Supply and Demand of Global Energy and Electricity

Abstract

The implementation of the two-replacement policy towards clean energy and electric power will trigger significant changes to the structure of global energy supply and demand, resulting in clean production, globalized allocation, and electricity-driven consumption. It is important to adapt to this new trend of energy development, with the objective of ensuring gross energy supply, readjusting the energy mix, and protecting the ecological environment. Based on an understanding of the basic factors that influence the supply and demand of energy, we should conduct research into and accurately evaluate global energy demand, together with a comprehensive study of the global situation of energy development and electricity flows. These efforts should provide an important foundation for the building of global energy interconnections in a scientific manner.

Keywords

global energy interconnection

energy demand

electricity demand

energy development structure

electricity flow

1. Major Factors

Nowadays, energy development is closely associated and aligned with socioeconomic development. It determines the close link that energy supply and demand has with economy, society, the environment and resources. Generally speaking, socioeconomic development, energy resource endowment, energy environment constraints, technological progress, and energy policy regulation are the five major factors that influence energy supply and demand (See Fig. 4.1). In particular, socioeconomic development, including economic and population growth, industrialization, and urbanization, determines the growth trend of gross energy demand and regional distribution. The reserves and distribution of energy resources determine the supply potential, structure, and distribution of energy. Energy and environmental constraints restrict the overall level, structure and way of mankind’s utilization of energy resources to meet energy demand. As the Earth’s ecological environment deteriorates, its impact on energy consumption, supply structure, and structural readjustment has become increasingly prominent. Energy technological advancement and energy policy regulation mirror the combined effect of science and technology and government regulation on economy, energy, and the environment. Energy technological progress is a major decisive factor in directly determining the efficiency of energy production and consumption as well as environmental emissions. Energy-related policy and regulation play a role in guiding and regulating socioeconomic development, energy resource supply, and energy consumer behavior.

Figure 4.1Schematic Diagram of Factors Influencing Energy Supply and Demand

In-depth analysis and comprehensive assessment of the previous factors will have important implications for learning the development trend of global energy, studying and evaluating the mode of global energy development in a scientific manner, and formulating in the right way a roadmap for energy development.

1.1. Socioeconomic Development

Energy demand reflects the ups and downs of economic development. Looking ahead, development will remain the major theme and global energy demand will continue to rise, despite the crippling impact of the financial crisis on the world economy. In developing countries (regions) in particular, fast-growing populations and accelerated economic expansion will bring about catch-up growth in energy demand and the energy consumption gaps between different regions will narrow.

Energy demand will continue to grow on the back of relatively fast socioeconomic development. It is driven by the requirement to satisfy mankind’s production and living needs. With continued improvements in economic development and quality of life, demand for energy will continue to soar for a long while, especially in underdeveloped countries and regions where most of the populations suffering from energy poverty will gradually live a modern life enriched by the supply of power as a commodity. We are of the view that by the mid-twenty-first century, the gross capacity of the world economy will maintain, albeit at a slower rate, the rising trend that started at the end of World War II. It is projected that before 2030, the world economy will grow more strongly, but energy-intensive enterprises in the steel and iron, nonferrous metals, building materials, and chemical engineering industries will experience slower growth. The production of key products will reach the saturation point in 2030 or thereabouts, with energy demand maintaining an average growth rate of 1.6%. After 2030, energy-intensive industries will see themselves degenerating into “sunset industries,” with the industrialization and urbanization processes drawing to an end in most regions. By contrast, the weighting of other industrial, transportation and commercial sectors in the economy will rise further, amid an overall slowdown in energy demand growth.

A more balanced development of the global economy will narrow the gap in energy demand per capita between different regions. Sluggish growth and poverty are the major reasons for the long years of war and social unrest in some locales of Asia, Africa, and South America. With the progress of the globalization process, the gaps between the underdeveloped regions of Asia, Africa, and South America and the developed regions of Europe, the Americas, and Oceania will be significantly narrowed in the future, with an improvement in the imbalanced development between north and south. By 2030, the role of Asia as the engine of world economic growth will be further strengthened. China will overtake the United States as the world’s largest economy; Africa and South America will occupy a more important position in the world economy. The developed countries in Europe, North America, and Oceania will continue to lead the world in technology, finance, and education, but economic growth will be relatively lower due to the impact of population ageing, heavy government debts, and an excessively exuberant virtual economy. By 2050, the currently developing countries (regions) will rise to developed status following the completion of the industrialization process. The gross capacity of emerging economies will account for over 50% of the world economy by then. The gap in energy demand per capita between different regions will close gradually along with the narrowing differences in economic development. Energy consumption per capita in the underdeveloped regions of Asia, Africa, and South America will increase substantially.

The marked difference in population growth will produce a greater impact on energy demand. According to United Nations projections, under the scenario of medium fertility rates, the world population will continue to increase, albeit at a steadily lower rate. The world population is forecast to reach 9.55 billion by 2050. The difference in population growth will become increasingly obvious among different regions, with the African population growing fastest, followed by the Oceanian population; the Asian and South American populations will fall sharply from a high level; the North American population will maintain a low and steady rate of growth while the European region will see negative population growth. In the mid-twenty-first century, along with a slowdown in economic and population growth, energy demand in developed countries will only post marginal growth in the long term. By contrast, the rapid economic expansion, rising populations and faster urbanization among developing and emerging markets will continue to drive global energy consumption higher.

Global economic policy is shifting in the direction of globalization, balance, and low-carbon development. Over the past 20 years, the global economy has exhibited a growing trend of “moving east,” with emerging economies like China, India, and Russia becoming the new drivers of global economic growth. This trend will remain intact and spread to underdeveloped countries and regions. Driven by a fundamental view of concerted and sustainable development on a global basis, all countries are working hard to create a new international economic order characterized by globalization, multipolarization, and mutual coordination, guided by the shared objective of combating global climate change and eliminating war and poverty. Moreover, the emerging low carbon economy is providing an important impetus to global economic growth in the future. In view of the global impact of carbon emissions, countries around the world are finding themselves competing and working with each other to promote global low-carbon development together.

1.2. Energy Resource Endowments

Judging by the supply of energy resources around the world, the long-term development and utilization of fossil energy has imposed rigid growth restrictions on fast-growing energy demand. In contrast, renewable energy sources are inexhaustible with great development potential. The development and utilization of energy resources is limited by regional resource endowments and affected by the economics of technology.

The supply of fossil energy is subject to rigid resource restrictions, with limited room for development and utilization in the future. Fossil energy sources like coal, oil, and natural gas supported the progress of human civilization and socioeconomic development for 200 years in the nineteenth and twentieth centuries. In spite of a steady year-on-year rise in proven reserves of global fossil energy thanks to fast-developing exploration technology, the reserves of global fossil energy remain limited. Unless mankind can stop relying on fossil fuels, this source of energy will eventually and inevitably be exhausted as a matter of reality and natural restriction.

The abundant renewable energy resources around the world will become the dominant energy source in the future. Given their abundance and thanks to the growing maturity of development and application technologies, hydropower, wind, and solar energy resources worldwide can meet energy development requirements. The global demand for energy in 2050 can be satisfied simply by developing just a fraction, at 0.05 percent (5/10,000), of the developable capacity of global wind and solar energy. Moreover, the Earth also possesses other abundant energy resources, like ocean, biomass, and geothermal energy. If these renewable energy resources can be developed on a large scale, the energy problems facing mankind will be fundamentally eradicated.

The imbalanced distribution of energy resources calls for efforts to coordinate energy allocation on a global basis. Regionally, remaining recoverable coal reserves are distributed mainly in Europe and Eurasia, Asia Pacific, and North America. Remaining recoverable, conventional oil reserves are concentrated in the Middle East, Central and South America, and North America. Remaining recoverable natural gas reserves are mainly located in the Middle East, Europe, and Eurasia. Given the abundance of hydropower resources available and a low degree of development and utilization, Asia, Africa, and South America will become the focus of hydropower development in the future. The world’s wind and solar energy resources are mostly concentrated near the Arctic and equatorial regions, making them ideal locations for development and construction of large energy bases. Historically, the uneven distribution of conventional energy sources has propelled the development of global fossil energy trade and traditional energy markets. The global development of electricity-oriented clean energy in the future will lead to the formation of global electricity trade and electricity markets and invoke new requirements on the global allocation of electric power.

