Chapter 6. Cash Handling and Control

Retailers have to ensure that their cashiers are equipped with sufficient knowledge on handling sales transactions accurately and cash management efficiently on the sales floor. To help the cashiers, retailers have to introduce consistent procedures on the execution of transactions and cash handling. At the same time, these procedures also help the retailers to control and monitor their cashiers’ activities. Checklists for all the procedures are included at the end of this chapter.

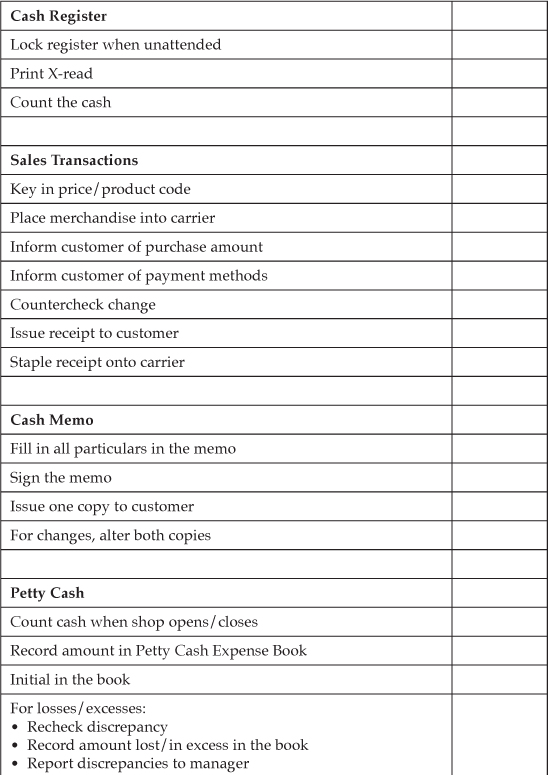

Cash Register

Operating Instructions

Please refer to:

• Chapter 4, Shop Opening Tasks on the opening of the Point-Of-Sale (POS) system and front-end procedures.

• Chapter 4, on Closing Procedures.

Cashier counter management

(courtesy of The Executive Home Store – XZQT)

Precautionary Measures

The cash register, when unattended, must always be in a locked position and the keys should be held by the cashier.

In cases where the cashier needs to leave the shop, the next person in line (for example, assistant cashier or supervisor) is to take over the transaction duties. Ensure that a cash count is done between both parties before the handover based on the X-read receipt from the cash register.

Payment Processing

Sales Transactions

1. Enter the price or product code into the register and place the items purchased into a carrier bag.

2. Inform the customer of the total amount due and ensure that every customer pays the correct amount.

3. Inform the customer or display a sign for the payment methods available in the shop.

4. If a customer pays by cash:

• Collect the money received from the customer and countercheck the change due before handing it to him. Remember to use both hands when returning change.

• Issue a receipt to the customer. The cashier may staple the receipt onto the carrier bag or hand the receipt together with the change to the customer.

5. If a customer pays by NETS:

• Request for the customer’s NETS card.

• Carry out the necessary steps to process the NETS payment.

• Hand the NETS receipt and the POS system receipt to the customer with both hands.

• The machine will automatically duplicate another NETS receipt for the shop’s record. File this copy.

6. If a customer pays by credit card:

• Request for the credit card.

• Carry out the steps to process the credit card payment.

• Hand the credit card invoice and the POS system receipt to the customer with both hands.

• Keep the other two sheets of credit card invoices for record purposes.

Steps to Prevent Credit Card Fraud

Small retailers may have to consider accepting credit card payment because cashless transaction is becoming popular. However, this may also give rise to more opportunities for fraud. The following measures can help retailers reduce and prevent credit card fraud.

1. Train the cashier to process credit card transactions.

• Ensure that the cashier is able to recognise and process all types of credit card transactions; for example, VISA card, Mastercard, Diners card and American Express card.

