Determinacy of equilibria in a model of intertemporal equilibrium with capital goods

Domenico Tosato*

1 Introduction

In the history of economic thought, the theory of value with fixed capital goods and capital formation is essentially linked to the names of Wicksell and Walras. Two different analytical roads were pursued. While Wicksell’s theoretical construction builds on the notion of aggregate capital measured in value terms, Walras’s model of general economic equilibrium is based on the assumption of heterogeneous capital goods available in arbitrarily given initial quantities. Piero Sraffa’s discovery of the possibility of reswitching of techniques — and, subsequently, of more general phenomena of capital deepening reversal — represents an insuperable critique of the notion of an aggregate measure of capital and of the related tool of the aggregate production function. This critique has, accordingly, determined the abandonment of the Wicksellian1 approach as a foundation for an internally consistent theory of value.

The debate remains open, on the contrary, with regard to Walras’s theory and the developments of the general equilibrium approach in the intertemporal dimension. This circumstance justifies the interest for a re-examination of some of the themes of the debate on the consistency and the properties of the general equilibrium model, especially in the context of a formulation of the theory of capital formation more clearly and closely derived from Walras’s analytical construction.

In Arrow—Debreu’s (1954) and Debreu’s (1959) canonical approach, the issues concerning the production of new capital goods are, to some extent, ‘concealed’ inside an extremely general formulation of the production sets, which sidesteps the distinction between fixed capital goods and other factors of production, and of consumers’ choices, which obscures the aspects con cerning the saving decision.2 The distinctive feature of capital goods, namely of being commodities that are currently produced, but subject to the constraint that their rates of return be equal to the market rate, risks thereby to be lost. In other words, in the canonical intertemporal equilibrium approach, the fact that the capital goods available in the periods following the initial one are endogenously determined by households’ saving decisions and firms’ production decisions, as well as the role that the condition of the uniformity of the rates of return plays in shaping such decisions, cannot be clearly perceived.

In the Arrow—Debreu economy, every commodity — be it a capital good or not — can be the object of a loan contract, so that every commodity becomes a potential asset. The own rates of return are accordingly defined in a form quite different from that used by Walras. In Walras’s theory, the own rate of return is the ratio of the rental rate to the purchase price of the capital good, while in the Arrow—Debreu model it is the ratio of the discounted purchase prices of two successive periods. Own rates are consequently defined with reference to capital goods only in the first instance, to all commodities in the second. It is in this sense that the specific nature of capital goods and of what determines their rates of return is lost sight of.

On the other hand, the distinction operated in the Arrow—Debreu inter temporal approach between commodities available in different periods and the subsequent possibility that relative prices may change over time pave the way for a solution to the difficulty that Walras had met with the condition of the equality of the rates of return. In the Arrow—Debreu model, own rates of interest are distinguished from rates of return: whereas the former may diverge, the latter are necessarily equal in equilibrium, due to the role played by the appreciation, or depreciation, of capital values.

The belief that there is a gain in clarity to be achieved by recasting the theory of intertemporal equilibrium in the setting of the Walrasian tradition, taking account of the correct formulation of the equality condition on the rates of return of capital goods, is at the origin of this paper. The plan of the work is as follows. Section 2 offers a review of the literature on the problems of capital formation in general equilibrium models, from Walras’s effort to formulate a theory that eliminates the role of time to the subsequent constructions that refer to the Hicksian methods of temporary and intertemporal equilibrium; the focus of the presentation is on the main critiques moved to the analytical structure of the models and to the nature of their equilibrium solutions. The model of capital formation here examined is presented in Section 3; a proof of the existence of generically isolated equilibria, using Kehoe’s (1980) approach, follows in Sections 4 and 5. Mandler’s (1995, 1999a, 1999b) result on the possibility of sequential indeterminacy of the equilibrium solution in an intertemporal model, in which, as envisaged here, the quantities of some of the factors of production are endogenously determined, is examined in Section 6; a qualification emerges to the general validity of this result. In Section 7 the possibility of paradoxical behaviour argued by Garegnani (2000) and Schefold (1997, 2000) is considered; a critical evaluation of their result is offered. A brief summing up concludes the paper in Section 8.

2 The theory of capital formation in models of general equilibrium: a review of the literature

2.1 Walras and the critique of Sraffian origin

In the introductory paragraph of his 1929 paper, The place of capital in the theory of price, Lindahl (1939) writes that the aim of his work is to offer a contribution to the study of the complexities arising for the theory of value from ‘the existence of a time factor in production, i.e. to the complex of problems where the theory of capital and interest and the general theory of price meet’ (Lindahl, 1939, p. 271, emphasis added). Most economists would certainly agree with Lindahl’s assertion that time is intimately related to capital and interest, both in the sense that the central issue of economic dynamics is represented by the theory of capital accumulation and that the proper setting for the study of such problems is that of an economy in which agents have a multi-period time horizon.

Yet, perhaps paradoxically, the first systematic analysis of the problems of capital formation in a general equilibrium framework is carried out by Walras from a point de vue statique. This does not mean that Walras’s economy is stationary. On the contrary, his economy is progressive. In Lesson 36,3 Walras defines economic progress as a situation in which the quantity of consumption goods grows so as to lead to a ‘diminution in the intensities of last wants satisfied […] in a country with an increasing population’ (Walras, 1954, p. 383). Thus, the current production of capital goods proper is in no way confined to the mere replacement of those used up during the period. Walras envisages in fact a growth path for his economy in which capital accumulation has to proceed at a pace faster than population, so as to make possible the substitution of the services of capital goods proper for those of the irreproducible land.

In order to enact his static approach, Walras basically relies on two assumptions: the first concerns households’ behaviour, the second financial calculations. Walras assumes that households offer the services of the productive factors they possess and, among them, the services of the capital goods that represent the initial endowment of the economy. With the income thus received, households consume and save. Walras actually adopts the fiction that households demand not only the currently produced consumption goods, but also a particular commodity that produces a flow of perpetual income and whose price is the inverse of the rate of interest, a sort of consol named commodity E. With this fiction Walras avoids the problem of modelling households’ decisions in terms of a true intertemporal consumption programme and eliminates the time factor from consumers’ choices. The introduction of commodity E has the further implication that consumers’ demand for a complex of heterogeneous capital goods is reduced to the demand for a homogenous income-yielding commodity; this means that we should think of portfolio decisions as being taken by a not better-specified financial sector, which invests the savings of the households.

The demand for commodity E is satisfied by those goods that are capable of producing a perpetual income flow: these are the capital goods, which are the only assets considered in the economy. The current demand for perpetual income is therefore, through the intermediation of the financial sector, a demand for the newly produced capital goods: in equilibrium this demand in value terms must be equal to the value of the supply of investment goods.

It is, however, clear that capital goods qualify for satisfying the demand of perpetual income only insofar as they succeed in offering a return — a rate of net income in Walras’s terms — equal to the market rate. The rates of return of the various capital goods must therefore meet the competitive non arbitrage condition of being uniform. It is in the definition of this condition that the second of Walras’s two fundamental assumptions is introduced.

The percentage return of a capital good is, in general, the sum of two components: the first is the rental rate for the use of the service, net of depreciation, expressed in terms of the purchase price; the second is the capital gain or loss, due to the percentage variation of the purchase price between the beginning and the end of the period. The time factor is obviously present in the second component, but could be involved also in the first if the purchase price is made to coincide with the value of the capital good at the beginning of the period. Walras assumes, at this point, that the beginning of the period purchase prices of capital goods are equal to their end of period prices, which under competitive conditions must in turn be equal to the costs of production of additional quantities of the same goods (ibid., p. 309). With this assumption, any possible change in the purchase price of capital goods is, by definition, excluded. The rate of return on the asset is thus made up of the sole component represented by the ratio of the current rental price to the current purchase price; it is, in other words, identified with the own rate of interest. The model of general equilibrium with capital formation is thereby closed without having to consider the time factor.

