CHAPTER 3

Credit Derivatives

The interest rate derivatives explained in the previous chapter are used in structured finance transactions to control interest rate risk with respect to changes in the level of interest rates. Credit derivatives, in contrast, allow the transfer of credit risk from parties in a structured finance transaction who want to shed credit risk to counterparties willing to accept credit risk.

The eight major credit derivatives according to the British Bankers Association are:1

- credit default swaps;

- index swaps such as credit default index swaps;

- basket default swaps;

- asset swaps;

- total return swaps;

- portfolio/synthetic collateralized debt obligations; and

- credit-linked notes.

We will discuss all but the last two credit derivatives in this chapter. Portfolio/synthetic collateralized debt obligations are discussed in Chapter 7 and credit-linked notes in Chapter 9.

DOCUMENTATION AND CREDIT DERIVATIVE TERMS

Before describing the various types of credit derivatives, we will discuss the documentation and key terms for credit derivatives. The International Swap and Derivatives Association (ISDA) first developed in 1998 a standard contract that could be used by parties for trades in credit derivatives contracts. While the documentation is primarily designed for credit default swaps and total return swaps, the contract form is sufficiently flexible so that it can be used for the other credit derivatives described in this chapter as well.

Reference Entity and Reference Obligation

The documentation will identify the reference entity and/or the reference obligation. The reference entity, also referred to as the reference issuer, is the issuer of the debt instrument. The reference obligation, also referred to as the reference asset, is the particular debt issue for which the credit protection is being sought. For example, a reference entity could be Viacom. The reference obligation would be a specific Viacom bond issue.

Credit Events

A credit derivative has a payout that is contingent upon a credit event occurring. The 1999 ISDA Credit Derivatives Definitions (referred to as the “1999 Definitions”) provides a list of eight credit events that seek to capture every type of situation that could cause the credit quality of the reference entity to deteriorate or cause the value of the reference obligation to decline:

- bankruptcy;

- credit event upon merger;

- cross acceleration;

- cross default;

- downgrade;

- failure to pay;

- repudiation/moratorium; and

- restructuring.

Bankruptcy is defined as a variety of acts that are associated with bankruptcy or insolvency laws. Failure to pay results when a reference entity fails to make one or more required payments when due. When a reference entity breaches a covenant, it has defaulted on its obligation. When a default occurs, the obligation becomes due and payable prior to the original scheduled due date (had the reference entity not defaulted). This is referred to as an obligation acceleration. A reference entity may disaffirm or challenge the validity of its obligation. This is a credit event that is covered by repudiation/moratorium.

The most controversial credit event that may be included in dealing with credit derivatives is restructuring of an obligation. A restructuring occurs when the terms of the obligation are altered so as to make the new terms less attractive to the debt holder than the original terms. The terms that can be changed typically include, but are not limited to, one or more of the following:

- a reduction in the interest rate;

- a reduction in the principal;

- a rescheduling of the principal repayment schedule (e.g., lengthening the maturity of the obligations) or postponement of an interest payment; and

- a change in the level of seniority in the reference entity's debt structure.

The reason why restructuring is so controversial is that a protection buyer benefits from the inclusion of restructuring as a credit event and feels that eliminating restructuring as a credit event will erode its credit protection. The protection seller, in contrast, would prefer not to include restructuring since even routine modifications of obligations that occur in lending arrangements may trigger a payout to the protection buyer. Moreover, if the reference obligation is a loan and the protection buyer is the lender, there is a dual benefit for the protection buyer to restructure a loan. The first benefit is that the protection buyer receives a payment from the protection seller. Second, the accommodating restructuring fosters a relationship between the lender (who is the protection buyer) and its customer (the corporate entity that is the obligor of the reference obligation).

Because of this problem, the Restructuring Supplement to the 1999 ISDA Credit Derivatives Definitions (the “Supplement Definition”) issued in April 2001 provided a modified definition for restructuring. There is a provision for the limitation on reference obligations in connection with restructuring of loans made by the protection buyer to the borrower that is the obligor of the reference obligation. In addition, the supplement limits the maturity of reference obligations that are physically deliverable when restructuring results in a payout triggered by the protection buyer.

