Savings, investment and capital in a system of general intertemporal equilibrium

Pierangelo Garegnani†

1.1 Introduction

1. The criticism of the neoclassical theory based on the inconsistency of the concept of a ‘quantity of capital’ has been met from the orthodox side essentially with the claim that contemporary reformulations of the theory do not rely on any such concept.1 The present chapter is intended to show that the claim is unfounded and that the deficiencies of the concept undermine the reformulations no less than they do the traditional versions.2

In Section 1.2 we shall introduce for this purpose, the very simple model of intertemporal equilibrium which Hahn put forward in 1982 to counter what he took to be the ‘neo-Ricardian’ critique. This model will allow us to bring out the decisions to save and to invest of any ‘year’ which are implied in an intertemporal general equilibrium (GE).3 In Section 1.3 we shall then define what can be described as the ‘general-equilibrium saving-supply schedule’ and the ‘general-equilibrium investment-demand schedule’ for such a ‘year’. The detailed determination of those schedules — which may be left aside at a first reading — has been postponed to Appendix I and to the Mathematical Note attached to the chapter. Section 1.4 will examine the general information which the schedules provide about the behaviour of the system, while Section 1.5 will deal with the effects on investment demand of changes in techniques and in consumption outputs as intertemporal prices change.

The above will enable us to approach in the final section the question of how a ‘quantity of capital’ enters intertemporal equilibrium. That will involve pointing out first how misleading can the idea be that the adjustments in intertemporal consumptions (i.e. in decisions to save and invest) raise no more problems than adjustments in contemporary consumption do.4 Whereas the latter imply a shift of resources between the respective contemporary productions and can be activated directly by the disequilibrium prices, the analogous disequilibrium in intertemporal prices (own rates of interest), due, for example, to excess savings, can only adjust the respective intertemporal productions indirectly, through the intermediate link of an incentive given to entrepreneurs to change methods of production and/or relative consumption outputs, so as to increase the ‘amount of means of production’ relative to labour and other primary factors employed in the economy in that year. The corresponding additional investment is indeed what should, on the one hand, absorb in the production of the capital goods, the resources of time (t − 1) set free by the additional savings of t and, on the other, increase the productivity of primary factors in (t + 1), (t + 2), etc. to provide for the future increased consumption which the savers have planned. It will then be seen how the impossibility of measuring that ‘amount of means of production’ independently of distribution entails that no such ‘increase’ in means of production needs to follow from the competitive fall of the prices of commodities of early, relative to those of later dates (fall of the respective own rates of interest) caused by excess savings. The conclusion will thus be that treating under the same heading inter temporal and contemporary consumptions can obscure, but not do away with the differences between the two cases — the “quantity of capital” re-emerging essentially unchanged in its relevance, and in its deficiencies, for the determination of the equilibria. Indeed in proportion to their value, heterogeneous capital goods are for savers perfectly substitutable means of transferring purchasing power over time, so that savers’ decisions about capital goods will refer to that ‘quantity’,5 which will accordingly have to be implicitly or explicitly present in the system like that of any other good on which individuals exert their demand and supply decisions.

Appendix II completes the chapter by examining some flaws in the mathematical argument Professor Hahn has conducted in his 1982 article. Those flaws will allow bringing out some misunderstandings which appear to have seriously hindered communication between the two sides in the course of the capital controversies.

Our analysis of general equilibrium will be conducted by analytical instruments, other than excess demands generated by treating all prices as independent variables and used since Hicks (1939). As indicated, we shall use ‘general equilibrium demands and supplies’ of particular commodities or factors, assuming that all markets other than the specific ones on which we focus our attention are in equilibrium.6 An equilibrium in the particular market considered will then imply an equilibrium of the whole system. The advantage of these instruments is the possibility they offer to trace the effects of peculiarities of that market on the general equilibrium and its properties. Thus we shall here centre on those commodity markets which constitute the savings-investment market, and study the effects of the phenomenon of ‘reverse capital deepening’ which directly affects such markets. The reader is thus asked for some effort in entering a less familiar method of analysis, which however, we hope, may turn out to allow for some novel results and for a better economic grasp of key phenomena affecting a general intertemporal equilibrium. In particular, the reader should try to take these unfamiliar instruments on their logic, and resist the temptation to translate them too quickly into the language with which he is more familiar.

1.2 Decisions to save and invest in a system of intertemporal general equilibrium

2. To have a first, bird’s eye view of the ground we shall travel, it might be useful briefly to focus our attention back on the traditional versions of the theory. We need to consider the seeming contradiction between the varying physical capital underlying the demand function and that underlying the supply function for capital,7 the single ‘factor’ characterising those versions.8 For the sake of a definite example we may refer to Wicksell’s “Lectures” (1901) where a ‘quantity of capital’ demanded, expressed as a value in terms of consumption goods, is equalised to the economy’s endowment of it (loc. cit. vol. I, 204–205).