It is convenient, for ease of subsequent reference, to have a simplified version of this model. Consider, therefore, an economy of pure production of capital goods by means of capital goods only, i.e. using as factors of production the services of the initially available quantities of the same commodities, in the proportion of one unit of service per unit of stock, and no other input. Assume, furthermore, a linear technology without any choice of techniques; the coefficients aij indicate the quantity of commodity i needed to produce one unit of commodity j. Letting Ki be the initial endowments of capital goods and of the corresponding services, ΔKi the quantities of the newly produced capital goods, Qi their purchase prices, Wi the rental rates, and r the rate of interest, the basic Walrasian model of capital formation is described by the following system of equations:

| (2.1) |

|

| (2.2) |

|

| (2.3) |

|

| (2.4) |

|

with i, j = 1, … M. Equations (2.1) state that the demand for the services of the available capital goods due to the new productions must be equal to their supply, which is inelastically determined by the arbitrarily given initial quantities of the different capital goods. The equality between cost of production and price in equations (2.2) represents the competitive condition of absence of extra profits. The non arbitrage condition of uniformity of the rates of return is introduced through equations (2.3), with the simplifying hypothesis that depreciation may be neglected. Finally, the equality (2.4) between savings — which, in the absence of any consumption activity, coincide with the entire income distributed in the form of rental rates to the owners of capital goods — and investment completes the model, that is thus composed of 3M + 1 equations in an equal number of unknowns. Because of the Walras Law, one of the equations is linearly dependent on the others; it is thus possible to determine only the relative prices of commodities. It is worth noticing that Qi represents both the value of the capital good Ki available at the beginning of the period considered — which belongs to the data of the problem — and the value of the same capital good available at the end of the period — which is, instead, part of the unknowns of the problem, being the sum of the initial quantity Ki and of the new production ΔKi. Notice, also, that le point de vue statique adopted by Walras makes it unnecessary to introduce a time index for the variables.

It has been observed, resuming a line of critique formulated in the 1930s to Cassel’s version of Walras’s general equilibrium theory, that the model (2.1)–(2.4) may not possess economically meaningful solutions; and particularly that the condition (2.3) of equality of the rates of returns on all capital goods may fail to be satisfied.4 Leaving this specific point for subsequent discussion, it is worth remarking here that linear programming and activity analysis techniques, developed some twenty years later in the early 1950s, have shown that an equilibrium solution can be proved to exist, provided that the strict equality signs adopted in the specification of equations (2.1)–(2.3) are substituted with ‘less than or equal’ signs and that the formulation of the model is accompanied by the appropriate slack conditions. The equilibrium solution resulting from these amendments to the original formulation of the theory may exhibit: (i) an excess supply of some of the arbitrarily given capital goods, with the consequence that for these goods the rental rates will be nil; and (ii) a cost of production of some capital goods in excess of the equilibrium price, with the consequence that the production of these goods will be not be undertaken. On account of either of these situations, conditions (2.3) may fail to hold as strict equalities. The need of a reformulation of equations (2.3) as weak inequalities now becomes apparent. If, on account of its double role, Qi is identified with the end of period price and in particular — as in the original formulation of the model — with the cost of production (supply price) of the newly produced capital good i, the inequalities are necessary to guarantee the internal consistency of the model. Specifically, they take care of the possibility that some capital goods may be unable to offer the market rate of return, either because the rental rate is nil or because the cost of production exceeds the price required for the rate of return to be equal to the market rate.

The main criticism of Walras’s theory of capital comes from economists working in the classical and Sraffian tradition. Garegnani (1990), in particular, has objected to the reformulation of the general equilibrium model with capital formation in terms of inequality constraints. He has argued that, if differences in the rates of return were to occur — as the theory so reformulated admits — there would be a tendency among maximising investors to concentrate their demand exclusively on those newly produced capital goods that ensure the highest rate of return. The composition of the initial stock would, therefore, turn out to be modified, with subsequent effects on equilibrium prices and quantities.

From these elements, Garegnani draws the conclusion that the modifications to be made to the Walrasian model of capital accumulation, in order to make sure that there will exist a solution, cause a departure from the notion of equilibrium that Walras had in common with all previous theory — the classical school and Marshall. Such a notion is centred on the identification of ‘normal’ or long-period values for prices and quantities, which are the result of the action of all persisting forces of the system and therefore able to represent centres of gravitation for the observed values of the economic variables. Among the persisting forces are naturally to be included those resulting from the rational behaviour of investors aiming at maximising the return on their assets. It is then argued that, since it is not possible to rule out the existence of meaningful equilibrium solutions to the Walrasian model (as modified by substituting inequality for equality constraints) in which the condition of a uniform rate of return may obtain only with reference to a subset of capital goods, the model itself is in general capable of identifying only a short-period equilibrium, contrary not only to the traditional tenets of economic theorising, but also and foremost to Walras’s own intentions.

Walras’s theory of capital formation would then be affected by an internal inconsistency between the choice of representing capital as a set of heterogeneous goods available in arbitrarily given quantities and the need to meet the competitive condition that the rates of return on all capital goods, determined with respect to the reproduction costs, be equal. The impossibility of realising the latter condition should thus be attributed to the fact that ‘the composition of the capital stock is not adjusted to the equilibrium outputs and methods of production’ (Garegnani, 1990, p. 21). The implications Garegnani draws from these considerations are very severe for the neoclassical general equilibrium theory of value. The only way in which it would be possible to determine a long-run position by means of a supply and demand analysis would be to conceive of capital, not as a set of heterogeneous goods, but as a single value magnitude, free to assume the form of any physical 35 capital good as required by the fulfilment of the condition of equality of the rates of return. The critique of the Wicksellian approach would then apply, thus leading to a complete dismissal of the demand and supply analysis of price formation.

In conclusion, Garegnani claims that a contradiction emerges between the alleged scope of the theory, namely to define a long-period position, and a consistent formulation of it, which is confined to yielding only a short-period equilibrium.

Walras, as if anticipating this line of critique, is in fact quite aware of the difficulties that may arise in meeting the condition of uniformity of the rates of return and, apparently, ready to abandon it, as it results from a passage in which he dwells on the order in which the different capital goods are produced as a means of eliminating the internal inconsistency of his model. ‘In an economy like the one we have imagined [namely with given quantities of capital goods], which establishes its economic equilibrium ab ovo, it is probable that there would be no equality of the rates of net income’ (Walras, 1954, p. 308). In that case, not all capital goods would be produced. There would be an obvious order: the first capital goods to be manufactured would be those yielding the highest rate of net income, while the production of the other capital goods yielding a lower rate of return would be nil. In terms that have by now become familiar, Walras is here clearly hinting at the possibility of a ‘corner’ solution, as opposed to an ‘internal’ solution, to the investors’ optimisation problem.

Is this to be considered an ‘unobtrusive’ admission conveying the ‘meaning of retraction’, as Garegnani (ibid., p. 20) maintains, or the recognition of the primacy of analytical rigour, when linear programming techniques had yet to be discovered?

According to Currie and Steedman (1990, p. 58), ‘it is hardly credible that Walras [faced with Garegnani’s objection] would have accepted [Garegnani’s proposed] reformulation of his approach’. I am inclined to take side with them and opt for a generous reading, that privileges analytical rigour as Walras’s foremost preoccupation and aim.