1.3. Energy Environment Constraints

With the substantial growth of energy consumption, environmental issues arising from energy development and utilization are becoming increasingly prominent and commanding widespread attention. Global energy environment issues are reflected mainly in greenhouse gas emissions, environmental pollution and ecological damage caused by burning fossil fuels.

Global efforts to combat climate change have accelerated low-carbon development of energy. Putting a spotlight on the growing urgency of work on energy efficiency and emission control, global climate change has been driving the development and improvement of relevant energy technology, energy policy and global energy management systems. The massive emission and build-up of CO2 caused by fossil fuel combustion has increased the concentration of this pollutant gas in the atmosphere and further aggravated the greenhouse effect, resulting in abnormal climate events and global ecological imbalances. To avoid severe disaster and achieve the goal of limiting global temperature rise to no more than 2°C in this century from the temperature recorded before industrialization, the major developed countries and emerging market economies are expected to introduce mandatory measures to control emissions in the future. The global action to combat climate change will bring improvements, making global energy technology, energy policy and global energy management systems more comprehensive, in-depth, and synergistic.

Pollutant discharges caused by energy utilization are attracting growing attention. Long before the Industrial Revolution, firewood was the main source of energy for consumption. Basically this did not create environmental concerns at a time when consumption was limited and timber resources harvested could be replenished through revegetation, not to mention the fact carbon emissions from burning could be offset by the carbon fixation of the growing plants, and the smoke pollution caused by combustion was within an environmentally acceptable limit. The Industrial Revolution triggered rapid growth of energy consumption, making fossil fuels the dominant energy source, with a tremendous impact on the environment. For example, China now faces the severe challenge of compound air pollution caused by soot and vehicle exhaust emissions. With the growing prominence of environmental problems and the ever-higher demand for environmental quality, more importance is being attached to the pollutant discharges from fossil fuel burning as a restrictive factor for energy development.

The current development and utilization of energy resources is ecologically and environmentally unsustainable. Energy development and utilization focusing on fossil energy has brought about increasingly conspicuous damage to the ecological environment. For instance, land subsidence and water contamination caused by coal mining as well as the serious heavy acid rain caused by particulate, sulfur dioxide, and nitrogen oxide emissions in the coal burning process have led to soil acidification, forest deterioration, and other ecological damage. The current over-reliance on fossil fuels for energy development and utilization is unsustainable, which demands the completion an energy transition as soon as practicable in order to reduce destructive exploitation and promote clean energy development.

1.4. Advancement of Energy Technology

By taking advantage of better energy technology to improve demand-side energy efficiency, we can reduce energy supply. By enhancing supply-side capacity while lowering the cost of energy supply, we can significantly alleviate the environmental impact of energy development and utilization and also ease energy environment constraints.

Technological progress has led to improved energy efficiency and lower energy demand. Around the world, energy end-use and intermediate conversion efficiency have improved to various extents, thanks to technology process improvement, energy efficiency technology development, and energy management enhancement. For example, the world’s advanced-level aluminum electrolytic AC power consumption decreased from 14,400 kWh/ton in 1990 to 12,900 kWh/ton in 2012, whereas comprehensive energy consumption of ethylene also went down from 897 kg of standard coal/ton to 629 kg of standard coal/ton over the same period. Energy consumption in the construction and transport sectors has shown significant improvement along with growing technology development in motors, electronic information, materials, and energy gradient utilization. Thanks to the advanced gas turbine and coal-fired power generation technologies, such as extra supercritical coal-fired power generation, integrated gasification combined cycle power generation, and circulating fluidized bed, the efficiency of fossil-based power generation has improved exponentially. Improvement in energy development, energy conversion, and utilization efficiency has not only reduced the production of primary energy required to meet the same level of demand, but also provided conditions for restructuring the energy mix and mitigating energy and environmental problems.

Technological progress has enhanced energy supply capacity and lowered energy supply costs. The oil crisis of the 1970s triggered a far-reaching structural change in the world energy market, prompting global efforts to actively develop energy efficiency technology and seek alternative energy sources to ensure supply security. For example, along with the rapid development of exploration technology, the proven reserves of fossil energy around the world have increased from year to year. The successful development of horizontal well technology, multilayer fracturing technology, hydraulic fracturing technology, refracturing technology, and simultaneous fracturing technology has made the commercialized mass production of shale gas in North America possible. Technological advancements in nuclear energy utilization and renewable energy generation have led to ever-higher levels of clean energy utilization, steadily lowering costs, and growing capacity expansion. As a result of technological development, grid parity for photovoltaic energy generation will be reached in 2016–2017 in Europe and America. However, parity between on-grid photovoltaic power tariffs and residential sales tariffs in China is not expected to be reached until 2020, given the country’s relatively low power price benchmarks. In line with technological progress, generating costs based on the same type of power generation show a steadily downward trend, allowing the electricity industry to meet increasing power demand at increasingly competitive system costs.

Pollutant emissions are reduced and impact on energy and the environment mitigated through technological advancement. As a unique high-quality energy source, electric power is not only highly efficient (over 90% in general), but also pollution-free in consumption and conducive to high-precision control. It is also a good substitute for fossil energy at the end-use level. Amid the dwindling supply of fossil energy resources and the growing concerns about the contribution of fossil energy development and utilization to environmental pollution and climate change, application technologies for renewable energy, such as wind and solar energy, have become the focus of competition in the technologies for global primary energy development and the way forward in energy technology development around the world. With technological progress, the share of electric power in energy end-use and primary energy consumption can be improved and the structure of energy demand optimized to reduce the environmental impact brought about by energy development and utilization and alleviate energy and environmental constraint.

1.5. Energy Policy Regulation

Energy policy can be described as the regulator and controller of energy development, providing a guiding tool at the macro level and a management tool at the micro level to enable the private and public sectors to adjust the relationship between the energy system and the socioeconomic/environmental systems.

Energy policy drives innovation in energy technology. Progress and innovation in energy technology is an important pillar of energy development. Driven by a consensus on global sustainability, governments around the world hold in high regard the development of energy technology, as evidenced by the strong financial, policy and taxation support provided for the development of energy efficiency technology and clean energy technology. For instance, a US$150.7 billion investment plan for the years 2009–2014 was put forward in the United States Recovery and Reinvestment Act by the Obama Administration to provide direct investment, tax incentives, and loans or loan guarantees for clean energy technology. Of this funding amount, 74% is dedicated to promotion and application of clean technologies, 18% to the research and development and demonstration of clean technologies, and the remaining 8% to the provision of financial subsidies for clean technology manufacturers. In recent years, the Chinese government has been working vigorously on the research and development and promotion of energy technologies and creating conditions for energy technology development by improving the market mechanism, technical standards and policy environment.

Policy-guided energy production and utilization. Energy is an important physical foundation for socioeconomic development. With the fast expanding energy demand and the growing scarcity of resources over the past decades, meeting the energy demand arising from socioeconomic development has become the top priority of policy-based regulation. To achieve this goal, measures such as technological progress, market regulation, and system guidance have been taken to support the policy objectives of promoting energy development and ensuring a more adequate supply of energy, while encouraging energy conservation and efficiency and controlling rapid energy demand growth. For example, to improve energy conservation and rein in unreasonable energy demand, the Chinese government has proposed a target of approximately 4.8 billion tons of standard coal for total primary energy consumption and of approximately 4.2 billion tons of standard coal for total coal consumption by 2020 so as to strengthen control of the coal-dominated energy mix. In addition, plans have been proposed to vigorously develop renewables as well as clean energy like nuclear energy and natural gas, with the share of nonfossil energy in primary energy consumption set at 15% and 20% by 2020 and 2030, respectively, to improve the level of substituting clean energy for fossil energy.

