CHAPTER 12

Leveraged Lease Fundamentals

The leveraged form of a true lease of equipment is the ultimate form of lease financing. It allows a company, as lessee, to harness the lessor's capital, leveraged by institutional debt, as a source of funding somewhat like subordinated debt. The most attractive feature of a leveraged lease, from the standpoint of a lessee unable to use tax benefits of MACRS (Modified Accelerated Cost Recovery System), is its low cost as compared to that of alternative methods of financing. Leveraged leasing also satisfies a need for lease financing of especially large capital equipment projects with economic lives of up to 25 or more years, although leveraged leases are also used where the life of the equipment is considerably shorter. The leveraged lease can be a most advantageous financing device when used for the right kinds of projects and structured correctly.

Single-investor nonleveraged leases of equipment are simple two-party transactions involving a lessee and a lessor. In single-investor leases (sometimes called nonleveraged leases or direct leases), the lessor provides all of the funds necessary to purchase the leased asset from its own resources. While the lessor may borrow some or all of these funds, it does so on a full-recourse basis to its lenders, and it is at risk for all of the capital employed.1

A leveraged lease of equipment is conceptually similar to a single-investor lease. The lessee selects the equipment and negotiates the lease in much the same manner. Also, the terms for rentals, options, and responsibility for taxes, insurance, and maintenance are similar. However, a leveraged lease is appreciably more complex in size, documentation, legal involvement, and, most importantly, the number of parties involved and the unique advantages that each party gains.

Leveraged leases of equipment are generally offered only by corporations and financial institutions acting as lessors. This is because in a leveraged lease the tax benefits available to individual lessors are much more limited than those available to a corporation. This chapter is devoted to leveraged leases offered by corporations and financial institutions.

The lessor in a leveraged lease of equipment becomes the owner of the leased equipment by providing only a percentage (20% to 30%) of the capital necessary to purchase the equipment.2 The remainder of the capital (70% to 80%) is borrowed from institutional investors on a nonrecourse basis to the lessor. This loan is secured by a first lien on the equipment, an assignment of the lease, and an assignment of the lease rental payments. The cost of the nonrecourse borrowing is a function of the credit standing of the lessee.3 The lease rate varies with the debt rate and with the risk of the transaction.

A “leveraged lease” is always a true lease. The lessor in a leveraged lease can claim all of the tax benefits incidental to ownership of the leased asset even though the lessor provides only 20% to 30% of the capital needed to purchase the equipment. This ability to claim the MACRS tax benefits attributable to the entire cost of the leased equipment and the right to 100% of the residual value provided by the lease, while providing and being at risk for only a portion of the cost of the leased equipment, is the “leverage” in a leveraged lease. Such leverage enables the lessor in a leveraged lease to offer the lessee much lower lease rates than the lessor could provide under a direct lease.

The legal expenses and closing costs associated with leveraged leases are larger than those for single-investor nonleveraged leases and usually confine the use of leveraged leases to financing relatively large capital equipment acquisitions. However, leveraged leases are also used for smaller lease transactions that are repetitive in nature and use standardized documentation so as to hold down legal and closing costs.

Several parties may be involved in a leveraged lease. Whereas direct or single-investor nonleveraged leases are basically two-party transactions with a lessee and a lessor, leveraged leases by their nature involve a minimum of three parties with diverse interests: a lessee, a lessor, and a nonrecourse lender. Indeed, leveraged leases are sometimes called three-party transactions.

Several owners and lenders may be involved in a large leveraged lease. In such a case, an owner trustee is generally named to hold title to the equipment and represent the owners or equity participants, and an indenture trustee is usually named to hold the security interest or mortgage on the property for the benefit of the lenders or loan participants. Sometimes a single trustee may be appointed to perform both of these functions.

In this chapter we will review the rights, obligations, functions, and characteristics of the various parties that may be involved with a leveraged lease; the structure; the cash flows; and the debt arrangements possible.4

PARTIES TO A LEVERAGED LEASE

The parties to a leveraged lease include:

- the lessee;

- equity participants;

- loan participants or lenders;

- owner trustee;

- indenture trustee;

- manufacturer or contractor;

- packager; and

- guarantor.

We discuss each in the following subsections.

The Lessee

The lessee selects the equipment to be leased, negotiates the price and warranties, and hires the use of the equipment by entering into a lease agreement. The lessee accepts, uses, operates, and receives all revenue from the equipment. The lessee makes rental payments. The credit standing of the lessee supports the rent obligation, the credit exposure of the lenders of leveraged debt, and the credit exposure of the equity participants.