2.2 Taking account of Lindahl’s time factor

There clearly is a different and analytically more convincing way to recover the internal consistency of a general equilibrium model of capital formation. I observed elsewhere (Tosato, 1997) that the inconsistency of the Walrasian theory is not to be attributed to the assumption that the initial capital goods are arbitrarily given, but rather to the assumption that the beginning of the period purchase price of capital goods is set equal to the end of the period price, and in particular equal to the cost of production of the newly produced capital goods.5 With this assumption, the rate of return on every asset is identified with only one of its two components, namely with the own rate of interest. Markets, however, generally assign different prices to capital goods available at the beginning and at the end of the period. It is then the variation in relative prices thus allowed for that makes it possible to verify the condition of uniformity of the rates of return, no matter what the composition of the initial endowment of capital goods may be. Arbitrage opportunities would, otherwise, exist, which are not compatible with a situation of competitive equilibrium.

This consideration has a twofold implication. It shows, first of all, that the supply price of the newly produced capital goods — which is necessarily the end of period price of the complex of all capital goods, both inherited from the past and newly produced — cannot be, in general, the equilibrium price of the initially available endowments.6 Second, and more fundamentally, it leads to the observation that a correct formulation of the condition of uniformity of the rates of return requires that commodities, in particular capital goods, available in different periods be considered as distinct commodities, to which different prices ought to be assigned. This shows that Lindahl’s time factor, mentioned at the beginning of the section, truly lies at the heart of the problem and cannot be dismissed: the problems of capital formation are inexorably linked to the time factor and must accordingly be analysed in the context of a time horizon made up of a sequence of periods.

There are two roads available at this stage. They consist in setting, and therefore in reinterpreting, Walras’s theory of capital formation in the context of the methods of dynamic analysis proposed by Hicks (1939, pp. 115–40): the method of temporary equilibrium and the method of intertemporal equilibrium. Both methods generally envisage the time horizon of the economy as made up of a finite number of periods of equal length.

The temporary equilibrium method builds on the idea that, in the absence of generalised forward markets, it may be possible to take account of the time factor by considering the price expectations relative to the future time periods. In other words, the realistic assumption is made that agents replace the missing prices for future deliveries, which ought to result from transactions in the forward markets, with corresponding price expectations formulated on the basis of past experience and current prices. Current and expected future prices enable agents to define complete programmes relating to consumption and production, saving and investment, indebtedness and portfolio composition. A temporary equilibrium is then a situation in which there exist: (i) market clearing prices for all goods and services currently produced and exchanged; and (ii) a rate of interest that clears the asset market, namely makes consumers’ demand for assets to hold equal to the corresponding supply. Equilibrium prices and interest rate thus determined hold only for the current period; new temporary equilibrium prices and interest rates will rule in each of the following periods; only by chance will previous price expectations prove to be confirmed by subsequent equilibrium prices and interest rates.

With the temporary equilibrium method the economy is, therefore, described not only as ‘a network of interdependent markets, but as a process in time’ (Hicks, 1939, p. 116), namely as a sequence of temporary equilibria. The efficiency of the resulting process of intertemporary allocation of resources will depend, coeteris paribus, on the validity of agents’ expectations, that is on the degree to which expectations will approximate the prices that will subsequently turn out to be market clearing. The cost of the absence of complete forward markets is thus represented by the inefficiency of the overall allocative process; a sequence of temporary equilibria does not constitute an equilibrium in time.

The intertemporal equilibrium method is based on the notion of a ‘pure futures economy’ (ibid., p. 140). In other words, the assumption is made that in the economy there are complete forward markets so that agents, on the basis of the prices obtaining in those markets, can objectively evaluate their consumption and production programmes for the entire horizon. An intertemporal equilibrium is represented by a system of present value prices for all dated commodities that are market clearing in each of the time periods considered. In a pure futures economy, the entire horizon is telescoped into the present. In the present, i.e. in the current period, agents not only carry out contracts and exchanges concerning goods and services currently demanded and produced, but also specify all the obligations that they assume to deliver and receive goods and services in each of the future periods. There are thus no incentives to revise plans, to reopen the markets, to transact in asset markets. The economy ‘as a process in time’ is reduced to the mere execution of contracts, as all decisions have already been taken ab initio.

There are two interpretations of the intertemporal equilibrium model, which represent an alternative to the usual assumption of complete forward markets. The first, advanced by Lindahl in the 1929 paper, is based on the assumption of perfect foresight by the agents: ‘individuals in every concrete instance have such a knowledge of the conditions determining prices that they can let their sales and their demand be governed by the prices that are the result of these conditions’ (Lindahl, 1939, pp. 273–4). Hicks (1939, p. 140) believes that this approach meets with ‘awkward logical difficulties’. Currie and Steedman (1990, p. 115) think that these difficulties may be the same that had concerned Lindahl himself, ‘namely, [the difficulty] of reconciling the assumption that individuals know what future prices will be with the idea that future prices will be the result of the actions of those individuals’.

The second interpretation consists in supposing that there are spot markets in each of the periods considered and forward markets only for the numeraire commodity.7 In this instance, the price system is made up of two logically distinct components: (i) a system of forward prices, namely the prices — obviously in terms of the numeraire — to be paid in the initial period for the delivery of one unit of the same numeraire commodity in the various successive periods; and (ii) a system of prices for current delivery and consumption, in terms of the numeraire, in each of the periods considered. The first of these components plays the role of operating the intertemporal redistribution of incomes desired by the consumers, the second of attending to the clearing of the markets in the different periods. The usual indication of this latter component of the price system as a system of ‘spot prices’ ought not to deceive and lead one into thinking that the determination of those prices actually takes place in each of the periods to which they refer. If this were true, the agents would not be in a position to determine their consumption and production programmes. The agents must, in fact, know the entire price system in order to be able to decide, in particular, their behaviour in the forward markets of the numeraire. It is accordingly necessary to assume that agents have, from the very beginning, a unanimously shared expectation of the equilibrium spot prices that will obtain in each of the future periods. This second line of interpretation thus ends with joining the first and consequently faces the same type of critique.

The link with Lindahl’s ideas becomes even closer when Radner’s (1972) approach of equilibrium of plans, prices and price expectations in a sequence of markets is considered. Radner’s theory is based on a definition of perfect foresight that is more elaborate and more stringent than Lindahl’s: perfect foresight is defined as a situation in which agents’ behaviour is such as to determine a unique sequence of equilibrium prices in each of the different periods. The expectations, on the basis of which every agent formulates his plans, are represented by a function that determines a complete system of prices for every date in the horizon. Consumers’ and producers’ plans are mutually consistent if planned excess demands are nil on each date. An equilibrium of plans and price expectations is therefore defined by a common price expectation function and by a set of mutually consistent plans, such that each agent’s plan may be optimal for him, conditioned on an appropriate sequence of budget constraints. Radner’s approach is of particular interest in this context, as Mandler refers directly to it for his proposition of indeterminacy of sequential equilibria, which will be considered in Section 6.

It is clear that a pure futures economy, in which ‘everything is fixed in advance for a considerable period ahead’ (Hicks, 1939, p. 140), cannot offer the basis for an understanding of the behaviour of real economies in time. So, if the model of intertemporal equilibrium cannot avoid — from this point of view — a critique of sterility, it continues nonetheless to represent an unreplaceable benchmark for considerations of normative economics, as Hicks had pointed out, and an analytical reference for research in a general equilibrium context.

2.3 Walras’s theory of capital formation in a temporary equilibrium setting

Diewert (1977) offers an interpretation of Walras’s theory of capital formation in the context of the temporary equilibrium approach. In effect, he believes that Walras’s own theoretical construction can be read in this context: ‘Walras seems to have been the first to work out a relatively complete model of the temporary equilibrium in his model of capital formation and credit’ (p. 74). The element on which such an interpretation seems to be based is Walras’s assumption that the price of initially available capital goods is the same as the price of the newly produced ones. This statement is considered as expressing an assumption of static expectations, namely that the stock price of capital goods ruling in the subsequent period is the same as the current price. The reformulation proposed by Diewert raises, however, several queries with regard to the logical structure of the model and a more fundamental concern as to the appropriateness of the temporary equilibrium method as a tool for a reconsideration of Walras’s theory. It is not necessary to go into a detailed exposition of the complete model to show where the problems seem to lie.