Energy policy supports energy and environmental improvements. For a long time, the continued growth of fossil energy consumption has been responsible for environmental issues like ecological damage, environmental pollution, and global climate change. Against this background, the resolution of these energy and environmental problems has figured more prominently in policy terms in some countries. For instance, environmental standards governing energy utilization have been developed, covering coal consumption and pollutant discharges at thermal power plants, environmental well-being and energy efficiency, vehicle exhaust emissions, and the economics of fuels. Intensive efforts have also been exerted to promote the application of environmental management technologies, covering clean energy, high-efficiency power generation, and high-efficiency desulfurization and denitrification.

2. Energy Demand

Energy supply and demand is affected by various factors, such as socioeconomic development, energy resource supply, environmental constraints, technological progress, and regulatory policy. This reality gives rise to great uncertainties surrounding the future development of energy. Among the many probable scenarios of global energy and power demand growth, we focus particularly on the impact of shared global prosperity and an active response to climate change on the future demand for energy and electricity. In terms of socioeconomic development, the global economy is expected to maintain relatively steady growth between 2010 and 2050, with annual growth of approximately 3%,1 and the world’s population will continue to grow from 6.92 billion to 9.55 billion2 in the same period. In response to the restrictions caused by climate change, a global consensus has been reached with aggressive efforts to attain the achievable target of limiting global temperature rise to 2°C. This is expected to lower global carbon emissions from energy consumption by 40–70% to within 12 billion tons3 by 2050, representing a dramatic 50% reduction from 1990 levels and nothing short of a revolutionary challenge to the way of global energy development in the future.

Taking an integrated view of energy demand and environmental constraints, among other factors, an energy system analysis model of “end-use energy demand – energy processing and conversion – demand for primary energy” is adopted for analyzing scenarios of global demand for energy and electricity. The general idea is to project the end-use demand for different types of energy (e.g., coal, oil, natural gas, electricity, and heat) based on the levels of economic activity and historical energy consumption among different energy end-use sectors, while also taking into account trends of fossil energy consumption, electric energy substitution, and carbon constraints. Based on the end-use demand so projected, an integrated view is then taken of the conversion efficiency of different energy segments, including raw coal-fired generation, heating, coking, crude oil refining, power generation, natural gas-fired generation, liquefication, and nonfossil fuel–based power generation and heating, as well as the availability and technology economics of different resources for power generation. This will form the base for projecting the demand for primary energy resources such as coal, oil, natural gas, and nonfossil energy. See Fig. 4.2 for the reasoning behind the global energy and electricity analysis model.

Figure 4.2Global Energy Electricity Model Idea

Based on the previously mentioned reasoning, a scenario analysis of global demand for energy and electricity is performed for the target years of 2020, 2030, 2040, and 2050 in order to forecast the total volume, structure and distribution of global primary energy demand as well as the total volume and distribution of electricity demand in the future. The analysis provides fundamental support for global energy development and the building of a globally interconnected energy network.

2.1. Total Energy Demand

Primary energy demand worldwide is expected to continue growing, albeit at a steadily lower rate. In 2013, global GDP totaled US$74 trillion; with a global population of approximately 7.2 billion, and total primary energy demand of approximately 19.5 billion tons of standard coal.4 With the steady economic and population growth worldwide and continued improvements in energy efficiency, global GDP is expected to reach US$220 trillion and the global population to increase to around 9.55 billion by 2050. We have adopted here a model of “end-use energy demand – energy processing and conversion – primary energy demand” by taking into full account global socioeconomic development, energy supply, energy environment constraints, energy technological progress, and regulatory energy policy. Based on a scenario of quickening clean energy development, global primary energy demand is expected to increase to 30 billion tons of standard coal (see Fig. 4.3) by 2050, which is in line with the scenario proposed in the World Energy Council’s World Energy Scenarios: composing energy futures to 2050. Under this scenario, global energy consumption is expected to grow 1.2% on a yearly basis in 2010–2050, representing an increase of 11.2 billion tons, or the aggregate energy consumption of China, the United States and the European Union combined in 2010. Global energy consumption per capita will grow by around 15% from 2.7 tons of standard coal to 3.1 tons of standard coal, or 46% of the coal consumption per capita of 6.7 tons of standard coal among OECD nations in 2000. This level of per capita consumption is necessary to support the economic growth of developing countries. At the same time, the progress of energy technologies will contribute to a 50% reduction in energy consumption per unit of GDP from 2.7 tons/US$10,000 to 1.4 tons/US$10,000, indicating a significant improvement in the efficiency of energy utilization.

Figure 4.3Total Volume and Growth Rate of Global Primary Energy Demand

In the future, the elasticity coefficient of energy consumption is expected to fall steadily, with faster economic growth being supported by relatively low energy growth. Between 1990 and 2000, average annual global economic growth stood at 2.8%, compared with an average annual growth of 1.4% in global energy consumption, indicating an elasticity coefficient of energy consumption at about 0.5. Between 2000 and 2010, average annual global economic growth was estimated at 2.7%, compared with an average annual growth of 2.4% in energy consumption. The elasticity coefficient of energy consumption climbed to 0.9 as a result of the growing energy consumption in non-OECD countries. As regards future energy development, average annual global economic growth is expected to be about 3.0% between 2010 and 2050, compared with energy demand growth of about 1.2%, indicating an elasticity coefficient of energy consumption at about 0.4. On a phased basis, between 2010 and 2020, average annual global economic growth is estimated at about 3.0% and annual energy demand growth at about 2.0%, indicating an elasticity coefficient of energy consumption at about 0.6. Between 2020 and 2030, average annual global economic growth is expected to rebound to 3.2%, fuelled by the growing emerging economies, and the quickening pace of promoting and applying green energy technology (like the industrial internet, smart buildings, and transport electrification) in the industrial, construction, transport, and other major energy-consuming sectors, is expected to drive global energy demand growth down to 1.4% and the elasticity coefficient of energy consumption down to 0.4. With a slowdown in global economic growth, average annual global economic growth is expected drop to 3.0% in 2030–2040, while average annual energy demand growth will decline to 0.9% and the elasticity coefficient of energy consumption will be about 0.3. With more intensified global efforts in energy efficiency and GHG emission control, average annual world economic growth is expected to fall to 2.8% in 2040–2050, with average annual energy demand growth easing to 0.5%, indicating an elasticity coefficient of energy consumption of approximately 0.2.

The afore-mentioned are projections of world energy consumption growth based on a historical view of global energy development and scenarios of faster clean energy development. But objectively there are uncertainties, as total primary energy demand growth is inextricably linked with global economic growth, changing industry structures, urbanization, population growth, and energy policy. In the event of a slowdown in global economic and population growth, or significant breakthroughs in energy efficiency technology, global primary energy demand may reach approximately 23 billion tons of standard coal by 2030, to rise to 25–27 billion tons in 2050.

2.2. Energy Demand Structure

The continued optimization of the primary energy demand structure will result in a fundamental shift of focus from an energy system dominated by fossil fuels and supplemented by clean energy, to one oriented towards clean energy and supplemented by fossil fuels. In 2013, coal, oil and natural gas accounted for 30.1%, 32.9%, and 23.7%, respectively, and nuclear energy, hydropower and nonhydropower renewable energy accounted for 4.4%, 6.7%, and 2.2%, respectively, of global energy consumption, with the share of fossil energy standing at 86.7%. Amid intensified global efforts in clean energy development, the development of favorable hydropower resources will be basically completed by 2030, with continued rapid growth in various nonhydropower energy resources. Two-thirds of new energy demand will be met by renewables, with over 50% of this new demand to be satisfied by nonhydropower renewable energy, such as wind and solar power. That said, coal, oil, natural gas, and other fossil energy sources will still account for two-thirds of total primary energy demand by 2030. After 2030, we will see more mature technology for development and utilization of wind, solar, and other renewable energy, with continued improvements in conversion efficiency and economics to expedite the substitution for fossil energy (especially coal and oil). Consumption of coal, oil, and natural gas will experience negative growth and all new demand for energy will be met by renewables. Based on a scenario of faster clean energy development, clean energy is expected to represent 80% of total energy supply by 2050, replacing fossil energy as the dominant energy source, while the share of fossil energy will drop to around 20%. See Fig. 4.4 for the global demand for different forms of primary energy between 2010 and 2050.