In January 2003, the ISDA published its revised credit events definitions in the 2003 ISDA Credit Derivative Definitions (referred to as the “2003 Definitions”). The revised definitions reflected amendments to several of the definitions for credit events set forth in the 1999 Definitions. Specifically, there were amendments for bankruptcy, repudiation, and restructuring. The major change was to restructuring, whereby the ISDA allows parties to a given trade to select from among the following four definitions:

- no restructuring;

- ldquo;full” or “old” restructuring, which is based on the 1998 Definitions;

- “modified restructuring,” which is based on the Supplement Definition; and

- “modified modified restructuring.”

CREDIT DEFAULT SWAPS2

By far, credit default swaps are the largest sector of the credit derivatives market. A credit default swap has a single reference entity and is therefore referred to as a single-name credit default swap. In a credit default swap, the protection buyer pays a fee to the protection seller in exchange for the right to receive a payment conditioned upon the occurrence of a credit event by the reference entity. Should a credit event occur, the protection seller must make a payment and the contract terminates. If no credit event occurs by the maturity of the swap, both sides terminate the swap agreement and no further obligations are incurred. The tenor, or length of time of a credit default swap, is typically three to five years.

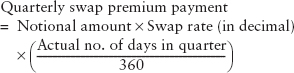

In a typical credit default swap, the protection buyer pays for the protection premium over several settlement dates rather than upfront. A standard credit default swap specifies quarterly payments. The quarterly payment is determined using one of the day-count conventions in the bond market. The day-count convention used for credit default swaps is actual/360, the same convention used in the U.S. dollar interest rate swap market. A day convention of actual/360 means that to determine the payment in a quarter, the actual number of days in the quarter are used and 360 days are assumed for the year. Consequently, the swap premium payment for a quarter is

Credit default swaps can be settled in cash or physically. Physical delivery means that if a credit event as defined by the documentation occurs, a bond issue of the reference entity is delivered by the protection buyer to the protection seller in exchange for a cash payment. Because physical delivery does not rely upon obtaining market prices for the reference obligation in determining the amount of the payment in a credit default swap, this method of delivery is more efficient in terms of determining the protection payout.

To illustrate the mechanics of a credit default swap, we assume that the reference entity is Corporation W and the underlying is $10 million par value of the bonds of Corporation W. The $10 million is the notional amount of the contract. The swap premium—the payment made by the protection buyer to the protection seller—is 250 bp per annum. Suppose that there are 91 actual days in a quarter. Then the quarterly swap premium payment made by the protection buyer would be

![]()

In the absence of a credit event, the protection buyer will make a quarterly swap premium payment over the life of the swap. If a credit event occurs, two things happen:

- The protection buyer pays out the accrued premium from the last payment date to time of credit event, on a days fraction basis. After that payment, there are no further payments of the swap premium by the protection buyer to the protection seller.

- A termination value is determined for the swap.

The procedure for computing the termination value depends on the settlement terms provided by the swap. Settlement will be either physical or cash. As noted above, the market practice for credit default swaps is physical settlement. With physical settlement the protection buyer delivers a specified amount of the face value of bonds of the reference entity to the protection seller. The protection seller pays the protection buyer the face value of the bonds.

Since all reference entities that are the subject of credit default swaps have many issues outstanding, there will be a number of alternative issues of the reference entity that the protection buyer can deliver to the protection seller. These issues are known as deliverable obligations. The swap documentation will set forth the characteristics necessary for an issue to qualify as a deliverable obligation. The short will select the cheapest-to-deliver issue and the choice granted to the short is effectively an embedded option. From the list of deliverable obligations, the protection buyer will select for delivery to the protection seller the cheapest-to-deliver issue.3

With cash settlement, the termination value is equal to the difference between the nominal amount of the reference obligation for which a credit event has occurred and its market value at the time of the credit event. The termination value is then the amount of the payment made by the protection seller to the protection buyer No bonds are delivered by the protection buyer to the protection seller. The documentation for the basket default swap, explained in the next section, sets forth how the market value at the time of the credit event is determined.