Equity Participants

The equity participants provide the equity contributions (20% to 30% of the purchase price) needed to purchase the leased equipment. They receive the rental payments remaining after the payment of debt service and any trustee fees. They claim the tax benefits incidental to the ownership of the leased equipment, consisting of MACRS tax depreciation deductions and deductions for interest used to fund their investment. They are entitled to receive the residual value of the equipment at the end of the lease subject to limitations provided by the lease agreement. The equity participants are sometimes referred to as the lessors. Actually, in most cases they are the beneficial owners by way of an owner trust that is the lessor. Equity participants are also sometimes referred to as equity investors, owner participants, or trustors.

Loan Participants or Lenders

The loan participants or lenders are typically banks, finance companies, insurance companies, trusts, pension funds, and foundations. The funds provided by the loan participants, together with the equity contributions, make up the full purchase price of the asset to be leased. The loan participants provide 70% to 80% of the purchase price on a nonrecourse basis to the equity participants. As noted earlier, these loans are secured by a first lien on the leased equipment, an assignment of the lease, an assignment of rents under the lease, and an assignment of any ancillary agreements such as easements and supply contracts. Principal and interest payments that are due the loan participants (or lenders) from the indenture trustee are paid by the lessee to the indenture trustee, which then pays the loan participants.

Owner Trustee

The owner trustee represents the equity participants, acts as the lessor, and executes the lease and all of the basic documents that the lessor would normally sign in a lease. The owner trustee records and holds title to the leased asset for the benefit of the equity participants, subject to the mortgage or security agreement to the indenture trustee. The owner trustee issues trust certificates to the equity holders evidencing their beneficial interest as owners of the assets of the trust, issues bonds or notes to loan participants evidencing the leveraged debt, grants to the indenture trustee the security interests that secure repayment of the bonds (that is, the lease, the lease rentals, and a first mortgage on the leased asset), receives distributions from the indenture trustee, distributes earnings to the equity participants, and receives and distributes any information or notices regarding the transaction that are required to be provided to the parties. The owner trustee has little discretionary power beyond that specifically granted in the trust agreement and has no affirmative duties.

The owner participants indemnify the owner trustee against costs and liabilities arising out of the transaction, except for willful misconduct or negligence. It can be argued that an owner trustee is unnecessary. Where a leveraged lease has a single equity investor, the parties may conclude that an owner trustee is not needed and that the equity investor may act as the lessor. However, the cost of an owner-trustee for a leveraged lease is usually modest compared with the benefits unless the transaction is extremely simple and straightforward.

Indenture Trustee

The indenture trustee (sometimes called the security trustee) is appointed by and represents the lenders or loan participants. The owner trustee and the indenture trustee enter into a trust indenture whereby the owner trustee assigns to the indenture trustee, for the benefit of the loan participants and as security for the leveraged debt and any other obligations, all of the owner trustee's interest as lessor in:

- the equipment to be leased and the lessor's rights under manufacturer's or contractor's warranties related to the equipment;

- the lease agreement;

- the lessor's right to receive rents (including all payments) owed by the lessee (subject to such exceptions as agreed between the lessor and lessee);

- the lessor's rights to receive any payments under any guarantee agreements (subject to the same exceptions as the payments due the lessor); and

- the lessor's rights under any ancillary facility support agreements such as easements, service contracts, supply contracts, and sales contracts.

The indenture agreement sets forth the form of the notes or loan agreements, the events of default, and the instructions and priorities for distributions of funds to the loan participants and other parties.

The indenture trustee receives funds from the loan participants (lenders) and the equity participants when the transaction is about to close, pays the manufacturer or contractor the purchase price of the equipment to be leased, and records and holds the senior security interest in the leased equipment, the lease, any ancillary facility support contracts, and the rents for the benefit of the loan participants. The indenture trustee collects rents and other sums due under the lease from the lessee. Upon the receipt of rental payments, the indenture trustee pays debt payments of principal and interest due on the leveraged debt to the loan participants and distributes revenues not needed for debt service to the owner trustee. In the event of default, the indenture trustee can foreclose on the leased equipment and take other appropriate actions to protect the security interests of the loan participants.5

Manufacturer or Contractor

The manufacturer or contractor manufactures or constructs the equipment to be leased. The manufacturer or contractor (or supplier) receives the purchase price upon acceptance of the equipment by the lessee and delivers the equipment to the lessee at the beginning of the lease. The warranties of the manufacturer, contractor, or supplier as to the quality, capabilities, and efficiencies of the leased equipment are important to the lessee, the equity participants, and the loan participants.

Packager or Broker

The packager or broker is the leasing company arranging the transaction. In many instances, the packager is purely a broker and not an investor. From the standpoint of the lessee, it may be desirable that the packager also be an equity participant. The packager may, in fact, be the sole equity participant.