Figure 4.4Global Demand for Different Forms of Primary Energy, 2010–2050

The substitution of electricity for fossil energy, together with improved electrification, has become the dominant trend in the changes in the world’s end-use energy structure. With population expansion and improving quality of life, mankind’s demand for available energy5 will continue to grow. The efficiency of energy utilization will rise substantially, driven by the growing conversion of clean energy into electricity to gradually replace fossil energy in the end-use sector. Based on meeting equivalent level of demand for available energy, a higher share of electricity in the end-use energy structure will lead to lower energy demand at the end-use level. Higher demand for available energy and improved efficiency of end-use energy will cause end-use energy demand globally to peak around 2030. From 1980 to 2010, global end-use energy consumption increased by 1.6% on an annual basis. Average annual growth in 1980–1990, 1990–2000, and 2000–2010 was 1.6, 1.1, and 2.1%, respectively. Global end-use energy demand is expected to post average annual growth of 0.4% in 2010 to 2050. See Fig. 4.5 for the global end-use energy demand and global demand for available energy from 2010 to 2050.

Figure 4.5Global End-Use Energy Demand and Global Demand for Available Energy

Judging by the trend of end-user, energy utilization has been marked by a shift from a direct, low efficiency consumption model to an indirect, high-efficiency model, with demand for electricity continuing to grow. In 2010, electricity was responsible for 17.7% of global terminal energy consumption, 2.2 percentage points higher than that in 2000. Electricity consumption of OECD countries accounted for 21.9% of end-use energy consumption, and non-OECD countries accounted for 15.7%. It is expected that from 2010 to 2030, the substitution of electricity for coal will be carried out rapidly in the world’s industrial and construction sectors, electric vehicles will gradually be used for commercial application, railway electrification will grow rapidly, coal and oil will have a decreasing share in end-use energy consumption, and electricity will have an increasing share in the energy structure. By 2030, electric energy will have accounted for 25.0% of end-use energy consumption, 7 percentage points higher than that in 2010. See Fig. 4.6 for the world’s end-use energy consumption structure from 2010 to 2050.

Figure 4.6Structure of Global End-Use Energy Consumption, 2010–2050

Because the major emerging economies and developing countries in Asia, South America, and Africa will complete the industrialization process successfully after 2030, the electric furnace will gradually take the place of traditional converters and blast furnaces as the major iron smelting equipment. In other industries (including construction), renewables-generated electricity, and heat will be utilized on a larger scale. In transportation, electric vehicles will replace traditional petrol vehicles at a faster rate to such an extent that oil will be edged out of its current position as the dominant fuel in transportation. Under a scenario of the “two-replacement policy” gathering speed, electricity is expected to account for over half (52.2%) of end-use energy demand by 2050, or a doubling of its share in 2030.

Given the stringent carbon emission controls, the share of fossil energy in total energy consumption is expected to be limited to around 20% by 2050, with more than half of the coal consumed and around 45% of the natural gas consumed going into power generation. The remainder will be used mainly by certain segments of the industrial sector or for nonenergy purposes. By that time, oil-fired generation will basically be nonexistent, with oil used primarily for water transport, air transport, and nonenergy uses. Of all nonfossil energy sources, around 88% will be utilized in the form of electricity and the remaining in the form of heat.

The uncertainty of the energy demand structure is derived mainly from clean energy substitution on the supply side, and electricity substitution at the end-use level. If clean energy substitution and electricity substitution should proceed at a slower-than-expected speed due to technological, cost, policy and other reasons, fossil energy will still have accounted for one-quarter to one-third of the primary energy demand structure by 2050, and electricity will still accounted for less than 50% of end-use energy consumption.

2.3. Energy Demand Distribution

As Asia, South America, and Africa have moved into or completed the industrialization and urbanization processes, accompanied by relatively fast population growth, the share of these regions in global energy consumption is expected to increase quite strongly. By contrast, Europe and America will see a declining share, but nonetheless will remain the world’s most energy-intensive regions in terms of per capita consumption and total energy consumption. Traditionally, the developed nations of Europe and America have been the world’s largest energy consumers. But in recent years, Asia has also become one of the largest energy consumers, reflecting strong demand growth in China and India. In 2013, Asia, North America and Europe were responsible for 39.4, 21.9, and 23.0% of global primary energy consumption, respectively, and South America, Africa, and Oceania accounted collectively for 15.7% of the world’s primary energy consumption. In the future, with the progress of economic globalization and balanced development, Asia, Africa, and South America are expected to experience faster economic growth and account for a higher share of the world economy from 34% in 2010 to around 45% in 2030, rising further to over 50% by 2050. As the north–south divide narrows, underdeveloped regions will enjoy higher living standards and energy consumption. From 2010 to 2050, annual energy consumption per capita in Asia will increase from 1.9 tons of standard coal to 3.1 tons of standard coal, reaching the world average level; annual energy consumption per capita of Africa and South America will grow from 0.6 and 1.8 tons of standard coal to 1.7 and 3.0 tons of standard coal, respectively. Although the energy consumption per capita of North America, Europe and Oceania is notably higher than the world average, it is expected to show a downward trend after reaching its peak under the pressure to reduce greenhouse gas emissions in absolute terms. See Fig. 4.7 for the energy consumption per capita of the world and different continents between 1990 and 2050.

Figure 4.7Energy Consumption Per Capita in the World and Continents, 1990–2050

The rapid growth in energy consumption per capita and population size is expected to make Africa the fastest-growing region in terms of total energy consumption before 2050. Africa’s population will grow from 1.03 billion in 2010 to 2.39 billion in 2050, accounting for a higher share of the world population from 14.9% to 25.1% during this period. The continent’s share of global energy consumption will also rise from 3.0% in 2010 to 13.7% in 2050. Between 2010 and 2050, global energy demand is expected to grow by 11.2 billion tons of standard coal, with Asia, Africa, and South America contributing to the growth. Given their massive population base, these three regions will be able to further consolidate their position as the world’s largest energy consumers. These three regions are also expected to take up a 74.1% share of total global energy demand by 2050. Africa and South America will rise to a more prominent position as the world’s major energy consumers. See Fig. 4.8 for the share of primary energy in global energy consumption by continent between 2010 and 2050.

Figure 4.8The Share of Primary Energy in Global Consumption by Continents, 2010–2050

North America, Europe, and Oceania, regions of traditionally high energy consumption, are expected to experience slower growth in energy consumption, with a correspondingly lower share of world energy consumption to 11.7, 13.4, and 0.8%, respectively, by 2050, as a result of slower economic and population expansion and high energy efficiency. However, annual energy demand per capita in these regions will expectedly remain higher than the world average by 1.5, 0.8, and 0.4 times. See Table 4.1 for scenarios for energy demand by continent.