CREDIT DEFAULT SWAP INDEX

In a credit default swap index, the credit risk of a standardized basket of reference entities is transferred between the protection buyer and protection seller. As of year end 2005, the only standardized indexes are those compiled and managed by Dow Jones. For the corporate bond indexes, there are separate indexes for investment-grade and high-yield names. The most actively traded contract as of year end 2005 is the one based on the North American Investment Grade Index (denoted by DJ.CDX.NA.IG). As the name suggests, the reference entities in this index are those with an investment-grade rating. The index includes 125 corporate names in North America. The index is an equally weighted index. That is, each corporate name (i.e., reference entity) comprising the index has a weight of 0.8%. The index is updated semiannually by Dow Jones.

The mechanics of a credit default swap index are slightly different from those of a single-name credit default swap. As with a single-name credit default swap, a swap premium is paid. However, if a credit event occurs, the swap premium payment ceases in the case of a single-name credit default swap. In contrast, for a credit default swap index the swap payment continues to be made by the protection buyer. However, the amount of the quarterly swap premium payment is reduced. This is because the notional amount is reduced as result of a credit event for a reference entity.

For example, suppose that a portfolio manager is the protection buyer for a DJ.CDX.NA.IG and the notional amount is $100 million. Using the formula above for computing the quarterly swap premium payment, the payment before a credit event occurs would be

![]()

After a credit event occurs for one reference entity, the notional amount declines from $100 million to $99,200,000. The reduced notional amount is equal to 99.2% of the $100 million because each reference entity for the DJ.CDX.NA.IG is 0.8%. Thus, the revised quarterly swap premium payment until the maturity date or until another credit event occurs for one of the other 124 reference entities is

![]()

As of this writing, the settlement term for a credit default swap index is physical settlement. However, the market is considering moving to cash settlement. The reason is because of the cost of delivering an odd lot in the case of a credit event for a reference entity. For example, in our hypothetical credit default swap index if there is a credit event, the protection buyer would have to deliver to the protection seller bonds of the reference entity with a face value of $80,000. Neither the protection buyer nor the protection seller would like to deal with such a small position.

BASKET DEFAULT SWAPS

As explained in Chapter 1, a collateralized debt obligation (CDO) is a structured portfolio credit. The major growth in this sector of the market is the synthetic CDO sector. This structure relies on the use of basket default swaps. Unlike a single-name CDS, in a basket default swap, there is more than one reference entity. There are different types of basket default swaps. They are classified as follows:

- Nth-to-default swaps;

- subordinate basket default swaps; and

- senior basket default swaps.

Nth-to-Default Swaps

In an Nth-to-default swap, the protection seller makes a payment to the protection buyer only after there has been a default for the Nth reference entity and no payment for default of the first (N − 1) reference entities. Once there is a payout for the Nth reference entity, the credit default swap terminates. That is, if the other reference entities that have not defaulted subsequently do default, the protection seller does not make any payout.

Let us begin with an illustration of a first-to-default basket swap. We will assume that there are five reference entities. The payout for a first-to-default basket swap is triggered after there is a default for only one of the reference entities. For any subsequent defaults for the four remaining reference entities, there is no payment made by the protection.

In a second-to-default basket swap, a payout is triggered only after there is a second default from among the reference entities. Again, assuming there are five reference entities, in a second-to-default swap, if there is only one reference entity that a defaults over the tenor of the swap, no payment is made by the protection seller. However, if there is a default for a second reference entity during the swap's tenor, there is a payout by the protection seller. After that payment, the swap terminates and the protection seller does not make any payment for a default that may occur for the three remaining reference entities.

Subordinate Basket Default Swaps

In a subordinate basket default swap the two key elements are:

- a maximum payout for each defaulted reference entity; and

- a maximum aggregate payout over the tenor of the swap for the basket of reference entities.

To illustrate a subordinate basket default swap, we will assume that there are five reference entities and that (1) the maximum payout is $10 million for a reference entity and (2) the maximum aggregate payout is $15 million. We will also assume that defaults result in the following losses over the tenor of the swap:

| Loss Resulting from Default: | Amount |

|---|---|

| First reference entity | $6 million |

| Second reference entity | $10 million |

| Third reference entity | $16 million |

| Fourth reference entity | $12 million |

| Fifth reference entity | $15 million |

The mechanics of a subordinate basket default swap are then as follows:

- Should there be a default for the first reference entity, there is a $6 million payout.

- The remaining amount that can be paid out on any subsequent defaults for the other four reference entities is $9 million.