Guarantor

A guarantor of the lessee's credit may be present in some leveraged lease transactions. Although a member of the lessee group may not guarantee the leveraged debt under Internal Revenue rules, a member of the lessee group may guarantee the lessee's obligation to pay rent. A party unrelated to the lessee may guarantee either rents or debt. Such a guarantor might be a third party such as a bank under a letter of credit agreement, an insurer of residual value, or a government guarantor.6

STRUCTURE OF A LEVERAGED LEASE

A leveraged lease transaction is usually structured as follows where a broker or a third-party leasing company arranges the transaction.

The leasing company arranging the lease, “the packager,” enters into a commitment letter with the prospective lessee (obtains a mandate) that outlines the terms for the lease of the equipment, including the timing and amount of rental payments. Since the exact rental payment cannot be determined until the debt has been sold and the equipment delivered, rents are agreed tentatively based on certain variables, including assumed debt rates and the delivery dates of the equipment to be leased.

After the commitment letter has been signed, the packager prepares a summary of terms for the proposed lease and contacts potential equity participants to arrange for firm commitments to invest equity in the proposed lease to the extent that the packager does not intend to provide the total amount of the required equity funds from its own resources. Contacts with potential equity sources may be fairly informal or may be accomplished through a bidding process. Typical equity participants include banks, independent finance companies, captive finance companies, and corporate investors that have tax liability to shelter, have funds to invest, and understand the economics of tax-oriented leasing. The packager may also arrange the debt either directly or in conjunction with the capital markets group of a bank or an investment banker selected by the lessee or the lessor. If the equipment is not to be delivered and the lease is not to commence for a considerable period of time, the debt arrangements may be deferred until close to the date of delivery.

The packager may agree at the outset to “bid firm” or underwrite the transaction on the mandated terms and may then “syndicate” its bid to potential equity participants. However, the lessee may prefer to use a bidding procedure without an underwritten price on the theory that more favorable terms can be arranged using this approach.

In some instances, the lessee may prefer to prepare its own bid request and solicit bids directly from potential lessors without using a packager or broker to underwrite or arrange the transaction. This might be the case, for example, where the lessee has considerable experience in leveraged leasing and has already arranged leases of similar equipment, such as computers or computer systems.

If an owner trustee is to be used, a bank or trust company mutually agreeable to the equity participants and the lessee is selected to act as owner trustee. If an indenture trustee is to be used, another bank or trust company acceptable to the loan participants is selected to act as indenture trustee. As discussed previously, a single trustee may act as both owner trustee and indenture trustee.

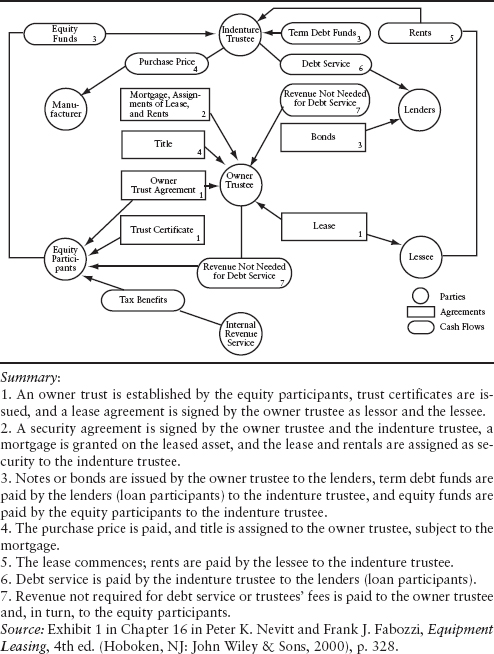

Exhibit 12.1 illustrates the parties, cash flows, and agreements among the parties in a simple leveraged lease.

If the leveraged lease is arranged by sponsors of a project who want to be the equity participants, the structure and procedures are essentially the same as those for a leveraged lease by a third-party equity participant. In such circumstances, the sponsors are the equity investors. If some of the sponsors can use tax benefits and some cannot, the equity participants may include a combination of sponsors and one or more third-party leasing companies. This arrangement is more complex, but the structure and procedures are essentially the same as those for a leveraged lease by a third-party equity participant.

EXHIBIT 12.1 Leveraged Lease

CLOSING THE TRANSACTION

Participation Agreement

The key document in a leveraged lease transaction is the participation agreement (sometimes called the financing agreement). This document is, in effect, a script for closing the transaction.

When the parties to a leveraged lease transaction are identified, all of them except the indenture trustee enter into a participation agreement that spells out in detail the various undertakings, obligations, mechanics, timing, conditions precedent, and responsibilities of the parties with respect to providing funds and purchasing, leasing, and securing or mortgaging the equipment to be leased. More specifically, the equity participants agree to provide their investment or equity contribution; the loan participants agree to make their loans; the owner trustee agrees to purchase and lease the equipment; and the lessee agrees to lease the equipment. The substance of the required opinions of counsel is described in the participation agreement. The representations of the parties are detailed. Tax indemnities and other general indemnities are often set forth in the participation agreement rather than the lease agreement. The exact form of agreements to be signed, the opinions to be given, and the representations to be made by the parties are usually attached as exhibits to the participation agreement.