The seeming contradiction lies in the fact that, whereas in the demand schedule the physical capital which the quantity K demanded at each interest rate should express is that corresponding to the techniques and outputs most profitable at such a rate and changes with it, the physical capital making up the supply, or endowment of K is the stock in existence in the economy and will of course generally differ physically from the unknown one of the equilibrium to be determined. Thus, while in equilibrium ‘quantity’ demanded and supplied of ‘capital’ are equal, the two apparently refer to altogether different aggregates of capital goods.

However, clearly, this contradiction is only apparent: what is in fact meant in the supply schedule of ‘capital’ is that the physical form of the stock appropriate to the equilibrium position will be assumed by the existing stock over a period of time as, each ‘year’, a part of the capital goods in existence has to be replaced and a corresponding proportion of the labour force is set free to be re-equipped by investing the gross savings of the year.9

The implications of this for us here are important. The demand and supply schedules for ‘capital’ (the fund) envisaged in Wicksell and the other traditional writers for their equilibria, were in fact intended to analyse forces supposed to operate through the demand for gross investment, and the supply for gross savings (the flows). The attention was concentrated on the fund (capital) rather than the flow (savings-investment) concepts, in order to analyse that key case of substitution of factors in a purer form, undisturbed by the monetary and other phenomena which would have interfered when dealing with a savings-investment market. Now, once that is made clear, it should also be clear that all the phenomena traditionally treated by means of the ‘quantity of capital’, and therefore the ‘quantity of capital’ itself, cannot be absent in the new intertemporal versions of the theory, where each ‘year’ will of course entail investment and savings.10

Our task now will therefore be, first of all, to render explicit the savings supply and investment demand which pertain to each ‘year’ in the equations of general intertemporal equilibrium: this will be done in this section, leaving for the next the presentation of the method we shall use for analysing their changes as prices vary in the intertemporal system.

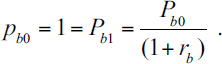

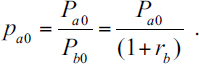

3. A very simple model will suffice for that purpose. Assume an economy with two goods only, a and b, each being both a consumption and a (circulating) capital good. The economy lasts two ‘years’ in all, t = 0 and t = 1, indicated by their initial moments 0 and 1. Production therefore occurs in a single cycle for t = 0, with all outputs becoming available at the end of that ‘year’ (a second production cycle in t = 1 would make no sense, because it is completed when the economy ceases to exist). As usual, all markets occur at ‘moment’ zero, so that the prices Pa1 and Pb1 of commodities a1 and b1 available for the year t = 1 are discounted to moment zero, when they are quoted together with the prices Pa0 and Pb0 of the spot commodities a0 and b0, and with the wage W.

We may at first suppose that one method only is known for producing each of the two commodities (this assumption will be abandoned in Section 1.5); la, aa, ba and lb, ab, bb are the corresponding production coefficients, which for simplicity we shall assume to be all strictly positive. The methods are of course assumed to be ‘viable’, i.e. capable of producing a surplus over the mere replacement of the means of production.

We shall then have the following equilibrium relations:

|

(1.1e) |

| (1.2e) | |

|

(1.3e) |

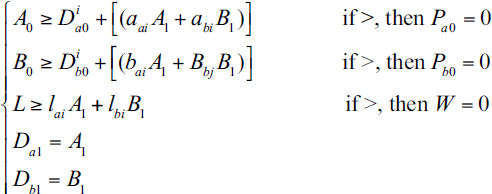

In system (E), equations (1.1e) are the usual competitive price relations for the products a1 and b1,11 while equation (1.2e) chooses b1 as the numéraire. The first two relations (1.3e), on the other hand, regard the supply of commodities a0 and b0, provided by endowments A0 and B0, and the demand for them, given by consumptions Da0 and Db0, plus investment (aaA1 + abB1) and (baA1 + bbB1), respectively; the third relation regards the demand and supply of labour, while the remaining two express the utilisation of the two outputs A1 and B1 for (only) the consumptions Da1, Db1.

System (E) thus has eight relations, only seven of which are independent, with seven unknowns: i.e. the four prices, the wage and the two outputs A1 and B1. Beyond the first test of consistency given by these numbers, the enquiry into the existence and character of the solutions of (E) will be part of the analysis we intend to conduct by means of the above-mentioned general equilibrium savings-supply and investment-demand schedules (see system (F) par. 7).

It may now be important to observe first that we have here simplified the system by ignoring the possibility of storing the two goods between t = 0 and t = 1, thus ‘transforming’ a0 into a1, and b0 into b1 — a simplification which does not affect the limited conclusions aimed at here, but the implications of which will be recalled below when necessary.12 It is this simplification which justifies the assumption that both commodities are produced, and that, therefore, relations (1.1e) hold with 2 a strict equality sign (cf. also Appendix II par. [iv]).