- Should there be a default for the second reference entity of $10 million, only $9 million will be paid out.

- The swap terminates.

Senior Basket Default Swap

In a senior basket default swap there is a maximum payout for each reference entity, but the payout is not triggered until after a specified dollar loss threshold is reached. To illustrate this type of swap, we once again assume that there are five reference entities and the maximum payout for an individual reference entity is $10 million. We also assume that there is no payout until the first $40 million of default losses. This amount is the threshold.

Using the hypothetical losses listed above for the subordinate basket default swap, the payout by the protection seller would be as follows. The losses for the first three defaults total $32 million. However, because of the maximum payout for a reference entity, only $10 million of the $16 million loss on the third reference entity is applied to the $40 million threshold. Consequently, after the third default, $26 million ($6 million + $10 million + $10 million) is applied toward the threshold. When the fourth reference entity defaults, only $10 million is applied to the $40 million threshold. At this point, $36 million is applied to the $40 million threshold. When the fifth reference entity defaults in our illustration, only $10 million is relevant since the maximum payout for a reference entity is $10 million. The first $4 million of the $10 million is applied to cover the threshold, bringing the the total payment by the protection seller to $40 million.

Comparison of Riskiness of Different Default Swaps4

Let's compare the riskiness of each type of default swap from the perspective of the protection seller. This will also help reinforce an understanding of the different types of swaps.

We will assume that for the basket default swaps there are the same five reference entities. The following four credit default swaps are ranked from highest to lowest risk for the reasons explained:

- Subordinate basket default swap: The maximum for each reference entity is $10 million with a maximum aggregate payout of $10 million.

- First-to-default swap: The maximum payout is $10 million for the first reference entity to default.

- Fifth-to-default swap: The maximum payout for the fifth reference entity to default is $10 million.

- Senior basket default swap: There is a maximum payout for each reference entity of $10 million, but there is no payout until a threshold of $40 million is reached.

All but the senior basket default swap will definitely require the protection seller to make a payout by the time the fifth loss reference entity defaults (subject to the maximum payout on the loss for the individual reference entities). Consequently, the senior basket default swap exposes the protection seller to the least risk.

Now look at the relative risk of the other three default swaps with a $10 million maximum payout: subordinate basket default swap, first-to-default swap, and fifth-to-default swap. Consider first the subordinate basket default swap versus first-to-default swap. Suppose that the loss for the first reference entity to default is $8 million. In the first-to-default swap the payout required by the protection seller is $8 million and then the swap terminates (i.e., there are no further payouts that must be made by the protection seller). For the subordinate basket swap, after the payout of $8 million of the first reference entity to default, the swap does not terminate. Instead, the protection seller is still exposed to $2 million for any default loss resulting from the other four reference entities. Consequently, the subordinate basket default swap has greater risk than the first-to-default swap. Finally, the first-to-default has greater risk for the protection seller than the fifth-to-default swap because the protection seller must make a payout on the first reference entity to default.

ASSET SWAPS

An investor who seeks to earn a credit spread on a fixed-rate credit-risky bond but also wants to minimize interest rate risk by converting a fixed-rate exposure to a floating-rate exposure can do so by using an asset swap. In an asset swap, the investor enters into the following two transactions simultaneously: buys the fixed-rate, credit-risky bond and enters into an interest rate swap. We discussed interest rate swaps in Chapter 2.

While an asset swap is not a true credit derivative, it is closely associated with the credit derivatives market because it explicitly sets out the price of credit as a spread over an investor's funding cost, typically the London interbank offered rate (LIBOR). Although it allows the acquiring of credit risk while minimizing interest rate risk, it does not allow an investor to protect against or transfer credit risk. It is because of this shortcoming of an asset swap that other types of derivative instruments and structured products, particularly credit default swaps, were created.

Investor Structured Asset Swap

An investor creates this structure by entering into the following terms in an interest rate swap:

- The investor will agree to be the fixed-rate payer.

- The term of the swap selected by the investor will match the maturity of the credit-risky bond purchased.

- The timing of the swap payments will match the timing of the cash flow of the credit-risky bond purchased.

If the issuer defaults on the issue, the investor must continue to make payments to the dealer and is therefore still exposed to interest rate risk.