Other Key Documents

The key documents in a leveraged lease transaction in addition to the participation agreement are: the lease agreement, the owner trust agreement, and the indenture trust agreement.

The lease agreement is between the lessee and owner trustee. The lease is for a term of years and may contain renewal options and fair-market-value purchase options. Rents and all payments due under the lease are net to the lessor, and the lessee waives defenses and offsets to rents under a “hell or high water clause.”

The owner trust agreement creates the owner trust and sets forth the relationships between the owner trustee and the equity participants that it represents. The owner trust agreement spells out the duties of the trustee, the documents the trustee is to execute, and the distribution to be made of funds it receives from equity participants, lenders, and the lessee. The owner trustee has little or no authority to take discretionary or independent action.

The owner trust grants a lien or security interest on the leased equipment and assigns the lease agreement, any ancillary facility support agreements and right to receive rents under the lease to the indenture trustee (which may also be the owner trustee). It spells out the obligations of the indenture trustee to the lenders.

Indemnities by the Lessee

Lessee indemnities fall into three general categories:

- A general indemnity that protects all of the other parties to the transaction from any claims of third parties arising from the lease or the use of the leased equipment.

- A general tax indemnity that protects all of the other parties to the transaction from all federal, state, or local taxes arising out of or in connection with the transaction except for certain income tax or income-related taxes.

- Special tax indemnities by the lessee that protect the owner participants from the loss of expected income tax benefits as a result of the acts and omissions of the lessee and certain other events.

The coverage of the special tax indemnities beyond the acts and omissions of the lessee is a matter of significant negotiation between the lessee and lessor.

CASH FLOWS DURING THE LEASE

The equity participants receive cash flow from three sources: rents after the payment of debt service and trustee fees, tax benefits, and proceeds from the sale of the equipment at the conclusion of the lease.

The lessee pays periodic rents to the indenture trustee, which uses such funds to pay currently due principal and interest payments to the loan participants and to pay trustee fees for its services. The balance of the rental payments is paid to the owner trustee. After the payment of any trustee fees due the owner trustee and any administrative or other expenses, the owner trustee pays the remainder of the rental payments to the equity participants.

The equity participants also realize cash flow from tax benefits as quickly as they can claim such benefits on their quarterly tax estimates and tax returns.

The leveraged debt is usually amortized over a period of time identical to the lease term, with payments of principal and interest due on or shortly after the due date of the rental payments. These payments may be monthly, quarterly, semiannual, or annual. Where “optimized debt” structures are used for competitive reasons, the rental payments approximately equal the debt service payments plus deferred income tax. This has the effect of reducing the leveraged debt payments in the later years of the lease. Rental payments are usually level but may vary upward or downward (sawtooth rents) to achieve a maximum yield for the lessor.7 Also, debt payments may be concluded entirely before the lease term ends in order to generate additional cash for the lessor.

When the lease terminates, the equipment is returned to the owner trustee, who sells or releases the property at the direction of the owner participants.

The lease agreement usually requires the lessee to furnish the owner trustee and the indenture trustee with financial statements, evidence of insurance, and other similar information. The trustees distribute this information to all parties to the transaction.

DEBT FOR LEVERAGED LEASES

Debt for leveraged leases is usually at a fixed rate of interest although it also may be at a floating rate of interest. Such debt is available from a variety of sources. The lead equity source or packager may arrange the debt. Sometimes the lessee may prefer to have the debt arranged by its commercial bank, the capital markets group of its commercial bank, or its investment bank. Most leveraged lease debt is raised in the private placement market at little or no premium over what the lessee would expect to pay directly for such debt. The sources include:

- Insurance companies;

- Pension plans;

- Profit-sharing plans;

- Commercial banks;

- Finance companies;

- Savings banks;

- Domestic leasing companies;

- Foreign banks;

- Foreign leasing companies;

- Foreign investors; and

- Institutional investors.

Other less frequently used instruments and sources of debt that may be useful in special circumstances include the following:

Commercial Paper Investors. Commercial paper has sometimes been used for leveraged debt for short (five to seven years) leveraged leases. The major risks in using commercial paper are the floating interest rates and the possible inability to roll over the commercial paper. Such debt may require a backup line of credit. Interest rate risk can be hedged to some extent by using caps, interest rate futures, or interest rate swaps.

Public Debt Markets. It is possible, but not very practical, to use the public debt markets for leveraged debt. Public debt is expensive since it must be underwritten by an investment banking firm and registered under the Securities Act. For these reasons, issuance of public debt is not economical in amounts less than $50 million. Also, amending the lease difficult is when public debt is used.