Table 4.1

Energy Demand Scenario Analysis by Continent

Region

Energy Demand (Billion Tons Standard Coal)

Share (%)

Growth Rate (%)

2010

2020

2030

2040

2050

2010

2050

2010–2050

Asia

7.7

10.4

12.5

14.2

15.8

41.1

52.6

1.8

Europe

4.8

5.0

5.1

4.9

4.0

25.6

13.4

−0.4

North America

4.4

4.6

4.6

4.4

3.5

23.4

11.7

−0.6

South America

1.1

1.4

1.8

2.1

2.3

5.8

7.8

1.9

Africa

0.6

1.0

1.6

2.6

4.1

3.0

13.7

5.0

Oceania

0.2

0.2

0.3

0.3

0.3

1.1

0.8

0.0

World

18.8

22.6

25.9

28.5

30.0

100

100

1.2

Economic globalization has produced the greatest impact on the distribution of global energy demand. If economic growth is lower than expected, the share of Asia, Africa, and South America in energy consumption may be lower than the levels described in the previous scenario. In Africa in particular, local industrialization and urbanization will remain low, dragging down regional energy consumption growth and weakening its position in the world’s energy demand structure, if economic development has not significantly improved while war and turbulence persist. Against this background and as opposed to the previous scenario, Africa’s total primary energy consumption in 2050 may fall to 1.5–2.0 billion tons of standard coal, thereby bringing down global energy consumption to around 27 billion tons of standard coal. By 2050, the share of Africa in global energy demand will maintain at around 5%, and annual energy consumption per capita at 0.6 tons of standard coal, little changed from 2010 levels.

Currently, energy consumption per capita in Africa, where 600 million people are still without access to electricity, is less than one-quarter of the world’s average. Judging by the fast-growing energy and electricity consumption in the developed countries of Europe and America and also China since it launched a policy of reform and opening-up, it can be envisaged that Africa will also see rapid growth in energy and electricity demand after embarking on a modernization drive. Expanding the supply of modern energy and improving energy consumption per capita in Africa is one of the important objectives towards eliminating energy poverty and achieving joint development globally, and also the major driving force behind global electricity demand growth.

3. Electricity Demand

Electricity demand is an important component of the energy demand structure. Given the continued economic and population growth worldwide, along with improved electrification, electricity demand will experience continued growth at a relatively fast speed. Under the framework of electricity substitution and clean energy substitution, the share of electricity will continue to rise in the end-use energy consumption structure and the primary energy supply structure. The share of electricity in energy demand will also rise substantially. Electricity will play a more important role in supporting socioeconomic development and helping to achieve greater economic expansion with lower energy demand growth.

3.1. Total Electricity Demand

Global electricity demand is expected to maintain relatively rapid growth. Over the past few decades, global electricity demand has been growing at a steadily faster rate, with average annual growth of electricity demand worldwide being 2.6% between 1990 and 2000, rising to 3.3% between 2000 and 2010. Judging by the growth trend in global energy demand and considering the accelerating efforts in implementing the two-replacement policy, global electricity demand is expected to soar from 21,400 TWh to 73,000 TWh in 2010–2050, representing annual growth of 3.1%. Annual electricity consumption per capita will shoot up from 3096 kWh to 7654 kWh, representing a 1.5-fold increase and annual growth of 2.3%. On a phased basis, electricity demand growth will slow down, as the major developed countries will have reached the saturation point by 2020 and renewable energy development and electricity substitution are still in their nascent stage. With the energy demand among emerging economies and underdeveloped countries growing rapidly while electricity substitution in developed countries has moved into a stage of fast advancement, electricity demand growth will pick up between 2020 and 2040. With the growing base of electricity demand and less room for substitution, electricity demand growth will slow by 2050. See Fig. 4.9 for the world’s total electricity demand and growth rates between 2010 and 2050.

Figure 4.9World’s Total Electricity Demand and Growth Rates, 2010–2050

Electricity demand growth is comparable to economic growth. Over the past two decades, the elasticity coefficient of global electricity consumption has hovered around 1. In 1990–2000, the elasticity coefficient stood at 0.9, increasing to 1.3 in 2000–2010. It is expected to fall to 1.0 in 2010–2050. By 2020, electrification in the industrial, construction, and transportation sectors will gain steady momentum, contributing to constantly rising electricity demand. However, with the subdued consumption growth among the major energy-intensive industries impacted by the global financial crisis, average growth of global electricity demand is expected to be 2.8% between 2010 and 2020, down 0.5 percentage points from the first decade of the twenty-first century, with an elasticity coefficient of electricity consumption of 0.9. After 2020, the substitution of electricity in various end-use segments for conventional fossil energy, especially coal and oil, will progress at an increasingly noticeable pace. The generating capacity of wind, solar, and other forms of renewable energy will experience significant expansion, with global electricity demand accelerating steadily, on an average annual basis, at expected rates of 3.3 and 3.8% in 2020–2030 and 2030–2040, respectively, with the elasticity coefficient of electricity consumption of 1.0 and 1.3, respectively. After 2040, due to the significantly expanding basis for comparison, electricity demand growth will slow to 2.6%, with the elasticity coefficient of electricity consumption easing to 0.9, in 2040–2050.

The fact that electricity demand growth has surpassed energy demand growth indicates the increasingly dominant role of electricity in the energy structure. It is statistically shown that global electricity demand will post annual growth of 3.1% between 2010 and 2050, 2.6 times the rate of energy demand growth and slightly higher than the average rate of economic growth. Average energy demand growth is expected to be 1.2%, indicative of the saturation of demand and growth “delinked” from the total economy. The fact that electricity demand growth has markedly surpassed energy demand growth reflects a gradual strengthening of the central position of electricity in the energy system and the need to prioritize electric energy development. See Fig. 4.10 for the total world economy and growth in energy and electricity demand between 2010 and 2050.

Figure 4.10The World’s Total Economy and Energy, Electricity Demand Growth, 2010–2050 Note: The initial values of the total economy, electricity demand, and energy demand are set at 1 for the purpose of nondimensionalization.

In developed countries and regions, electricity demand has moved into a period of steady natural growth, with future growth potential coming primarily from electricity substitution. Asia, Africa, and South America are now the world’s major centers of electricity demand growth where demand is expected to maintain relatively fast growth for a while. If the saturation point of electricity demand sets in ahead of time in Asia, Africa, and South America, or electricity substitution in Europe, America and Oceania proceeds more slowly than expected, total global electricity demand may drop to 50,000–60,000 TWh as opposed to the above-mentioned scenario.

3.2. Electricity Demand Distribution

Fundamental changes in the world’s electricity demand situation are expected to occur in line with economic adjustments. The share of developed economies in Europe and America in total global electricity demand will decline substantially, in contrast with a significantly higher share of Asia, Africa, and South America in a rise in total global electricity demand. For a long period, the developed economies in Europe and America have been the world’s major electricity consumers. In 1990, the OECD countries accounted for about 65% of the world’s total electricity consumption and non-OECD countries, only about 35%. More recently, and driven by the fast-growing electricity consumption among emerging economies, non-OECD countries accounted for 51% of total global consumption in 2010, rising to 53% in 2013. In 2010–2050, Asia, Africa, and South America will contribute to over 80% of new global demand growth on account of their population and economic growth, representing shares of 56.7, 17.1, and 7.8%, respectively. Asia will continue to see improvements in electrification in the industrial, construction and transportation sectors, with annual electricity demand per capita rising from 2088 kWh to 7361 kWh (equivalent to the consumption per capita of Europe in 2010), and its share of electricity demand increasing from 41% to 52% of the global total. From very low levels of electrification, Africa and South America will see a sharp increase in electrified operations, as evidenced by the expected growth of annual electricity demand to 3971 and 6547 kWh, or 13 and 7% of the global total, respectively. See Table 4.2 for the electricity demand scenario analysis for the world and individual continents between 2010 and 2050.

