Chapter 17. Financial Control

Pre-planning is the essence of good financial management. The financial problems experienced by many retail companies highlight the need for a thorough understanding of the financial implications of retail decisions.

The major objectives of financial management are:

• To obtain funds for business uses

• To maintain and increase the invested capital

• To generate income

Financing the Initial Operation

When planning to open a shop, you must consider the necessity of having sufficient funds (that is, start-up costs) for the following:

• Pay for professional advice if needed

• Pay for legal fees

• Pay rent in advance

• Pay renovation cost

• Purchase fixtures and equipment

• Buy merchandise for resale

• Purchase signs and display materials

• Install a telephone and other utilities

• Buy office supplies

• Promote the shops for opening (for example, advertising, sales promotion)

• Buy business insurance

• Pay for licence, permits and miscellaneous fees

To run a successful business, you must have working capital, that is, enough funds to permit the timely payment of required business expenses, from the day the business starts. The start of the business may have already depleted the majority of your cash resources. Thus you have to begin with enough cash to honour the terms of all investments, pay for expenses and still maintain an adequate cash balance.

To operate comfortably and without financial pressure, it is important to conduct a thorough research of all cost factors and standard operating ratios, and to prepare a financial worksheet to outline the start-up costs and the operating expenses for at least the first three months. Some operating expenses include the following:

• Owner’s salary

• Salaries and commissions

• Rent

• Utilities

• Inventory

• Maintenance and supplies

• Repayment of loan

• Interest

• Accounts receivable

• Advertising and promotions

• Petty cash

Budgetary Control

A budget is a plan that estimates future sales, expenses or some other financial aspects of a company over a specific period of one, three or six months. These estimates are based on past experience, present economic conditions and future plans. The actual figures are then compared with the estimates to determine how well specific areas are staying within the estimates. Many well-managed shops use budgets to plan, evaluate and control retail operations.

Generally, there are three main types of budgets that are interrelated:

1. The operating budget which consists of the sales budget, merchandise budget and the expense budget

2. The cash budget

3. The capital budget

The Sales Budget

One of the key items in the merchandise and cash budget is the sales forecast. This is true because

an overestimation or underestimation of sales has a serious effect on merchandising decisions as well as cash flow.

A typical retailer develops forecasts on the basis of the following:

• Experience and knowledge of the field

• Input from suppliers and sales staff

• Past sales reports, paying special attention to factors such as comparability (for example, exceptional events that occurred in the previous year but not the current year) and environmental changes (for example, changes in consumers’ taste of a product, recession and high unemployment)

The Merchandise Budget

Merchandise must be stocked to accommodate sales patterns. It is difficult to operate at a constant retail inventory level. Facing seasonal variations, you need to plan in advance to ensure a constant and adequate flow of merchandise to generate income.

The use of the stock-sales ratio can also help to estimate the amount of inventory needed to maintain that sales level. For example, if you estimate sales for the month to be S$20,000, and if you know from past experience that you need three times the sales volume to be in inventory, then you know that you will need S$60,000 in inventory to achieve the planned sales and still have sufficient opening inventory for the next month.

The Expense Budget

All the expenses (refer to the section on Financing the Initial Operation for examples of operating expenses) expected during the planning period, especially those that are incurred in generating the forecasted sales, should be included in this budget.

Expenses can be classified into fixed or variable expenses:

• Fixed expenses are those that do not vary with the volume of the business, such as insurance, property tax and depreciation.

• Variable expenses vary in direct proportion to the business volume, and they can therefore be controlled on a short-term basis. Such expenses include sales commissions, advertising, travel expenses and delivery expenses.

The Cash Budget

Continuous projection of an accurate cash flow (or a cash budget) will enable many small businesses to increase their operational performance and ensure sufficient funds for buying merchandise, paying for all operating expenses and for future growth. Such projection helps to predict when cash will come into the company and when payments of cash will have to be made, as well as the quantities coming in and going out.

