CHAPTER 1

First-Order ODEs

Chapter 1 begins the study of ordinary differential equations (ODEs) by deriving them from physical or other problems (modeling), solving them by standard mathematical methods, and interpreting solutions and their graphs in terms of a given problem. The simplest ODEs to be discussed are ODEs of the first order because they involve only the first derivative of the unknown function and no higher derivatives. These unknown functions will usually be denoted by y(x) or y(t)when the independent variable denotes time t. The chapter ends with a study of the existence and uniqueness of solutions of ODEs in Sec. 1.7.

Understanding the basics of ODEs requires solving problems by hand (paper and pencil, or typing on your computer, but first without the aid of a CAS). In doing so, you will gain an important conceptual understanding and feel for the basic terms, such as ODEs, direction field, and initial value problem. If you wish, you can use your Computer Algebra System (CAS) for checking solutions.

COMMENT. Numerics for first-order ODEs can be studied immediately after this chapter. See Secs. 21.1–21.2, which are independent of other sections on numerics.

Prerequisite: Integral calculus.

Sections that may be omitted in a shorter course: 1.6, 1.7.

References and Answers to Problems: App. 1 Part A, and App. 2.

1.1 Basic Concepts. Modeling

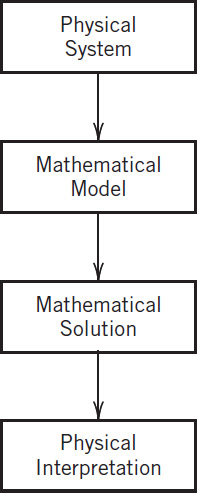

If we want to solve an engineering problem (usually of a physical nature), we first have to formulate the problem as a mathematical expression in terms of variables, functions, and equations. Such an expression is known as a mathematical model of the given problem. The process of setting up a model, solving it mathematically, and interpreting the result in physical or other terms is called mathematical modeling or, briefly, modeling.

Modeling needs experience, which we shall gain by discussing various examples and problems. (Your computer may often help you in solving but rarely in setting up models.)

Now many physical concepts, such as velocity and acceleration, are derivatives. Hence a model is very often an equation containing derivatives of an unknown function. Such a model is called a differential equation. Of course, we then want to find a solution (a function that satisfies the equation), explore its properties, graph it, find values of it, and interpret it in physical terms so that we can understand the behavior of the physical system in our given problem. However, before we can turn to methods of solution, we must first define some basic concepts needed throughout this chapter.

Fig. 1. Modeling, solving, interpreting

Fig. 2. Some applications of differential equations

An ordinary differential equation (ODE) is an equation that contains one or several derivatives of an unknown function, which we usually call y(x) (or sometimes y(t) if the independent variable is time t). The equation may also contain y itself, known functions of x (or t), and constants. For example,

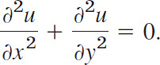

are ordinary differential equations (ODEs). Here, as in calculus, y′ denotes dy/dx, yn = d2y/dx2, etc. The term ordinary distinguishes them from partial differential equations (PDEs), which involve partial derivatives of an unknown function of two or more variables. For instance, a PDE with unknown function u of two variables x and y is

PDEs have important engineering applications, but they are more complicated than ODEs; they will be considered in Chap. 12.

An ODE is said to be of order n if the n th derivative of the unknown function y is the highest derivative of y in the equation. The concept of order gives a useful classification into ODEs of first order, second order, and so on. Thus, (1) is of first order, (2) of second order, and (3) of third order.

In this chapter we shall consider first-order ODEs. Such equations contain only the first derivative and may contain y and any given functions of x. Hence we can write them as

or often in the form

![]()

This is called the explicit form, in contrast to the implicit form (4). For instance, the implicit ODE x−3y′ − 4y2 = 0 (where x ≠ 0) can be written explicitly as y′ = 4x3y2.

Concept of Solution

A function

![]()

is called a solution of a given ODE (4) on some open interval a < x < b if h(x) is defined and differentiable throughout the interval and is such that the equation becomes an identity if y′ and are replaced with h and h′, respectively. The curve (the graph) of h is called a solution curve.

Here, open interval a < x < b means that the endpoints a and b are not regarded as points belonging to the interval. Also, a < x < b includes infinite intervals −∞ < x < b, a < x < ∞, −∞ < x < ∞ (the real line) as special cases.

EXAMPLE 1 Verification of Solution

Verify that y = c/x (c an arbitrary constant) is a solution of the ODE xy′ = −y for all x ≠ 0. Indeed, differentiate y = c/x to get y′ = −c/x2. Multiply this by x, obtaining xy′ = −c/x; thus, xy′ = −y, the given ODE.

EXAMPLE 2 Solution by Calculus. Solution Curves

The ODE y′ = dy/dx = cos x can be solved directly by integration on both sides. Indeed, using calculus, we obtain y = ∫ cos x dx = sin x + c, where c is an arbitrary constant. This is a family of solutions. Each value of c, for instance, 2.75 or 0 or −8, gives one of these curves. Figure 3 shows some of them, for c = −3, −2, −1, 0, 1, 2, 3, 4.

Fig. 3. Solutions y = sin x + c of the ODE y′ = cos x

EXAMPLE 3 (A) Exponential Growth. (B) Exponential Decay

From calculus we know that y = ce0.2t has the derivative

![]()

Hence y is a solution of y′ = 0.2y (Fig. 4A). This ODE is of the form y′ = ky. With positive-constant k it can model exponential growth, for instance, of colonies of bacteria or populations of animals. It also applies to humans for small populations in a large country (e.g., the United States in early times) and is then known as Malthus's law.1 We shall say more about this topic in Sec. 1.5.

(B) Similarly, y′ = −0.2 (with a minus on the right) has the solution y = ce−0.2t, (Fig. 4B) modeling exponential decay, as, for instance, of a radioactive substance (see Example 5).

Fig. 4A. Solutions of y′ = 0.2y in Example 3 (exponential growth)

Fig. 4B. Solutions of y′ = −0.2y in Example 3 (exponential decay)

We see that each ODE in these examples has a solution that contains an arbitrary constant c. Such a solution containing an arbitrary constant c is called a general solution of the ODE.

(We shall see that c is sometimes not completely arbitrary but must be restricted to some interval to avoid complex expressions in the solution.)

We shall develop methods that will give general solutions uniquely (perhaps except for notation). Hence we shall say the general solution of a given ODE (instead of a general solution).

Geometrically, the general solution of an ODE is a family of infinitely many solution curves, one for each value of the constant c. If we choose a specific c (e.g., c = 6.45 or 0 or −2.01) we obtain what is called a particular solution of the ODE. A particular solution does not contain any arbitrary constants.

In most cases, general solutions exist, and every solution not containing an arbitrary constant is obtained as a particular solution by assigning a suitable value to c. Exceptions to these rules occur but are of minor interest in applications; see Prob. 16 in Problem Set 1.1.

Initial Value Problem

In most cases the unique solution of a given problem, hence a particular solution, is obtained from a general solution by an initial condition y(x0) = y0, with given values x0 and y0, that is used to determine a value of the arbitrary constant c. Geometrically this condition means that the solution curve should pass through the point (x0, y0) in the xy-plane. An ODE, together with an initial condition, is called an initial value problem. Thus, if the ODE is explicit, y′ = f(x, y), the initial value problem is of the form

EXAMPLE 4 Initial Value Problem

Solve the initial value problem

![]()

Solution. The general solution is y(x) = ce3x; see Example 3. From this solution and the initial condition we obtain y(0) = ce0 = c = 5.7. Hence the initial value problem has the solution y(x) = 5.7e3x. This is a particular solution.

More on Modeling

The general importance of modeling to the engineer and physicist was emphasized at the beginning of this section. We shall now consider a basic physical problem that will show the details of the typical steps of modeling. Step 1: the transition from the physical situation (the physical system) to its mathematical formulation (its mathematical model); Step 2: the solution by a mathematical method; and Step 3: the physical interpretation of the result. This may be the easiest way to obtain a first idea of the nature and purpose of differential equations and their applications. Realize at the outset that your computer (your CAS) may perhaps give you a hand in Step 2, but Steps 1 and 3 are basically your work. And Step 2 requires a solid knowledge and good understanding of solution methods available to you—you have to choose the method for your work by hand or by the computer. Keep this in mind, and always check computer results for errors (which may arise, for instance, from false inputs).

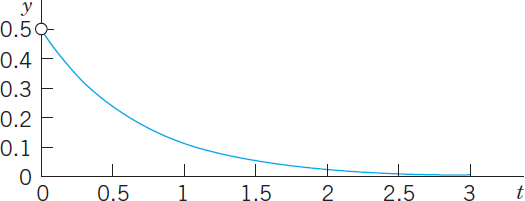

EXAMPLE 5 Radioactivity. Exponential Decay

Given an amount of a radioactive substance, say, 0.5 g (gram), find the amount present at any later time.

Physical Information. Experiments show that at each instant a radioactive substance decomposes—and is thus decaying in time—proportional to the amount of substance present.

Step 1. Setting up a mathematical model of the physical process. Denote by y(t) the amount of substance still present at any time t. By the physical law, the time rate of change y′(t) = dy/dt is proportional to y(t). This gives the first-order ODE

![]()

where the constant k is positive, so that, because of the minus, we do get decay (as in [B] of Example 3). The value of k is known from experiments for various radioactive substances (e.g., k = 1.4 · 10−11 sec−1, approximately, for radium ![]() ).