Diewert introduces three stock or purchase prices of capital good i: Qi, Qie and Pi , which are, respectively, the price of the capital good available at the beginning of the period (i.e. of the already installed capital good), its expected price at the beginning of the subsequent period (or end of period price) and the price of the newly produced capital good or, for short, investment good. Letting Ci be the unit cost of production of the investment good, which is supposed to depend on the rental rates of all factors of production and on the prices of intermediate goods, the part of the model dealing with the relations between these variables is made up of the following equations:

| (2.5) |

|

| (2.6) |

|

| (2.7) |

|

Equation (2.5) is the competitive condition of absence of extra profits in the production of investment goods; (2.6) is the standard definition of the expected rate of return, as the sum of the percentage rental price and the percentage change of the expected price, when account is taken of Diewert’s implicit assumption that the rental rate is paid at the beginning of the period; finally, (2.7) expresses the idea that investment goods, which become pro ductive only at the beginning of the subsequent period, ensure a rental stream that lags one period behind that of the already installed capital goods, so that the price of investment goods must be equal to the discounted price of the already installed capital goods. Diewert suggests that, given the unit costs of production of investment goods, the rental prices Wi and the expected prices Qe, the above system of equations is in principle capable of yielding a solution for the remaining variables, namely the price Q of already installed capital goods, the price P of investment goods and the rate of interest r. This is all straightforward in the case of only one capital good, as in the example he works with the aim of offering an intuition of how a general proof of existence of solutions can be reached. Dropping the subscript i, which is superfluous with just one capital good, P is determined by (2.5); eliminating Q from equations (2.6) and (2.7) and given Qe and the rental price W, a nonlinear relation is obtained from which r can in principle be derived; at this point, (2.7) yields Q. Things are obviously much more complex in the case of several capital goods.

Quite apart from the analytical problems of showing the existence of a solution, it is the logical structure of Diewert’s model that deserves to be probed into. In fact, several problems emerge with reference to equation (2.7), which establishes a relation between the price Qi of the initially available capital goods and the price Pi of the newly produced capital goods (investment goods), which will become productive only at the beginning of the following period. As the flow of rental services generated by the latter begins with a delay of one period with respect to the flow generated by the former, equation (2.7) states that the ratio between the corresponding prices must be equal to the discount factor. This statement would clearly apply to the study of a path of balanced growth, in which the productive structure of the economy remains unchanged, as well as the relative prices. But this is certainly not the case under examination. The temporary equilibrium is an analytical tool conceived for the study of a situation in which the links with the past are ignored and the connections with the future are entrusted to price expectations. In a temporary equilibrium context, especially if applied to the problem of capital formation envisaged by Walras, there is no reason to suppose that the productive structure should remain unchanged, that the initially available capital goods should be fully utilised, or that the ratio between prices of capital goods available in successive periods should be equal to the discount factor.

If we keep in mind that the rental rate Wi is supposed to be paid at the beginning of the period, and the price Qi of the already installed capital goods is equally defined as a beginning of the period price, equation (2.7) actually determines the price of investment goods as a present value price at the same date. It is then proper to raise the issue concerning the relation between the present value price Pi of investment goods produced in the period considered and the expected price Qie of capital goods that will be available in the following period. The latter ought to be equal to the undiscounted price of investment goods, namely to Qi. How therefore can be explained a possible difference between Qi and Qie? Assume Qi > Qie; this implies that investors anticipate a capital loss. Nobody would then want to invest in capital good i, and its output would be nil. Assume, on the contrary, Qi < Qie; this implies that investors anticipate the opportunity of a capital gain. Everybody would want to buy such a commodity; demand would be infinitely large; and there would be no equilibrium. A straightforward application of the arbitrage principle to equilibrium prices leads to the conclusion that Qie must be equal to Qi. The assumption of static expectations appears therefore to be the only one consistent with the rest of the model.

If we impose this condition on expectations, the solution of the model turns out to be quite different from the one Diewert hints at. From (2.6), we obtain Qi = (1 + r)(Wi /r) and from (2.7) r = Wi /Ci , which is of course the standard result when changes in the values of commodities available at different moments in time are ignored, as Walras did by means of a direct assumption, and as Diewert does indirectly, through the hypothesis concerning expectations.

The conclusion that emerges from these considerations is that Diewert’s model of capital formation raises serious doubts as regard its logical consistency. The consequent failure to offer a credible reinterpretation of the Walrasian theory underlies, however, a more fundamental issue. As we saw, the method of temporary equilibrium builds on the notion that agents have expectations of prices that will rule in the following periods and make, on that basis, plans that are reconciled by the existing spot markets only for the current component. This notion represents an appropriate answer only to the first issue faced by Walras in his attempt to sterilise the time factor, but not to the second, namely to the problem of correct financial calculations. This takes us back to the problem earlier mentioned of the meaning to be attributed to Walras’s equations, which establish, as an equilibrium condition, the equality of the rates of return on all capital goods.

The problem that Walras’s construction faces is not a problem of how to generate future prices, but rather a problem of how to assign a value to the arbitrarily given quantities of capital goods, somehow inherited from the past and currently installed. It is not a problem of missing futures markets to be replaced by expectations of future prices, but a problem of missing spot markets for current assets, the initially given capital goods. The temporary equilibrium method is of no help to solve this problem. Granted that initially available durable goods that will turn out to be installed at the beginning of the following period must have, in the temporary equilibrium envisaged, the same price as that of the currently newly produced investment goods, the equality of the rates of return can be achieved by supposing that there are markets where the initially available capital goods can be traded. Agents who possess capital goods that, at given prices, would have a percentage rental price below that of other capital goods will try to sell them. Their prices will accordingly fall relative to their future prices, thus contributing to enhancing their net rate of return both by increasing the percentage rental price — if different from zero — and generating a capital value appreciation. When the prices of beginning and end of period capital goods are — as they should be — distinguished, the conditions of equality of the rates of return play the role of determining the values of the initially available capital goods. But, just looking one period ahead may not be sufficient for capital goods in large excess supply; an approach based on the intertemporal equilibrium method is indeed required at this stage.

2.4 Walras’s model of capital formation in an Arrow—Debreu economy

The following Sections 3 to 5 are dedicated to a reformulation of the Walrasian theory of capital formation in the setting of an intertemporal equilibrium model. It is nonetheless convenient to preliminarily consider two issues that are relevant to the subsequent formulation of the model. The first concerns the choice of the time horizon, the second the formulation of the condition of uniformity of the rates of return of the capital goods.

The Arrow—Debreu model examines the properties of the competitive allocation in a system of complete spot and futures market, in which demand and supply of dated commodities meet to determine present value equilibrium prices. Optimising agents take their decisions assuming these prices to be given. Consumers maximise an interemporal utility function subject to a single intertemporal budget constraint, encompassing the entire horizon, with the implication that wealth can be reallocated — through positive and negative savings — between the present and the future in a perfect capital market. Analogously, producers choose input—output combinations and carry out investment plans in view of maximising the sum of discounted future profits. In equilibrium, which is proved to exist, current consumption and production plans as well as saving and investment plans are mutually consistent.

With the device of considering commodities to be delivered in different periods as distinct goods, the Arrow—Debreu model reaches the goal of extend ing Walras’s static one-period approach to a multi-period approach. The general isationthus achieved is not, however, without a cost.