Cash receipts are determined from forecasts of cash sales, accounts receivable collection and other sources of business income. Cash payments are based on anticipated operating expenses.

The Capital Budget

To ensure sufficient funds for future growth (for example, renovating the shop when needed, opening new outlets and replacement of or addition to existing assets), capital budgeting is necessary.

Evaluation of Merchandise Effort

Merchandising efficiency is measured by:

• Sales and markdowns

• Inventory and stock turnover

• Stock shortages

• Gross margin

Sales

Profit is the surplus after deducting the cost of goods sold and expenses from the sales revenue. However, greater sales do not necessarily lead to greater profit. Here are two examples:

1. If the economy is experiencing an inflation rate of 10 percent and your sales increase is only 5 percent, this indicates that the additional sales volume cannot keep pace with inflation.

2. If the sales record shows a 20 percent increase in dollar sales but a 15 percent decrease in units sold, this indicates that the merchandise is being sold at a higher price with fewer customers buying. If you have no intention to sell goods at a higher price at the expense of the number of units sold, you should analyse the cost and selling price of the merchandise carefully.

These examples show that you need to carefully analyse your sales figures to ensure that they are truly profit-producing.

Profit is essential for the survival of any business activity.

Markdowns

Generally, when sales figures are below those estimated, there will be excess merchandise. An effective way to speed up the sales of the merchandise or to dispose of merchandise that is unsaleable at its present price is to use markdowns.

An effective way to speed up the sales of merchandise is to use markdowns

Although markdowns eat into the profit, it is necessary to help the retailer get rid of outdated merchandise, create funds for purchasing new merchandise, foster customer goodwill or perhaps even to widen the base of potential customers.

The ratio of old stock to new stock is an important standard for measuring your inventory’s value and effectiveness.

It is important, however, to note that a shallow reduction is not an effective policy. Your first reduction should be the best one to ensure immediate sales increase.

Inventory

A major key to profitability is inventory control. It is important to know the amount of stock on hand at any point in time in order to make better merchandising decisions. Inventory control may be carried out periodically or on a continuous (perpetual) basis either in dollars or in units.

Periodic inventory is one method of keeping track of inventory by counting the stock on hand once, twice or more times per year on a specific date. However, this method is costly and can be time-consuming.

Perpetual inventory provides up-to-date information by monitoring merchandise movement into and out of the shop at any given time. Due to the cost and complexity, perpetual inventory control is better suited to high-ticket merchandise such as electrical appliances than to low-priced merchandise such as food. However, the use of POS equipment, as discussed in Chapter 15, can enhance such a method of inventory control.

For ease of planning, analysis and stocktaking, retailers generally maintain inventory records at retail prices and then convert the figure to its cost equivalent (where necessary).

Stock Turnover

Having too much inventory may lead to excessive markdowns if all the merchandise cannot be sold. It can also increase holding, storage and insurance costs. Having too little inventory may lead to lost sales because merchandise is not in stock when customers ask for the goods.

One way to measure whether there is too little or too much money invested in inventory is to calculate the number of times stock turns over in a given period. Stock turnover is a measure of how fast merchandise is sold and replaced. It indicates the number of times an average inventory is sold during the year.

A good turnover is a result of good merchandising management.

Stock turnover is also used to measure the retailer’s ability to meet its cash obligations.

To derive the number of stock turns obtained in a given period, just divide the net sales of the period by the average inventory for that period. For example, if the net sales for the year is S$120,000 and the average inventory is S$20,000:

Turnover rate = S$120,000 ÷ S$20,000 = 6

This figure indicates that the average amount of merchandise on hand turns over (is sold) six times a year or once every two months (12 months ÷ 6).

Whether a stock turnover of six is good or bad depends on the type of retail business. In some retail businesses, such as supermarkets, turnover rates can be very high. This is because supermarket sales are more rapid and frequent replenishment is required. Thus supermarket retailers do not need to keep too much inventory on hand.