).

Now the given initial amount is 0.5 g, and we can call the corresponding instant t = 0. Then we have the initial condition y(0) = 0.5. This is the instant at which our observation of the process begins. It motivates the term initial condition (which, however, is also used when the independent variable is not time or when we choose a t other than t = 0). Hence the mathematical model of the physical process is the initial value problem

![]()

Step 2. Mathematical solution. As in (B) of Example 3 we conclude that the ODE (6) models exponential decay and has the general solution (with arbitrary constant c but definite given k)

![]()

We now determine c by using the initial condition. Since y(0) = c from (8), this gives y(0) = c = 0.5. Hence the particular solution governing our process is (cf. Fig. 5)

![]()

Always check your result—it may involve human or computer errors! Verify by differentiation (chain rule!) that your solution (9) satisfies (7) as well as y(0) = 0.5:

Step 3. Interpretation of result. Formula (9) gives the amount of radioactive substance at time t. It starts from the correct initial amount and decreases with time because k is positive. The limit of y as t → ∞ is zero.

Fig. 5. Radioactivity (Exponential decay, y = 0.5e−kt, with k = 1.5 as an example)

1–8 CALCULUS

Solve the ODE by integration or by remembering a differentiation formula.

- y′ + 2 sin 2πx = 0

- y′ = y

- y′ = −1.5y

- y′ = 4e−x cos x

- y″ = −y

- y′ = cosh 5.13x

- y″′ = e−0.2x

9–15 VERIFICATION. INITIAL VALUE PROBLEM (IVP)

(a) Verify that y is a solution of the ODE. (b) Determine from y the particular solution of the IVP. (c) Graph the solution of the IVP.

- 9. y′ + 4y = 1.4, y = ce−4x + 0.35, y(0) = 2

- 10.

- 11.

- 12. yy′ = 4x, y2 − 4x2 = c(y > 0), y(1) = 4

- 13.

- 14. y′ tan x = 2y − 8, y = c sin2 x + 4,

- 15. Find two constant solutions of the ODE in Prob. 13 by inspection.

- 16. Singular solution. An ODE may sometimes have an additional solution that cannot be obtained from the general solution and is then called a singular solution. The ODE y′2 − xy′ + y = 0 is of this kind. Show by differentiation and substitution that it has the general solution y = cx − c2 and the singular solution y = x2/4. Explain Fig. 6.

Fig. 6. Particular solutions and singular solution in Problem 16

17–20 MODELING, APPLICATIONS

These problems will give you a first impression of modeling. Many more problems on modeling follow throughout this chapter.

- 17. Half-life. The half-life measures exponential decay. It is the time in which half of the given amount of radioactive substance will disappear. What is the half-life of

(in years) in Example 5?

(in years) in Example 5? - 18. Half-life. Radium has a half-life of about 3.6 days.

(a) Given 1 gram, how much will still be present after 1 day?

(b) After 1 year?

- 19. Free fall. In dropping a stone or an iron ball, air resistance is practically negligible. Experiments show that the acceleration of the motion is constant (equal to g = 9.80 m/sec2 = 32 ft/sec2, called the acceleration of gravity). Model this as an ODE for y(t), the distance fallen as a function of time t. If the motion starts at time t = 0 from rest (i.e., with velocity ν = y′ = 0), show that you obtain the familiar law of free fall

- 20. Exponential decay. Subsonic flight. The efficiency of the engines of subsonic airplanes depends on air pressure and is usually maximum near 35,000 ft. Find the air pressure y(x) at this height. Physical information. The rate of change y′(x) is proportional to the pressure. At 18,000 ft it is half its value y0 = y(0) at sea level. Hint. Remember from calculus that if y = ekx, then y′ = kekx = ky. Can you see without calculation that the answer should be close to y0/4?

1.2 Geometric Meaning of y′ = f(x, y). Direction Fields, Euler's Method

A first-order ODE

has a simple geometric interpretation. From calculus you know that the derivative y′(x) of y(x is the slope of y(x). Hence a solution curve of (1) that passes through a point (x0, y0) must have, at that point, the slope y′(x0) equal to the value of f at that point; that is,

![]()

Using this fact, we can develop graphic or numeric methods for obtaining approximate solutions of ODEs (1). This will lead to a better conceptual understanding of an ODE (1). Moreover, such methods are of practical importance since many ODEs have complicated solution formulas or no solution formulas at all, whereby numeric methods are needed.

Graphic Method of Direction Fields. Practical Example Illustrated in Fig. 7. We can show directions of solution curves of a given ODE (1) by drawing short straight-line segments (lineal elements) in the xy-plane. This gives a direction field (or slope field) into which you can then fit (approximate) solution curves. This may reveal typical properties of the whole family of solutions.

Figure 7 shows a direction field for the ODE

![]()

obtained by a CAS (Computer Algebra System) and some approximate solution curves fitted in.

Fig. 7. Direction field of y′ = y + x, with three approximate solution curves passing through (0, 1), (0, 0), (0, −1), respectively

If you have no CAS, first draw a few level curves f(x, y) = const of f(x, y), then parallel lineal elements along each such curve (which is also called an isocline, meaning a curve of equal inclination), and finally draw approximation curves fit to the lineal elements.

We shall now illustrate how numeric methods work by applying the simplest numeric method, that is Euler's method, to an initial value problem involving ODE (2). First we give a brief description of Euler's method.

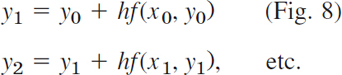

Numeric Method by Euler

Given an ODE (1) and an initial value y(x0) = y0, Euler's method yields approximate solution values at equidistant x-values x0, x1 = x0 + h, x2 = x0 + 2h, …, namely,

In general,

![]()

where the step h equals, e.g., 0.1 or 0.2 (as in Table 1.1) or a smaller value for greater accuracy.

Fig. 8. First Euler step, showing a solution curve, its tangent at (x0, y0), step h and increment hf(x0, y0) in the formula for y1

Table 1.1 shows the computation of n = 5 steps with step h = 0.2 for the ODE (2) and initial condition y(0) = 0, corresponding to the middle curve in the direction field. We shall solve the ODE exactly in Sec. 1.5. For the time being, verify that the initial value problem has the solution y = ex − x − 1. The solution curve and the values in Table 1.1 are shown in Fig. 9. These values are rather inaccurate. The errors y(xn) − yn are shown in Table 1.1 as well as in Fig. 9. Decreasing h would improve the values, but would soon require an impractical amount of computation. Much better methods of a similar nature will be discussed in Sec. 21.1.

Table 1.1 Euler method for y′ = y + x, y(0) = 0 for x = 0, …, 1.0 with step h = 0.2

Fig. 9. Euler method: Approximate values in Table 1.1 and solution curve

1–8 DIRECTION FIELDS, SOLUTION CURVES

Graph a direction field (by a CAS or by hand). In the field graph several solution curves by hand, particularly those passing through the given points (x, y).

- y′ = 1 + y2,

- yy′ + 4x = 0, (1, 1), (0, 2)

- y′ = 1 − y2, (0, 0), (2,

)

) - y′ = 2y − y2, (0, 0), (0, 1), (0, 2), (0, 3)

- y′ = x − 1/y, (1, )

- y′ = sin2y, (0, −0.4), (0, 1)

- y′ = ey/x, (2, 2), (3, 3)

- y′ = −2xy, (0, ), (0, 1), (0, 2)

9–10 ACCURACY OF DIRECTION FIELDS

Direction fields are very useful because they can give you an impression of all solutions without solving the ODE, which may be difficult or even impossible. To get a feel for the accuracy of the method, graph a field, sketch solution curves in it, and compare them with the exact solutions.

- 9. y′ = cos πx

- 10.

- 11. Autonomous ODE. This means an ODE not showing x (the independent variable) explicitly. (The ODEs in Probs. 6 and 10 are autonomous.) What will the level curves f(x, y) = const (also called isoclines curves of equal inclination) of an autonomous ODE look like? Give reason.

12–15 MOTIONS

Model the motion of a body B on a straight line with velocity as given, y(t) being the distance of B from a point y = 0 at time t. Graph a direction field of the model (the ODE). In the field sketch the solution curve satisfying the given initial condition.

- 12. Product of velocity times distance constant, equal to 2, y(0) = 2.

- 13. Distance = Velocity × Time, y(1) = 1

- 14. Square of the distance plus square of the velocity equal to 1, initial distance

- 15. Parachutist. Two forces act on a parachutist, the attraction by the earth mg (m = mass of person plus equipment, g = 9.8 m/sec2 the acceleration of gravity) and the air resistance, assumed to be proportional to the square of the velocity ν(t). Using Newton's second law of motion (mass × acceleration = resultant of the forces), set up a model (an ODE for ν(t)). Graph a direction field (choosing m and the constant of proportionality equal to 1). Assume that the parachute opens when ν = 10 m/sec. Graph the corresponding solution in the field. What is the limiting velocity? Would the parachute still be sufficient if the air resistance were only proportional to ν(t)?

- 16. CAS PROJECT. Direction Fields. Discuss direction fields as follows.

(a) Graph portions of the direction field of the ODE (2) (see Fig. 7), for instance, −5

x 2, −1 y 5. Explain what you have gained by this enlargement of the portion of the field.

x 2, −1 y 5. Explain what you have gained by this enlargement of the portion of the field.(b) Using implicit differentiation, find an ODE with the general solution x2 + 9y2 = c(y > 0). Graph its direction field. Does the field give the impression that the solution curves may be semi-ellipses? Can you do similar work for circles? Hyperbolas? Parabolas? Other curves?