• Designate the supervisor or manager as the person to authorise transactions involving large amounts or attend to such transactions if the cashier is in doubt.

2. Teach the cashier to recognise fake cards. On the left of a genuine card, look out for the pre-printed four digits that appear either above or below the embossed account number. The pre-printed four digits should match the first four embossed digits of the account number. These numbers cannot be erased by scratching the surface of the card.

3. The cashier should always carry out the following procedures:

• Check the expiry date of the card.

• Request the customer to sign on the credit card invoice in the presence of the cashier.

• Check that the signature on the back of the card matches that on the invoice.

• If the card is not signed, request from the customer relevant identification, such as driver’s licence, passport or identification card. If the customer produces the identification, ask him to sign on the invoice and the card in front of you.

• If the cashier is unsure, seek assistance from the supervisor or manager.

• Look out for suspicious characters and actions.

Cash Memo Procedures

In the event of a power failure or at a customer’s request, a cash memo could be used.

Cash memo

1. Issue a cash memo by entering the particulars accordingly.

2. The cashier or the staff issuing the memo must write his name on the memo and initial it.

3. A copy of the cash memo is to be given to the customer. The duplicate copy is for the shop’s record and is needed for the counting and tallying of sales at the end of the day.

4. When the cash memo is altered, all copies of the memo should be altered at the same time and countersigned by the authorised personnel.

Cash Management

Petty Cash

1. Count the petty cash twice every day, when the shop opens and again at closing time.

2. After counting, record the exact amount and initial in the Petty Cash Expense Book.

3. If there are any losses or excesses:

• Re-check and verify the discrepancy.

• Upon verification, record the amount lost or in excess in the Petty Cash Expense Book.

• Report discrepancies to the person-in-charge.

4. Record petty cash expenditure in the Petty Cash Expense Book and submit the official receipts for purchases to the person-in-charge for authorisation. This can be done on a daily or weekly basis.

5. At the end of every month, the person-in-charge should:

• Close the petty cash account for the month.

• Record the list of expenses incurred in the Petty Cash Expense Book.

• Record the balance of petty cash on a new page for the next month.

• Reimburse the outstanding amount into the petty cash box.

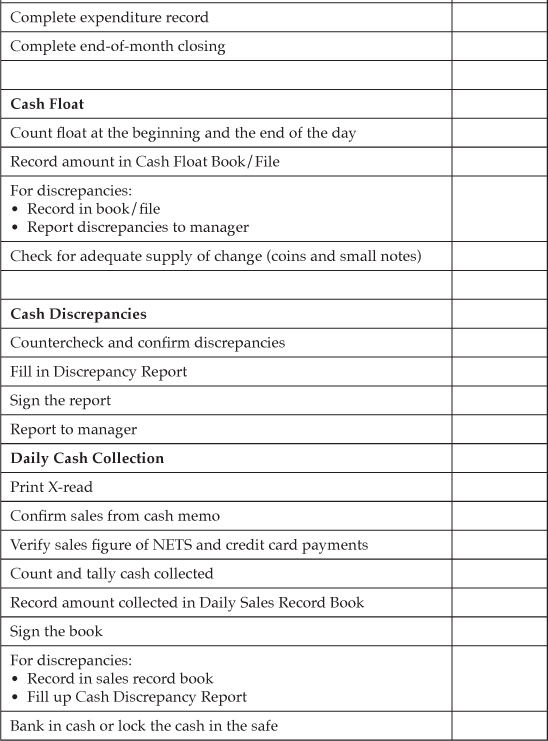

Cash Float

1. Count the cash float twice a day, when the shop opens and at the end of the day. When the cashier needs to be excused from the cashier counter while on duty, another authorised person is to take over. The cashier has to tally the float and sales with this person before he leaves.

2. Record the amount in the Cash Float Book/File and initial against the amount.

3. If there are discrepancies:

• Record the discrepancy in the Cash Float Book/File.