A second observation may be in order about system (E). The choice of b1 as numé raire in equation (1.2e) entails that the variables Pa0 and Pb0 emerge from (E) as the relative prices Pa0 /Pb1 and Pb0 /Pb1 which involve commodities of the two different dates, and which we shall accordingly call ‘intertemporal relative prices’. We shall distinguish them from ‘contemporary relative prices’, e.g. Pa0/Pb0, since we shall find that the properties of the two sets differ in important respects.13

4. We can now come to the decisions to save and to invest implied in system (E) for each of the two years’ life of the economy. Indeed, some readers might have been surprised by our reference in par. 3 to savings distinguished by year in a context of intertemporal equilibrium — where all contracts are made in an initial ‘moment’, and therefore all income is received and disposed off in that single ‘moment’; and furthermore it will be disposed in consumption only (if ‘final’ capital is zero). However, reflection shows that outputs, including of course capital goods, have to flow out year by year, and accordingly the incomes making up the prices of those outputs must also be distinguishable by year, together with their 20111 savings component.

The fact that, given the two years’ life of the economy, production only makes sense in t = 0, entails investment and savings will also only make sense for year t = 0. The aggregate decisions to invest I0 of that period are the value of two physical components Ia0 and Ib0, consisting of the parts of the two initial stocks A0 and B0 which are used as the means for the production of a1 and b1, and have already 6 appeared in the first two relations (1.3e). We thus have

|

(1.4) |

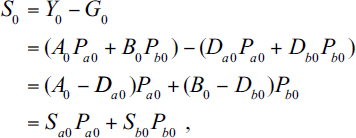

Similarly gross savings S0 will be part of the social gross income Y014 of t = 0 — which, unlike the income Y1 of t = 1, will not be the counterpart of a social gross product, and will consist instead of the initial stocks, A0 and B0. Thus S0 will be expressed as the following difference between the gross income Y0 and the aggregate consumption G0 in year t = 0:

|

(1.5) |

where the physical components of the aggregate saving decisions S0 are distinguished by Sa0 and Sb0 and where the equilibrium magnitudes of system (E) imply Sa0 = Ia0, Sb0 = Ib0 and therefore I0 = S0.15

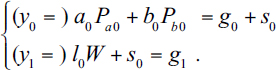

As for the year t = 1, we shall have

where (L0W + S0) is the value of the gross social product from the income side, and where, however, the last two equations (1.3e) stating that the entire output of t = 1 is consumed, entail I1 = 016 and S1 = 0.17

5. It may now be of interest to note how, in the individual ‘wealth equations’, relating to the entire lifetime of the economy, the savings of each year disappear (contributing perhaps to the misleading view that the problems raised by savings and investments disappear leaving place to a question ‘not any different from […] choosing commodities today’).18

The equation in question is in fact simply the sum of the yearly individual budget equations of the kind just seen, and in that sum the savings on the ‘expenditure side’ of the budget equation for any year t, reappear on the ‘income side’ for (t + 1), and must therefore cancel out with the latter (the exception being any savings of the final year of the economy which will of course be zero, if terminal capital is to be zero).

Thus, for example, the yearly budget equations of an individual in our two-year economy can be written as follows, where the small letters y, g, s stand for the individual’s income, consumption and gross savings for the respective year, and l0, a0, b0 stand for initial endowments:

|

(1.5a) |

In summing equations (1.5a), the s0’s cancel out and we are left with

![]()

where the terms after the first equality sign constitute the ‘wealth equation’.

Non-zero gross savings and investments being possible in our model only for t = 0, we shall henceforth simplify our notation by dropping the zero deponent from the savings and investment variables.

1.3 The general-equilibrium schedules of savings-supply and investment-demand

6. Our task is now to bring out how the savings and investment decisions of equations (1.4) and (1.5) vary with prices and can accordingly affect the equilibria of the system. This is what will be done here by means of the two constructs mentioned already: ‘the general-equilibrium investment-demand schedule’ and ‘the general-equilibrium savings-supply schedule’.

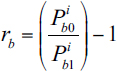

The two schedules will be obtained from the relations of system (E) by (i) treating one of the two own rates of interest of period t = 0, say rb, as the independent variable;19 (ii) waiving the equality between I and S implied in (E).20 This requires first of all, the introduction of the definitory equation

|

(1.6) |

The release of condition I = S, on the other hand, allows for either Sa ≠ Ia, or Sb ≠ Ib, or both, and therefore a difference between what we may now call the total demand of a0 given by A0D = Da0 + Ia (cf. the R.H.S. of the first of the relations (1.3e) in par. 3) and its total supply A0S = A0, which can also be expressed as A0S = Da0 + Sa (cf. equation (1.5), par. 4) — and similarly for the total demand and supply of b0.

7. The result is seen in system (F) below where,

1 the two unknowns A0D, B0D replace the data A0 and B0 in the relations (1.3e) which now, in their form (1.3f), with an equality sign only define the two total demands;

2 the data A0, B0, re-labelled as A0S, B0S, appear instead in the relation (1.5f) defining savings;

and where the unknowns I and S constitute the points of the two schedules corresponding to the given level of the independent variable rb:

|

(1.1f) |

| (1.2f) | |

|

(1.3f) |

| (1.4f) | |

| (1.5f) | |

|

(1.6f) |

|

(1.7f) |

All markets are here assumed to be in equilibrium except those of savings and investments, i.e. as we saw, the markets where saved and investible quantities of a0 and b0 are traded.21 System (F) in fact implies equilibrium

1 in the market for labour (see the respective relation in (1.3f));

2 in the markets for commodities a1 and b1 (see the last two equations in (1.3f));

3 in the markets of a0 and b0 for consumption (see the inclusion of Da0 and Db0 in equation (1.5f)).