(c) Make a conjecture about the solutions of y′ = −x/y from the direction field.

(d) Graph the direction field of

and some solutions of your choice. How do they behave? Why do they decrease for? y > 0?

and some solutions of your choice. How do they behave? Why do they decrease for? y > 0?

17–20 EULER'S METHOD

This is the simplest method to explain numerically solving an ODE, more precisely, an initial value problem (IVP). (More accurate methods based on the same principle are explained in Sec. 21.1.) Using the method, to get a feel for numerics as well as for the nature of IVPs, solve the IVP numerically with a PC or a calculator, 10 steps. Graph the computed values and the solution curve on the same coordinate axes.

- 17. y′ = y, y(0) = 1, h = 0.1

- 18. y′ = y, y(0) = 1, h = 0.01

- 19. y′ = (y − x)2, y(0) = 0, h = 0.1 Sol. y = x − tanh x

- 20. y′ = −5x4y2, y(0) = 1, h = 0.2 Sol. y = 1/(1 + x)5

1.3 Separable ODEs. Modeling

Many practically useful ODEs can be reduced to the form

by purely algebraic manipulations. Then we can integrate on both sides with respect to x, obtaining

On the left we can switch to y as the variable of integration. By calculus, y′ dx = dy, so that

If f and g are continuous functions, the integrals in (3) exist, and by evaluating them we obtain a general solution of (1). This method of solving ODEs is called the method of separating variables, and (1) is called a separable equation, because in (3) the variables are now separated: x appears only on the right and y only on the left.

The ODE y′ = 1 + y2 is separable because it can be written

It is very important to introduce the constant of integration immediately when the integration is performed. If we wrote arctan y = x, then y = tan x, and then introduced c, we would have obtained y = tan x + c, which is not a solution (when c ≠ 0). Verify this.

The ODE y′ = (x + 1)e−xy2 is separable; we obtain y−2 dy = (x + 1)e−x dx.

By integration, ![]() .

.

EXAMPLE 3 Initial Value Problem (IVP). Bell-Shaped Curve

Solve y′ = −2xy, y(0) = 1.8.

Solution. By separation and integration,

This is the general solution. From it and the initial condition, y(0) = ce0 = c = 1.8. Hence the IVP has the solution ![]() . This is a particular solution, representing a bell-shaped curve (Fig. 10).

. This is a particular solution, representing a bell-shaped curve (Fig. 10).

Fig. 10. Solution in Example 3 (bell-shaped curve)

Modeling

The importance of modeling was emphasized in Sec. 1.1, and separable equations yield various useful models. Let us discuss this in terms of some typical examples.

EXAMPLE 4 Radiocarbon Dating2

In September 1991 the famous Iceman (Oetzi), a mummy from the Neolithic period of the Stone Age found in the ice of the Oetztal Alps (hence the name “Oetzi”) in Southern Tyrolia near the Austrian–Italian border, caused a scientific sensation. When did Oetzi approximately live and die if the ratio of carbon ![]() to carbon

to carbon ![]() in this mummy is 52.5% of that of a living organism?

in this mummy is 52.5% of that of a living organism?

Physical Information. In the atmosphere and in living organisms, the ratio of radioactive carbon ![]() (made radioactive by cosmic rays) to ordinary carbon

(made radioactive by cosmic rays) to ordinary carbon ![]() is constant. When an organism dies, its absorption of

is constant. When an organism dies, its absorption of ![]() by breathing and eating terminates. Hence one can estimate the age of a fossil by comparing the radioactive carbon ratio in the fossil with that in the atmosphere. To do this, one needs to know the half-life of

by breathing and eating terminates. Hence one can estimate the age of a fossil by comparing the radioactive carbon ratio in the fossil with that in the atmosphere. To do this, one needs to know the half-life of ![]() , which is 5715 years (CRC Handbook of Chemistry and Physics, 83rd ed., Boca Raton: CRC Press, 2002, page 11–52, line 9).

, which is 5715 years (CRC Handbook of Chemistry and Physics, 83rd ed., Boca Raton: CRC Press, 2002, page 11–52, line 9).

Solution. Modeling. Radioactive decay is governed by the ODE y′ = ky (see Sec. 1.1, Example 5). By separation and integration (where t is time and y0 is the initial ratio of ![]() to

to ![]() )

)

Next we use the half-life H = 5715 to determine k. When t = H, half of the original substance is still present. Thus,

![]()

Finally, we use the ratio 52.5% for determining the time t when Oetzi died (actually, was killed),

![]()

Other methods show that radiocarbon dating values are usually too small. According to recent research, this is due to a variation in that carbon ratio because of industrial pollution and other factors, such as nuclear testing.

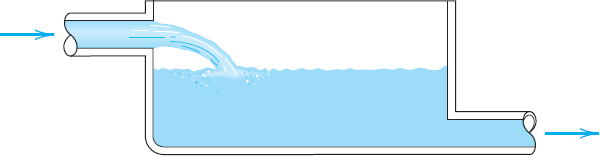

Mixing problems occur quite frequently in chemical industry. We explain here how to solve the basic model involving a single tank. The tank in Fig. 11 contains 1000 gal of water in which initially 100 lb of salt is dissolved. Brine runs in at a rate of 10 gal min, and each gallon contains 5 lb of dissoved salt. The mixture in the tank is kept uniform by stirring. Brine runs out at 10 gal min. Find the amount of salt in the tank at any time t.

Solution. Step 1. Setting up a model. Let y(t) denote the amount of salt in the tank at time t. Its time rate of change is

![]()

5 lb times 10 gal gives an inflow of 50 lb of salt. Now, the outflow is 10 gal of brine. This is 10/1000 = 0.01 (= 1%) of the total brine content in the tank, hence 0.01 of the salt content y(t), that is, 0.01 y(t). Thus the model is the ODE

![]()

Step 2. Solution of the model. The ODE (4) is separable. Separation, integration, and taking exponents on both sides gives

![]()

Initially the tank contains 100 lb of salt. Hence y(0) = 100 is the initial condition that will give the unique solution. Substituting y = 100 and t = 0 in the last equation gives 100 − 5000 = ce0 = c. Hence c = −4900. Hence the amount of salt in the tank at time t is

![]()

This function shows an exponential approach to the limit 5000 lb; see Fig. 11. Can you explain physically that should increase with time? That its limit is 5000 lb? Can you see the limit directly from the ODE?

The model discussed becomes more realistic in problems on pollutants in lakes (see Problem Set 1.5, Prob. 35) or drugs in organs. These types of problems are more difficult because the mixing may be imperfect and the flow rates (in and out) may be different and known only very roughly.

Fig. 11. Mixing problem in Example 5

EXAMPLE 6 Heating an Office Building (Newton's Law of Cooling3)

Suppose that in winter the daytime temperature in a certain office building is maintained at 70°F. The heating is shut off at 10 P.M. and turned on again at 6 A.M. On a certain day the temperature inside the building at 2 A.M. was found to be 65°F. The outside temperature was 50°F at 10 P.M. and had dropped to 40°F by 6 A.M. What was the temperature inside the building when the heat was turned on at 6 A.M.?

Physical information. Experiments show that the time rate of change of the temperature T of a body B (which conducts heat well, for example, as a copper ball does) is proportional to the difference between T and the temperature of the surrounding medium (Newton's law of cooling).

Solution. Step 1. Setting up a model. Let T(t) be the temperature inside the building and TA the outside temperature (assumed to be constant in Newton's law). Then by Newton's law,

![]()

Such experimental laws are derived under idealized assumptions that rarely hold exactly. However, even if a model seems to fit the reality only poorly (as in the present case), it may still give valuable qualitative information. To see how good a model is, the engineer will collect experimental data and compare them with calculations from the model.

Step 2. General solution. We cannot solve (6) because we do not know TA, just that it varied between 50°F and 40°F, so we follow the Golden Rule: If you cannot solve your problem, try to solve a simpler one. We solve (6) with the unknown function TA replaced with the average of the two known values, or 45°F. For physical reasons we may expect that this will give us a reasonable approximate value of T in the building at 6 A.M.

For constant TA = 45 (or any other constant value) the ODE (6) is separable. Separation, integration, and taking exponents gives the general solution

![]()

Step 3. Particular solution. We choose 10 P.M. to be t = 0. Then the given initial condition is T(0) = 70 and yields a particular solution, call it Tp. By substitution,

![]()

Step 4. Determination of k. We use T(4) = 65, where t = 4 is 2 A.M. Solving algebraically for k and inserting k into Tp(t) gives (Fig. 12)

![]()

Fig. 12. Particular solution (temperature) in Example 6

Step 5. Answer and interpretation. 6 A.M. is t = 8 (namely, 8 hours after 10 P.M.), and

![]()

Hence the temperature in the building dropped 9°F, a result that looks reasonable.

EXAMPLE 7 Leaking Tank. Outflow of Water Through a Hole (Torricelli's Law)

This is another prototype engineering problem that leads to an ODE. It concerns the outflow of water from a cylindrical tank with a hole at the bottom (Fig. 13). You are asked to find the height of the water in the tank at any time if the tank has diameter 2 m, the hole has diameter 1 cm, and the initial height of the water when the hole is opened is 2.25 m. When will the tank be empty?

