CHAPTER 9

Credit-Linked Notes

Credit derivatives are grouped into funded and unfunded variants. In an unfunded credit derivative, typified by a credit default swap, the protection seller does not make an upfront payment to the protection buyer. In a funded credit derivative, typified by a credit-linked note (CLN), the investor in the note is the credit protection seller and is making an upfront payment to the protection buyer when buying the note. Thus, the protection buyer is the issuer of the note. If no credit event occurs during the life of the note, the redemption value of the note is paid to the investor on maturity. If a credit event does occur, then on maturity a value less than par will be paid out to the investor. This value will be reduced by the nominal value of the reference asset to which the CLN is linked. In this chapter, we discuss CLNs.

DESCRIPTION OF CLNS

Credit-linked notes exist in a number of forms, but all of them contain a link between the return they pay and the credit-related performance of the underlying asset. A standard CLN is a security, usually issued by an investment-grade-rated entity, that has an interest payment and fixed maturity structure similar to a vanilla bond. The performance of the CLN, however, including the maturity value, is linked to the performance of a specified underlying asset or assets as well as that of the issuing entity. CLNs are usually issued at par. They are often used as a financing vehicle by borrowers in order to hedge against credit risk; CLNs are purchased by investors to enhance the yield received on their holdings. Hence, the issuer of the CLN is the protection buyer and the buyer of the note is the protection seller.

Essentially CLNs are hybrid instruments that combine a pure credit risk exposure with a vanilla bond. The CLN pays regular coupons; however the credit derivative element is usually set to allow the issuer to decrease the principal amount, and/or the coupon interest, if a specified credit event occurs.

ILLUSTRATION OF A CLN

To illustrate a CLN, consider a bank issuer of credit cards that wants to fund its credit card loan portfolio via an issue of debt. The bank is rated AA-. In order to reduce the credit risk of the loans, it issues a two-year CLN. The principal amount of the bond is 100 (par) as usual, and it pays a coupon of 7.50%, which is 200 bp above the 2-year benchmark. The equivalent spread for a vanilla bond issued by a bank of this rating would be of the order of 120 bp. With the CLN though, if the incidence of bad debt among credit card holders exceeds 10% then the terms state that note holders will only receive back 85 per 100 par. The credit card issuer has in effect purchased a credit option that lowers its liability in the event that it suffers from a specified credit event, which in this case is an above-expected incidence of bad debts. The cost of this credit option to the credit protection buyer is paid in the form of a higher-coupon payment on the CLN. The credit card bank has issued the CLN to reduce its credit exposure, in the form of this particular type of credit insurance. If the incidence of bad debts is low, the CLN is redeemed at par. However, if there a high incidence of such debt, the bank will only have to repay a part of its loan liability.

INVESTOR MOTIVATION

Investors may wish purchase the CLN because the coupon paid on it will be above what the credit card bank would pay on a vanilla bond it issued, and higher than other comparable investments in the market. In addition such notes are usually priced below par on issue. Assuming the notes are eventually redeemed at par, investors will also realize a substantial capital gain.

SETTLEMENT

As with credit default swaps, CLNs may be cash settled or physically settled. However, there are differences associated with the funded nature of CLNs and also with the specific type of CLN that is being considered.

The true credit derivative CLN is a note issued by one party that references another party as the credit reference name. But certain bonds have been labeled as “CLNs” despite being issued by the same companies that are the credit references. For these bonds, the occurrence of a credit event signifies immediate termination of the bond. However, there is no settlement process as such because the protection seller is already holding the bond. In this respect, such CLNs are more akin to vanilla cash bonds of the same issuer.1

For true CLNs, the settlement process is similar to that for CDS contracts. Consider a CLN issued by ABC Securities that references XYZ Automotive plc. Specifically:

- Under cash settlement, upon occurrence of a credit event the note is terminated. The protection buyer will pay the default value, or recovery value (RR), of the reference name to the protection seller. This is equivalent to the [100 – RR] payout under a CDS contract.

- Under physical settlement, upon occurrence of a credit event the note is terminated. The protection buyer will deliver a XYZ Automotive plc bond—out of a deliverable basket of XYZ bonds—to the protection seller. The protection seller of course retains the original CLN bond, issued by ABC Securities.

Note that the protection buyer may well be ABC Securities, but does not have to be.

The value of the reference asset at the time of the credit event determines the payout under the terms of the CLN. This is known as the recovery value. In practice, a process of administration must be undertaken, in some cases lasting years, before the ultimate recovery value for the various classes of debtors can be realized. To assist payout under a credit derivative contract, a third-party calculation agent may be appointed at the inception of the contract. The role of the calculation agent is to determine the market value of the defaulted reference asset at, or shortly after, the credit event has occurred, so that the CLN may be matured and the redemption proceeds calculated. This would apply under cash or physical settlement.