Table 4.2

Electricity Demand Scenario Analysis for the World and Individual Continents, 2010–2050

Region

Electricity Demand (1000 TWh)

Share (%)

Growth Rate (%)

2010

2020

2030

2040

2050

2010

2050

2010–2050

Africa

8.7

12.8

18.8

28.9

38.0

40.7

52.0

3.8

Europe

5.4

6.2

7.8

9.4

9.5

25.0

13.0

1.4

North America

5.3

6.2

7.6

9.3

10.2

24.9

14.0

1.6

South America

1.1

1.6

2.3

3.7

5.1

5.0

7.0

4.0

Africa

0.6

1.0

2.0

4.5

9.5

3.0

13.0

6.9

Oceania

0.3

0.4

0.5

0.6

0.7

1.4

1.0

2.2

World

21.4

28.2

39.0

56.4

73.0

100

100

3.1

Despite a very high base of per capita electricity demand, North America, Europe, and Oceania will continue to experience growing power demand as the substitution of electricity for traditional fossil energy continues. By 2050, electricity demand per capita in North America, Europe and Oceania will have increased to 22,927, 13,398, and 12,835 kWh, respectively. In 2010–2050, the total electricity demand of the three regions is expected to grow at a yearly rate lower than the world average, accounting for a sharply lower share of the world’s total power demand.

In terms of growth rates, Europe, North America, and Oceania will see relatively low demand growth after the completion of the industrialization process, with annual growth of 1–2% between 2010 and 2050. In contrast, Asia, South America, and Africa will see faster growth in electricity demand at a yearly rate of more than 3% between 2010 and 2050, due to their population numbers and ongoing industrialization. Average annual growth in electricity demand in Africa, the least industrialized continent, is expected to almost double the level recorded in Asia, reflecting the combined effect of fast-growing industrialization and population. See Fig. 4.11 for the annual growth of electricity demand by continent between 2010 and 2050.

Figure 4.11Annual Growth Rate of Electricity Demand by Continents, 2010–2050

On a per capita basis, the world’s electricity demand is expected to be around 7650 kWh in 2050, slightly higher than Europe’s consumption per capita in 2010 and equivalent to that of the United States in 2010. By that time, following decades of relatively strong growth, Asia and South America will reach or come close to the world average in terms of per capita electricity consumption. Despite its fast growing demand, Africa’s electricity consumption per capita will only reach 52% of the world average by 2050, given the very low base it started from.

In Europe, Oceania, and North America, consumption per capita will continue to grow driven by a large consumer base and the potential of electricity substitution, but the margin with the world average will become significantly narrower. In 2010, per capita electricity consumption in Europe, Oceania, and North America was 2.3, 2.7, and 5.0 times the world average, respectively. In 2050, the figures are expected to fall to 1.8, 1.7, and 3.0 times, respectively, indicating a narrowing gap in per capita consumption around the world in the future. See Fig. 4.12 for the electricity consumption per capita in the world and individual continents in 2010 and 2050.

Figure 4.12Electricity Consumption Per Capita of the World and Individual Continents in 2010 and 2050

As an overall trend, the narrowing gap in electricity demand among different continents is apparently in line with the globalization process. Although the speed of narrowing varies with the natural growth of regional demand and the substitution rate of electricity for other energy forms, the overall share of developed countries and regions in global electricity demand will maintain a downward trend.

The factors affecting regional electricity demand are wide and varied, and there are divergent expectations as to the future electricity demand in selected regions. For example, the IEA is relatively conservative about the level of electrification improvement in Africa, expecting that by 2040, over 500 million people on the continent will still be denied access to electricity.6 In 2012, over 620 million people in Sub-Saharan Africa went without electricity, accounting for half of the world’s total population being denied access to electric power. Furthermore, with the benefit of increased power supply offset by rapid population growth, Sub-Saharan Africa will become the world’s only region with a population living without electricity. See Fig. 4.13 for information on Africa’s “powerless” population.

Figure 4.13Africa’s Population Without Access to Electricity by Country, 2012Source: Ref. [70].

A lack of power infrastructure has become a major hindrance to the development of Africa, amid its rapid economic expansion. According to IEA estimates, an investment of more than US$300 billion in electricity infrastructure is required for Sub-Saharan Africa to completely resolve the problem of power shortage by 2030. In recent years, China as well as the United States and European countries and regions have strengthened their investments in Africa’s electricity infrastructure. For example, China offered a US$20 billion loan to Africa in March 2013, with the greater part of the amount planned to go into building electricity infrastructure in support of the continent’s economic development. During his visit to Africa in July 2013, United States President Barack Obama proposed the Power Africa program to resolve the power shortage problem in Africa through an US$7 billion investment. With improvements in the global economy and the governance structure over the next few decades, Africa will see greatly improved popularity of power supplies and a significant reduction in its “powerless” population, with the growing development of electricity infrastructure.

4. Future Global Energy Development Structure

In 2050, global primary energy demand is expected to surge to 30 billion tons of standard coal, including electricity demand of 73,000 TWh. The need to meet such massive power and electricity requirements spells major changes to the development of energy worldwide. Particularly in a low-carbon development environment in response to climate change, the pace of clean substitution will quicken with a rising share of fast developing and utilized renewables in the energy mix to gradually replace fossil fuels, which will see increasingly lower levels of development and utilization, as the dominant energy source of the future. By 2050, global supplies of fossil energy are forecast to decrease to 6.3 billion tons of standard coal, down 57% from 2010, while global supplies of nonfossil energy are expected to skyrocket to 23.7 billion tons of standard coal, up 480%. As the dominant energy source, renewables will see a new pattern of global development focusing on the construction of bases supplemented by distributed generation, with accelerated efforts in building large bases of hydropower, wind, solar, and other renewable energy in the Arctic and equatorial regions and on each continent.

4.1. Overview of Energy Supply

As the dominant energy source of the future, clean energy will see accelerated development and it is expected that the generating capacity of global clean energy will reach 66,000 TWh (accounting for 90% of the world’s total generating capacity) in 2050. Here is a breakdown of clean energy as a share of global generation: solar and wind power (66%), hydropower (14%), biomass energy and others (approximately 10%), and ocean and nuclear energy (approximately 10%). Judging by the conditions of clean energy development on each continent,7 Asia’s share of global clean energy generation is expected to reach 49% by 2050, followed by a 16% share attributable to Africa as the most important region of solar energy development. See Fig. 4.14 for the global power supply structure in 2050 and Fig. 4.15 for each continent’s share of global clean energy generation in the same year.

Figure 4.14Global Power Supply Structure in 2050

Figure 4.15Share of Clean Energy Generation by Continents in 2050

Fossil energy generation will experience a sharp decrease. Fossil energy, mainly natural gas and coal-fired generation, is expected to account for approximately 10% of global electricity generation in 2050. In anticipation of the need to accommodate the system operational requirements of grid-connected, large-capacity wind, solar, and other renewable energy generation, a certain level of natural gas generation capacity will be retained while efforts continue to develop pumped storage capability. Dictated by its own level of development and the capacity of renewable energy generation, Asia will retain a relatively high level of natural gas and coal-fired generation in 2050. North America, owing to the mature technology and relatively low costs of developing shale gas and other unconventional gas resources, will retain a relatively high level of natural gas generation. See Fig. 4.16 for the change in the share of power generation attributable to fossil energy in 2010–2050. A breakdown of fossil energy generation by continent in 2050 is shown in Fig. 4.17.

Figure 4.16Changes in the Share of Fossil Energy Generation in 2010–2050

Figure 4.17Fossil Energy Power Generation by Continents in 2050

Distributed generation is an integral part of energy supply. Distributed generation worldwide is expected to reach 11,000 TWh in 2050, accounting for 15% of total power generation. Based on each continent’s development of distributed generation with reference to renewable energy resources, population and other factors, Asia’s share of global distributed generation is expected to reach 41% in 2050. Africa, blessed with favorable conditions for developing distributed generation of solar, hydropower, biomass, and other renewable energy, is expected to have a 27% share, ranking second among all continents. See Fig. 4.18 for a breakdown of distributed power generation by continent in 2050.

Figure 4.18Share of Distributed Generation by Continents in 2050

4.2. Large-Scale Clean Energy Bases on Each Continent

World continents are basically abundant in clean energy resources, such as hydropower, wind, solar, and ocean energy. The development of large-scale power generation bases in regions with favorable resource conditions can render strong support to the requirements of energy sustainability at the intracontinental or transcontinental level.