Physical information. Under the influence of gravity the outflowing water has velocity

![]()

where h(t) is the height of the water above the hole at time t, and g = 980 cm/sec2 = 32.17 ft/sec2 is the acceleration of gravity at the surface of the earth.

Solution. Step 1. Setting up the model. To get an equation, we relate the decrease in water level h(t) to the outflow. The volume ΔV of the outflow during a short time Δt is

![]()

ΔV must equal the change ΔV* of the volume of the water in the tank. Now

![]()

where Δh (> 0) is the decrease of the height h(t) of the water. The minus sign appears because the volume of the water in the tank decreases. Equating ΔV and ΔV* gives

![]()

We now express ν according to Torricelli's law and then let Δt (the length of the time interval considered) approach 0—this is a standard way of obtaining an ODE as a model. That is, we have

![]()

and by letting Δt → 0 we obtain the ODE

![]()

where ![]() . This is our model, a first-order ODE.

. This is our model, a first-order ODE.

Step 2. General solution. Our ODE is separable. A/B is constant. Separation and integration gives

![]()

Dividing by 2 and squaring gives h = (c − 13.28At/B)2. Inserting 13.28A/B = 13.28 · 0.52π/1002π = 0.000332 yields the general solution

![]()

Step 3. Particular solution. The initial height (the initial condition) is h(0) = 225 cm. Substitution of t = 0 and h = 225 gives from the general solution c2 = 225, c = 15.00 and thus the particular solution (Fig. 13)

![]()

Step 4. Tank empty. hp(t) = 0 if t = 15.00/0.000332 = 45,181 [sec] = 12.6 [hours].

Here you see distinctly the importance of the choice of units—we have been working with the cgs system, in which time is measured in seconds! We used g = 980 cm/sec2.

Step 5. Checking. Check the result.

Fig. 13. Example 7. Outflow from a cylindrical tank (“leaking tank”). Torricelli's law

Extended Method: Reduction to Separable Form

Certain nonseparable ODEs can be made separable by transformations that introduce for y a new unknown function. We discuss this technique for a class of ODEs of practical importance, namely, for equations

Here, f is any (differentiable) function of y/x, such as sin(y/x), (y/x)4, and so on. (Such an ODE is sometimes called a homogeneous ODE, a term we shall not use but reserve for a more important purpose in Sec. 1.5.)

The form of such an ODE suggests that we set y/x = u; thus,

![]()

Substitution into y′ = f(y/x) then gives u′x + u = f(u) or u′x = f(u) − u. We see that if f(u) − u ≠ 0, this can be separated:

EXAMPLE 8 Reduction to Separable Form

Solve

![]()

Solution. To get the usual explicit form, divide the given equation by 2xy,

Now substitute y and y′ from (9) and then simplify by subtracting u on both sides,

![]()

You see that in the last equation you can now separate the variables,

![]()

Take exponents on both sides to get 1 + u2 = c/x or 1 + (y/x)2 = c/x. Multiply the last equation by x2 to obtain (Fig. 14)

![]()

This general solution represents a family of circles passing through the origin with centers on the x-axis.

Fig. 14. General solution (family of circles) in Example 8

- CAUTION! Constant of integration. Why is it important to introduce the constant of integration immediately when you integrate?

2–10 GENERAL SOLUTION

Find a general solution. Show the steps of derivation. Check your answer by substitution.

- 2. y3y′ + x3 = 0

- 3. y′ = sec2y

- 4. y′ sin 2πx = πy cos 2πx

- 5. yy′ + 36x = 0

- 6. y′ = e2x−1y2

- 7.

- 8. y′ = (y + 4x)2 (Set y + 4x = ν)

- 9. xy′ = y2 + y (Set y/x = u)

- 10. xy′ = x + y (Set y/x = u)

11–17 INITIAL VALUE PROBLEMS (IVPS)

Solve the IVP. Show the steps of derivation, beginning with the general solution.

- 11. xy′ + y = 0, y(4) = 6

- 12. y′ = 1 + 4y2, y(1) = 0

- 13. y′ cosh2x = sin2y,

- 14. dr/dt = −2tr, r(0) = r0

- 15. y′ = −4x/y, y(2) = 3

- 16. y′ (x + y − 2)2, y(0) = 2 (Set ν = x + y − 2)

- 17. xy′ = y + 3x4 cos2(y/x), y(1) = 0

- 18. Particular solution. Introduce limits of integration in (3) such that y obtained from (3) satisfies the initial condition y(x0) = y0.

- 19. Exponential growth. If the growth rate of the number of bacteria at any time t is proportional to the number present at t and doubles in 1 week, how many bacteria can be expected after 2 weeks? After 4 weeks?

- 20. Another population model.

(a) If the birth rate and death rate of the number of bacteria are proportional to the number of bacteria present, what is the population as a function of time.

(b) What is the limiting situation for increasing time? Interpret it.

- 21. Radiocarbon dating. What should be the

content (in percent of y0) of a fossilized tree that is claimed to be 3000 years old? (See Example 4.)

content (in percent of y0) of a fossilized tree that is claimed to be 3000 years old? (See Example 4.) - 22. Linear accelerators are used in physics for accelerating charged particles. Suppose that an alpha particle enters an accelerator and undergoes a constant acceleration that increases the speed of the particle from 103 m/sec to 104 m/sec in 10−3 sec. Find the acceleration a and the distance traveled during that period of 10−3 sec.

- 23. Boyle–Mariotte's law for ideal gases.5 Experiments show for a gas at low pressure p (and constant temperature) the rate of change of the volume V(p) equals −V/p. Solve the model.

- 24. Mixing problem. A tank contains 400 gal of brine in which 100 lb of salt are dissolved. Fresh water runs into the tank at a rate of 2 gals/min. The mixture, kept practically uniform by stirring, runs out at the same rate. How much salt will there be in the tank at the end of 1 hour?

- 25. Newton's law of cooling. A thermometer, reading 5°C, is brought into a room whose temperature is 22°C. One minute later the thermometer reading is 12°C. How long does it take until the reading is practically 22°C, say, 21.9°C?

- 26. Gompertz growth in tumors. The Gompertz model is y′ = −Ay ln y (A > 0), where y(t) is the mass of tumor cells at time t. The model agrees well with clinical observations. The declining growth rate with increasing y > 1 corresponds to the fact that cells in the interior of a tumor may die because of insufficient oxygen and nutrients. Use the ODE to discuss the growth and decline of solutions (tumors) and to find constant solutions. Then solve the ODE.

- 27. Dryer. If a wet sheet in a dryer loses its moisture at a rate proportional to its moisture content, and if it loses half of its moisture during the first 10 min of drying, when will it be practically dry, say, when will it have lost 99% of its moisture? First guess, then calculate.

- 28. Estimation. Could you see, practically without calculation, that the answer in Prob. 27 must lie between 60 and 70 min? Explain.

- 29. Alibi? Jack, arrested when leaving a bar, claims that he has been inside for at least half an hour (which would provide him with an alibi). The police check the water temperature of his car (parked near the entrance of the bar) at the instant of arrest and again 30 min later, obtaining the values 190°F and 110°F, respectively. Do these results give Jack an alibi? (Solve by inspection.)

- 30. Rocket. A rocket is shot straight up from the earth, with a net acceleration (= acceleration by the rocket engine minus gravitational pullback) of 7t m/sec2 during the initial stage of flight until the engine cut out at t = 10 sec. How high will it go, air resistance neglected?

- 31. Solution curves of y′ = g(y/x). Show that any (nonvertical) straight line through the origin of the xy-plane intersects all these curves of a given ODE at the same angle.

- 32. Friction. If a body slides on a surface, it experiences friction F (a force against the direction of motion). Experiments show that |F| = μ|N| (Coulomb's6 law of kinetic friction without lubrication), where N is the normal force (force that holds the two surfaces together; see Fig. 15) and the constant of proportionality μ is called the coefficient of kinetic friction. In Fig. 15 assume that the body weighs 45 nt (about 10 lb; see front cover for conversion). μ = 0.20 (corresponding to steel on steel), a = 30°, the slide is 10 m long, the initial velocity is zero, and air resistance is negligible. Find the velocity of the body at the end of the slide.

- 33. Rope. To tie a boat in a harbor, how many times must a rope be wound around a bollard (a vertical rough cylindrical post fixed on the ground) so that a man holding one end of the rope can resist a force exerted by the boat 1000 times greater than the man can exert? First guess. Experiments show that the change ΔS of the force S in a small portion of the rope is proportional to S and to the small angle Δφ in Fig. 16. Take the proportionality constant 0.15. The result should surprise you!

- 34. TEAM PROJECT. Family of Curves. A family of curves can often be characterized as the general solution of y′ = f(x, y).

(a) Show that for the circles with center at the origin we get y′ = −x/y.

(b) Graph some of the hyperbolas xy = c. Find an ODE for them.

(c) Find an ODE for the straight lines through the origin.

(d) You will see that the product of the right sides of the ODEs in (a) and (c) equals −1. Do you recognize this as the condition for the two families to be orthogonal (i.e., to intersect at right angles)? Do your graphs confirm this?

(e) Sketch families of curves of your own choice and find their ODEs. Can every family of curves be given by an ODE?

- 35. CAS PROJECT. Graphing Solutions. A CAS can usually graph solutions, even if they are integrals that cannot be evaluated by the usual analytical methods of calculus.

(a) Show this for the five initial value problems,

, y(0) = 0, ±1, ±2, graphing all five curves on the same axes.