The Arrow—Debreu model typically envisages a finite horizon, so as to sidestep the analytical problems otherwise arising from the infinite dimension of the commodity space.8 This assumption raises, however, a specific issue, namely that of the determination of the terminal stocks of the capital goods. There are two alternative ways in which the required transversality condition can be formulated. One possibility is simply to assume that life materially comes to an end with the attainment of the horizon. In this instance, no consumer would want to reach the horizon with a positive wealth, and the appropriate assumption would then be of zero terminal stocks. At the opposite end stands the idea that somehow life continues after the attainment of the horizon. It would then make sense to provide for the ‘distant’ future and the ‘distant’ generations with a positive endowment of commodities, in particular of capital goods. In this case, at least some consumers would want to transverse the horizon with a strictly positive terminal wealth. This idea could be modelled introducing terminal wealth, subject to a nonnegativity constraint, in the utility function of consumers. Desired terminal wealth at the level of the economy as a whole could thus be determined. This approach would, however, not be adequate by itself to pin down the equilibrium configuration of the economy, as just any of an infinite number of compositions of terminal stocks would be compatible with a given aggregate terminal wealth. Aggregate terminal stocks of all capital goods but one would have, therefore, to be pre scribed from outside the model, with the remaining one being residually determined by consumers’ wealth decisions. This is the approach taken in the model developed in Section 3.

These considerations suggest a further remark. In one way or another, the assumption of a finite horizon introduces an arbitrary discontinuity in the flow of the economic process that must be filled with an ad hoc transversality assumption concerning variables defined only at the level of the economy as a whole. This circumstance does not appear to be easily reconcilable with an approach that aims at describing a decentralised process of market-oriented resource allocation.

In conclusion, the assumption of finite horizon shows clear limitations and must be considered acceptable only as a convenient shortcut to keep the mathematical techniques at that manageable level that has become standard in the study of general equilibrium theory.9

The second issue, concerning the formulation of the condition of uniformity of the rates of return, links up with the remark made in the introductory section of the paper, namely that the great generality of the Arrow-Debreu approach ‘conceals’ some relevant aspects of the theory of capital formation that are at the core of Walras’s theoretical construction and at the origin of the analytical problems dealt with in the preceding Section 2.1.

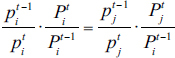

In the Arrow-Debreu economy, the non arbitrage condition, although not explicitly stated, is actually identically fulfilled by present value prices of the different commodities. In fact, present value prices have the property that the return on a loan in terms of good i must be equal to the return realized from the more complex operation of exchange at the beginning of the period of good i with good j, in the subsequent loan denominated in terms of goodj, and in the further retrade at the end of the period of goodj for good i:

| (2.8) |

|

where the small-letter pjt−1 and ptj denote the beginning and end of period present value prices. Remembering that the relative price of any two commodities in terms of discounted values is the same as in terms of undiscounted or current values, indicated by the corresponding capital letters (Burmeister, 1980, p. 13), we have

| 2.9 |

|

Rearranging terms, (2.8) becomes therefore

| (2.10) |

|

As the ratio of current to future discounted prices defines the own rate of interest, while the ratio of future to current undiscounted prices defines the rate of inflation in terms of the specific commodity considered, we can rewrite (2.10) as

| (2.11) |

|

where own rates ρi and inflation rates πi are defined over the time period t. By approximation, we finally obtain

| (2.12) |

|

which shows that: (i) the rate of return on any commodity, considered as an asset, is equal to the sum of the own rate plus the capital value appreciation or depreciation and (ii) the rates of return of any two commodities are equal.

The level at which they are equalised depends on the choice of numeraire. Let n be the numeraire commodity and r its own rate of interest. The properties defining the numeraire are that: (i) its undiscounted prices are equal to one in every period10 (Pnt = 1) and (ii) its discounted price at the beginning of the horizon, here t−1, is also equal to one (Pnt−1 = 1). On account of the first of these properties, the rate of return on the numeraire commodity is equal to its own rate of interest

| (2.13) |

|

which in equilibrium is the common rate of return of all commodities. Then, letting j be just any commodity, from (2.12) and (2.14), the non arbitrage condition implicit in the Arrow—Debreu model takes the form

| (2.14) |

|

As is clear from the above derivation, in the Arrow—Debreu approach, the own rate of interest is defined with exclusive reference to the discounted prices to a given commodity. When the commodity considered is, however, a capital good, the usual way to define the own rate of interest is not through the ratio of the current to the future discounted purchase price of the durable good, but rather through the ratio of the rental rate of the service supplied by the capital good (which is a flow variable) to the purchase price of the capital good (which is a stock variable). Following this more conventional approach, the percentage rate of return on any capital good j must then satisfy, in equilibrium, the non arbitrage condition expressed in terms of undiscounted prices

| (2.15) |

|

where the first term in the right-hand side of (2.15) is the undiscounted rental rate, which is supposed to be paid at the end of the period, as a percentage of the initial purchase price, and the second term is the percentage capital gain or loss on the purchase price of the asset. Using equations (2.9) and the definition (2.13) of the own rate of interest on the numeraire commodity, (2.15) can be expressed in terms of present value prices and rental rates11 as

| (2.16) |

|

The relationship between the conventional and the Arrow—Debreu way of defining the own rate of interest can now be readily derived from equation (2.16). Rearranging terms, we obtain

| (2.17) |

|

This shows that the ratio of the rental rate to the purchase price is indeed equal to the own rate of interest, when account is taken of the different times to which the variables refer.

Equation (2.16) suggests two further considerations. First, the formulation of the condition of uniformity of the rates of return does not require us to think in terms of a rate of interest. The common interest factor is implicit in the use of present value prices; the equality of the rates of return is thus expressed with the sole reference to the asset prices and the rental rates of each capital good. This may appear at first sight odd, but it really is not. The variables — asset prices and rental rates — relating to each capital good incorporate all the information required for an efficient allocation of resources. This means that, in equilibrium, consumers may safely hold their wealth in just any capital good.12 Second, and most important, (2.16) exhibits the relation of interdependence that links, in equilibrium, the rental rate to the purchase prices of capital goods. It is this interdependence, which is specific to capital goods, that is not made explicit in the Arrow—Debreu approach, and its role will be investigated in the following sections of the paper.13

I have suggested (Tosato, 1997) that the different way to express the own rate of interest in the Arrow—Debreu model as compared with Walras’s theory may simply reflect a difference in the classification of commodities: the accent being on the distinction between commodities available in different time periods, in the former; between capital goods and their services, in the latter. In effect, the conclusion could be somewhat sharper, in the sense that the omission of equation (2.16) implies that the specific nature of capital goods is not properly recognised in the standard formulation of the intertemporal general equilibrium model: prices of capital goods and of their services cannot be independently determined.

3 The model

3.1 Description of the economy

We consider a two-period economy; the generalisation of the model to any finite number of periods is straightforward. With a notation consistent with that used in the preceding sections of the paper, beginning of the period variables are indicated with the superscript t − 1 to distinguish them from the end of period variables, which are denoted by the superscript t. We suppose that there are complete spot and forward markets, which are open at the beginning of the horizon considered, i.e. at time t = 0. Obligations entered into at t = 0 are subsequently carried out at the end of period 1 and in period 2.

The production process taking place in each period is of the point-input—point-output type. Inputs, represented by the services of M capital goods and N primary factors of production, e.g. various types of labour, are applied at the beginning of each period, while outputs, represented by L consumption goods and M newly produced capital goods, are obtained — in a sense that will be clarified — at the end of each period. We make the usual assumption that one unit of any productive resource generates one unit of service and suppose, for simplification, that there is no depreciation on capital goods. No pure intermediate goods are considered; Kehoe (1982) has, however, shown that the model can be generalised to also encompass this case. Firms maximise profits at given market prices in the production set determined by the known technology.