4.2.1. Asia

Asia, covering an area of over 44 million km2 (30% of the global land mass), is the largest continent in the world where water, wind, solar and other clean energy resources abound. Favorable water resource conditions are found mainly in the upper reaches of the Yangtze River and the Yalong Zangbo River in China as well as the Yenisei, Rivers Ob and Lena in the Russian far-east and Siberia. Wind power resources are mainly distributed in Mongolia, Central Asia, the “Three North” region (northwestern China, northern China, and northeastern China), as well as the Kara Sea, the Bering Strait, and the Kamchatka Peninsula in the Arctic region. Solar energy resources abound in Mongolia, Central Asia, the Middle East, and north-west China.

4.2.1.1. Renewable Energy Generation Bases in China

1.Hydropower bases in southwestern China. The technologically developable capacity of the country’s hydropower resources is estimated at about 570 GW, the great majority (82%) of which is concentrated in southwest China. As at the end of 2013, conventional hydropower stations in China boasted a total installed capacity of 280 GW, with the remaining technologically developable capacity of 290 GW concentrated in Sichuan, Yunnan, Tibet, and other areas. Large hydropower bases are to be built along the Jinsha River, the Yalong River, the Dado River, the Lanchang River, the Yalong Zangbo River, and the Nujiang River, carrying a total installed capacity of over 260 GW. See Fig. 4.19 for the distribution of hydropower bases in China.

2.Wind power bases in the “Three North” region. In China, onshore wind resource potential at 80 m height with a wind power intensity of above 150 W/m2 is estimated at 10,200 GW; wind resource potential over Grade 3 in near-shore areas with a water depth of 5–25 m and at 50 m height (wind power intensity ≥300 W/m2), at 200 GW. The “Three North” region accounts for approximately 80% of China’s national total of onshore wind resources. The distribution of China’s wind power resources is shown in Fig. 4.20.

3.Solar energy generation bases in northwestern China. The annual solar radiation falling on China’s land surface is estimated at the equivalent of 4.9 trillion tons of standard coal. In particular, the Qinghai–Tibet Plateau, northern Gansu, northern Ningxia, southern Xinjiang, the Gobi Desert, and other desert areas are blessed with the most abundant solar resources, with strong development potential estimated at over 85,000 TWh per year or approximately 75% of the nation’s total solar energy reserves. With favorable conditions for development, large-scale solar energy generation bases can be established to transmit power to load centers in eastern and central China. The distribution of China’s solar energy resources is shown in Fig. 4.21.

Figure 4.19Distribution of Hydropower Bases in China

Figure 4.20Distribution of China’s Wind Power ResourcesSource: SGCC, Wind Power Development Promotion White Paper by SGCC, 2011.

Figure 4.21Distribution of China’s Solar Energy ResourcesSource: CMA Wind and Solar Energy Resources Center.

4.2.1.2. Wind Power Bases in North Russia and Hydropower Bases in Siberia, the Russian Far-East

1.Wind power bases in north Russia. Russia is endowed with abundant wind power resources, largely along the coast of the Arctic Ocean in the Arctic region. Technologically developable wind power capacity in the region from the Kamchatka Peninsula to the Bering Strait is estimated at more than 7000 TWh per year,8 compared with an estimated 3400 TWh per year8 for the Kara Sea and its coastal regions, based on approximately 4000 h of utilization. With its huge potential, the Arctic region in Russia holds great promise as Asia’s major base of wind power to be. See Fig. 4.22 for a wind speed map of Russia (based on satellite-based observations).

2.Hydropower bases in the Russian far-east and Siberia. The water resources in Russia available for large-scale development are located chiefly along the Lena River, the Yenisei, the River Ob, and the Amur River (the section in China is known as the Heilongjiang River) in the Russian Far East and Siberia. Out of an economically developable capacity of over 700 TWh/year, 500 TWh/year has yet to be developed. See Fig. 4.23 for the distribution of Russia’s major river basins.

Figure 4.22Wind Speed Map of Russia (Based on Satellite-Based Observations)

Figure 4.23Distribution of Russia’s Major River Basins

4.2.1.3. Wind, Solar, and Hydropower Bases in Central Asia

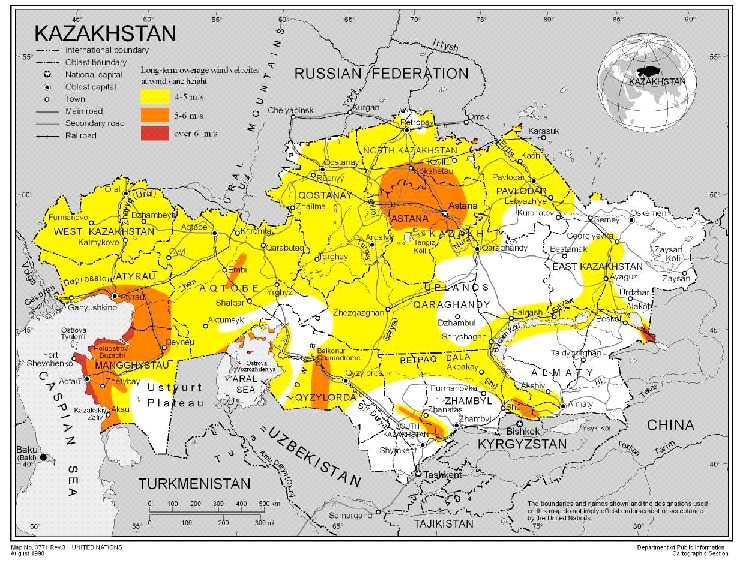

1.Wind power bases in Central Asia. Wind power resources in Central Asia are mainly distributed in Kazakhstan, with a technologically developable capacity of approximately 1800 TWh. Wind power resources are most abundant in Atyrau and Mangistau near the Caspian Sea, centrally located Astana and Karaganda, and regions in the south, where large wind power bases can be built in the future. See Fig. 4.24 for the distribution of wind power resources in Kazakhstan.

2.Solar power bases in Central Asia. Central Asia has an annual irradiation intensity of 1300–1800 kWh/m2. In the eastern and southeastern parts of Turkmenistan where the terrain is flat, an annual irradiation intensity that often exceeds 1800 kWh/m2 is recorded, reaching 70–80% of the comparative figure for the Sahara Desert in Africa. Solar energy resources abound in South Kazakhstan, Kyzylordinskaya, the coastal regions of the Caspian Sea, and southeastern Uzbekistan, where conditions are favorable for the development of solar power stations. See Figs. 4.25–4.27 for the distribution of solar energy resources in Turkmenistan, Kazakhstan, and Uzbekistan.

3.Hydropower bases in Central Asia. Hydropower resources in Central Asia are chiefly distributed in Kyrghyzstan and Tajikistan, the former with a technologically developable capacity of about 150 TWh/year, compared with the latter’s approximately 260 TWh/year. Large hydropower bases can be built there in the future to supply power to surrounding countries.

In Mongolia, the technologically developable capacity of wind power is estimated at 2500 TWh/year, while solar power potential is estimated at 3400 TWh/year. These resources are concentrated in Mongolia’s southeastern regions. Wind power resources on over 10% of Mongolian land receive an “excellent” rating, while wind power resources on over 40% of Mongolian land are rated between “average” and “good.” The country’s southern and eastern regions see the highest concentration of wind power potential, whereas solar energy resources are mostly located in the central and southern regions of Gobi, where conditions are suitable for building large solar power bases with an annual irradiation intensity of 1200–1600 kWh/m2. Given the country’s relatively low power load, virtually all wind and solar energy to be developed locally can be exported. Renewable energy produced in Mongolia is mostly delivered to Northeast Asia, with a transmission distance of less than 2500 km. See Figs. 4.28 and 4.29 for the distribution of wind and solar energy resources in Mongolia.

Figure 4.28Distribution of Wind Energy Resources in MongoliaSource: Wind Energy Resources Map by the US National Renewable Energy Laboratory; data from AWS TruePower.