, y(0) = 0, ±1, ±2, graphing all five curves on the same axes.(b) Graph approximate solution curves, using the first few terms of the Maclaurin series (obtained by termwise integration of that of y′) and compare with the exact curves.

(c) Repeat the work in (a) for another ODE and initial conditions of your own choice, leading to an integral that cannot be evaluated as indicated.

- 36. TEAM PROJECT. Torricelli's Law. Suppose that the tank in Example 7 is hemispherical, of radius R, initially full of water, and has an outlet of 5 cm2 cross-sectional area at the bottom. (Make a sketch.) Set up the model for outflow. Indicate what portion of your work in Example 7 you can use (so that it can become part of the general method independent of the shape of the tank). Find the time t to empty the tank (a) for any R, (b) for R = 1 m. Plot t as function of R. Find the time when h = R/2 (a) for any R, (b) for R = 1 m.

1.4 Exact ODEs. Integrating Factors

We recall from calculus that if a function u(x, y) has continuous partial derivatives, its differential (also called its total differential) is

From this it follows that if u(x, y) = c = const, then du = 0.

For example, if u = x + x2y3 = c, then

![]()

or

an ODE that we can solve by going backward. This idea leads to a powerful solution method as follows.

A first-order ODE M(x, y) + N(x, y)y′ = 0, written as (use dy = y′dx as in Sec. 1.3)

is called an exact differential equation if the differential form M(x, y)dx + N(x, y)dy is exact, that is, this form is the differential

of some function u(x, y). Then (1) can be written

![]()

By integration we immediately obtain the general solution of (1) in the form

This is called an implicit solution, in contrast to a solution y = h(x) as defined in Sec. 1.1, which is also called an explicit solution, for distinction. Sometimes an implicit solution can be converted to explicit form. (Do this for x2 + y2 = 1.) If this is not possible, your CAS may graph a figure of the contour lines (3) of the function u(x, y) and help you in understanding the solution.

Comparing (1) and (2), we see that (1) is an exact differential equation if there is some function u(x, y) such that

From this we can derive a formula for checking whether (1) is exact or not, as follows.

Let M and N be continuous and have continuous first partial derivatives in a region in the xy-plane whose boundary is a closed curve without self-intersections. Then by partial differentiation of (4) (see App. 3.2 for notation),

By the assumption of continuity the two second partial derivaties are equal. Thus

This condition is not only necessary but also sufficient for (1) to be an exact differential equation. (We shall prove this in Sec. 10.2 in another context. Some calculus books, for instance, [GenRef 12], also contain a proof.)

If (1) is exact, the function u(x, y) can be found by inspection or in the following systematic way. From (4a) we have by integration with respect to x

in this integration, y is to be regarded as a constant, and k(y) plays the role of a “constant” of integration. To determine k(y), we derive ∂u/∂y from (6), use (4b) to get dk/dy, and integrate dk/dy to get k. (See Example 1, below.)

Formula (6) was obtained from (4a). Instead of (4a) we may equally well use (4b). Then, instead of (6), we first have by integration with respect to y

To determine l(x), we derive ∂u/∂x from (6*), use (4a) to get dl/dx, and integrate. We illustrate all this by the following typical examples.

Solve

![]()

Solution. Step 1. Test for exactness. Our equation is of the form (1) with

Thus

From this and (5) we see that (7) is exact.

Step 2. Implicit general solution. From (6) we obtain by integration

To find k(y), we differentiate this formula with respect to y and use formula (4b), obtaining

![]()

Hence dk/dy = 3y2 + 2y. By integration, k = y3 + y2 + c*. Inserting this result into (8) and observing (3), we obtain the answer

![]()

Step 3. Checking an implicit solution. We can check by differentiating the implicit solution u(x, y) = c implicitly and see whether this leads to the given ODE (7):

![]()

This completes the check.

EXAMPLE 2 An Initial Value Problem

Solve the initial value problem

![]()

Solution. You may verify that the given ODE is exact. We find u. For a change, let us use (6*),

![]()

From this, ∂u/∂x = cos y sinh x + dl/dx = M = cos y sinh x + 1. Hence dl/dx = 1. By integration, l(x) = x + c*. This gives the general solution u(x, y) = cos y cosh x + x = c. From the initial condition, cos 2 cosh 1 + 1 = 0.358 = c. Hence the answer is cos y cosh x + x = 0.358. Figure 17 shows the particular solutions for c = 0, 0.358 (thicker curve), 1, 2, 3. Check that the answer satisfies the ODE. (Proceed as in Example 1.) Also check that the initial condition is satisfied.

Fig. 17. Particular solutions in Example 2

EXAMPLE 3 WARNING! Breakdown in the Case of Nonexactness

The equation −y dx + x dy = 0 is not exact because M = −y and N = x, so that in (5), but ∂M/∂y = −1 but ∂N/∂x = 1. Let us show that in such a case the present method does not work. From (6),

Now, ∂u/∂y should equal N = x, by (4b). However, this is impossible because k(y) can depend only on y. Try (6*); it will also fail. Solve the equation by another method that we have discussed.

Reduction to Exact Form. Integrating Factors

The ODE in Example 3 is −y dx + x dy = 0. It is not exact. However, if we multiply it by 1/x2, we get an exact equation [check exactness by (5)!],

Integration of (11) then gives the general solution y/x = c = const.

This example gives the idea. All we did was to multiply a given nonexact equation, say,

by a function F that, in general, will be a function of both x and y. The result was an equation

![]()

that is exact, so we can solve it as just discussed. Such a function F(x, y) is then called an integrating factor of (12).

The integrating factor in (11) is F = 1/x2. Hence in this case the exact equation (13) is

These are straight lines y = cx through the origin. (Note that x = 0 is also a solution of −y dx + x dy = 0.)

It is remarkable that we can readily find other integrating factors for the equation −y dx + x dy = 0, namely, 1/y2, 1/(xy), and 1/(x2 + y2), because

How to Find Integrating Factors

In simpler cases we may find integrating factors by inspection or perhaps after some trials, keeping (14) in mind. In the general case, the idea is the following.

For M dx + N dy = 0 the exactness condition (5) is ∂M/∂y = ∂N/∂x. Hence for (13), FP dx + FQ dy = 0, the exactness condition is

By the product rule, with subscripts denoting partial derivatives, this gives

![]()

In the general case, this would be complicated and useless. So we follow the Golden Rule: If you cannot solve your problem, try to solve a simpler one—the result may be useful (and may also help you later on). Hence we look for an integrating factor depending only on one variable: fortunately, in many practical cases, there are such factors, as we shall see. Thus, let F = F(x). Then Fy = 0, and Fx = F′ = dF/dx, so that (15) becomes

![]()

Dividing by FQ and reshuffling terms, we have

This proves the following theorem.

THEOREM 1 Integrating Factor F(x)

If (12) is such that the right side R of (16) depends only on x, then (12) has an integrating factor F = F(x), which is obtained by integrating (16) and taking exponents on both sides.

Similarly, if F* = F*(y) then instead of (16) we get

and we have the companion

THEOREM 2 Integrating Factor F*(y)

If (12) is such that the right side R* of (18) depends only on y, then (12) has an integrating factor F* = F*(y), which is obtained from (18) in the form

EXAMPLE 5 Application of Theorems 1 and 2. Initial Value Problem

Using Theorem 1 or 2, find an integrating factor and solve the initial value problem

![]()

Solution. Step 1. Nonexactness. The exactness check fails:

Step 2. Integrating factor. General solution. Theorem 1 fails because R [the right side of (16)] depends on both x and y.

![]()

Try Theorem 2. The right side of (18) is

![]()

Hence (19) gives the integrating factor F*(y) = e−y. From this result and (20) you get the exact equation

![]()

Test for exactness; you will get 1 on both sides of the exactness condition. By integration, using (4a),

Differentiate this with respect to y and use (4b) to get

Hence the general solution is

![]()

Setp 3. Particular solution. The initial condition y(0) = −1 gives u(0, −1) = 1 + 0 + e = 3.72. Hence the answer is ex + xy + e−y = 1 + e = 3.72. Figure 18 shows several particular solutions obtained as level curves of u(x, y) = c, obtained by a CAS, a convenient way in cases in which it is impossible or difficult to cast a solution into explicit form. Note the curve that (nearly) satisfies the initial condition.

Step 4. Checking. Check by substitution that the answer satisfies the given equation as well as the initial condition.

Fig. 18. Particular solutions in Example 5

1–14 ODEs. INTEGRATING FACTORS

Test for exactness. If exact, solve. If not, use an integrating factor as given or obtained by inspection or by the theorems in the text. Also, if an initial condition is given, find the corresponding particular solution.

- 2xy dx + x2 dy = 0

- x3dx + y3dy = 0

- sin x cos y dx + cos x sin y dy = 0

- e3θ(dr + 3r dθ) = 0

- (x2 + y2)dx − 2xy dy = 0

- 3(y + 1) dx = 2x dy, (y + 1)x−4

- 2x tan y dx + sec2 y dy = 0

- ex(cos y dx − sin y dy) = 0

- e2x(2 cos y dx − sin y dy) = 0, y(0) = 0

- y dx + [y + tan (x + y)] dy = 0, cos (x + y)

- 2 cosh x cos y dx = sinh x sin y dy

- e−y dx + e−x(−e−y + 1)dy = 0, F = ex+y

- (x + 1)y dx + (b + 1)x dy = 0, y(1) = 1, F = xayb

- Exactness. Under what conditions for the constants a, b, k, l is (ax + by) dx + (kx + ly) dy = 0 exact? Solve the exact ODE.