• Report the discrepancy to the person-in-charge immediately.

4. Ensure that there is always an adequate supply of small change for the whole day.

Cash Discrepancies

1. Various retailers may handle the accountability issue differently. This is sometimes dependent on the amount involved. Usually, the cashier will be responsible for it.

2. In the event of any cash discrepancies, the cashier must confirm these discrepancies by signing a Discrepancy Report.

3. The manager or supervisor should investigate the cause of the discrepancies.

The next page will show an example of a Discrepancy Report:

Daily Sales Collection

1. Designate an authorised person to do this task (it need not be the cashier).

2. Together with the cashier, count and tally the amount collected.

3. Verify the total sales figure from the various payment methods. Refer to Chapter 4, Closing Procedures, on closing of daily account.

4. Record the amount collected and sign in the Daily Sales Record Book, which is kept at the shop. The cashier should countersign in the book.

5. If there are any discrepancies, the cashier is to complete the Cash Discrepancy Report.

6. Bank in the sales on the next working day.

Cash Handling and Control Checklists

The following are samples of checklists for cash handling and control. Staff can check alongside the tasks that they have completed to ensure that all procedures have been carried out. Managers and supervisors can also use the checklist for training purposes.

Conclusion

Cashiers manage money in the shop. Hence, the measures discussed are essential to help them perform their tasks more effectively and efficiently.

There are no short-cuts!

I need help...: Can my Cashier Serve the Customer Better?

Do you train your cashiers adequately to perform these tasks?

What are your expectations of your cashiers?

Responsibilities of a Competent Cashier

• Able to use the POS system effortlessly

– Send the cashier for intensive training especially if you acquire a new system or when there are new additions or versions to the existing system.

– Customers frequently feel that a cashier who is familiar with the POS system tends to appear more professional.

• Able to communicate effectively with customers

– There are many types of information that customers require from the cashier, both related and unrelated to the store. Examples are product availability, price, sales promotion, locations of other stores and toilets, news on the shopping mall, and more.

– The cashier who can converse well with customers will be able to please the customers and enhance the image of the store.

• Processes transactions accurately and quickly

– No one likes to wait, and customers tend to walk away from crowds and queues. Hence, if a cashier is slow in his job, an exceptionally long queue at the checkout will be formed. Some customers may change their mind about the purchase.

– During peak hours and seasons, get an assistant cashier to assist at the checkout.

• Possesses adequate product knowledge

– Often customers who cannot find the sales staff will approach the cashier for product information.

• Knows the locations of merchandise

– Customers who are in a rush may most likely ask the cashier for the exact location of a particular product.

– Sometimes, customers bring an untagged product to the checkout and the cashier needs to know where to locate the product to facilitate scanning of the price ticket.

• Knows how to calculate

– The ability to calculate accurately is the basic mathematical skill that a cashier requires. It minimises mistakes.

Traits of a Good Cashier

• Honesty

– Cashiers handle petty cash, daily float, cash and credit transactions, vouchers, gifts and samples. Honesty is therefore of paramount importance.

• Keeping cool under stressful conditions

– Sometimes, complicated situations may arise. Being a member of the front-line staff, the cashier has to be patient and remain polite when dealing with difficult customers.

– Often customers go straight to the cashier to complain. The cashier may feel unjustified, especially if he may not be the one who sold the product to the customers. Thus the cashier must always maintain poise.

– Cashiers need to be humble and be willing to apologise to customers when necessary.

• Always smile

– Before customers leave the shop, smile at them. Remember that the cashier forms the last impression on customers.

These are not the only tasks and traits. However, they are sufficient to get the retailers thinking. What should you do now? You can help your cashier make a difference. Assess your cashier’s strengths and weaknesses, and provide relevant training to increase his productivity.

Remember that the checkout is a profit centre,

a place where products are translated into cash. Your cashier’s performance has an impact on customer perception of your store’s service, and ultimately, on the store’s profitability.