The relationship between networks and earned value analysis (EVA) is demonstrated by an example of a boiler construction project in this chapter. The network shown in activity on arrow and activity on node format is converted into a bar chart with the man-hours added. These hours were then transferred to an EVA sheet, from which curves were generated showing the movement and trends of the actual hours, value hours (earned value), estimated final hours, percent complete and percent efficiency. The jargon terms budgeted cost of work performed, budgeted cost of work scheduled, actual cost of work performed, cost performance index, schedule performance index, actual time expended and budget at completion are explained and compared with the equivalent non-jargon terms, and calculations are provided to show how to obtain these. A sample time sheet for feedback of EVA data is also included.

Keywords

ACWP; BCWP; BCWS; % Complete; Control graphs; CPI; % Efficiency; EVA; SPI; Time sheets

In addition to the numerical report shown in Fig. 33.5, two very useful management control graphs can be produced:

1. Showing budget hours, actual hours, value hours and predicted final hours, all against a common time base; and

2. Showing percent planned, percent complete and efficiency, against a similar time base.

The actual shape of the curves on these graphs give the project manager an insight into the running of the job, enabling appropriate action to be taken.

Fig. 33.1 shows the site returns of man-hours of a small project over a nine-month period, and, for convenience, the table of percent complete and actual and value hours is drawn on the same page as the resulting curves. In practice, a greater number of activities would not make such a compressed presentation possible.

A number of interesting points are ascertainable from the curves:

1. There was obviously a large increase in site labour between the fifth and sixth months, as shown by the steep rise of the actual hours curve.

2. This has resulted in increased efficiency.

3. The learning curve given by the estimated final hours has flattened in month 6 making the prediction both consistent and realistic.

4. Month 7 showed a divergence of actual and value hours (indicated also by a loss of efficiency), which was corrected (probably by management action) by month 8.

5. It is possible to predict the month of actual completion by projecting all the curves forward. The month of completion is then given:

a. When the value hours curve intersects the budget line; and

b. When the actual hours curve intersects the estimated final hours curve.

Figure 33.1 Control curves.

In this example, one could safely predict completion of the project in month 10.

It will be appreciated that this system lends itself ideally to computerization, giving the project manager the maximum information with very minimum site input. The sensitivity of the system is shown by the immediate change in efficiency when the value hours diverged from the actual hours in month 7. This alerts management to investigate and apply corrections.

For maximum benefit, the returns and calculations should be carried out weekly. By using the normal weekly time cards very little additional site effort is required to complete the returns, and with the aid of a good computer program the results should be available 24hours after the returns are received.