However, if we exclude equation (1.7f) to be presently discussed, system (F) has eleven relations, ten of which are independent, containing eleven unknowns (the five prices; the two outputs A1, B1, the two aggregate quantities demanded B0D, A0D, and, finally, I and S).22 Were it not for equation (1.7f), system (F) would therefore possess the one degree of freedom which we could expect since, essentially, we replaced with the two new unknowns A0D and B0D, the single unknown Pb0 of (E) which becomes a given in (F) in the shape of the given rb = Pb0 − 1 of equation (1.6f).

Before discussing that degree of freedom, and its closure by means of (1.7f), we may, however, re-write the equations (1.3f), (1.4f) and (1.5f) in the more transparent form which we shall frequently use in what follows.

|

(1.3f′) |

| (1.4f′) | |

| (1.5f′) |

8. In fact, the economic meaning of the degree of freedom we would have in (F) but for equation (1.7f) is quite simple. We have aggregated all decisions to invest into the single magnitude I, but nothing has been specified about the physical composition of the investment flows of Schedule I: this is what is done by means of equation (1.7f) which in fact fixes Ia/Ib jointly with Da0/Db0 since A0D/B0D is a weighted average of those two ratios.

That physical composition cannot, however, be specified arbitrarily. Our use of the I and S schedules in order to analyse the properties of system (E) imposes two requirements. The first and stricter requirement is that when S = I, the aggregate demands of a0 and b0 should also be equal to the respective supplies. And the same correspondence should hold for possible ‘extreme’ equilibria at the level rb min with S > I, or with W = 0 for S < I (see par. 14 below, points I and IV respectively, and Appendix I). This will in fact be the case when the proportion A0D/B0D in which the two commodities are there ‘demanded’ are the same as the proportion A0S/B0S in which they are supplied, as is imposed by equation (1.7f) (cf. parr. 15–16). The second, less strict, requirement is that the proportion A0D/B0D should reflect a non-unplausible out-of-equilibrium behaviour of the economy. And equation (1.7f) seems to provide a description of an out-of-equilibrium behaviour as plausible, it seems, as any equally general condition (cf. parr. 17–18).

9. There remains a rather technical point we need to consider in order to complete our account of system (F). It concerns the consistency of the system with the sum of the individual budget equations underlying it (Walras’s identity) and the often supposed impossibility of a disequilibrium confined to a single market, such as we have assumed in (F).23 However, that impossibility would follow only if the individuals could spend for the commodities available in t = 1 according to the total income which they would derive from selling exactly the quantities of a0 and b0 they wish to sell at the going prices (i.e. A0S/B0S in the aggregate, if we include in the demand the consumption by owners) and realise the corresponding savings for t = 0, but that is just what cannot happen when S ≠ I. When, on the other hand, the purchasing power for t = 1 originating from the savings S0 is appropriately ‘adjusted’ to what the going level I would allow them to sell of a0 and b0 — and this is what we have assumed in (F) — the contradiction disappears and system (F) is consistent.24

The ‘adjustment’ in expenditure we assume here, when compared with the more usual procedure of admitting disequilibrium in at least one further market, has the advantage of being compatible with a constancy in the employment of labour as rb, varies, thus providing a more transparent basis for deducing the shapes of the S and I schedules. It also allows for a simpler and perhaps better than any equally general representation of the out-of-equilibrium behaviour of the system, in the sense just mentioned that households failing to sell part of their A0S and B0S resources because of excess savings can hardly exert excess demand on the commodities of t = 1.25