At the beginning of the horizon (t = 0), consumers have strictly positive endowments of M capital goods km0(m = 1, 2, …, M) and of N primary factors of production (labour) ωn0 (n = 1, 2, …, N) and will have new endowments ωn1 of the same primary factors at the beginning of period 2. We assume that consumers do not have a reservation demand for the services of their endowments and maximise an intertemporal utility function.

For the purpose of defining consumers’ behaviour, we assume that consumers rent to the firms the services of their primary factors, for which we obviously do not envisage the possibility of selling the corresponding human capital. This possibility exists, however, for capital goods, so that there are alternative ways — corresponding to alternative institutional arrangements of the working of the economy — in which the individual budget constraint can be constructed.

We could think that consumers lease to the firms only the services of the initial capital goods constituting their endowment, purchase at the end of period 1 the newly produced capital goods and rent again — now at the beginning of period 2 — the services of the old and of the new capital goods and purchase at the end of the same period the capital goods currently produced. But, if we were to adopt this approach, it would be necessary to model consumers’ demand for capital goods also at the end of period 1, and this would substantially require us to operate with separate budget constraints for each of the two periods.

We could, alternatively, suppose that, at t = 0, there exists a market for capital goods in which consumers sell to firms their initial endowments in exchange for financial assets, say bonds, that earn the market rate of return.14 Consumers then carry out the subsequent wealth adjustments necessary to realise their optimal consumption programme in the two periods, in terms of financial wealth; each consumer can thus either reduce his initial wealth, selling, with delivery at the end of period 1, part of his initial stock of bonds or increase it, buying forward either old bonds from other consumers or, from firms, the new bonds representing the value of newly produced capital goods. Note that in this approach firms maintain, at the beginning of period 2, the ownership of the capital goods purchased at t = 0 and of the investment goods produced in period 1. Only at the end of the two-period horizon do all capital goods — the initial ones plus the newly produced ones — return into the possession of the consumers in exchange for the bonds issued by the firms at t = 0 and at t = 1. This requires that the budget constraint at the individual and at the market levels be appropriately defined.

The approach now considered has two main advantages. First, it easily accommodates the possibility for any consumer to reduce, if he so desires, his initial wealth. Second, there is no need to model consumers’ demand for capital goods at the end of period 1, but only the economy’s demand for capital goods at the end of period 2: and this, as discussed in Section 2.4, is made up of the desired terminal stocks of all capital goods but one, which is residually determined by consumers’ wealth decisions. The absence of a demand for end of period 1 capital goods requires, however, an appropriate formulation of the technology matrix, so that the investment goods produced in period 1 be available, together with those produced in period 2, to be transferred to the consumers only at the end of the horizon.

The definitions adopted here of consumers’ net demand functions and firms’ net supply functions reflect this second approach. We will show that, with the non arbitrage condition, the formulation of consumers’ aggregate budget constraints in terms of sale of the initial stocks is equivalent to supposing that consumers rent the services of the initial endowment of capital goods to the firms for the two-period horizon and receive, in each period, the corresponding rental rates.

3.2 Consumers’ behaviour

We are going to model consumers’ behaviour in terms of properties of market demand functions rather than in terms of properties of individual utility and demand functions. It is nonetheless useful to go through the exercise of deriving the individual budget constraint in present value terms and show the connection between this formulation and that of the constraint that must be met by market demand functions. Using Kehoe’s (1980) terminology, this constraint — which we will, for short, call the market budget constraint — represents a formulation of Walras’s law with reference to the consumer side of the economy.

Let cht be the flow vector of consumption goods (l = 1, 2, …, L) available to consumer h (h = 1, 2, …, H) in period t, and Aht be the stock of net wealth of consumer h at the end of period t. Let Pt and Qt be the current value purchase prices of consumption goods and end of period capital goods; Wt and Vt the current value rental rates, respectively, of capital goods and primary factors. Let also the corresponding lower-case letters aht, pt, qt, wt and vt stand, respectively, for the present value of net wealth and the present value purchase prices and rental rates. We can write the budget constraints faced by a typical consumer in periods 1 and 2 as

| (3.1) |

|

| (3.2) |

|

where r1 and r2 are the market rates of return, Q0·kh0 is the consumer’s initial wealth, and Ah2 is his terminal wealth.15 The resulting intertemporal budget constraint, as of t = 0, is

| (3.3) |

|

This intertemporal budget constraint (3.3) can be transformed from current value purchase prices and rental rates to present value purchase prices and rental rates, obtaining16

| (3.4) |

|

Individual demands,17 exhibiting nonnegative entries for commodities received by the consumer and nonpositive entries for the value of the capital goods sold and the services of labour rented to the firms, are represented by the vector (ch1, ch2, ah2, q0·kh0, −ωh0, −ωh1). The optimal choice depends on the price vector (p1, p2, q0, v1, v2). Notice that we can consider the difference ah2 − q0·kh0 as the individual net demand for wealth to hold at the end of the horizon.

As we move from the individual to the market level, account must, however, be taken of the institutional setting previously described — regarding consumers’ sale of capital goods at the beginning of the horizon to the firms and consumers’ purchase from firms of the stocks available at the end of the horizon — and of the transversality conditions regarding terminal stocks mentioned in Section 2.4. At the individual level, the initial endowment of k0 capital goods enters the budget constraint as initial wealth; at the market level, as the economy’s endowment of capital goods, transferred to the firms for the two-period horizon. This means that consumers as a whole have a net offer of capital goods at the beginning of period 1, which is repeated at the beginning of period 2. At the end of the horizon, old and newly produced capital goods are sold by the producers to the consumers, with the implication that terminal wealth of the economy must be equal to the value of the terminal stocks of the various capital goods

| (3.5) |

|

with k2 ≥ 0.

Turning now to the transversality condition, the remarks made in Section 2.4 become at this stage relevant, namely that M − 1 terminal capital stocks must be exogenously fixed, while the Mth one is residually determined by consumers’ wealth decisions. The vector of desired terminal stocks can thus be specified as

where the vectors ![]() 2 and

2 and ![]() 2 coincide with the vectors k2 and q2 after dropping the last element, and

2 coincide with the vectors k2 and q2 after dropping the last element, and ![]() 2 denotes the prescribed terminal stocks of the first M−1 capital goods. Letting now z = k2 − k0, the net demand for terminal capital goods can be expressed as

2 denotes the prescribed terminal stocks of the first M−1 capital goods. Letting now z = k2 − k0, the net demand for terminal capital goods can be expressed as

| (3.6) |

|

Market demands are then represented by the J = 2L + 3M + 2N vector function

| (3.7) |

|

where the f(·) terms are the components expressing the demand for consumption goods and terminal stocks, and the other terms are the supply to firms of the initial capital stocks for two periods and of the services of labour.

Aggregating the individual budget constraints (3.4), we have

| (3.8) |

|

which, taking account of (3.5) and of the definition z = k2 − k0, becomes

| (3.9) |

|

To make the aggregate budget constraint consistent with the formulation of the market demand functions, it is necessary to consider the non arbitrage condition (2.16). Repeated application of the latter yields the relation q0 − q2 = w1 + w2. Substituting in (3.9), we finally have

| (3.10) |

|

which is in line with the description (3.7) of the market net demands. This shows that the market budget constraint that consumers’ net demands must satisfy can be formulated in two equivalent ways: the first — equation (3.8) — stresses the circumstance that consumers sell their initial endowment of capital assets to the firms and buy them back only at the end of the horizon; the second — equation (3.10) — points, more traditionally, at the fact that consumption and net terminal stocks decisions are constrained by consumers’ income as determined by renting the services of the endowments of the initial capital stocks and labour.

Let (π, Φ) be the vector of present value prices and rental rates, with components π = (p1, w1, v1, p2, q2, w2, v2) ∈ R+J and Φ = (q0, q1) ∈ R+2M. In view of (3.10), market demands (3.7) are a function of the subset of prices π and thus a mapping f: R+j → RJ.