Others, such as apparel stores, may operate at very low turnover rates. This is because the system for manufacturing and distributing apparel requires retailers to order in bulk and therefore, it is necessary to carry backup stock and backup stock tends to slow down the rate of stock turnover. Shops that carry high-priced merchandise, such as jewellery, generally show low turnover rates too.

Retailers should compare their turnover rates for previous periods to detect the relative frequency of sales activity. A significant change in a rate may call for an analysis of sales and inventory operations.

A fast stock turnover ensures better use of capital and shop space, as well as reduces outdated merchandise and insurance costs. There are several ways to increase stock turnover:

• Carry minimum slow-moving merchandise or do not sell them at all

• Reduce the number of lines carried and concentrate on key merchandise

• Negotiate with suppliers to speed up deliveries of merchandise ordered

• Reduce prices

• Increase sales promotions

However, the above suggestions must be carried out with care as lowering prices may affect profitability, increasing promotions may increase expenses, and reducing inventory may lose customers and quantity discounts.

Stock Shortages

Stock shortage is the difference between the book value and the dollar value of a physical count. Stock shortages are unavoidable and will reduce gross margin. The retailer should attempt to minimise this loss of stock by recognising the reasons why they occur and by taking measures to prevent them. Shortages can be due to clerical errors, errors in selling, theft, errors in stock count or poor housekeeping.

Gross Margin

Gross margin or gross profit is the difference between net sales and the cost of goods sold. It is the initial level of profit (before deducting operating expenses) and must be sufficiently high to cover the operating expenses. Thus in making commitments to purchase merchandise, the retailer must always consider the mark-ups (or selling price) of the merchandise.

Both mark-ups and markdowns have an immediate effect on the gross margin.

Care must be taken in pricing merchandise for resale so that excessive markdowns can be avoided subsequently.

To improve the gross margin, the retailer can consider the following:

• Selling exclusive merchandise to enhance sales and discourage price comparison by customers

• Selling more of the higher-margin merchandise through advertising, better display and incentives to sales personnel

• Reducing frequent markdowns or discounts

• Reducing merchandise shortages

Evaluation of the Retail Performance

The basic tools of financial analysis are the balance sheet and the income statement of the company. These two statements summarise the company’s activities in terms of financial impact.

Balance Sheet

A balance sheet contains a list of assets, liabilities and owner’s equity. Assets and liabilities are further categorised as current or long-term. The balance sheet reflects the operating efficiency of the business by showing whether the company has over- or under-committed in asset holdings or is heavily in debt. Several measurements based on the balance sheet figures are useful to the retailer.

1. The current ratio indicates the retailer’s ability to meet current debts with current assets.

Current Ratio = Current Assets ÷ Current Liabilities

For example, a ratio of 2:1 means that there is S$2 of current assets available to pay every S$1 of current liabilities. A current ratio of 2:1 is usually considered satisfactory.

2. The quick ratio measures the retailer’s ability to meet current debts with assets that can be converted into cash immediately. This ratio is used instead of the current ratio when the inventory forms a large part of the current assets.

Quick Ratio = (Cash + Receivables) ÷ Current Liabilities

For example, a ratio of 1.5:1 means that there is S$1.50 of current assets available to pay every S$1 of current liabilities. A quick ratio of above 1 is usually considered favourable in securing loans from banks or financial institutions.

3. The debt-to-equity ratio measures the retailer’s ability to meet all debts.

Debt-to-Equity Ratio = Total Liabilities ÷ Owner’s Equity

The higher the ratio, the more difficult it is for the company to meet its debt. A ratio of below 1 is usually considered excellent.

Income Statement (Profit and Loss Statement)

An income statement consists of three sections:

1. Income from sales

2. Cost of goods sold

3. Operating expenses

The final amount at the end of the statement indicates whether the company has made a net profit or sustained a net loss over a specific period.