Figure 4.29Distribution of Solar Energy Resources in MongoliaSource: 3TIER Wind and Solar Energy Resources Evaluation Company.

4.2.1.5. Solar Power Bases in the Middle East

Solar energy resources abound in the Middle East, especially in Saudi Arabia and Yemen with an annual irradiation intensity of over 2500 kWh/m2. The annual irradiation intensity in Iran, Oman, the United Arab Emirates, Jordan, and other countries exceeds 2100 kWh/m2. The technologically developable capacity of solar energy in the Middle East is initially estimated at over 100,000 TW/year. See Fig. 4.30 for the distribution of solar energy resources in the Middle East.

A southern Asian country, India provides favorable sunlight conditions for solar power generation. Gujarat and Rajasthan in the west boast the most abundant solar energy resources, with an annual solar irradiation intensity of over 2100 kWh/m2, followed by central and southern regions with a sunlight intensity of 1850–2100 kWh/m2. These regions are expected to become home to large solar energy bases in the future. The distribution of solar energy resources in India is shown in Fig. 4.31.

India’s total wind power resources are estimated at about 100 GW. Quality resources are located predominantly in the western states of Gujarat and Rajasthan, as well as the southern region and eastern coastal areas, usually with a wind power intensity of 250 W/m2. The best wind energy resources are found near the southern state of Kerala, with a wind power intensity of over 350 W/m2. The distribution of wind power resources in India is shown in Fig. 4.32.

With an area of over 10 million km2, Europe boasts relatively rich wind and solar energy resources. Wind resources are predominantly located near the North Sea, Greenland and its surrounding waters further north, the Norwegian Sea, and the Barents Sea. Solar resources are mainly distributed along the coasts of the Mediterranean Sea in the south.

4.2.2.1. Wind Power Bases in Greenland

Greenland and its surrounding waters occupy an area of 2.63 million km2, with a wind power intensity of over 300 W/m2 at 70 m height,9 and a technologically developable capacity of wind energy of about 32.5 TW.10 The annual average wind across the Greenland Sea south of Greenland carries a maximum speed of 12–14 m/s; the annual average wind speed in the north is relatively low, at 7–10 m/s. The annual average wind speed in the northwest is about 5–7 m/s; the wind speed near the sea is quite low. The wind power intensity in the west, east and south of Greenland is high, while that along the coast is quite low. In winter, the wind power intensity of over 50% of Greenland is higher than 400 W/m2. Wind power is stronger in the west in spring and also stronger in the east in autumn. Seasonally, average wind speed and wind power intensity move in the descending order of winter > autumn > spring > summer.

4.2.2.2. Wind Power Bases in the Norwegian Sea and the Barents Sea

Lying to the east of Greenland in the Arctic Ocean, the Norwegian Sea, and the Barents Sea are regarded as the second windiest place in the Arctic region, with an annual average wind speed of 9–10 m/s, second only to that of the Greenland Sea.

4.2.2.3. Wind Power Bases in Europe’s North Sea Region

In the North Sea region, annual average wind speed at 60 m height is estimated at 8 m/s, with the region’s wind power resources amounting to 30,000 TWh/year. Coastal wind power resources are especially abundant in the United Kingdom, Denmark, Germany, and the Netherlands. Based on an installed capacity of 6000 kW/km2, the United Kingdom’s highest offshore wind power potential reaches 986 TWh/year, compared with 24 TWh/year for Belgium, 136 TWh/year for the Netherlands, 237 TWh/year for Germany, and 550 TWh/year for Denmark.11 Large wind power bases can be built offshore in the future to supply power to the domestic markets and countries in central-southern Europe. See Fig. 4.33 for the wind power development in the North Sea.

Figure 4.33Wind Power Development in the North SeaSource: Friends of the Supergrid, the first phase of the European supergrid.

4.2.2.4. Solar Energy Bases in South Europe

South Europe consists of the Iberian Peninsula, the Apennine Peninsula and south Balkan Peninsula, covering 17 countries on a total area of about 1.66 million km2. It is also known as Mediterranean Europe for its proximity to the Mediterranean. It has an annual average irradiation intensity of 2000 kWh/m2, with a technologically developable solar capacity of approximately 2600 TWh/year. Teeming with solar energy resources, Portugal, Spain, Italy, Greece, and Turkey provide favorable conditions for building large solar energy bases. The distribution of solar energy resources in South Europe is shown in Fig. 4.34.

North America, covering a territory of over 24 million km2 or 16.2% of the world’s total land area, is the third largest continent in the world. Its topography is characterized by mountain ranges lying far apart in the west and in the east that run north–south in alignment with the coastlines. The Great Plains are situated in the middle of North America. Wind power resources are most abundant in the Midwest while solar energy resources are concentrated mainly in the American Southwest and northern Mexico.

4.2.3.1. Wind Power Bases in the Midwest

Wind power resources in North America are concentrated mainly in North Dakota, South Dakota, Montana, and Wyoming in the Midwest. Based on a capacity coefficient of over 30% at 80 m height, the technologically developable wind power capacity in the US is estimated at approximately 33,000 TWh/year.12 Offshore wind resources in the United States are mainly distributed along the coastal areas in the east and west. Based on 830,000 km2 of offshore areas within 50 nautical miles from the coast and with a wind speed of over 7.0 m/s at 90 m height, the technologically developable wind power capacity is estimated at approximately 17,000 TWh/year. The flat and open terrain of the Central United States, with an annual average wind speed of over 7 m/s and abundant wind resources, creates ideal conditions for the development of large wind power bases. See Figs. 4.35 and 4.36 for the annual average onshore wind power intensities and the distribution of average wind speeds in the United States.

Figure 4.35Distribution of Annual Average Onshore Wind Power Intensities in the United StatesSource: Wind power data and map formulated by Pacific Northwest National Laboratory, courtesy of the National Renewable Energy Laboratory.

Figure 4.36Distribution of Annual Average Onshore Wind SpeedsSource: Wind Energy Resources Map by National Renewable Energy Laboratory; data from AWS TruePower.

4.2.3.2. Solar Power Bases in the American South-West

Abundant solar energy resources in the United States are predominantly located in the south-west, covering Arizona, New Mexico, California, South Nevada, and other states. Considering the ratio of land suitable for development and also generation efficiency, technologically developable capacity is estimated at approximately 254,000 TWh/year. See Fig. 4.37 for the distribution of solar energy resources in the US.

The annual solar irradiation falling on over 80% of Mexican territory has an intensity of over 2,000 kWh/m2, providing suitable conditions for building large solar energy generation bases with a technologically developable capacity of about 78,000 TWh. The Baja California Peninsula west of the Gulf of California enjoys the highest annual irradiation intensity at above 2300 kWh/m2. The distribution of solar energy resources in Mexico is shown in Fig. 4.38.

In Canada, the technologically developable capacity of hydropower resources is estimated at about 262 GW,13 with 160 GW under development planning in Quebec in the east (44 GW), Ontario (10 GW), British Columbia (33 GW), Alberta (12 GW), the Yukon (GW), and the Northwest Territories (16 GW). The country’s main rivers include the St. Lawrence River, the Nelson River, and the Columbia River. Hydropower development and bases are mainly located in the provinces and regions near the United States border. The distribution of Canada’s major rivers is shown in Fig. 4.39.

Figure 4.39Distribution of Canada’s Major Rivers

4.2.4. South America

Occupying over 17 million km2, South America is situated in the southern part of the Western Hemisphere, separated from North America by the Panama Canal. In this region, the Andes Mountains, several kilometers high, tower over the west, with plains lying to the east, including the Amazon rainforest. Abundant solar energy resources are distributed west of the Andes Mountains, covering countries such as Peru, Chile, and Bolivia. Water resources are concentrated in the Amazon and other river basins in Brazil.

4.2.4.1. Solar Power Bases Along the East and West Coasts