We make the following assumptions on consumers’ demand functions:

(A.1) Differentiability. Let Z denote a subset of the boundary of the price set R+J, including the origin, defined as Z = H ∪ {0}, with H = {π ∈ R+J|p1 = p2 = q2 = 0}. Then, f(π) is a continuously differentiable function defined on the domain R+J/Z.

(A.2) Boundedness from below. f(π) is bounded from below on R+J/Z, withfc1(·), fc2(·), fz2(·), ≥ 0.

(A.3) Desirability of commodities. If πi → π with πi ∈ R+J/Z and π ∈ Z/{0}, then ||f(πi)|| → ∞.

(A.4) Homogeneity. f(π) is homogeneous of degree zero.

(A.5) Walras’s law. f(π) satisfies the aggregate budget constraint (3.10), that is 3.11 π·f(π) = 0

Assumptions (A.3), (A.4) and (A.5) are standard, while (A.2) underlies that fact that endowments are finite and that a negative demand for consumption goods is meaningless, as would be a negative demand for net wealth acquisition when a reduction of the initial capital stocks is not physically possible. Assumption (A.1) on the contrary — taken over from Kehoe (1982) — requires explanation. The presence of endowments of capital goods and primary factors of production unelastically supplied by the consumers requires special care in the formulation of the differentiability assumption. Suppose that the only positive prices are the purchase prices of initial capital goods and the rental rates of the primary factors of production; then, if f(π) is in fact continuous, we would have a violation of the aggregate budget constraint (3.10). Note that, on account of (A.3), equilibrium could never occur on the part of the boundary of the price set that has been excluded. Note further that the possibility that some of the endowments will not be fully utilised is not ruled out.

3.3 Production activities

We consider a production technology of the linear activity analysis type without joint production (Koopmans, 1951). As is usual with a constant returns to scale technology, the specification of the production set of individual firms is irrelevant for the study of equilibria; all that matters is the aggregate technology.

The production technology of the economy is described by the (2L + 3M + 2N) × (2![]() + 2

+ 2![]() + 2M + 2N) block matrix A

+ 2M + 2N) block matrix A

| (3.12) |

|

Positive coefficients refer to outputs, and negative coefficients refer to inputs; empty entries indicate blocks of zero coefficients.

The form attributed to the technology matrix is unusual and needs explanation. The blocks in the first three rows refer to outputs and inputs, respectively, made available and used in period 1; the blocks in the last four rows refer to outputs and inputs made available and used in period 2. The blocks in the first four columns refer to activities carried on in period 1, the remaining four columns to activities performed in period 2. Reading the matrix by columns, it is convenient to start from the latter. Activities in period 2 have no outputs or inputs referring to period 1: this accounts for the blocks of zero coefficients in the upper part. As regards the lower part, the first two columns, i.e. columns five and six of the matrix A, indicate the set of ![]() ≥ L activities producing consumption goods and the

≥ L activities producing consumption goods and the ![]() ≥ M activities producing new capital goods, while the final two columns denote the free disposal activities of the services of capital goods and primary factors. As we have assumed that there are no initial endowments of consumption goods and newly produced capital goods, there is no need to consider disposal activities also for these commodities.

≥ M activities producing new capital goods, while the final two columns denote the free disposal activities of the services of capital goods and primary factors. As we have assumed that there are no initial endowments of consumption goods and newly produced capital goods, there is no need to consider disposal activities also for these commodities.

As to the first four columns of the matrix A, column one refers to the production of consumption goods, which is self-contained in period 1, as are the disposal activities of columns three and four. Column two reflects the assumption that capital goods effectively produced in period 1 are actually received by the saving consumers only in period 2. The production activity described by column two of the matrix A uses inputs −A32 and −A42 of services of initial capital goods and primary factors and produces investment goods that are, by assumption, available for sale to the consumers only in period 2 (and this accounts for the first entry A22 in the lower part of column two), and services of these capital goods that can be used for production purposes in period 2 (and this accounts for the second A22).

Let y = (yc1, yz1, yk1, yω1; yc2, yz2, yk2, yω2) be a vector of nonnegative activity levels. Aggregate net production, or net supply, is then Ay, and net profits are π·Ay. The output of investment goods is, accordingly, A22yz1 + A22yz2, demand for services of capital goods in period 2 is A22yz1 − A31yc2 − A32yz2 − Iyz2 where the positive term A22yz1 indicates the contribution of the first-period production of investment goods to meet the second-period demand for services, and net profits of the activities that produce investment goods in period 1 are − w1·A32 − v1·A42 + q2·A22 + w2·A22.

We make the following standard assumption about the matrix A.

(A.6) Boundedness. No output is possible without input, i.e. {x ∈ RI | x = Ay ≥ 0, y ≥ 0} = {0}, with I = 2(![]() +

+ ![]() + M + N) . Equivalently, there exists a strictly positive price vector π such that π·A < 0, i.e. unit profits are negative.

+ M + N) . Equivalently, there exists a strictly positive price vector π such that π·A < 0, i.e. unit profits are negative.

3.4 Equilibrium

An equilibrium for the economy described by the net demand functions f and by the technology matrix A − in short the economy (f, A) — is a price vector (![]() ,

, ![]() ) ∈ R+J × R+2M/Z that satisfies the following conditions:

) ∈ R+J × R+2M/Z that satisfies the following conditions:

(i) there exists ![]() ≥ 0 such that f(

≥ 0 such that f(![]() ) = A

) = A![]() ;

;

(ii) ![]() · A ≥ 0;

· A ≥ 0;

(iii) purchase price and rental rates of capital assets satisfy the non arbitrage condition ![]() t−1 = ŵt +

t−1 = ŵt + ![]() t with t = 1, 2;

t with t = 1, 2;

(iv) (![]() ,

, ![]() )e = 1, where e is a vector of all one.

)e = 1, where e is a vector of all one.

Condition (i) requires that consumers’ net demand be equal to producers’ net supply. Condition (ii) means that no activity makes positive profits in equilibrium. Condition (iii) is the competitive condition of uniformity of the rates of return on all assets previously defined in equation (2.16). It is convenient to write the non arbitrage conditions in matrix form. Accordingly, let B and C be the block matrices, respectively, of dimensions J × 2M and 2M × 2M:

| (3.13) |

|

We can then write (2.16) as

| (3.14) |

|

Condition (iv), finally, is the normalisation rule.

The non arbitrage condition has already been extensively commented. Here it may be nonetheless useful, returning to an issue discussed in Section 2.1, to reconsider the role of the non arbitrage condition for capital goods in temporary or permanent excess supply. If a capital good m is in excess supply over the entire horizon, its rental rate wmt is always nil, and so are the purchase prices qmt. Such a capital good is not an economic good and could be dropped from consideration without altering the equilibrium configuration of the economy. If a capital good m is, on the contrary, only temporarily in excess supply, obviously in the initial stages of the horizon, its rental will at a certain point become positive, say from period τ onward. Equation (2.16) would then imply that the purchase price qmτ−1 must also be positive, as will be all the preceding purchase prices qmt, down to the very beginning of the horizon. This means that a capital good in temporary excess supply is always an economic good in view of its future scarcity.

4 Existence of equilibrium

To prove the existence of equilibrium, we take advantage of an analytical construction due to Todd (1979) and used by Kehoe (1980) to construct a continuous, single-valued mapping of the price set to itself, whose fixed points are equivalent to equilibria of the economy (f, A).

Let Δ be the unit simplex

| (4.1) |

|

Because of the homogeneity assumption (A.4), we can restrict attention to demand functions f(π) defined on Δ/Z.

The first step to take is to extend the definition of these demand functions on the entire price set Δ. This can be done, as Kehoe (1982) shows, using appropriate techniques. We will take this result as given and consider henceforth the net demand functions f(π) to be defined on Δ.