Let us now illustrate a basic asset swap. Suppose that an investor purchases $20 million par value of a 6.85%, 5-year bond for a single A rated telecom company at par value. The coupon payments are semiannual. At the same time, the investor enters into a 5-year interest rate swap with a dealer where the investor is the fixed-rate payer and the payments are made semiannually. Suppose that the swap rate is 6.00% and the investor receives 6-month LIBOR plus 45 bp.

Let's look at the cash flow for the investor every six months for the next five years:

Thus, regardless of how interest rates change, if the telecom issuer does not default on the issue, the investor earns a 85 bp over 6-month LIBOR. Effectively, the investor has converted a fixed-rate, single-A, 5-year bond into a 5-year floating-rate bond with a spread over 6-month LIBOR. Thus, the investor has created a synthetic floating-rate bond.

This transaction has some similarities to an unfunded total return swap (TRS), although the dealer is not paying the total return of the bond. Rather it pays a floating LIBOR-based rate. Hence this deal lies between a pure asset swap and a TRS. As a matter of terminology, we should note that in a pure asset swap, the investor in a fixed-rate bond would pay the exact coupon on that bond to a counterparty in return for a floating-rate payment such as LIBOR, flat or plus or minus a spread. If the fixed-rate payment is different from the bond coupon, then in correct technical terms the investor simply owns a fixed-rate bond and enters into an interest rate swap, although the economics of the transaction are similar to those of a pure asset swap.

While our illustration has demonstrated how an asset swap can convert a fixed-rate bond into a synthetic floating-rate bond, an asset swap can also be used to convert a floating-rate bond into a synthetic fixed-rate bond.

Asset Swap Structure (Package) Created by a Dealer

In our description of an asset swap, the investor bought the credit-risky bond and entered into an interest rate swap with a dealer. Typically, an asset swap combines the sale of a credit-risky asset owned by an investor to a counterparty, at par and with no interest accrued, with an interest rate swap. This type of asset swap structure or package is referred to as a par asset swap. If there is a default by the issuer on the credit-risky bond, the asset swap transaction is terminated and the defaulted bonds are returned to the investor plus or minus any mark-to-market on the asset swap transaction. Hence, the investor is still exposed to the bond issuer's credit risk.

The coupon on the bond in the par asset swap is paid in return for LIBOR, plus a spread if necessary. This spread is the asset swap spread and is the price of the asset swap. In effect the asset swap allows investors that are LIBOR funded to receive the asset swap spread. This spread is a function of the credit risk of the underlying credit-risky bond. The asset swap spread may be viewed as equivalent to the price payable on a credit default swap written on that asset.

To illustrate this asset swap structure, suppose that in our previous illustration the swap rate prevailing in the market is 6.30% rather than 6.00%. The investor owns the telecom bonds and sells them to a dealer at par with no accrued interest. The asset swap agreement between the dealer and the investor is as follows:

- The term is five years.

- The investor agrees to pay the dealer 6.30% semiannually.

- The dealer agrees to pay the investor every six months 6-month LIBOR plus an asset-swap spread of 30 bp.

- Having sold the telecom bonds to the dealer, the investor no longer receives interest on them.

In our first illustration of an asset swap given earlier, the investor is creating a synthetic floater without a dealer. The investor owns the bonds. The only involvement of the dealer is as a counterparty to the interest rate swap. In the second structure, the dealer is the counterparty to the asset swap structure and the dealer owns the underlying credit-risky bonds. If there is a default, the dealer returns the bonds to the investor. This transaction in effect amounts to an unfunded total return swap (TRS). Normally, in an unfunded TRS, the bond is moved off the balance sheet to the dealer, and the dealer pays the floating rate (in this case, six-month LIBOR + 30 bp) and receives the prevailing swap rate (in this case 6.30% fixed), but the investor still receives the bond coupon. In a true-sale asset swap, however, the investor does not receive the coupon.

Using Swaptions to Remove Unwanted Structural Features

There are variations of the basic asset swap structure to remove unwanted noncredit structural features of the underlying credit-risky bond. The simplest example of an asset swap variation to remove an unwanted noncredit structural feature is when the bond is callable. If the bond is callable, then the future cash flows of the bond are uncertain because the issue can be called. Moreover, the issue is likely to be called if interest rates decline below the bond's coupon rate.