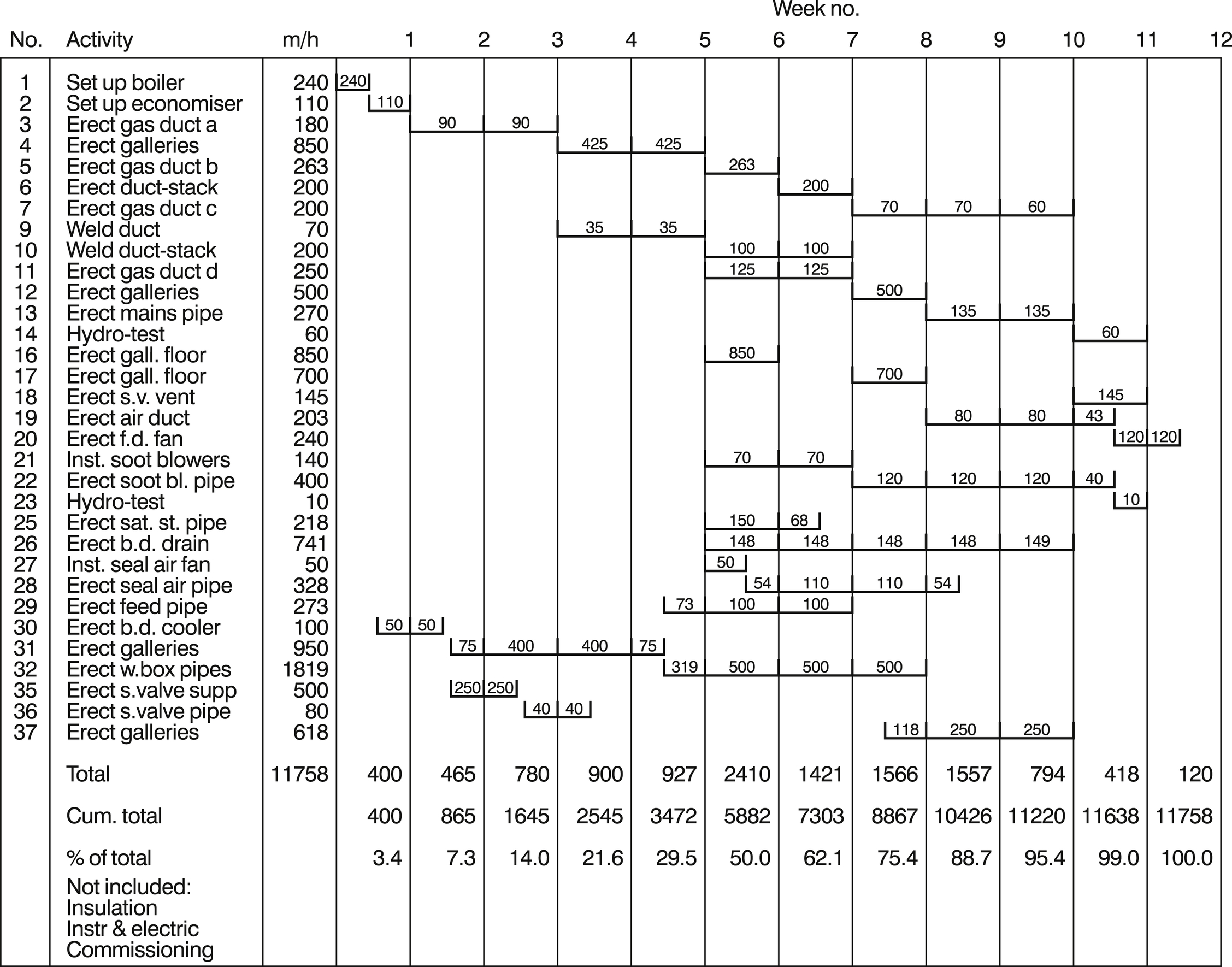

An example of the application of a manual earned value analysis (EVA) is shown in Figs 33.2–33.9. The site-construction network of a package boiler installation is given in Fig. 33.2. Although the project consisted of three boilers, only one network, that of boiler no. 1 is shown. In this way, it was possible to control each boiler construction separately and compare performances. The numbers above the activity description are the activity numbers, while those below are the durations. The reason for using activity numbers for identifying each activity, instead of more conventional beginning and end event numbers, is that the identifier must always be uniquely associated with the activity description.

If the event numbers (in this case the coordinates of the grid) were used, the identifier could change if the logic were amended or other activities were inserted. In a sense, the activity number is akin to the node number of a precedence diagram, which is always associated with its activity. The use of precedence diagrams and computerized EVA is therefore a natural marriage, and to illustrate this point, a precedence diagram is shown in Fig. 33.3.

Once the network has been drawn, the man-hours allocated to each activity can be represented graphically on a bar chart. This is shown in Fig. 33.4. By adding up the man-hours for each week, the totals, cumulative totals and each week’s percentage of the total man-hours can be calculated. If these percentages are then plotted as a graph, the planned percent-complete curve can be drawn. This is shown in Fig. 33.7.

All the work described up to this stage can be carried out before work starts on site. The only other operation necessary before the construction stage is to complete the left-hand side of the site-returns analysis sheet. This is shown in Fig. 33.5, which covers only periods four to nine of the project. The columns to be completed at this stage are:

1. The activity number

2. The activity title

3. The budget hours

Figure 33.2 Boiler No. 1. Network arrow diagram.

Figure 33.3 Boiler No. 1. Precedence diagram.

Figure 33.4 Boiler No. 1. Bar chart and man-hour loadings.

Figure 33.5 Earned value analysis sheet.

Figure 33.6 Boiler No. 1. Man hour–time curves.