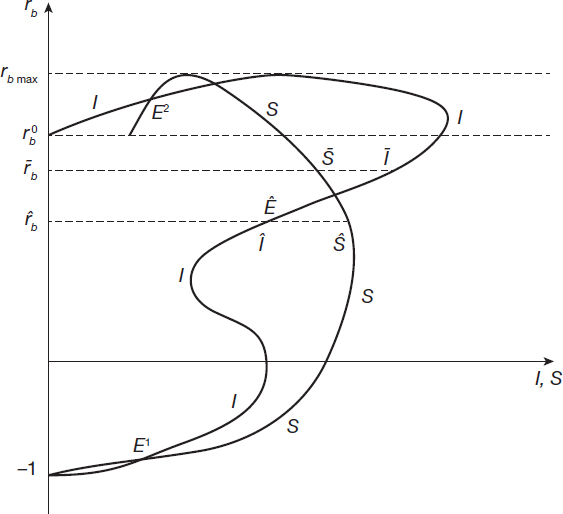

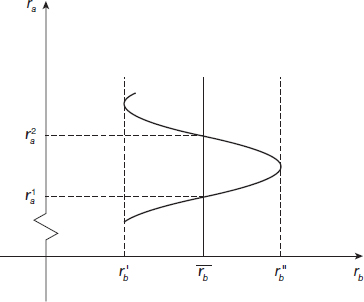

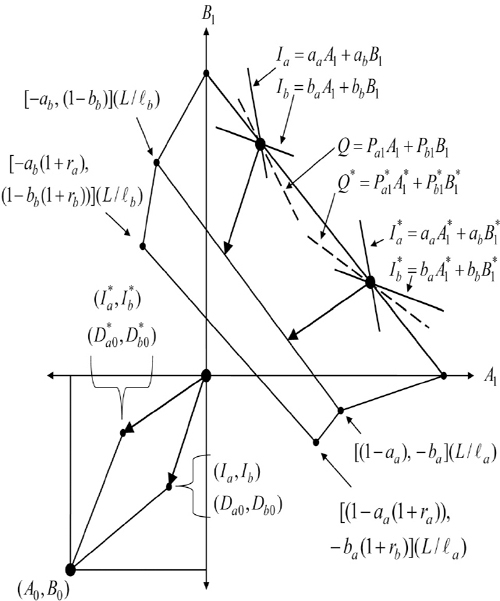

10. Some preliminary observations concerning our method of analysis may in fact be useful at this point. The general equilibrium nature of the two schedules and condition (1.7f) entail that any equilibrium in the market they represent is also an equilibrium of the system and that the converse is true (parr. 15–16). The properties of the general equilibrium relevant for its uniqueness and stability, and their dependence in particular on the circumstances of the savings and investment market then become visible in a form not unlike that of a partial equilibrium problem. It is in this way that in Sections 1.4–1.6 the two schedules will render visible a cause of multiple and unstable equilibria which does not appear to have yet been sufficiently analysed in the literature. That cause is the way in which investment changes as intertemporal prices change (see Figure 1.1).

Possibilities of non-uniqueness and instability of the equilibria have in fact been in the foreground of current general equilibrium literature. However, those possibilities seem to have been investigated in what we may describe as a mainly negative and economically unspecific way. The attention has been focused, that is, either on the impossibility of establishing uniqueness and stability under the more general premises of the theory, or on some sufficient, rather than necessary conditions for such properties.26 Similarly, the efforts seem to have been concentrated on systems of pure exchange, or of production without capital — this, despite the fact that the implications of reverse capital deepening and reswitching which had been pointed out for the traditional versions of neoclassical general equilibrium should have alerted scholars to the possible implications of those phenomena for intertemporal theory (cf. par. 2).

Thus, with regard to the causes of multiplicity and instability of the equilibria, recent literature does not seem to have added substantially to what, owing to a more simplified, but also better focussed analysis, had been known, since Walras, Marshall or Wicksell,27 about income effects and their causes. The paradox seems then to be that general conclusions about those properties that are at times presented as drastically negative for neoclassical theory28 have in effect favoured the comparatively comfortable, but unwarranted belief that the difficulties in question all have their origin in income effects — with which the theory has, after all, long managed to co-exist — and thus have had little dissuasive effect on the actual practice of the profession.29

11. Our general equilibrium demand and supply schedules may be seen as part of an attempt to remedy this situation by tackling again such central properties of the equilibria in the way Marshall, Walras or Wicksell approached them, that is by starting from specified economic conditions susceptible of causing the difficulties in order to arrive at their consequences for the equilibrium. This has led to an analysis of production with capital, and to focussing on the savings-investment market — on which reverse capital deepening impinges directly — in order to ascertain how those phenomena can affect the properties of a general intertemporal equilibrium (Figure 1.1).

A word of caution must now be added concerning our application of the method of general-equilibrium demand and supply schedules. Just because of its greater specificity, these tools of analysis bring to light questions which, apparently buried in the mathematical formalism previously used, require now30 definite answers. Where possible, those answers have been attempted here, however

provisionally. At other times the questions have been treated by referring to specific, more manageable sub-cases which do not however alter the generality of the negative results the paper is concerned with, since the sub-case is part of the general case.31 It may incidentally be stressed that when sub-cases have been resorted to, they have been specified so as to grant more favourable conditions to the theory. In particular, care has been taken to avoid mixing the cases of non-uniqueness, instability or zero factor prices emerging here, with the altogether different cases which might be due to income effects.