This problem can be addressed in a transaction where the investor buys the bond and enters into an interest rate swap. The tenor of the interest rate swap would still be for the term of the bond. However, the investor would also enter into a swaption in which the investor has the right to effectively terminate the swap from the time of the first call date for the bond to the maturity date of the bond. In the swaption, since the investor is paying fixed and receiving floating, the swaption must be one in which the investor receives fixed and pays floating. Specifically, the investor will enter into a receive fixed swaption.

In an asset swap that is structured with a dealer, this is simpler to do. The transaction can be structured such that the asset swap is terminated if the bonds are called.

TOTAL RETURN SWAPS

A total return swap is a swap in which one party makes periodic floating-rate payments to a counterparty in exchange for the total return realized on a reference asset (or underlying asset). The reference asset could be one of the following:

- credit-risky bond;

- a loan;

- a reference portfolio consisting of bonds or loans;

- an index representing a sector of the bond market; or

- an equity index.

Our focus in this section is on total return swaps where the reference asset is one of the first four types listed above. We first explain how a total return swap can be used when the reference asset is a credit-risky bond and a loan. While these types of total return swaps are more aptly referred to as total return credit swaps, we will simply refer to them as total return swaps. When the bond index consists of a credit risk sector of the bond market, the total return swap is referred to as a total return bond index swap or in this chapter as simply a total return index swap. We will explain how a total return index swap offers asset managers and hedge fund managers increased flexibility in managing a bond portfolio. In the appendix to this chapter we explain the pricing of total return swaps.

ECONOMICS OF A TOTAL RETURN SWAP

The total return on a reference asset includes all cash flows as well as the capital appreciation or depreciation of that reference asset. The floating rate is a reference interest rate (typically LIBOR) plus or minus a spread. The party that agrees to make the floating rate payments and receive the total return is referred to as the total return receiver or the swap buyer; the party that agrees to receive the floating rate payments and pay the total return is referred to as the total return payer or swap seller. Total return swaps are viewed as unfunded credit derivatives, because there is no up-front payment required.

If the total return payer owns the underlying asset, it has transferred its economic exposure to the total return receiver. Effectively then, the total return payer has a neutral position that typically will earn LIBOR plus a spread. However, the total return payer has only transferred the economic exposure to the total return receiver; it has not transferred the actual asset. The total return payer must continue to fund the underlying asset at its marginal cost of borrowing or at the opportunity cost of investing elsewhere the capital tied up by the reference assets.

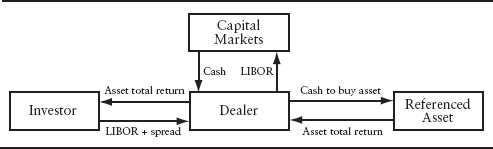

The total return payer may not initially own the reference asset before the swap is transacted. Instead, after the swap is negotiated, the total return payer will purchase the reference asset to hedge its obligations to pay the total return to the total return receiver. In order to purchase the reference asset, the total return payer must borrow capital. This borrowing cost is factored into the floating rate that the total return receiver must pay to the swap seller. Exhibit 3.1 diagrams how a total return credit swap works.

In the exhibit the dealer raises cash from the capital markets at a funding cost of straight LIBOR. The cash that flows into the dealer from the capital markets flows right out again to purchase the reference asset. The asset provides both interest income and capital gain or loss depending on its price fluctuation. This total return is passed through in its entirety to the investor according to the terms of the total return swap. The investor, in turn, pays the dealer LIBOR plus a spread to fulfill its obligations under the swap.

From the dealer's perspective, all of the cash flows in Exhibit 3.1 net out to the spread over LIBOR that the dealer receives from the investor. Therefore, the dealer's profit is the spread times the notional amount of the total return swap. Furthermore, the dealer is perfectly hedged. It has no risk position except for the counterparty risk of the investor. Effectively, the dealer receives a spread on a riskless position.