- TEAM PROJECT. Solution by Several Methods. Show this as indicated. Compare the amount of work.

(a) ey(sinh x dx + cosh x dy) = 0 as an exact ODE and by separation.

(b) (1 + 2x)cos y dx + dy/cos y = 0 by Theorem 2 and by separation.

(c) (x2 + y2)dx − 2xy dy = 0 by Theorem 1 or 2 and by separation with ν = y/x.

(d) 3x2y dx + 4x3 dy = 0 by Theorems 1 and 2 and by separation.

(e) Search the text and the problems for further ODEs that can be solved by more than one of the methods discussed so far. Make a list of these ODEs. Find further cases of your own.

- WRITING PROJECT. Working Backward. Working backward from the solution to the problem is useful in many areas. Euler, Lagrange, and other great masters did it. To get additional insight into the idea of integrating factors, start from a u(x, y) of your choice, find du = 0, destroy exactness by division by some F(x, y), and see what ODE's solvable by integrating factors you can get. Can you proceed systematically, beginning with the simplest F(x, y)?

- CAS PROJECT. Graphing Particular Solutions. Graph particular solutions of the following ODE, proceeding as explained.

(a) Show that (21) is not exact. Find an integrating factor using either Theorem 1 or 2. Solve (21).

(b) Solve (21) by separating variables. Is this simpler than (a)?

(c) Graph the seven particular solutions satisfying the following initial conditions y(0) = 1,

,

,  , ±1 (see figure below).

, ±1 (see figure below).(d) Which solution of (21) do we not get in (a) or (b)?

Particular solutions in CAS Project 18

1.5 Linear ODEs. Bernoulli Equation. Population Dynamics

Linear ODEs or ODEs that can be transformed to linear form are models of various phenomena, for instance, in physics, biology, population dynamics, and ecology, as we shall see. A first-order ODE is said to be linear if it can be brought into the form

by algebra, and nonlinear if it cannot be brought into this form.

The defining feature of the linear ODE (1) is that it is linear in both the unknown function y and its derivative y′ = dy/dx, whereas p and r may be any given functions of x. If in an application the independent variable is time, we write t instead of x.

If the first term is f(x)y′ (instead of y′), divide the equation by f(x) to get the standard form (1), with y′ as the first term, which is practical.

For instance, y′ cos x + y sin x = x is a linear ODE, and its standard form is y′ + y tan x = x sec x.

The function r(x) on the right may be a force, and the solution y(x) a displacement in a motion or an electrical current or some other physical quantity. In engineering, r(x) is frequently called the input, and y(x) is called the output or the response to the input (and, if given, to the initial condition).

Homogeneous Linear ODE. We want to solve (1) in some interval a < x < b, call it J, and we begin with the simpler special case that r(x) is zero for all x in J. (This is sometimes written r(x) ≡ 0.) Then the ODE (1) becomes

and is called homogeneous. By separating variables and integrating we then obtain

![]()

Taking exponents on both sides, we obtain the general solution of the homogeneous ODE (2),

here we may also choose c = 0 and obtain the trivial solution y(x) = 0 for all x in that interval.

Nonhomogeneous Linear ODE. We now solve (1) in the case that r(x) in (1) is not everywhere zero in the interval J considered. Then the ODE (1) is called nonhomogeneous. It turns out that in this case, (1) has a pleasant property; namely, it has an integrating factor depending only on x. We can find this factor F(x) by Theorem 1 in the previous section or we can proceed directly, as follows. We multiply (1) by F(x), obtaining

![]()

The left side is the derivative (Fy)′ = F′ y + Fy′ of the product Fy if

![]()

By separating variables, dF/F = p dx. By integration, writing h = ∫p dx,

![]()

With this F and h′ = p, Eq. (1*) becomes

![]()

By integration,

![]()

Dividing by eh, we obtain the desired solution formula

This reduces solving (1) to the generally simpler task of evaluating integrals. For ODEs for which this is still difficult, you may have to use a numeric method for integrals from Sec. 19.5 or for the ODE itself from Sec. 21.1. We mention that h has nothing to do with in Sec. 1.1 and that the constant of integration in h does not matter; see Prob. 2.

The structure of (4) is interesting. The only quantity depending on a given initial condition is c. Accordingly, writing (4) as a sum of two terms,

we see the following:

EXAMPLE 1 First-Order ODE, General Solution, Initial Value Problem

Solve the initial value problem

![]()

Solution. Here p = tan x, r = sin 2x = 2 sin x cos x, and

![]()

From this we see that in (4),

![]()

and the general solution of our equation is

![]()

From this and the initial condition, 1 = c · 1 − 2 · 12; thus c = 3 and the solution of our initial value problem is y = 3 cos x − 2 cos2x. Here 3 cos x is the response to the initial data, and −2 cos2 x is the response to the input sin 2x.

Model the RL-circuit in Fig. 19 and solve the resulting ODE for the current I(t) A (amperes), where t is time. Assume that the circuit contains as an EMF E(t) (electromotive force) a battery of E = 48 V (volts), which is constant, a resistor of R = 11 Ω (ohms), and an inductor of L = 0.1 H (henrys), and that the current is initially zero.

Physical Laws. A current I in the circuit causes a voltage drop RI across the resistor (Ohm's law) and a voltage drop LI′ = L dI/dt across the conductor, and the sum of these two voltage drops equals the EMF (Kirchhoff's Voltage Law, KVL).

Remark. In general, KVL states that “The voltage (the electromotive force EMF) impressed on a closed loop is equal to the sum of the voltage drops across all the other elements of the loop.” For Kirchoff's Current Law (KCL) and historical information, see footnote 7 in Sec. 2.9.

Solution. According to these laws the model of the RL-circuit is LI′ + RI = E(t), in standard form

![]()

We can solve this linear ODE by (4) with x = t, y = I, p = R/L, h = (R/L)t, obtaining the general solution

By integration,

In our case, R/L = 11/0.1 = 110 and E(t) = 48/0.1 = 480 = const; thus,

![]()

In modeling, one often gets better insight into the nature of a solution (and smaller roundoff errors) by inserting given numeric data only near the end. Here, the general solution (7) shows that the current approaches the limit E/R = 48/11 faster the larger R/L is, in our case, R/L = 11/0.1 = 110, and the approach is very fast, from below if I(0) < 48/11 or from above if I(0) > 48/11. If I(0) = 48/11, the solution is constant (48/11 A). See Fig. 19.

The initial value I(0) = 0 gives I(0) = E/R + c = 0, c = −E/R and the particular solution

![]()

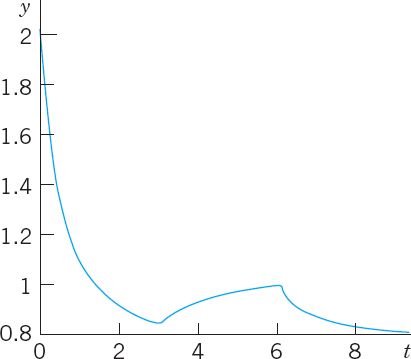

Assume that the level of a certain hormone in the blood of a patient varies with time. Suppose that the time rate of change is the difference between a sinusoidal input of a 24-hour period from the thyroid gland and a continuous removal rate proportional to the level present. Set up a model for the hormone level in the blood and find its general solution. Find the particular solution satisfying a suitable initial condition.

Solution. Step 1. Setting up a model. Let y(t) be the hormone level at time t. Then the removal rate is Ky(t). The input rate is A + B cos ωt, where ω = 2π/24 = π/12 and A is the average input rate; here A ![]() B to make the input rate nonnegative. The constants A, B, K can be determined from measurements. Hence the model is the linear ODE

B to make the input rate nonnegative. The constants A, B, K can be determined from measurements. Hence the model is the linear ODE

![]()

The initial condition for a particular solution ypart is ypart(0) with t = 0 suitably chosen, for example, 6:00 A.M.

Step 2. General solution. In (4) we have p = K = const, h = Kt, and r = A + B cos ωt. Hence (4) gives the general solution (evaluate ![]() cos ωt dt by integration by parts)

cos ωt dt by integration by parts)

The last term decreases to 0 as t increases, practically after a short time and regardless of c (that is, of the initial condition). The other part of y(t) is called the steady-state solution because it consists of constant and periodic terms. The entire solution is called the transient-state solution because it models the transition from rest to the steady state. These terms are used quite generally for physical and other systems whose behavior depends on time.

Step 3. Particular solution. Setting t = 0 in y(t) and choosing y0 = 0, we have

![]()

Inserting this result into y(t), we obtain the particular solution

![]()

with the steady-state part as before. To plot ypart we must specify values for the constants, say, A = B = 1 and K = 0.05. Figure 20 shows this solution. Notice that the transition period is relatively short (although K is small), and the curve soon looks sinusoidal; this is the response to the input ![]()

![]() .

.

Fig. 20. Particular solution in Example 3

Reduction to Linear Form. Bernoulli Equation

Numerous applications can be modeled by ODEs that are nonlinear but can be transformed to linear ODEs. One of the most useful ones of these is the Bernoulli equation7

If a = 0 or a = 1, Equation (9) is linear. Otherwise it is nonlinear. Then we set

![]()

We differentiate this and substitute y′ from (9), obtaining

![]()

Simplification gives

![]()

where y1 − a = u on the right, so that we get the linear ODE

For further ODEs reducible to linear form, see lnce's classic [A11] listed in App. 1. See also Team Project 30 in Problem Set 1.5.