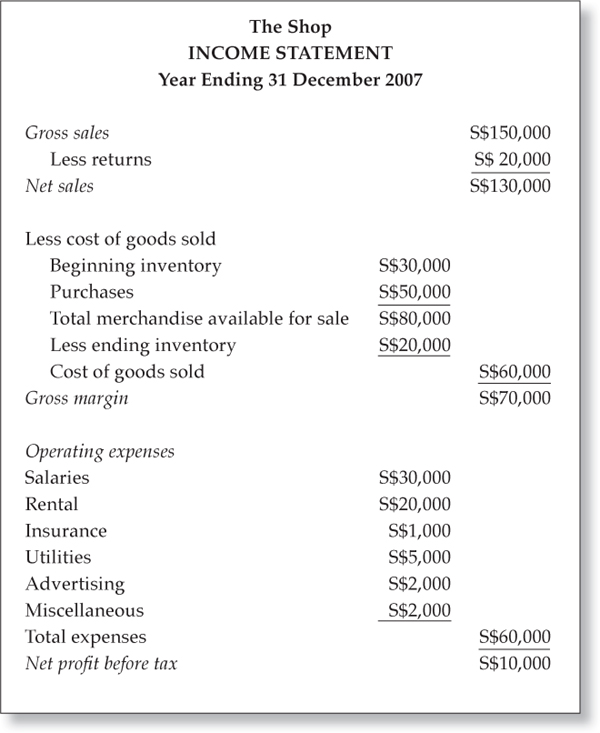

An example of an income statement is shown below. The income statement reflects the status of a company’s health in terms of whether it is making sales, and equally important, whether it is making any profit on the sales. For example, it can reveal information such as a shop with a favourable gross margin but poor profits due to a lack of expense control.

EXAMPLE

This gross margin is very good. Gross margin on sales indicates the percentage of gross margin on every sales dollar. Typical gross margin rates in the retail industry can range from 20 percent to as much as 60 percent.

A careful analysis of the income statement shows that there are a few ways to improve a shop’s profit performance.

• Increase sales but make sure that there is no proportionate increase in the cost of goods sold or operating expenses

• Decrease cost of goods sold but make sure that there is no proportionate decrease in sales or proportionate increase in operating expenses

• Decrease operating expenses but make sure that there is no proportionate decrease in sales or proportionate increase in cost of goods sold

As can be seen from above, a retailer may have to do more than simply increase sales to improve the retail performance.

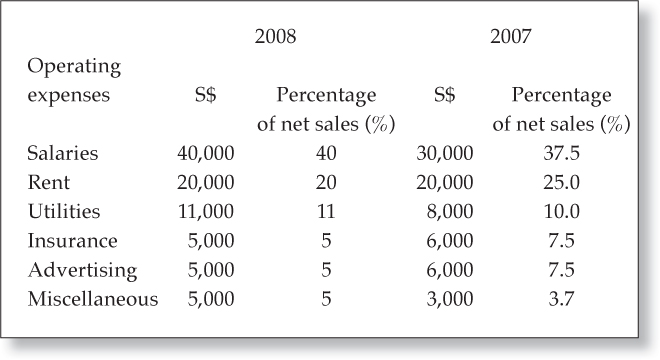

Retailers must analyse expenses in terms of their increases or decreases from one period to another frequently.

Percentages are a more realistic indication of such changes than the absolute dollar value. Operating expenses may also be evaluated as a percentage of sales. This practice allows retailers to judge the effect of operating expenses on sales volume.

Here is an example for evaluating the operating expenses (assuming net sales for The Shop is S$100,000 for 2008 and S$80,000 for 2007):

Based on the above calculations, the retailer may ask the following questions:

By answering the above questions, the retailer can better control or manage the operating expenses.

A combination of the balance sheet and the income statement amounts will also provide the retailer with other useful retail performance measures.

• The return on investment (ROI) indicates the percentage earned on investment in the business.