12. Passing now from the method to the content of our argument, the reader may ask why we have introduced the aggregate savings and aggregate investment of system (F) in order to discuss a system (E) which was in fact formulated independently of any such aggregates. The answer will of course have to come from what follows in this chapter. However, we have indicated already how the total demands of a0 and b0 which we find on the right-hand side of the first two relations in systems (1.3e), or (1.3f), are in fact made up of two quite heterogeneous elements each: the consumption demands Da0, Db0 (which we assumed to be always satisfied along the I and S schedules) and the investment demands I and Ib. Now, the investment demands are ruled by principles that are totally different from those which govern consumption demands: hunger can be satisfied by corn, and not by coal; but desire for future income, the motive of the demand for capital goods from savers, can surely be satisfied by tractors, as well as by looms or any of the thousands of other capital goods, whichever of them offers a higher rate of return. It can here be indifferently satisfied by a0 or b0 lent for production. In fact, as we shall see in par. 26, different capital goods are perfect substitutes for the savers.32

Now, in view of the different principles thus regulating investment demands as distinct from consumption demands, and in view above all of the perfect substitutability of heterogeneous capital goods for the saver, but of course not of consumption goods for the consumer — it does prima facie stand to reason that the separation of the two kinds of demand and, then, the aggregation of the capital goods demanded for investment, might lend transparency to the workings of the system.

13. In par. 8 we mentioned ‘stability’ among the properties of the equilibrium which might be inquired into by means of our two schedules. That implies that the schedules should be applied to discuss adjustments to the equilibrium. Although only hints of that analysis will be contained in the present chapter (parr. 17–18), we should perhaps clarify what can be meant by ‘adjustments’ and ‘stability’ here, in a context of dated equilibria.

In fact, as I have argued elsewhere (1976: 38), an analysis of stability, capable of fulfilling its traditional role of ensuring ‘correspondence’ between theoretical and observable magnitudes, has to be founded on the possibility of a sufficient repetition of transactions on the basis of approximately unchanged data. If a tendency to equilibrium could be established on that basis, it could also be generally supposed that disequilibrium deviations would tend to compensate each other, letting the equilibrium levels emerge as some average of observable levels, and be capable, therefore, of providing some guidance to reality. Essentially, the question in this respect would be to allow for a time setting in which

fitful and irregular causes in large measure efface one another’s influence so that…persistent causes dominate value completely.

(Marshall, 1949: p. 291)

That meaning of the positions of the economy to which theory refers its variables, and the corresponding notion of its stability, appear in fact to have been the unanimously accepted basis of economic analysis from Adam Smith, and before, until comparatively recent decades. At those earlier times, however, such a necessary repetition of markets on approximately unchanged data could be grounded in the conception of a normal position of the economy, a sufficient persistency of which was ensured by the uniform rate of return on the supply prices of the capital goods and by the corresponding adjusted composition of the capital endowment — which in neoclassical theory depends on the conception of the capital endowment as a single magnitude.33 If the abandonment of the corresponding notion of equilibrium (fundamentally different, recall, from that of ‘stationary’ or ‘steady states’) was by itself sufficient to undercut in fact the previous meaning of an analysis of stability, by imposing data too impermanent to allow for a sufficient repetition of markets, the ‘dating’ of the equilibria has jettisoned it even in principle by excluding repetition as such.34 This appears to leave in some obscurity the precise significance of present-day analyses of stability, quite independently of their negative results.

Our present critical purpose seems, however, to exempt us from entering further into the question and allows us to adopt the formal way out generally taken when the concern are still variables determinable by the equations of general equilibrium, and not the essentially indeterminable variables of a path-dependent equilibrium. This formal way out is, of course, that of ‘recontracting’, or of ‘tâtonnenment’, as it has come to be named with a misleading reference to Walras.35 In the modem fictitious theoretical world into which we shall enter by means of that assumption, the repetition of transactions — thus in fact admitted to be essential for an analysis of stability — is supposed to take place in some initial ‘moment’, or period before the actual time, measured out by ‘dated’ equilibria, has rendered such repetition impossible.

14. Though the model is simple, the discussion of system [F] and the determination of the schedules become complex as soon as we wish to go beyond the mere formal demonstration of the existence of solutions of system (F) — for which see the Mathematical Note at the end of the volume (p. 469) — and we attempt to gain an understanding of their properties and economic meaning. We have accordingly placed that discussion in an Appendix and shall here confine ourselves to listing the conclusions we shall use in the rest of the chapter, references being given to the Appendix for the supporting argument.

I. When we suppose, as is done above, that neither commodity can be stored, the economically meaningful interval of rb extends from rbmin = −1, for Pb0/Pb1 = 0 (Appendix I par. [1]) to a level rbmax, the highest among those for which W = 0 (see point IV below).

II. Changes in the intertemporal relative price rb = [(Pb0/Pb1) − 1] need not affect in one direction rather than the other total relative demands of the two contemporary commodities a0 and b0, i.e. the ratio (Da0 + Ia)/(Db0 + Ib), and therefore the relative contemporary price Pa0/Pb0 necessary to satisfy equation (1.7f). Making then the further reasonable supposition that such a contemporary relative price will not be much affected by changes in rb, we assume that the intertemporal price Pa0/Pb1 moves in the same direction as Pb0/Pb1 and hence rb in the interval rbmin < rb < rb+ in which W > 0. This suffices to ensure a unique solution in an interval rbmin < rb< rb0 where rb0 ≤ rb+ is, as we shall see under point IV below, the minimum level for which we find W = 0 (Appendix I, parr. [5]–[7]).