Solve the following Bernoulli equation, known as the logistic equation (or Verhulst equation8):

Solution. Write (11) in the form (9), that is,

![]()

to see that a = 2, so that u = y1−a = y−1. Differentiate this u and substitute y′ from (11),

![]()

The last term is −Ay−1 = Hence we have obtained the linear ODE

![]()

The general solution is [by (4)]

![]()

Since u = 1/y, this gives the general solution of (11),

Directly from (11) we see that y = ≡ 0 (y(t) = 0 for all t) is also a solution.

Fig. 21. Logistic population model. Curves (9) in Example 4 with A/B = 4

Population Dynamics

The logistic equation (11) plays an important role in population dynamics, a field that models the evolution of populations of plants, animals, or humans over time t. If B = 0, then (11) is y′ = dy/dt = Ay. In this case its solution (12) is y = (1/c)eAt and gives exponential growth, as for a small population in a large country (the United States in early times!). This is called Malthus's law. (See also Example 3 in Sec. 1.1.)

The term −By2 in (11) is a “braking term” that prevents the population from growing without bound. Indeed, if we write y′ = Ay[1 − (B/A)y], we see that if y < A/B, then y′ > 0, so that an initially small population keeps growing as long as y < A/B. But if y > A/B, then y′ < 0 and the population is decreasing as long as y > A/B. The limit is the same in both cases, namely, A/B. See Fig. 21.

We see that in the logistic equation (11) the independent variable t does not occur explicitly. An ODE y′ = f(t, y) in which t does not occur explicitly is of the form

and is called an autonomous ODE. Thus the logistic equation (11) is autonomous.

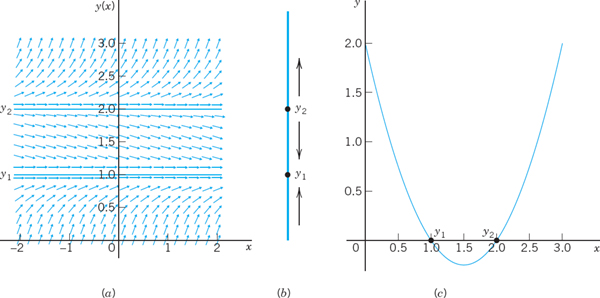

Equation (13) has constant solutions, called equilibrium solutions or equilibrium points. These are determined by the zeros of f(y), because f(y) = 0 gives y′ = 0 by (13); hence y = const. These zeros are known as critical points of (13). An equilibrium solution is called stable if solutions close to it for some t remain close to it for all further t. It is called unstable if solutions initially close to it do not remain close to it as t increases. For instance, y = 0 in Fig. 21 is an unstable equilibrium solution, and y = 4 is a stable one. Note that (11) has the critical points y = 0 and y = A/B.

EXAMPLE 5 Stable and Unstable Equilibrium Solutions. “Phase Line Plot”

The ODE y′ = (y − 1)(y − 2) has the stable equilibrium solution y1 = 1 and the unstable y2 = 2, as the direction field in Fig. 22 suggests. The values y1 and y2 are the zeros of the parabola f(y) = (y − 1)(y − 2) in the figure. Now, since the ODE is autonomous, we can “condense” the direction field to a “phase line plot” giving y1 and y2, and the direction (upward or downward) of the arrows in the field, and thus giving information about the stability or instability of the equilibrium solutions.

Fig. 22. Example 5. (A) Direction field. (B) “Phase line”. (C) Parabola f(y)

A few further population models will be discussed in the problem set. For some more details of population dynamics, see C. W. Clark. Mathematical Bioeconomics: The Mathematics of Conservation 3rd ed. Hoboken, NJ, Wiley, 2010.

Further applications of linear ODEs follow in the next section.

- CAUTION! Show that e−lnx = 1/x(not −x) and e−ln(sec x) = cos x.

- Integration constant. Give a reason why in (4) you may choose the constant of integration in ∫p dx to be zero.

3–13 GENERAL SOLUTION. INITIAL VALUE PROBLEMS

Find the general solution. If an initial condition is given, find also the corresponding particular solution and graph or sketch it. (Show the details of your work.)

- 3. y′ − y = 5.2

- 4. y′ = 2y − 4x

- 5. y′ + ky = e−kx

- 6.

- 7. xy′ = 2y + x3ex

- 8. y′ + y tan x = e−0.01x cos x, y(0) = 0

- 9. y′ + y sin x = ecosx, y(0) = −2.5

- 10.

- 11. y′ = (y − 2) cot x

- 12. xy′ +4y = 8x4, y(1) = 2

- 13. y′ = 6(y − 2.5) tanh 1.5x

- 14. CAS EXPERIMENT. (a) Solve the ODE y′ − y/x = −x−1 cos (1/x). Find an initial condition for which the arbitrary constant becomes zero. Graph the resulting particular solution, experimenting to obtain a good figure near x = 0.

(b) Generalizing (a) from n = 1 to arbitrary n, solve the ODE y′ − ny/x = −xn−2 cos (1/x). Find an initial condition as in (a) and experiment with the graph.

15–20 GENERAL PROPERTIES OF LINEAR ODEs

These properties are of practical and theoretical importance because they enable us to obtain new solutions from given ones. Thus in modeling, whenever possible, we prefer linear ODEs over nonlinear ones, which have no similar properties.

Show that nonhomogeneous linear ODEs (1) and homogeneous linear ODEs (2) have the following properties. Illustrate each property by a calculation for two or three equations of your choice. Give proofs.

- 15. The sum y1 + y2 of two solutions y1 and y2 of the homogeneous equation (2) is a solution of (2), and so is a scalar multiple ay1 for any constant a. These properties are not true for (1)!

- 16. y = 0 (that is, y(x = 0 for all x, also written y(x) ≡ 0) is a solution of (2) [not of (1) if r(x) ≠ 0!], called the trivial solution.

- 17. The sum of a solution of (1) and a solution of (2) is a solution of (1).

- 18. The difference of two solutions of (1) is a solution of (2).

- 19. If y1 is a solution of (1), what can you say about cy1?

- 20. If y1 and y2 are solutions of

and

and  respectively (with the same p!), what can you say about the sum y1 + y2?

respectively (with the same p!), what can you say about the sum y1 + y2? - 21. Variation of parameter. Another method of obtaining (4) results from the following idea. Write (3) as cy* where y* is the exponential function, which is a solution of the homogeneous linear ODE

. Replace the arbitrary constant c in (3) with a function u to be determined so that the resulting function y = uy* is a solution of the nonhomogeneous linear ODE y′ + py = r.

. Replace the arbitrary constant c in (3) with a function u to be determined so that the resulting function y = uy* is a solution of the nonhomogeneous linear ODE y′ + py = r.

22–28 NONLINEAR ODEs

Using a method of this section or separating variables, find the general solution. If an initial condition is given, find also the particular solution and sketch or graph it.

- 22. y′ + y = y2,

- 23. y′ + xy = xy−1, y(0) = 3

- 24. y′ + y = −x/y

- 25. y′ = 3.2y −10y2

- 26. y′ = (tan y)/(x − 1),

- 27. y′ = 1/(6ey − 2x)

- 28. 2xyy′ + (x − 1)y2 = x2ex (Set y2 = z)

- 29. REPORT PROJECT. Transformation of ODEs. We have transformed ODEs to separable form, to exact form, and to linear form. The purpose of such transformations is an extension of solution methods to larger classes of ODEs. Describe the key idea of each of these transformations and give three typical examples of your choice for each transformation. Show each step (not just the transformed ODE).

- 30. TEAM PROJECT. Riccati Equation. Clairaut Equation. Singular Solution.

A Riccati equation is of the form

A Clairaut equation is of the form

(a) Apply the transformation y = Y + 1/u to the Riccati equation (14), where Y is a solution of (14), and obtain for u the linear ODE u′ + (2Yg − p)u = −g. Explain the effect of the transformation by writing it as y = Y + ν, ν = 1/ν.

(b) Show that y = Y = x is a solution of the ODE y′ − (2x3 + 1) y = −x2y2 − x4 − x + 1 and slove this Riccati equation, showing the details.

(c) Solve the Clairaut equation y′2 − xy′ + y = 0 follows. Differentiate it with respect to x, obtaining y″(2y′ − x) = 0. Then solve (A) y″ = 0 and (B) 2y′ − x = 0 separately and substitute the two solutions (a) and (b) of (A) and (B) into the given ODE. Thus obtain (a) a general solution (straight lines) and (b) a parabola for which those lines (a) are tangents (Fig. 6 in Prob. Set 1.1); so (b) is the envelope of (a). Such a solution (b) that cannot be obtained from a general solution is called a singular solution.

(d) Show that the Clairaut equation (15) has as solutions a family of straight lines y = cx + g(c) and a singular solution determined by g′ (s) = −x, where s = y′, that forms the envelope of that family.

31–40 MODELING. FURTHER APPLICATIONS

- 31. Newton's law of cooling. If the temperature of a cake is 300°F when it leaves the oven and is 200°F ten minutes later, when will it be practically equal to the room temperature of 60°F, say, when will it be 61°F?