Once work has started on site, the construction manager reports weekly on the progress of each activity worked on during that week. All he has to state is:

1. The activity number

2. The actual hours expended in that week

3. The percent complete of that activity to date

If the computation is carried out manually, the figures are entered on the sheet (Fig. 33.5) and the following values calculated weekly:

1. Total man-hours expended this week (W column)

2. Total man-hours to date (A column)

Figure 33.7 Boiler No. 1. Percentage–time curves.

3. Percent complete of project (% column)

4. Total value hours to date (V column)

5. Efficiency

6. Estimated final hours

Alternatively, the site returns can be processed by computer and the resulting printout of part of a project is shown in Fig. 33.8. Whether the information is collected manually or electronically, the return can be made on a standard time sheet with the only addition being a % complete column. In other words, no additional forms are required to collect information for EVA. There are in fact only three items of data to be returned to give sufficient information:

1. The activity number of the activity actually being worked on in that time period;

2. the actual hours being expended on each activity worked on in that time period; and

3. The cumulative % complete of each of these activities.

Figure 33.8 Standard E.V. Report printout.

Figure 33.9 Weekly time sheet.

All the other information required for computation and reporting (such as activity titles and activity man-hour budgets) will already have been inputted and stored in the computer. A typical modified time sheet is shown in Fig. 33.9.

A complete set of printouts produced by a modern project-management system are shown in Figs 33.10–33.14. It will be noted that the network in precedence format has been produced by the computer, as have the bar chart and curves. In this program, the numerical EVA has been combined with the normal critical path analysis from one database, so that both outputs can be printed and updated at the same time on one sheet of paper. The reason the totals of the forecast hours are different from the manual analysis is that the computer calculates the forecast hours for each activity and then adds them up, while in the manual system the total forecast hours are obtained by simply dividing the actual hours by the percent complete rounded off to the nearest 1%.

As mentioned earlier, if the budget hours, actual hours, value hours and estimated final hours are plotted as curves on the same graph, their shape and relative positions can be extremely revealing in terms of profitability and progress. For example, it can be seen from Fig. 33.6 that the contract was potentially running at a loss during the first three weeks, since the value hours were less than the actual hours. Once the two curves crossed, profitability returned and in fact increased, as indicated by the diverging nature of the value- and actual-hour curves. This trend is also reflected by the final-hours curve dipping below the budget-hour line.

Figure 33.10 AoN diagram of boiler.

Figure 33.11 Bar chart.

Figure 33.12 Combined CPA and EVA print out.

Figure 33.13 Boiler No. 1. Erection man-hours.

Figure 33.14 Boiler No. 1. Percentage complete and efficiency.

The percentage–time curves in Fig. 33.7 enable the project manager to compare actual percent complete with the planned. This is a better measure of performance than comparing actual hours expended with planned hours expended. There is no virtue in spending the man-hours in accordance with a planned rate. What is important is the percent complete in relation to the plan and whether the hours spent were useful hours. Indeed, there should be every incentive to spend less hours than planned, provided that the value hours are equal or greater than the actual and the percent complete is equal or greater than the planned.

The efficiency curve in Fig. 33.7 is useful, since any drop is a signal for management action. Curve ‘A’ is based on the efficiency calculated by dividing the cumulative value hours by the cumulative actual hours for every week. Curve ‘W’ is the efficiency by dividing the value hours generated in a particular week by the actual hours expended in that week. It can be seen that Curve ‘W’ (shown only for the periods 5–9) is more sensitive to change and is therefore a more dramatic warning device to management.

Finally, by comparing the curves in Figs 33.6 and 33.7, the following conclusions can be drawn:

1. Value hours exceed actual hours (Fig. 33.6). This indicates that the site is efficiently run.

2. Final hours are less than budget hours (Fig. 33.6). This implies that the contract will make a profit.

3. The efficiency is over 100% and rising (Fig. 33.7). This bears out conclusion 1.

4. The actual percent complete curve (Fig. 33.7), although less than the planned, has for the last four periods been increasing at a greater rate than the planned (i.e., the line is at a steeper angle). Hence, the job may well finish earlier than planned (probably in week 11).