Government Financing. If government financing is available, it can sometimes be used as leveraged debt.

Supplier Financing. Supplier financing can be an excellent source of leveraged debt (shipyard financing for a ship, for example). U.S. Export-Import Bank financing offers such opportunities. One difficulty in using this source is matching the debt maturities to the lease maturities. Where the lease is for a longer term than that of the supplier financing, wraparound debt is difficult to arrange, particularly since the security interest of such debt usually must be subordinate to the supplier financing.

Multicurrency Financing. Where the lessee generates more than one currency from the sale of its product or service, it may prefer the leveraged debt to be in one or more matching currencies. Debt and rents can be arranged to satisfy this need. Currency swaps can be used to hedge the foreign exchange risk of foreign currency debt.

Bridge Financing. If interest rates on fixed long-term debt are, in the opinion of the lessee, unusually high, the lessee may arrange bridge financing on a floating-interest-rate basis with a view to refinancing term debt at a more favorable fixed-interest rate at a later time.

FACILITY LEASES

Leveraged leases have been used increasingly in recent years to finance the use of equipment that is impractical to move, such as electric generating plants, mining equipment, refineries, and chemical facilities.8 A series of facility support agreements are needed in order to provide the lessor with rights to the leased equipment upon the conclusion of the original lease.

The lessor will want either to own the land on which the facility is located or to have a leasehold interest in the land that is at least 20% longer than the base lease term and any fixed-rate renewal lease terms available to the lessee. The lessor will also want easement and access rights to the property on which the facility is located. If supply contracts for raw material, fuel, or energy are necessary for successful operation of the facility, these must be assigned by the lessee to the lessor at the conclusion of the initial lease. Rights-of-way for power lines, rail lines, pipelines, and roads may be necessary, as may access rights to adjoining port, rail, or pipeline facilities. The leased equipment facility may be part of a large complex of similar facilities in some cases, and in such a case where the lessor should have rights to service, fuel, energy, and so forth, shared in common with the other facilities owned by the lessee or other parties.

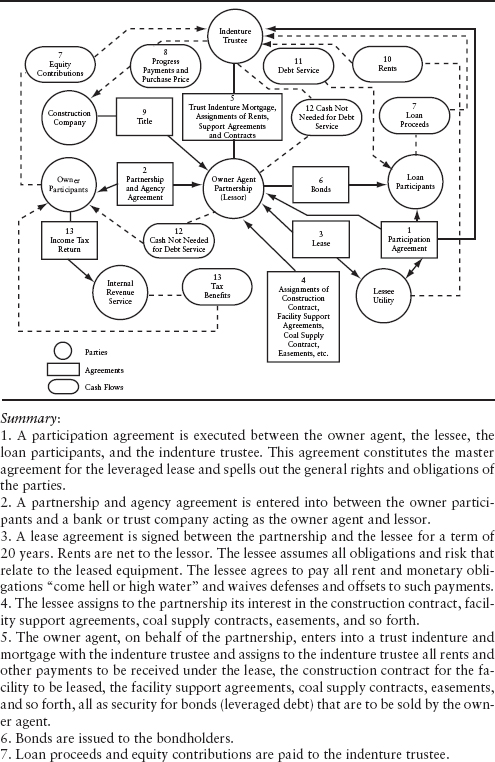

Exhibit 12.2 is a diagram of a leveraged lease of an electric coal-fired generating facility that illustrates the parties, the cash flows, and the agreements involved in a facility lease transaction in which the owner trustee takes title during construction. This transaction contemplates the assignment of the facility support agreements.

In this example, the purpose of the facility support agreements between the lessee and the owner trustee is to provide the owner trustee with access to all properties and things necessary or desirable to allow the owner trustee (acting on behalf of the equity participants) to operate the electric generating facility as an independent commercial electric generating unit and to sell electricity generated by the facility into a grid. The agreements stipulate that maintenance services, fuel supply, power transmission and/or distribution, and other things are to be provided by the lessee (for which the lessee will be reimbursed), while a third party is operating the facility on behalf of the lessor or on lease from the lessor. Without facility support agreements the assets of the project have little value as collateral. The facility support agreements are assigned to the indenture trustee as support for the leveraged debt. They remain in effect throughout the interim lease term, the base lease term, and any renewal lease terms, and for at least long enough thereafter to meet the useful-life tests of the Internal Revenue Service. Another purpose of the facility support agreements is to ensure that the facility will have value to someone other than the lessee at the end of the lease so as to satisfy the true-lease requirements of the Internal Revenue Service.