In fact, if the dealer already owns the reference asset on its balance sheet, the total return swap may be viewed as a form of credit protection that offers more risk reduction than a credit default swap. A credit default swap has only one purpose: to protect the investor against default risk. If the issuer of the reference asset defaults, the credit default swap provides a payment. However, if the underlying asset declines in value but no default occurs, the credit protection buyer receives no payment. In contrast, under a total return swap, the reference asset owned by the dealer is protected from declines in value. In effect, the investor acts as a “first loss” position for the dealer because any decline in value of the reference asset must be reimbursed by the investor.

The investor, on the other hand, receives the total return on a desired asset in a convenient format. There are several other benefits in using a total return swap as opposed to purchasing a reference asset itself. First, the total return receiver does not have to finance the purchase of the reference asset itself. Instead, the total return receiver pays a fee to the total return payer in return for receiving the total return on the reference asset. Second, the investor can take advantage of the dealer's “best execution” in acquiring the reference asset. Third, the total return receiver can achieve the same economic exposure to a diversified basket of assets in one swap transaction that would otherwise take several cash market transactions to achieve. In this way a total return swap is much more efficient means for transacting than the cash market is. Finally, an investor who wants to short a credit-risky asset such as a corporate bond will find it difficult to do so in the market. An investor can do so efficiently by using a total return swap. In this case the investor will use a total return swap in which it is a total return payer.

EXHIBIT 3.1 Total Return Swaps

There is a drawback of a total return swap if an asset manager employs it to obtain credit protection. In a total return swap, the total return receiver is exposed to both credit risk and interest rate risk. For example, the credit spread can decline (resulting in a favorable price movement for the reference asset), but this gain can be offset by a decline in the price of the reference asset resulting from a rise in the level of interest rates.

Total Return Swap Compared to an Interest Rate Swap

It is worthwhile comparing market conventions for a total return swap to those of an interest rate swap. A plain vanilla or generic interest rate swap involves the exchange of a fixed-rate payment for a floating-rate payment. A basis swap is a special type of interest rate swap in which both parties exchange floating-rate payments based on different reference interest rates. For example, one party's payments may be based on 3-month LIBOR, while the other party's payments are based on the 6-month Treasury rate. In a total return swap, both parties pay a floating rate.

The quotation conventions for a generic interest rate swap and a total return swap differ. In a generic interest rate swap, the fixed-rate payer pays a spread to a Treasury security with the same tenor as the swap (i.e., the swap spread) and the fixed-rate receiver pays the reference rate flat (i.e., no spread or margin). The payment by the fixed-rate receiver (i.e., floating-rate payer) is referred to as the funding leg. For example, suppose an interest rate swap quote for the swap spread of a 5-year, 3-month, LIBOR-based swap is 50 bp. This means that the fixed-rate payer agrees to pay the 5-year Treasury rate that exists at the inception of the swap plus 50 bp and the fixed-rate receiver agrees to pay 3-month LIBOR. In contrast, the quote convention for a total return swap is that the total return receiver receives the total return flat and pays the total return payer an interest rate based on a reference rate (typically LIBOR) plus or minus a spread. That is, the funding leg (i.e., what the total return receiver pays) includes a spread.

Illustration

Let's illustrate a total return swap where the reference asset is a corporate bond. Consider an asset manager who believes that the fortunes of XYZ Corporation will improve over the next year so that the company's credit spread relative to U.S. Treasury securities will decline. The company has issued a 10-year bond at par with a coupon rate of 9% and therefore the yield is 9%. Suppose at the time of issuance, the 10-year Treasury yield is 6.2%. This means that the credit spread is 280 bp and the asset manager believes it will decrease over the year to less than 280 bp.

The asset manager can express this view by entering into a total return swap that matures in one year as a total return receiver with the reference asset being the 10-year, 9% XYZ Corporation bond issue. For simplicity, assume that the total return swap calls for an exchange of payments semiannually. Suppose the terms of the swap are that the total return receiver pays the 6-month Treasury rate plus 160 bp in order to receive the total return on the reference asset. The notional amount for the contract is $10 million.

Suppose that over the course of the swap's 1-year term the following occurs:

- The 6-month Treasury rate for computing the first semiannual payment is 4.8%.

- The 6-month Treasury rate for computing the second semiannual payment is 5.4%.

- At the end of one year the 9-year Treasury rate is 7.6%.

- At the end of one year the credit spread for the reference asset is 180 bp.