5. By projecting the value-hour curve forward to meet the budget-hour line, it crosses in week 11 (Fig. 33.6).

6. By projecting the actual-hour curve to meet the projection of the final-hour curve, it intersects in week 11 (Fig. 33.6). Hence, week 11 is the probable completion date.

The computer printout shown in Fig. 33.8 is updated weekly by adding the man-hours logged against individual activities. However, it is possible to show the cost of both the historical and current man-hours in the same report. This is achieved by feeding the average man-hour rate for the contract into the machine at the beginning of the job and updating it when the rate changes. Hence, the new hours will be multiplied by the current rates. A separate report can also be issued to cover the indirect hours such as supervision, inspection, inclement weather and general services.

Since the value-hour concept is so important in assessing the labour content of a site or works operation, the following summary showing the computation in non-numerical terms can be of help:

If

B

=

Budget hours (total)

C

=

Actual hours (total)

D

=

Percent complete

E

=

Value hours (earned value) (total)

F

=

Forecast final hours

G

=

Percent efficiency (CPI)

Then:

E=B×D, D=E/B×100, G=E/C×100,F=C/DorB/G

Overall Project Completion

Once the man-hours have been ‘costed’, they can be added to other cost reports of plant, equipment, materials, subcontracts, etc. so that an overall percent completion of a project can be calculated for valuation purposes on the only true common denominator of a project – money.

The total value to date divided by the revised budget×100 is the percent complete of a job. The value-hour concept is entirely compatible with the conventional valuation of costing such as value of concrete poured, value of goods installed, cost of plant utilized – activities, which can, by themselves, be represented on networks at the planning stage.

Table 33.1 shows how the two main streams of operations, i.e., those categories measured by cost and those measured by man-hours can be combined to give an overall picture of the percent complete in terms of cost and overall cost of a project. While the operations shown relate to a construction project, a similar table can be drawn for a manufacturing process, covering such operations as design, tooling, raw material purchase, machinery, assembly, testing, packing.

Cost of overheads, plant amortization, licences, etc. can, of course, be added like any other commodity. An example giving quantities and cost values of a small job involving all the categories shown in Table 33.1 is presented in Tables 33.2–33.4. It can be seen that in order to enable an overall percent complete to be calculated, all the quantities of the estimate (Table 33.2) have been multiplied by their respective rates – as in fact would be done as part of any budget – to give the estimated costs.

Table 33.3 shows the progress after a 16-week period, but in order to obtain the value hours (and hence the cost value) of category D it was necessary to break down the man-hours into work packages that could be assessed for percent completion. Thus, in Table 33.4, the pipelines A and B were assessed as 35% and 45% complete, and the pump and tank connections were found to be 15% and 20% complete, respectively. Once the value hours (3180) were found, they could be multiplied by the average cost per man-hour to give a cost value of $14628.

Example showing effect of percent complete of different categories.

Estimate Category

Item

Unit

Quantity

Rate ($/Hour)

Cost $

A

Concrete

M3

1000

25

25,000

pipe 6-inch

M

2000

3

6000

Painting

M2

2500

10

25,000

56,000

B

Tanks

No

3

20,000

60,000

Pumps

No

1

8000

8000

Pumps

No

1

14,000

14,000

82,000

C

Cranes

Hours

200

6015

12,600

(hire)

Hours

400

6000

Welding

18,000

D

Pipe fitters

Hours

4000

4} Av.

16,000

Welders

Hours

6000

5} 4.6

30,000

10,000

46,000

Table 33.3

Progress after 16weeks.

Category

Item

Unit

Quantity

Rate ($/Hour)

Cost $

A

Concrete poured

M3

900

25

22,500

Pipe 6-inch supplied

M

1000

3

3000

Painting

M2

500

10

5,000

Complete:30,50056,000×100=54.46

30,500

B

Tanks delivered

No

2

20,000

40,000

Pumps A

No

1

8000

8000

Pumps B

No

1

–

Complete:48,00082,000×100=58.53

48,000

Table 33.4

Category

Item

Unit

Quantity

Rate ($/Hour)

Cost $

C

Cranes on-site

Hours

150

60

9000

Welding plant

Hours

200

15

3000

Complete:12,00018,000×100=66.66

12,000

D

Pipe fitters

Hours

1800

4

7200

Welders

Hours

2700

5

13,500

20,700

Erection work

Budget M/H

Percent complete

Value hours

Actual hours

Pipeline A

3800

35

1330

1550

Pipeline B

2800

45

1260

1420

Pump connection

1800

15

270

220

Tank connection

1600

20

320

310

10,000

3180

3500

Complete:318010,000×100=31.80

Cost value (Av.)=3180×4.6=$14,628

Table 33.5 shows the summary of the four categories. An adjustment should therefore also be made to the value of plant utilization category C since the two are closely related. The adjusted value total would therefore be as shown in column V.