EXHIBIT 12.2 Leveraged Lease of an Electric Generating Facility

For example, the mere ownership of the facility by the owner trustee, without the underlying supply contracts for coal to be used as fuel for the facility, might seriously undermine the value of the facility for collateral security purposes and residual value purposes. To protect the interests of the equity participants and the loan participants, it is necessary for the lessee to assign to the owner trustee any coal supply contracts that might be advantageous or valuable to it. The owner trustee, in turn, assigns its interest in such contracts to the indenture trustee for the benefit of the loan participants. The supplier to the facility must consent to the assignment, and the form of consent is usually included as part of the coal supply agreement.

The participation agreement and the lease agreement (as in Exhibit 12.2) may contemplate that the title to the property to be leased will be transferred to the owner trustee (lessor) while the facility is still in early stages of construction. In this situation, the construction contract is assigned by the lessee to the owner trustee, and construction financing is arranged as described next.

Although the facility will usually be constructed by a third-party contractor, the utility may wish to supervise the performance of the construction contract by that contractor. In this situation, the lessee and the owner trustee enter into a construction supervision agreement. The purpose of this agreement is to arrange for and require the owner trustee to use the services of the utility in the capacity of construction supervisor to oversee the construction testing, delivery, and acceptance of the facility.

CONSTRUCTION FINANCING

In the usual leveraged lease transaction, the equity participants pay in their equity funds simultaneously with the receipt of leveraged debt funds from the loan participants at the closing, when the leased equipment is accepted by the lessee and the lease begins.

However, where the construction period extends over a considerable time the contractor may require progress payments during construction. In such a situation the parties may agree that the owner trust will take title to the facility during construction, so that the lease involves an interim lease term during construction that precedes the base lease term. Where this type of arrangement is made, the lessee, the owner trustee, and the construction lenders, who usually are not also to be loan participants during the base term lease, enter into a separate interim loan (construction loan) agreement. The lessor's equity investment and short-term construction loan financing is used until the completion of construction, acceptance by the lessee, draw-down of the long-term financing (leveraged debt), and commencement of the base lease term. The lessee pays interim rents to the owner trustee in an amount sufficient to cover interest on the construction loan and an adequate yield to the equity participants. In the alternative, construction loan interest may be capitalized into the cost of the facility and included in the total cost of the facility which is to be financed by the lease.

Construction financing is usually provided by commercial banks. Such financing is secured by an assignment of interim rents and by the lessee's obligation to pay off the principal of the loan if the long-term lenders fail to provide the financing or if the facility is not constructed or completed by a certain date. In such a situation, the equity participants will also look to the lessee's guarantee to recover their investments plus an adequate yield. All of the lessee's guarantees of construction loans are eliminated on or before completion and acceptance of the leased equipment and commencement of the base term of the lease. Eliminating lessee guarantees of the owner trust debt obligations is necessary in order to comply with the Internal Revenue guidelines.

CREDIT EXPOSURE OF EQUITY PARTICIPANTS

As noted earlier, equity participants realize their yields from the following sources:

- the interest rate spread between their yield on investment and their cost of funds;

- tax benefits from MACRS tax depreciation deductions; and

- the residual value of the equipment at the conclusion of the lease.

Although equity participants sometimes like to view their credit exposure as being limited to their original equity investment, most of which may be recovered in the first few years of the lease term of a leveraged lease, this is not the case if a “forgiveness” of the leveraged debt occurs in the later years of the lease. In such a situation, the lessor may be deemed to realize taxable income from the forgiveness. A forgiveness might occur, for example, where the lessee defaults and the indenture trustee (on behalf of the loan participants) repossesses and sells the equipment for less than the outstanding principal of the leveraged debt.

For these reasons, leveraged leases are available only to lessees that present no apparent credit risk. Lenders and equity sources must be confident in the lessee's ability to meet all of its obligations under the lease, both for rental payments and for maintenance of the leased equipment.

TAX INDEMNIFICATION FOR FUTURE CHANGES IN TAX LAW

Where a company intends to use a true lease to finance the acquisition of equipment it needs, the lessee and lessor must agree as to which of them will bear the burden of future tax changes. The major tax benefits available to a lessor consist of MACRS-accelerated depreciation deductions. During the early years of a lease, tax deductions attributable to accelerated depreciation equal all or part of taxable rental income. This results in deferral of taxable income attributable to the lease rentals until the later years of the lease when depreciation deductions decline or are exhausted. If in the early years of a lease, the tax rate rises above that assumed by the lessor for pricing, the lessor's cash flows and yield will rise accordingly during those early years in which the lessor claims depreciation deductions. On the other hand, if the tax rate is higher than assumed by the lessor for pricing during the later years in which the rental income exceeds the depreciation deductions, the lessor's cash flow and yield will decline or even disappear.