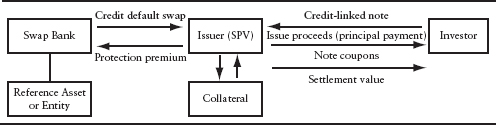

Exhibit 9.1 illustrates a cash-settled CLN.

EXHIBIT 9.1 Credit-Linked Note

FORMS OF CREDIT LINKING

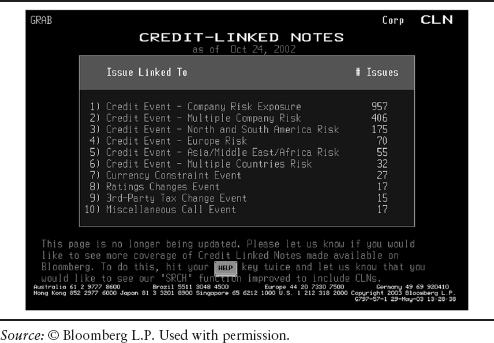

CLNs may be issued directly by a financial or corporate entity or via a special purpose vehicle (SPV). They have been issued with several different forms of credit-linking. For instance, a CLN may have its return performance linked to the issuer's, or a specified reference entity's, credit rating, risk exposure, financial performance or circumstance of default. Exhibit 9.2 shows a page from Bloomberg screen “CLN” with a list of the various types of CLN issue that have been made. Exhibit 9.3 shows another page accessed from Bloomberg screen CLN with a list of CLNs whose coupons have been affected by a change in the reference entity's credit rating.

EXHIBIT 9.2 Bloomberg Screen CLN

EXHIBIT 9.3 Bloomberg Screen Showing a Sample of CLNs Impacted by Change in Reference Entity Credit Rating, October 2002

Many CLNs are issued directly by banks and corporate borrowers in the same way as conventional bonds. An example of such a bond is shown at Exhibit 9.4. This shows Bloomberg screen DES for a CLN issued by British Telecom plc, the 8.125% note due in December 2010. The terms of this note state that the coupon will increase by 25 bp for each one-notch rating downgrade below A-/A3 suffered by the issuer during the life of the note. The coupon will decrease by 25 bp for each ratings upgrade, with a minimum coupon set at 8.125%. In other words, this note allows investors to take on a credit play on the fortunes of the issuer.

Exhibit 9.5 shows Bloomberg screen YA for this note as of May 29, 2003. We see that a rating downgrade meant that the coupon on the note was now 8.375%.

Exhibit 9.6 is the Bloomberg DES page for a U.S. dollar denominated CLN issued directly by Household Finance Corporation (HFC).2 Like the British Telecom bond, the return of this CLN is linked to the credit risk of the issuer, but in a different way. The coupon of the HFC bond was issued as floating USD-LIBOR, but the bond was not called by November 2001, the coupon would be the issuer's two-year “credit spread” over a fixed rate of 5.9%.3 In fact, the issuer called the bond with effect from the coupon change date. Exhibit 9.7 shows the Bloomberg screen YA for the bond and how its coupon remained as at first issue until the call date.

EXHIBIT 9.4 Bloomberg Screen DES for British Telecom plc 8.125% 2010 Credit-Linked Note Issued on December 5, 2000

EXHIBIT 9.5 Bloomberg Screen YA for British Telecom CLN, May 29, 2003

EXHIBIT 9.6 Bloomberg DES Screen for Household Finance Corporation CLN

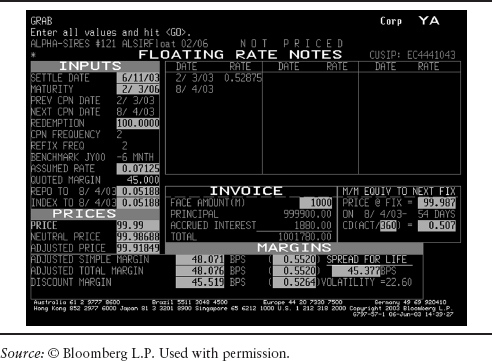

Another type of credit-linking is evidenced from Exhibit 9.8, the Ford CLN Bloomberg DES page. This is a Japanese-yen-denominated bond issued by Alpha-Spires, which is a medium-term note program vehicle (a SPV) set up by Merrill Lynch. The note itself is linked to the credit quality of Ford Motor Credit Co. In the event of a default of the reference name, the note will be called immediately. Exhibit 9.9 shows the rate fixing for this note as of the last coupon date. The screen snapshot was taken on June 6, 2003.