- 32. Heating and cooling of a building. Heating and cooling of a building can be modeled by the ODE

where T = T(t) is the temperature in the building at time t, Ta the outside temperature, Tw the temperature wanted in the building, and P the rate of increase of T due to machines and people in the building, and k1 and k2 are (negative) constants. Solve this ODE, assuming andP = const, Tw = const, and Ta varying sinusoidally over 24 hours, say, Ta = A − C cos (2π/24)t. Discuss the effect of each term of the equation on the solution.

- 33. Drug injection. Find and solve the model for drug injection into the bloodstream if, beginning at t = 0, a constant amount A g/min is injected and the drug is simultaneously removed at a rate proportional to the amount of the drug present at time t.

- 34. Epidemics. A model for the spread of contagious diseases is obtained by assuming that the rate of spread is proportional to the number of contacts between infected and noninfected persons, who are assumed to move freely among each other. Set up the model. Find the equilibrium solutions and indicate their stability or instability. Solve the ODE. Find the limit of the proportion of infected persons as t → ∞ and explain what it means.

- 35. Lake Erie. Lake Erie has a water volume of about 450 km3 and a flow rate (in and out) of about 175 km2 per year. If at some instant the lake has pollution concentration p = 0.04%, how long, approximately, will it take to decrease it to p/2, assuming that the inflow is much cleaner, say, it has pollution concentration p/4, and the mixture is uniform (an assumption that is only imperfectly true)? First guess.

- 36. Harvesting renewable resources. Fishing. Suppose that the population y(t) of a certain kind of fish is given by the logistic equation (11), and fish are caught at a rate Hy proportional to y. Solve this so-called Schaefer model. Find the equilibrium solutions y1 and y2 (> 0) when H < A. The expression Y = Hy2 is called the equilibrium harvest or sustainable yield corresponding to H. Why?

- 37. Harvesting. In Prob. 36 find and graph the solution satisfying y(0) = 2 when (for simplicity) A = B = 1 and H = 0.2. What is the limit? What does it mean? What if there were no fishing?

- 38. Intermittent harvesting. In Prob. 36 assume that you fish for 3 years, then fishing is banned for the next 3 years. Thereafter you start again. And so on. This is called intermittent harvesting. Describe qualitatively how the population will develop if intermitting is continued periodically. Find and graph the solution for the first 9 years, assuming that A = B = 1, H = 0.2, and y(0) = 2.

- 39. Extinction vs. unlimited growth. If in a population y(t) the death rate is proportional to the population, and the birth rate is proportional to the chance encounters of meeting mates for reproduction, what will the model be? Without solving, find out what will eventually happen to a small initial population. To a large one. Then solve the model.

- 40. Air circulation. In a room containing 20,000 ft3 of air, 600 ft3 of fresh air flows in per minute, and the mixture (made practically uniform by circulating fans) is exhausted at a rate of 600 cubic feet per minute (cfm). What is the amount of fresh air y(t) at any time if y(0) = 0? After what time will 90% of the air be fresh?

1.6 Orthogonal Trajectories. Optional

An important type of problem in physics or geometry is to find a family of curves that intersects a given family of curves at right angles. The new curves are called orthogonal trajectories of the given curves (and conversely). Examples are curves of equal temperature (isotherms) and curves of heat flow, curves of equal altitude (contour lines) on a map and curves of steepest descent on that map, curves of equal potential (equipotential curves, curves of equal voltage—the ellipses in Fig. 24) and curves of electric force (the parabolas in Fig. 24).

Here the angle of intersection between two curves is defined to be the angle between the tangents of the curves at the intersection point. Orthogonal is another word for perpendicular.

In many cases orthogonal trajectories can be found using ODEs. In general, if we consider G(x, y, c) = 0 to be a given family of curves in the xy-plane, then each value of c gives a particular curve. Since c is one parameter, such a family is called a one-parameter family of curves.

In detail, let us explain this method by a family of ellipses

![]()

and illustrated in Fig. 24. We assume that this family of ellipses represents electric equipotential curves between the two black ellipses (equipotential surfaces between two elliptic cylinders in space, of which Fig. 24 shows a cross-section). We seek the orthogonal trajectories, the curves of electric force. Equation (1) is a one-parameter family with parameter c. Each value of c (> 0) corresponds to one of these ellipses.

Step 1. Find an ODE for which the given family is a general solution. Of course, this ODE must no longer contain the parameter c. Differentiating (1), we have x + 2yy′ = 0. Hence the ODE of the given curves is

Fig. 24. Electrostatic field between two ellipses (elliptic cylinders in space): Elliptic equipotential curves (equipotential surfaces) and orthogonal trajectories (parabolas)

Step 2. Find an ODE for the orthogonal trajectories ![]() . This ODE is

. This ODE is

with the same f as in (2). Why? Well, a given curve passing through a point (x0, y0) has slope f(x0, y0) at that point, by (2). The trajectory through (x0, y0) has slope −1/f(x0, y0) by (3). The product of these slopes is −1, as we see. From calculus it is known that this is the condition for orthogonality (perpendicularity) of two straight lines (the tangents at x0, y0)), hence of the curve and its orthogonal trajectory at (x0, y0).

Step 3. Solve (3) by separating variables, integrating, and taking exponents:

This is the family of orthogonal trajectories, the quadratic parabolas along which electrons or other charged particles (of very small mass) would move in the electric field between the black ellipses (elliptic cylinders).

1–3 FAMILIES OF CURVES

Represent the given family of curves in the form G(x, y; c) = 0 and sketch some of the curves.

- All ellipses with foci −3 and 3 on the x-axis.

- All circles with centers on the cubic parabola y = x3 and passing through the origin (0, 0).

- The catenaries obtained by translating the catenary y = cosh x in the direction of the straight line y = x.

4–10 ORTHOGONAL TRAJECTORIES (OTs)

Sketch or graph some of the given curves. Guess what their OTs may look like. Find these OTs.

- 4. y = x2 + c

- 5. y = cx

- 6. xy = c

- 7. y = c/x2

- 8.

- 9.

- 10. x2 + (y − c)2 = c2

11–16 APPLICATIONS, EXTENSIONS

- 11. Electric field. Let the electric equipotential lines (curves of constant potential) between two concentric cylinders with the z-axis in space be given by u(x, y) = x2 + y2 = c (these are circular cylinders in the xyz-space). Using the method in the text, find their orthogonal trajectories (the curves of electric force).

- 12. Electric field. The lines of electric force of two opposite charges of the same strength at (−1, 0) and (1, 0) are the circles through (−1, 0) and (1, 0). Show that these circles are given by x2 + (y − c)2 = 1 + c2. Show that the equipotential lines (which are orthogonal trajectories of those circles) are the circles given by

(dashed in Fig. 25).

(dashed in Fig. 25).

- 13. Temperature field. Let the isotherms (curves of constant temperature) in a body in the upper half-plane y > 0 be given by 4x2 + 9y2 = c. Find the orthogonal trajectories (the curves along which heat will flow in regions filled with heat-conducting material and free of heat sources or heat sinks).

- 14. Conic sections. Find the conditions under which the orthogonal trajectories of families of ellipses x2/a2 + y2/b2 = c are again conic sections. Illustrate your result graphically by sketches or by using your CAS. What happens if a → 0? If b → 0?

- 15. Cauchy–Riemann equations. Show that for a family u(x, y) = c = const the orthogonal trajectories ν(x, y) = c* = const can be obtained from the following Cauchy–Riemann equations (which are basic in complex analysis in Chap. 13) and use them to find the orthogonal trajectories of ex sin y = const. (Here, subscripts denote partial derivatives.)

- 16. Congruent OTs. If y′ = f(x) with f independent of y, show that the curves of the corresponding family are congruent, and so are their OTs.

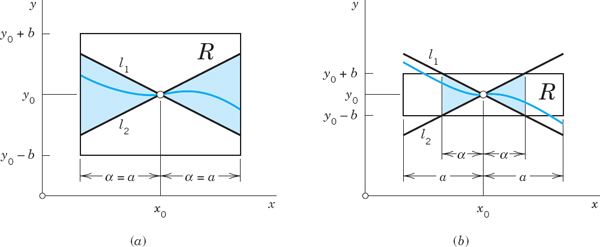

1.7 Existence and Uniqueness of Solutions for Initial Value Problems

The initial value problem

![]()

has no solution because y = 0 (that is, y(x) = 0 for all x) is the only solution of the ODE. The initial value problem

![]()

has precisely one solution, namely, y = x2 + 1. The initial value problem

![]()

has infinitely many solutions, namely, y = 1 + cx, where c is an arbitrary constant because y(0) = 1 for all c.

From these examples we see that an initial value problem

may have no solution, precisely one solution, or more than one solution. This fact leads to the following two fundamental questions.

Problem of Existence

Under what conditions does an initial value problem of the form (1) have at least one solution (hence one or several solutions)?

Problem of Uniqueness

Under what conditions does that problem have at most one solution (hence excluding the case that is has more than one solution)?

Theorems that state such conditions are called existence theorems and uniqueness theorems, respectively.

Of course, for our simple examples, we need no theorems because we can solve these examples by inspection; however, for complicated ODEs such theorems may be of considerable practical importance. Even when you are sure that your physical or other system behaves uniquely, occasionally your model may be oversimplified and may not give a faithful picture of reality.

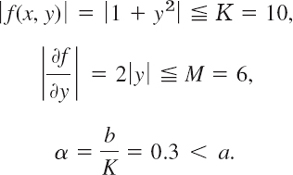

Let the right side f(x, y) of the ODE in the initial value problem

![]()

be continuous at all points (x, y) in some rectangle

![]()