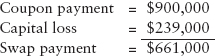

First let's look at the payments that must be made by the asset manager. The first swap payment made by the asset manager is 3.2% (4.8% plus 160 bp divided by two) multiplied by the $10 million notional amount. The second swap payment made is 3.5% (5.4% plus 160 bp divided by two) multiplied by the $10 million notional amount. Thus,

The payments that will be received by the asset manager are the two coupon payments plus the change in the value of the reference asset. There will be two coupon payments. Since the coupon rate is 9% the amount received for the coupon payments is $900,000.

Finally, the change in the value of the reference asset must be determined. At the end of one year, the reference asset has a maturity of nine years. Since the 9-year Treasury rate is assumed to be 7.6% and the credit spread is assumed to decline from 280 bp to 180 bp, the reference asset will sell to yield 9.4%. The price of a 9%, 9-year bond selling to yield 9.4% is 97.61. Since the par value is $10 million, the price is $9,761,000. The capital loss is therefore $239,000. The payment to the total return receiver is then:

Netting the swap payment made and the swap payment received, the asset manager must make a payment of $9,000 ($661,000 − $670,000).

Notice that even though the asset manager's expectations were realized (i.e., a decline in the credit spread), the asset manager had to make a net outlay. This illustration highlights one of the disadvantages of a total return swap noted earlier: The return to the investor is dependent on both credit risk (declining or increasing credit spreads) and market risk (declining or increasing market rates). Two types of market interest rate risk can affect the price of a fixed-income asset. Credit independent market risk is the risk that the general level of interest rates will change over the term of the swap. This type of risk has nothing to do with the credit deterioration of the reference asset. Credit dependent market interest rate risk is the risk that the discount rate applied to the value of an asset will change based on either perceived or actual default risk.

In the illustration, the reference asset was adversely affected by market interest rate risk, but positively rewarded for accepting credit dependent market interest rate risk. To remedy this problem, a total return receiver can customize the total return swap transaction. For example, the asset manager could negotiate to receive the coupon income on the reference asset plus any change in value due to changes in the credit spread. Now the asset manager has expressed a view exclusively on credit risk; credit independent market risk does not affect the swap value. In this case, in addition to the coupon income, the asset manager would receive the difference between the present value of the reference asset at a current spread of 280 bp and the present value of the reference asset at a credit spread of 180 bp.

Total Return Index Swaps

Thus far our focus has been on a single reference asset. Total return index swaps are swaps where the reference asset is the return on a market index. The market index can be an equity index or a bond index. Our focus will be on bond indexes.

Broad-based bond market indexes such as the Lehman, Salomon Smith Barney, and Merrill Lynch indexes have subindexes that represent major sectors of the bond market. For example, there is the Treasury and agency sector, the credit sector (i.e., investment-grade corporate bonds, at one time referred to as the corporate sector), the mortgage sector (consisting of agency residential mortgage-backed securities), the commercial mortgage-backed securities (CMBS) sector, and the asset-backed securities (ABS) sector. The non-Treasury sectors offer a spread to Treasuries and are hence referred to as “spread sectors.” The spread in the mortgage sector is primarily compensation for the prepayment risk associated with investing in this sector. Spread to compensate for credit risk is offered in the credit spread sector, of course, and the CMBS and ABS sectors. There are also indexes available for other credit spread sectors of the bond market such as the high-yield corporate bond sector and the emerging market bond sector. Thus, a total return index swap in which the underlying index is a credit spread sector allows an asset manager to gain or reduce exposure to that sector.

1 British Bankers Association, Credit Derivatives Report 2003/2004.

2 For a further discussion of credit default swaps, see Chapter 3 in Mark J. P. Anson, Frank J. Fabozzi, Moorad Choudhry, and Ren-Raw Chen, Credit Derivatives: Instruments, Applications, and Pricing (Hoboken, NJ: John Wiley & Sons, 2003).

3 While we did not cover Treasury bond and note futures contracts because they are not prevalent in structured financial transaction, the notion of a cheapest-to-deliver issue exists in that market because the short has the choice of which Treasury issue to deliver among the issues that the exchange specifies as acceptable for delivery.

4 The illustration and discussion in this section draws from “Nth to Default Swaps and Notes: All About Default Correlation,” CDO Insight (May 30, 2003) UBS Warburg.