Table 33.5

Total cost to date.

I

II

III

IV

V

Category

Budget

Cost

Value

Adjusted Value

A

56,000

30,500

30,500

30,500

B

82,000

48,500

48,000

48,000

C

18,000

12,000

12,000

10,920

D

46,000

20,700

14,628

14,628

Total

$202,000

$111,200

$105,128

$104,048

With a expenditure to date true value of $104,048, the percent completion in terms of cost of the whole site is therefore:

104,048202,000×100=51.5

It must be stressed that the cost completed is not the same as the completion of construction work. It is only a valuation method when the material and equipment are valued (and paid for) in their month of arrival or installation.

When the materials or equipment are paid for as they arrive on site (possibly a month before they are actually erected), or when they are supplied ‘free issue’ by the employer, they must not be part of the value or complete calculation.

It is clearly unrealistic to include materials and equipment in the complete and efficiency calculation as the cost of equipment is not proportional to the cost of installation. For example, a carbon steel tank takes the same time to lift onto its foundations as a stainless steel tank, yet the cost is very different. Indeed, in some instances, an expensive item of equipment may be quicker and cheaper to install than an equivalent cheaper item, simply because the expensive item may be more ‘complete’ when it arrives on site.

All the items in the calculations can be stored, updated and processed by computer, so there is no reason why an accurate, up-to-date and regular progress report cannot be produced on a weekly basis, where the action takes place – on the site or in the workshop.

Clearly, with such information at one’s fingertips, costs can truly be controlled – not merely reported!

It can be seen that the value hours for erection work are only 3180 against an actual man-hours usage of 3500. This represents an efficiency of only

31803500×100=91approx.

An adjustment should therefore also be made to the value of plant utilization, i.e., 12,000×91%=10,920. The adjusted value total would therefore be as shown in column V.

The SMAC system described on the previous pages was developed in 1978 by Foster Wheeler Power Products, primarily to find a quicker and more accurate method for assessing the % complete of multi-discipline, multi-contractor construction projects.

However, about 10years earlier the Department of Defense in the USA developed an almost identical system called cost, schedule, control system (CSCS), which was generally referred to as EVA. This was mainly geared to the cost control of defence projects within the USA, and apart from UK subcontractors to the American defence contractors, was not disseminated widely in the UK.

While the principles of SMAC and EVA are identical, inevitably a difference in terminology is developed, which has caused considerable confusion to students and practitioners. Fig. 33.16 lists these abbreviations and their meaning, and Fig. 33.17 shows the comparison between the now accepted EVA ‘English’ terms (shown in bold) and the CSCS jargon (shown in italics).

The CSCS also introduced four new parameters for cost efficiency and, for want of a better word, time efficiency:

1. The cost variance: this is the arithmetical difference at any point between the earned value and the actual cost.

2. The schedule variance: this is the arithmetical difference between the earned value and the scheduled (or planned) cost. However, comparing progress in time by subtracting the planned cost from the earned value is somewhat illogical as both are measured in monetary terms. It would make more sense to use parameters measured in time to calculate the time variance. This can be achieved by subtracting the actual duration [Actual time expended (ATE)] for a particular earned value from the originally planned duration (OD) for that earned value. This is shown clearly in Fig. 33.15. It can be seen that if the project is late, the result will be negative. There are therefore two schedule variances (SV):

a. SV (cost), which is measured on the cost scale of the graph; and

b. SV (time), which is measured on the time scale.