Lessors generally take the position that they should be held harmless by the lessee in the event of any tax law changes or tax rate changes adversely affecting their contemplated yield or cash flow. Lessors argue that the lessee is no worse off under such an indemnification than the lessee would have been had the lessee purchased the leased equipment and directly claimed tax benefits associated with equipment ownership. Lessees, on the other hand, generally take the position that after delivery of the leased equipment, lessors should assume the risk of loss of tax benefits for any reason except as a result of acts or omissions of the lessee.

The problem facing both lessees and lessors is how to engage in equipment leasing and protect themselves in view of the future tax rate and tax law and uncertainties. A significant tax rate change can have disastrous consequences for a lessor, and the possibility of such a change is very real.

Initial questions facing lessors and lessees include the following:9

- What is the definition of the tax-law risk and tax-rate risk covered by the indemnity?

- What risk of tax-rate change that needs to be covered?

- What event or events will trigger a tax indemnity?

- For what period of time will tax indemnities apply? For the entire lease? Or for a limited number of months or years?

- How will the loss (or gain) resulting from indemnified tax rate risks be computed?

- How will the indemnified party be compensated?

- Under what circumstances can the lessee or lessor terminate the lease?

NEED FOR A FINANCIAL ADVISER

An initial question for a company considering a leveraged lease is to determine its need for a financial adviser or broker.10 Basically, this question boils down to whether the services performed by a financial adviser will be cost effective as compared to the expenditure for the financial adviser's fee.

The services to be performed by a financial adviser for a company securing a leveraged lease include some or all of the following:

- Advise the company in structuring financing of the planned equipment acquisition:

- Understand the company's objectives, priorities, and constraints.

- Analyze the tax, legal, accounting, and economic consequences for the company as well as the potential market acceptance of alternative approaches.

- Meet and work with the company's legal and tax counsel with regard to the proposed financing.

- Consider alternative methods of financing and compare their advantages and disadvantages with lease financing.

- If leasing is the best alternative, recommend the optimal lease financing strategy.

- Assist the company in establishing a realistic transaction timetable, ensuring that all aspects of the financing progress in a timely and systematic fashion.

- Assist the company in preparing an equity offering memorandum describing the transaction for distribution to prospective equity sources.

- Identify the most appropriate equity investors for the transaction.

- Solicit commitments on a consistent basis from prospective equity participants so as to ensure a complete underwriting of the equity investment in the transaction. Arrange meetings and make face-to-face presentations with priority prospects to explain the transaction.

- Arrange meetings between the company's key executives and priority prospects where that is advisable.

- Review, rank, and clarify the equity responses for the company. Evaluate the economics of the equity commitments, including all relevant terms and conditions. Assist the company in selecting the best equity investor(s).

- Assist the company in negotiating and completing the commitment letter and any pricing adjustments with the equity participants.

- Arrange for the private placement of the leveraged debt or assist in doing so. Advise the company with regard to structuring the leveraged debt to achieve optimal pricing, amortization, and flexibility, as well as favorable terms and conditions.

- In conjunction with the company and its counsel, negotiate and document the terms and conditions of the various leveraged lease documents.

- Assist in the closing of the transaction.

In order to proceed without a financial adviser, a prospective lessee must be satisfied that:

- It has the technical and professional expertise to perform the above services with its own staff.

- Those persons on its staff with the technical ability and expertise to arrange a lease can devote the time necessary to arrange, negotiate, and complete the transaction as successfully as a financial adviser would do.

- It can gain access to the lease equity and/or debt placement markets as effectively and competitively as the financial adviser can.

Some companies that have regularly used leveraged leases to finance equipment feel comfortable with arranging additional leveraged leases themselves, particularly when the additional leases are repetitious and very similar to what they have done in the past. While such companies undoubtedly have the expertise to structure and negotiate leveraged leases, the questions they must address are whether they are familiar enough with changing lease equity markets to be up-to-date with regard to the latest innovative developments in those markets and whether they will be able to identify the full range of potential investors and lenders. Oftentimes the newest entrants are the most aggressive bidders as they seek to quickly build their portfolios.

THE STEPS IN STRUCTURING, NEGOTIATING, AND CLOSING A LEVERAGED LEASE

We conclude this chapter with a description of the various steps and milestones in structuring, negotiating and closing a leveraged lease are as follows:

- Review of the transaction by the lessee and its counsel.

- Preparation of drafts of the equity and debt-placement memos.

- Preparation of the equity and debt-placement offering memorandums with the lessee and its counsel.

- Preparation of equity and debt solicitation lists.

- Completion of the equity solicitation and receipt of firm commitments from selected equity sources.

- Completion and execution of the equity commitment letter.

- Completion of a draft of all documents to be required.

- Completion of debt solicitation and receipt of firm commitments from debt participants.

- Review of debt documents by the lessee and equity participants.