ROI = Net Income ÷ Owner’s Equity

An ROI of 5 percent means that the retailer earned 5 percent on its investment in that year of calculation. Whether this figure is favourable or not depends on factors such as the outlook of the economy, the competitor’s ROI or the possibility that the retailer may earn a higher return from other investments.

• Sales per square foot indicate how effectively sales are generated from the shop space devoted to selling.

Sales Per Square Foot = Net Sales ÷ Square Foot of Selling Space

A sales per square foot of S$100 means that every square foot of selling space is contributing S$100 to the shop’s sales. The interpretation of this figure depends on factors such as past performance and the retail industry averages.

I need help...: How do I Increase my Profit?

• The future of retailing: Are you up to it?

• Are you sharpening your competitive edge, for example, if your dealership disappears today, would any of your customers really care?

• Market performance: Customer composition, profitability and market potential

• Product/category management: Sales, margin, inventory productivity

• Customer performance: Productivity and revenue opportunities

• Employee productivity: Processing sales, customer service

• Financial analysis: Ensure overheads are within estimates

• Sales and profits show a declining trend.

• Customer base is steadily ageing and visiting its outlets less frequently and spending less.

• Market is shrinking but competition is growing rapidly.

• Reconsider its market positioning

• Attempt to increase its operating margins by consolidating outlets and merchandise assortment, and controlling operating cost

• Seek to participate in a more profitable market segment

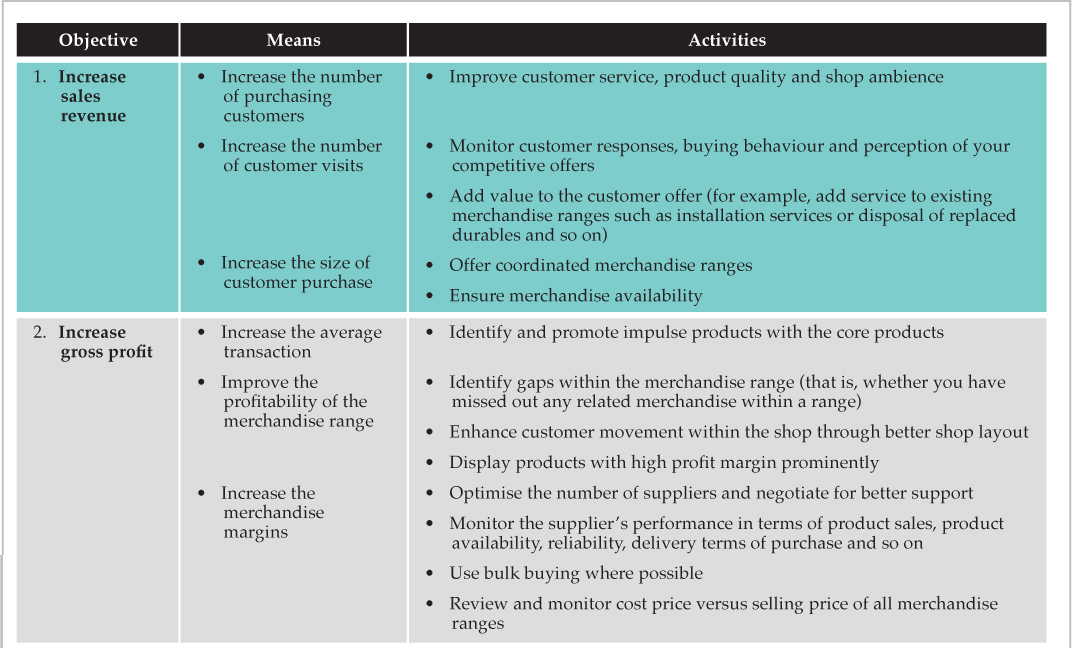

• To increase sales revenue

• To increase gross profit

• To reduce operating costs

• To increase the productivity of assets