3. The cost efficiency is called the cost performance index (CPI) and is earned value/actual cost.

4. The ‘time efficiency’ is called the schedule performance index (SPI) and is earned value/scheduled (or planned) cost.

Again, as with the schedule variance, measuring efficiency in time by dividing the earned value by the planned cost, which are both measured in monetary terms or man-hours, is equally illogical and again it would be more sensible to use parameters measured in time. Therefore, by dividing the planned duration for a particular earned value by the actual duration for that earned value, a more realistic index can be calculated. All time measurements must be in terms of hours, day numbers, week numbers, etc. – not calendar dates.

There are therefore now two SPIs:

a. SPI (cost) measured on the cost scale, i.e., earned value/scheduled cost; and

b. SPI (time) measured on the time scale, i.e., planned duration/actual duration.

Figure 33.15 Earned value chart reproduced from BS 6079 ‘Guide to Project Management’ by permission of British Standards Institution.

Figure 33.16

Figure 33.17 Comparison of EV terms.

In practice, the numerical difference between these two quotients is small, so that SPI (cost), which is easier to calculate, is sufficient for most purposes, bearing in mind that the result is still only a prediction based on historical data.

In 1996, the National Security Industrial Association (NISA) of America published their own Earned Value Management System (EVMS), which dropped the terms such as actual cost of work performed, budgeted cost of work performed and budgeted cost of work scheduled (BCWS) used in CSCS, and adopted the simpler terms of earned value, actual and schedule instead.

Since then, the American Project Management Institute (PMI), the British Association for Project Management (APM) and the British Standards Institution (BSI) have all discarded the CSCS abbreviations and also adopted the full English terms. In all probability, this will be the future universal terminology.

Fig. 33.17 clearly shows the earned value terms in both English (in bold) and EV jargon (in italics).

Earned Schedule

It has long been appreciated that Schedule Performance Index (cost) (SPIcost) based on the cost differences of the earned value and planned curves is somewhat illogical. An index reflecting schedule changes should be based on the time differences of a project. For this reason, Schedule Performance Index (time) (SPItime) is a more realistic approach and gives more accurate results, although in practice the numerical differences between SPIcost and SPItime are not very great. SPItime for any point in time, or the current time, can be obtained by dropping a vertical line from the planned curve (BCWS) to the time baseline. This is time now (ATE). Next, dropping a vertical line from the point on the planned curve, where the planned value is equal to the earned value to the time baseline, gives the original planned duration (OD).

This duration from the start date to (OD) is referred to as ‘Earned Schedule’

SPItime is therefore OD/ATE, i.e., the time efficiency. See Fig. 33.18.

Similar to budget cost/CPI=the final predicted cost, estimated duration/SPItime=final completion time. It is important to remember that all units of durations on the time scale must be in day, week or month numbers, not in calendar dates.

Integrated Computer Systems

Until 1992, the EVA system was run as a separate computer program in parallel with a conventional CPM system. Now, however, a number of software companies have produced project-management programs that fully integrate critical path analysis with EVA. One of the best programs of this type, Primavera P6, is fully described in Chapter 51.

Figure 33.18

The system can, of course, be used for controlling individual work packages, whether carried out by direct labour or by subcontractors, and by multiplying the total actual man-hours by the average labour rate, the cost to date is immediately available. The final results should be carefully analysed and can form an excellent base for future estimates.

As previously stated, apart from printing the EVA information and conventional CPM data, the program also produces a computer drawn network. This is drawn in precedence format.

The information shown on the various reports include:

1. The man-hours spent on any activity or group of activities

2. The percent complete of any activity

3. The overall percent complete of the total project

4. The overall man-hours expended

5. The value (useful) hours expended

6. The efficiency of each activity

7. The overall efficiency

8. The estimated final hours for completion

9. The approximate completion date

10. The man-hours spent on extra work

11. The relationship between programme and progress

12. The relative performance of subcontractors or internal subareas of work

EVA % Complete Assessment

For updating purposes, it is necessary to assess the percent complete of each EVA-related activity on the schedule. This is in fact a measure of the work done to date and involves different units of measurement, depending on the type of work involved. For example, the unit for cables laid is the metres actually installed, while for paintwork, it is the area in m2 of paint applied on date.

Figure 33.19

Fig. 33.19 gives an overview of some of the units used on a construction contract. This is only for assessment of percent complete. The EVA calculations must still be in man-hours or monetary units.