Consider now the subset ΔA ⊂ Δdefined by

| (4.2) |

|

As the intersection of closed and convex sets, ΔA is a non-empty, closed and convex subset of Δ. To help the intuition, we give in Figure 6.1 an idea of the subset ΔA. Consider the four-components price vector (p1, q1, w1, q0). Using the normalisation rule p1 + q1 + w1 + q0 = 1, the four-dimensional simplex can be reduced to the three-dimensional tethraedon ABCO, whose vertices are, respectively, the points p1 = 1, w1 = 1, q1 = 1 and q0 = 1. Consider then the non-positive profits constraint p1a11 − w1a21 ≤ 1. This reduces the admissible region to the truncated volume

Figure 6.1

A1B1C1OBC. Rewriting the non-arbitrage condition q0 = w1 + q1 as 1 = p1 + 2w1 + 2q1, it is seen that this in turns restricts the admissible region to the triangle AB2C2. The intersection of these two admissible regions is the shaded area B2C2C3B3, i.e. ΔA.

Let N be any nonempty, closed and convex subset of RN. Consider the projection map pN: RN → N defined by the rule that associates any point x ∈ RN with pN(x), which is closest to x in terms of Euclidean distance. In view of the assumed convexity of N, the mapping pN is continuous.

Using this idea, define now the map g: Δ → Δ by the rule (see Figure 6.2)

| (4.3) |

|

As composition of two continuous maps, g(π, Φ) is also a continuous map, in fact a continuous map of the nonempty, compact and convex set into itself, which by Brouwer’s theorem has some fixed points.

Figure 6.2

Proposition 1. (![]() ,

, ![]() ) is an equilibrium for the economy (f, A) if and only if is a fixed point of the map g(π, Φ).

) is an equilibrium for the economy (f, A) if and only if is a fixed point of the map g(π, Φ).

We begin by showing the sufficiency part of the proposition, i.e. that, if (![]() ,

, ![]() ) is a fixed point, it is also an equilibrium. By definition of projection map, (ψ,

) is a fixed point, it is also an equilibrium. By definition of projection map, (ψ, ![]() ) = g(π, Φ) is the unique solution to the quadratic programming problem

) = g(π, Φ) is the unique solution to the quadratic programming problem

| (4.4) |

|

subject to

| (4.5) |

|

| (4.6) |

|

| (4.7) |

|

where the constraints of the optimisation problem reflect the equilibrium conditions (ii)–(iv). Thus a fixed point is an equilibrium if condition (i) is also satisfied.

By the Kuhn—Tucker theorem, there exists nonnegative multipliers y and multipliers λ and μ such that the solution to the programming problem (4.4) must satisfy the following conditions:

| (4.8) |

|

| (4.9) |

|

| (4.10) |

|

Now, let (![]() ,

, ![]() ) be a fixed point of the map g(π, Φ), and

) be a fixed point of the map g(π, Φ), and ![]() ,

, ![]() ,

, ![]() are the associated values of the multipliers. This means ψ =

are the associated values of the multipliers. This means ψ = ![]() and

and ![]() =

= ![]() , so that (π, Φ) satisfies the following conditions:

, so that (π, Φ) satisfies the following conditions:

| (4.11) |

|

| (4.12) |

|

| (4.13) |

|

Multiplying (4.11) by ![]() and (4.12) by

and (4.12) by ![]() and summing, we obtain

and summing, we obtain

| (4.14) |

|

Observe now that, as a solution to the problem (4.4), (π, Φ) satisfies the nonarbitrage condition ![]() ·B =

·B = ![]() ·C and, in view of assumption A.5,

·C and, in view of assumption A.5, ![]() ·f(

·f(![]() ) = 0. As a consequence of these properties and of condition (4.13) (the Kuhn—Tucker condition), (4.14) becomes

) = 0. As a consequence of these properties and of condition (4.13) (the Kuhn—Tucker condition), (4.14) becomes

| (4.15) |

|

which, on account of (4.7), has a unique solution ![]() = 0. Substituting in (4.12), we obtain

= 0. Substituting in (4.12), we obtain ![]() = 0. We thus see that a fixed point satisfies conditions

= 0. We thus see that a fixed point satisfies conditions

| (4.16) |

|

| (4.17) |

|

which show that the fixed point (![]() ,

, ![]() ) is a competitive equilibrium with zero profits.

) is a competitive equilibrium with zero profits.

To prove the necessary part of proposition 1, we show that, if (![]() ,

, ![]() ) is an equilibrium, then it is also a fixed point. Let (

) is an equilibrium, then it is also a fixed point. Let (![]() ,

, ![]() ) be a competitive equilibrium. This means that it satisfies the equilibrium conditions (i)–(iv), i.e. f(

) be a competitive equilibrium. This means that it satisfies the equilibrium conditions (i)–(iv), i.e. f(![]() ) = A

) = A![]() ,

, ![]() ·A ≤ 0,

·A ≤ 0, ![]() ·B =

·B = ![]() ·C and (

·C and (![]() ,

, ![]() )e = 1. We have to show that it also satisfies the conditions (4.16) and (4.17) for a fixed point. Now, (4.16) is satisfied by definition of equilibrium and (4.17) from (4.16) and Walras’s law. Therefore, f(

)e = 1. We have to show that it also satisfies the conditions (4.16) and (4.17) for a fixed point. Now, (4.16) is satisfied by definition of equilibrium and (4.17) from (4.16) and Walras’s law. Therefore, f(![]() ) = A

) = A![]() , and (

, and (![]() ,

, ![]() ) ∈ ΔA is equivalent to (

) ∈ ΔA is equivalent to (![]() ,

, ![]() ) = g(

) = g(![]() ,

, ![]() ).

).

As we have just seen, ![]() = 0 at any fixed point, with the implication that the constraint represented by the non arbitrage conditions is not binding inasmuch as fixed points must satisfy the constraint. In other words, the non arbitrage conditions (3.14) simply determine the purchase price of capital goods q0 and q1, given p2, w1 and w2. This circumstance confirms, in the context of a formal analysis, the validity of the conclusion reached in Section 2.3. The non arbitrage conditions only play the role of determining appropriate, i.e. equilibrium, prices for the initial capital stocks, while the end of period purchase prices are determined by the competitive conditions concerning the newly produced goods. The interesting aspect that the two-period model reveals is that the nonpositive profit constraint is relevant for the determination of the equilibrium configuration only with regard to the final period of the horizon. The competitive conditions concerning the production of new capital goods in the remaining intermediate periods is implicitly taken care of by the condition of uniformity of the rates of return.

= 0 at any fixed point, with the implication that the constraint represented by the non arbitrage conditions is not binding inasmuch as fixed points must satisfy the constraint. In other words, the non arbitrage conditions (3.14) simply determine the purchase price of capital goods q0 and q1, given p2, w1 and w2. This circumstance confirms, in the context of a formal analysis, the validity of the conclusion reached in Section 2.3. The non arbitrage conditions only play the role of determining appropriate, i.e. equilibrium, prices for the initial capital stocks, while the end of period purchase prices are determined by the competitive conditions concerning the newly produced goods. The interesting aspect that the two-period model reveals is that the nonpositive profit constraint is relevant for the determination of the equilibrium configuration only with regard to the final period of the horizon. The competitive conditions concerning the production of new capital goods in the remaining intermediate periods is implicitly taken care of by the condition of uniformity of the rates of return.

The existence of equilibrium of the intertemporal model under consideration can therefore be analysed eliminating altogether the variables Φ, which do not play a role in the determination of demand and supply functions, and concentrating the attention uniquely on the subset of prices π. Adopting a normalisation rule limited to this subset of prices, let

| (4.18) |