- Completion and execution of the debt commitment letter.

- Completion of negotiations and agreement as to documents by the lessee and equity participants.

- Review of documents by the debt participants.

- Completion of negotiations and agreement as to debt documents by the equity participants, the lessee, and the debt participants.

- Completion of final documents and signatures on all documents by all parties.

- Delivery of the leased equipment, acceptance by the lessee, and payment of the purchase price.

The timetable for accomplishing those steps varies with each transaction depending upon the complexity of the structure, the strength of the lessee's credit, and the time remaining before the property to be leased is expected to be placed in service. While the placed-in-service date cannot in and of itself result in a rapid time schedule, it can motivate the parties to move with a greater sense of urgency than might otherwise be the case. As noted earlier, the lessee and the lessor can speed the process and hold down the costs by closely supervising their attorneys, segregating business decisions from legal decisions, and making business decisions promptly so that the documentation can move forward.

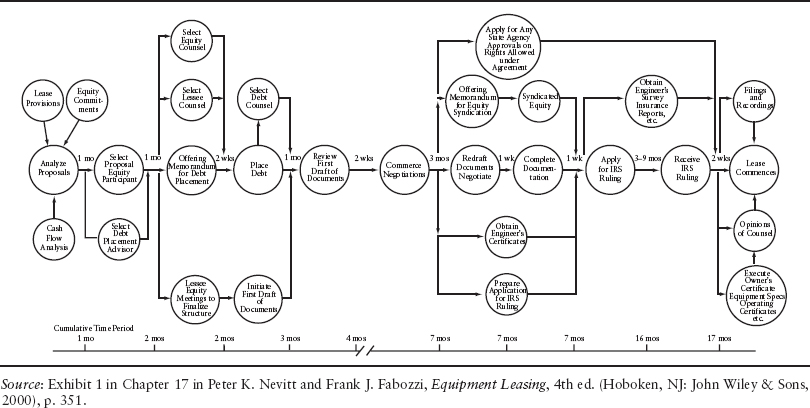

While it is possible to arrange a facility lease in a fairly short time, the financial planning for a large facility is complex and may involve a lead time extending over several months. Exhibit 12.3 is a flowchart for a facility leveraged lease transaction showing the decisions that will be made and the events that will take place from the inception to the completion of such a transaction.

EXHIBIT 12.3 Critical Path Chart of Leveraged Lease Financing for a Large Manufacturing Facility

1 The single-investor lessor may securitize all or part of the lease receivables at a later date.

2 The exact amount is a function of the economic result the lessor seeks to achieve.

3 If the credit of the lessee is insufficient to support the transaction, a guarantor of the lessee obligations under the lease including payment of rents may be necessary. This guarantor may, for example, be the parent or sister company of the lessee, an interested third party, or a government agency. As discussed elsewhere, leveraged debt cannot usually be directly guaranteed under the tax requirements of the IRS.

4 Tax requirements for leveraged leases are discussed in Chapter 5 in Peter K. Nevitt and Frank J. Fabozzi, Equipment Leasing, 4th ed. (Hoboken, NJ: John Wiley & Sons, 2000).

5 A single trustee may assume the duties of both an owner trustee and an indenture trustee in a leveraged lease. Where a single trustee is used, the trustee is referred to as the owner trustee. Those who favor using a single trustee in a leveraged lease transaction argue that such an arrangement is simpler and reduces the costs of the transaction. Although the use of a single trustee in a leveraged lease has become an increasingly common arrangement, serious conflicts of interest may arise between the equity participants and the loan participants in the event of a default by the lessee. Such potential conflicts make the use of a single trustee unattractive if there is any question regarding the lessee's credit.

6 Where rents are guaranteed by a third party, a controversy may arise under Revenue Procedure 75–21 that relates to whether the lessor is at risk for an amount equal to 20% of the cost of the equipment. It can be strongly argued that such a guarantee is merely the equivalent of a second credit exposure and does not alter the fact that the lessor is “at risk.”

7 Subject to Internal Revenue Service limitations imposed by Section 467 of the Code and Proposed Regulations under Section 467.

8 The equipment's lack of portability does not make it limited-use property for tax purposes so long as the facility is reasonably expected to have a fair market value equal to 20% of its original cost at the conclusion of the lease. The 20% useful life tests of Revenue Procedure 75–21 are met if, at the conclusion of the lease, the facility can continue to be used at its original location for a period of time equal to 20% or more of the base lease term plus any fixed-rate renewal terms.

9 For a further discussion of each, see Chapter 16 in Nevitt and Fabozzi, Equipment Leasing.

10 Generally the lessee's financial adviser will locate the equity and/or debt investors and thus perform the brokerage function. From the standpoint of the investor and in the parlance of the trade, the lessee's financial adviser is a broker.