III. Two other important consequences follow from that assumption. The first is that the monotonic relation between Pa0/Pb1 and Pb0/Pb1 entails a decreasing relation between W and the intertemporal price Pb0/Pb1 and hence rb over the whole interval rbmin < rb < rb+, along what we shall call ‘the main branch’ of the relation between rb and the unknowns in (F), in particular between rb and I and S. That ‘branch’ is of course where, as we saw under point II, we have unique solutions, but only up to rb0 and not for rb0 ≤ rb ≤ rb+ where a continuum of positions for W = 0 will exist (see point IV below). The second important consequence of the monotonic direct relation between the intertemporal prices Pa0/Pb1 and Pb0/Pb1 is that ra will move in the same direction as rb allowing us to refer unambiguously to a rise or fall of the own interest rates (Appendix I parr. [8]–[9]).

IV. Should labour continue to be supplied at W = 0 — as would generally be necessary for ensuring the continuity of the functions and the existence of solutions of system (E) (ibid. par. [10]) — then at that zero level of W we shall find a con tinuum of solutions of (F) for levels LD of labour demanded in the interval 0 ≤ LD ≤ LS, and for the corresponding levels of rb in the interval rb0 ≤ rb+ ≤ rbmax where, with rb0 as the minimum such level, rbmax ≥ rb0 is the maximum one (ibid. par. [6]: see also Figure (1.2)).

V. The minimum level rbmin = −1 corresponding to the intertemporal price Pb0/Pb1 = 0 does not entail, as one would perhaps expect, that b0 is a free com modity so that, for example, also Pb0/Pa0 = 0 . On the contrary, there are reasons which force us to admit that, as Pb0/Pb1 → 0, the contemporary relative price Pb0/Pa0 will generally tend to a positive and finite level, with all commodities available in t = 0 having zero price in terms of all commodities available in t = 1 (ibid., parr. [7] and [12]).

VI. As for the shape of the two schedules (see Figure 1.1) what we can say generally is that: (i) the choice of b1 as our numéraire entails, as just said, that for rb = rbmin = −1 both Pa0 and Pb0 are zero, so that both the S and I schedules intersect the vertical axes at rb = −1; (ii) as we saw under point III a ‘main branch’ of the S and I schedules will exist in the interval rbmin ≤ rb ≤ rb+: along it W will decrease from Wmax for r = rbmin down to zero for rb+; (iii) the two schedules will then continue beyond rb+ in order to represent the continuum of positions indicated under point IV above, with the I schedule finally reaching the vertical axis with LD = 0 (ibid. par. [14]); (iv) it does not seem however that anything general can be said about the overall shape of the schedules in the intermediate interval 0 ≤ rb ≤ rb0 except for the single-valued character of the schedules seen under point II and the bias towards rising S and I schedules due to our choice of b1 as numéraire, and therefore of Pa0 and Pb0 rising as rb rises (a bias which is of course innocuous as far as the properties of the equilibria are concerned, which only depend on the ratio S/I at each level of rb); (v) in particular, the impossibility of supposing a necessarily falling I schedule is not however due to that bias. Nor is it due to the fact that alternative techniques have not yet been considered: possibilities of substitution between labour and means of production are already present in the system because of consumer choice between a1 and b1. The essential reason why a falling I schedule cannot be assumed will be seen below (par. 19) and is the same as for the phenomenon of reverse capital deepening, familiar from the traditional analysis. No confusion should in fact be caused by the presence of two consumption goods which could conceivably engender a rising I schedule because of income effects: as we make clear by one of the assumptions on which our argument is based (Assumption (IIIa), ibid. par. [5]), our conclusions are independent of any income effects.

1.4 The representation of the intertemporal system

15. What we must now see, therefore, is how the two schedules can aid our understanding of the behaviour of system (E). In this and the next paragraph we shall see how the schedules can represent the equilibria of the system and then, in the following two, we shall consider the information they can provide on out-of-equilibrium behaviour.

A ‘position’ (F) of the system (i.e. the solution of (F) for a particular value of rb) will also be an equilibrium (i.e. a solution of E) when the first two relations in (1.3e) of par. 3, concerning the aggregate demand and supplies of a0 and b0 happen to be satisfied: all other relations of (E) are in fact already present in (F). Leaving aside at first the case of ‘extreme’ equilibria occurring, that is, for rbmin or for W = 0, it can be asserted that when the system is in equilibrium the two schedules S and I intersect, and that the converse is also true.

As for the first proposition, when rb is in that intermediate interval, or also in the upper interval rb+≥ rb≥ rb0 along the ‘main branch’ of the S and I functions (point III in par. 14), and Pa0, Pb0 are accordingly strictly positive, any solution of (E) entails that the first two relations in (1.3e) of par. 3 above are satisfied with an equality sign,36 i.e.

| (1.3a) |

and hence (see relations (1.3f′) in par. 7)

| (1.3a) |

and

| (1.3b) |

The general equilibrium of the system thus entails an intersection of the two schedules.

