and accounting activities meet with the governance standards as defined for the whole organization. This will also assist with general understanding by the various business units of how IT is funded. Communication and the reporting of internal funding practices across an organization are extremely important for enabling a true understanding of the costs of IT services.

Using a service management approach to delivering services should mean that the accounting for IT services is more effective, detailed, and efficient than it would be otherwise. For an internal service provider, this will enable a translation of information between service provider and business.

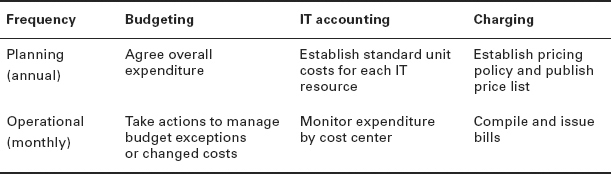

Financial management consists of three main processes:

Table 3.1 shows the cycles associated with financial management.

TABLE 3.1 Budgeting, IT accounting, and charging cycles

The two cycles are as follows:

- Planning (annual), where cost projections and workload forecasting form a basis for cost calculations and price setting

- Operational (monthly or quarterly), where costs are monitored and checked against budgets, bills are issued, and revenue is collected

Preparing and Using a Business Case

One of the key benefits of having an established financial management process is the ability to capture and understand costs and use this information to create justification for expenditure in the form of a business case.

A business case should be a tool for decision planning and support, allowing you to predict the likely consequences of a business decision. This outcome may be either quantitative or qualitative; for example, financial analysis is a common feature of a business case.

In Table 3.2, you can see an example of a basic structure for a business case.

TABLE 3.2 Structure of a business case

| A. Introduction | Presents the business objectives addressed by the service. |

| B. Methods and assumptions | Defines the boundaries of the business case, such as time period and which organizational context is being used to define costs and benefits. |

| C. Business impacts | The financial and nonfinancial results anticipated for the service or service management initiative. Please bear in mind that many nonfinancial results can also be expressed in financial terms. For example, an increase in staff morale can result in lower staff turnover and therefore less expenditure on hiring and training. |

| D. Risks and contingencies | The probability that alternative results will emerge. |

| E. Recommendations | The specific actions recommended. |

Two main considerations for any business case are business objectives and business impact.

Business Objectives

Obviously business objectives will vary from organization to organization. However, they should form a key part of any business case. It is only by examining and understanding the business objectives that you can properly appreciate the impact to the business of the proposal under consideration in the business case. Objectives should start broadly:

- Commercial provider organizations usually have objectives that are the organization’s overall objectives in terms of financial and organizational performance.

- Where the service provider is internal, the objectives are likely to be linked to business units, which in turn are linked to the overall organizational objectives.

- Business objectives for nonprofit organizations are more complex but are usually associated with the users or members who benefit from the organization’s goals, as well as the standard financial objectives.

Business Impact

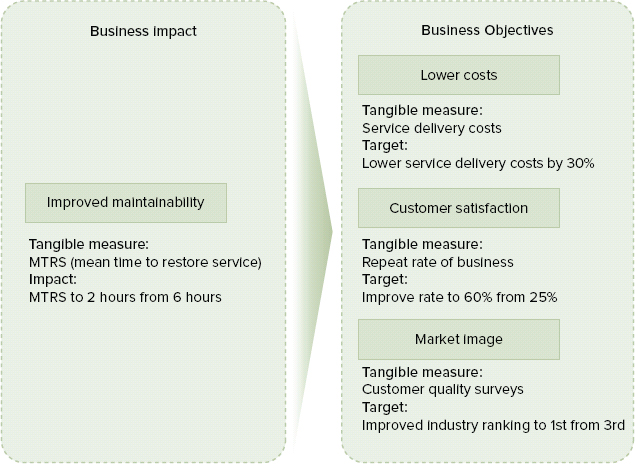

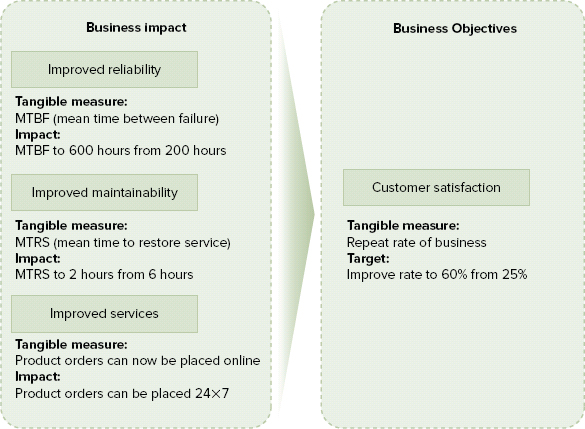

There is a strong relationship between the business objective and the business impact, as shown in the following figures. Figure 3.2 illustrates one aspect of this, and Figure 3.3 shows the converse.

FIGURE 3.2 A single business impact can affect multiple business objectives.

Based on Cabinet Office ITIL material. Reproduced under license from the Cabinet Office.

FIGURE 3.3 Multiple business impacts can affect a single business objective.

Based on Cabinet Office ITIL material. Reproduced under license from the Cabinet Office.

Once you are clear on the business objectives, you can begin to understand the business impact. Often the majority of the business case argument will be reliant on cost analysis, but there are other considerations for service management. There are potential nonfinancial impacts, including market image and perceptions of business ethics that could have an effect on sales or customer satisfaction.

When the term business case is used, it is common to consider only the financial aspects, but service management needs to include more than this, and a successful business will appreciate this. So, a business case should include both financial and nonfinancial recommendations. Much of the information required can be found as part of the service portfolio, because it will provide data for existing services and allow for comparing a new proposal.