Structured products such as synthetic collateralized debt obligations (CDOs) described in Chapter 7 may combine both CLNs and credit default swaps to meet issuer and investor requirements. For instance, Exhibit 9.10 shows a credit structure designed to provide a higher return for an investor on comparable risk to the cash market. An issuing entity is set up in the form of a special purpose vehicle (SPV) that issues CLNs to the market. The structure is engineered so that the SPV has a neutral position on a reference asset. It has bought protection on a single reference name by issuing a funded credit derivative, the CLN, and simultaneously sold protection on this name by selling a credit default swap on this name. The proceeds of the CLN are invested in risk-free collateral such as Treasury bills or a Treasury bank account. The coupon on the CLN will be a spread over LIBOR. It is backed by the collateral account and the fee generated by the SPV in selling protection with the credit default swap. Investors in the CLN will have exposure to the reference asset or entity, and the repayment of the CLN is linked to the performance of the reference entity. If a credit event occurs, the maturity date of the CLN is brought forward and the note is settled as par minus the value of the reference asset or entity.

EXHIBIT 9.7 Bloomberg YA Screen for Household Finance Corporation CLN, June 6, 2003

EXHIBIT 9.8 Bloomberg DES Screen for Ford CLN

EXHIBIT 9.9 Bloomberg YA Screen for Ford CLN, June 6, 2003

EXHIBIT 9.10 CLN and Credit Default Swap Structure on Single Reference Name

THE FIRST-TO-DEFAULT CREDIT-LINKED NOTE

A standard CLN is issued in reference to one specific bond or loan. An investor purchasing such a note is writing credit protection on a specific reference credit. A CLN that is linked to more than one reference credit is known as a basket credit-linked note. A development of the CLN as a structured product is the First-to-Default CLN (FtD), which is a CLN that is linked to a basket of reference assets. The investor in the CLN is selling protection on the first credit to default.4 Exhibit 9.11 shows this progression in the development of CLNs as structured products, with the fully funded synthetic CDO, described in Chapter 7, being the vehicle that uses CLNs tied to a large basket of reference assets.

EXHIBIT 9.11 Progression of CLN Development

An FtD CLN is a funded credit derivative in which the investor sells protection on one reference in a basket of assets, whichever is the first to default. The return on the CLN is a multiple of the average spread of the basket. The CLN will mature early on occurrence of a credit event relating to any of the reference assets. Settlement on the CLN can be either of the following:

- Physical settlement, with the defaulted asset(s) being delivered to the noteholder.

- Cash settlement, in which the CLN issuer pays redemption proceeds to the noteholder calculated as:

Principal amount × Reference asset recovery value

In practice, it is not the “recovery value” that is used but the market value of the reference asset at the time the credit event is verified. Recovery of a defaulted asset follows a legal process of administration and/or liquidation that can take some years, and so the final recovery value may not be known with certainty for some time. Because the computation of recovery value is so difficult, holders of a CLN may prefer physical settlement where they take delivery of the defaulted asset.

Exhibit 9.12 shows a generic FtD credit-linked note.

To illustrate, consider an FtD CLN issued at par, with a term-to-maturity of five years, that is linked to a basket of five reference assets with a face value (issued nominal amount) of $10 million. An investor purchasing this note will pay $10 million to the issuer. If no credit event occurs during the life of the note, the investor will receive the face value of the note on maturity. If a credit event occurs on any of the assets in the basket, the note will redeem early and the issuer will deliver a deliverable obligation of the reference entity, or a portfolio of such obligations, for a $10 million nominal amount. An FtD CLN carries a similar amount of risk exposure on default to a standard CLN, namely the recovery rate of the defaulted credit. However, its risk exposure prior to default is theoretically lower than a standard CLN, as it can reduce default probability through diversification. The investor can obtain exposure to a basket of reference entities that differ by industrial sector and by credit rating.

EXHIBIT 9.12 First-to-Default CLN Structure

EXHIBIT 9.13 Diversified Credit Exposure to Basket of Reference Assets: Hypothetical Reference Asset Mix

The matrix shown in Exhibit 9.13 illustrates how an investor can select a credit mix in the basket that diversifies risk exposure across a wide range; we show a hypothetical mix of reference assets to which an issued FtD could be linked. The precise selection of names will reflect an investor's own risk/return profile requirements.

The FtD CLN creates a synthetic credit entity that features a note return with enhanced spread. Investors receive a spread over LIBOR that is the average return of all the reference assets in the basket. This structure serves to diversify credit risk exposure while benefiting from a higher average return. If the pool of reference assets is sufficiently large, the structure becomes similar to a single-tranche CDO. This is discussed in Chapter 6.

1 The reason such bonds are termed “CLNs” is that their payoff is linked to a credit-related performance of the issuer such as a change in the credit rating.

2 HFC was subsequently acquired by HSBC.

3 Exactly how to calculate the credit spread would be specified in the CLN issue's offering circular. For example, it could be the difference between current LIBOR and the current yield on one of HFC's other bond issues or the average of current yields on several of its other issues.

4 “Default” here meaning a credit event as defined in the ISDA definitions.