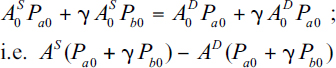

As for the converse proposition, when we have an intersection of the schedules in that same interval (see Figure 1.1, par. 11), equation (1.3b) is satisfied and therefore, after adding Da0Pa0 + Db0Pb0 to both sides, we obtain

| (1.3c) |

Indicating then, by the constant γ, the common value or the ratios appearing on the two sides of equation (1.7f), we may write equation (1.3c) above as follows:

|

(1.3d) |

from which A0S = A0 D and hence, from equation (1.3c), B0S = B0D, thus fulfilling all relations (1.3e) in system (E), and ensuring that we are in a general equilibrium position.

16. Turning now to the representation of possible ‘extreme’ equilibria of the system, we may note that equilibria in the upper interval rb0 ≤ rb ≤ rbmax (see Figure 1.2) will also be shown by intersections of the two schedules, but the converse proposition will not be true. Since different (F) positions may correspond to the same level of rb, an intersection between I and S may occur in that interval at a point representing an (F) position on the I schedule, and a different one on the S schedule. The intersections representing equilibria have then to be traced by checking whether the I and S points of the intersection pertain to the same (F) position. This will be possible in the diagram because, starting, for example, from points like I+ and S+ (see Figure 1.2), the two schedules will go through exactly the same values of rb in exactly the same sequence: ‘couples’ of I and S points corresponding to the same (F) position can therefore easily be singled out.37 The reasoning conducted in the preceding paragraph will then apply to those points of intersections which represent the same (F) position on both schedules.

As we proceed to rbmin, at the opposite extreme, although the zero intertemporal prices Pa0, Pb0 yield S = I = 0, we shall generally have definite non-zero physical

Figure 1.2 The upper reaches I+I0 and S+S0 of the I and S schedules representing positions (F) for W = 0 characterised by different levels of labour employment and therefore of the investment required to equip them

quantities Ia, Ib, Sa, Sb (par. [13] in Appendix I). We need first of all to note here that the assumption about both goods being scarce for consumption in t = 0 as well as in t = 1 (see Assumption (ii) in par. [3] of Appendix I) entails that the position (F) for rb = −1 is the one characterised by the ‘collective’ zero intertemporal price of all commodities available in t = 0 relative to those of t = 1, which we mentioned under point VI of par. 14 and discussed in parr. [7] and [12] of Appendix I.

Now, that (F) position is an equilibrium when, as rb → rbmin, Sb > Ib. At that position savings would generally exceed investment when expressed in contemporary prices by means of either a0 or b0. Then, by a reasoning analogous to the one conducted in par. 15 for equations (1.3c) and (1.3d) we could in fact conclude S > I; Sb > Ib and therefore we have an ‘extreme equilibrium’ with A0S > A0D; B0S > B0D. When however S < I as rb → rbmin no equilibrium will generally exist at rbmin.38

17. While thus representing the equilibria of the system, the two schedules can, as we said, provide elements for a discussion of its out-of-equilibrium behaviour. Suppose first an (F) position for rb = rb′ in the interval rbmin < rb′ < rb0 such that S′ > I′ (see Figure 1.1, par. 11). As we just saw, the inequality S > I entails A0S > A0D and B0S > B0D. It would then seem natural to suppose an ‘initial’ reaction in the markets for a0 and b0, more directly affected by the disequilibrium, which would occur before adjustments can take place in connected markets: in our case under the reasonable assumption of excess supply for both commodities, that ‘initial’ competitive reaction could only be a fall of intertemporal prices Pa0/Pb1 and Pb0/Pb1. However, the connected markets will then tend to adjust, so that we may envisage an out-of-equilibrium behaviour in the recontracting dominated by movements centring on the two general equilibrium schedules. In this respect equation (1.7f), assuming a proportionate change of the algebraic excess demands of a0 and b0, seems to be as reasonable an assumption as can be made at a general level: it may indeed be taken to represent a condition of ‘even flexibility’ of the price system, in the sense of allowing for the excess demands of a0 and b0 to change in the same proportion. Our critical aim strengthens on the other hand the legitimacy of assuming that the dominant out-of-equilibrium movement will be along the schedules: if deficiencies of the demand and supply apparatus result under that assumption, they would seem to be all the more plausible when obstacles to the adjustments to equilibrium are also considered in the connected markets, which the schedules assume instead to be broadly kept in equilibrium.

Then, as we start moving along the schedules, the ‘initial’ fall of both Pa0/Pb1 and Pa0/Pb0 in response to the assumed excess savings will result in a movement downward along the schedules with a fall of both own rates ra and rb (see point III in par. 14). This result can indeed be taken to be general — largely independent, that is, of our assumption about the monotonic rise of Pa0/Pb1 with Pb0/Pb1 (cf. point II in par. 14, and par. [8] in Appendix I).39

Similarly to what could be argued in any partial equilibrium use of the schedules — we have then elements for arguing a tendency e.g. toward equilibrium EIII in Figure 1.1 of par. 11, where the I schedule cuts the S schedule from above and where therefore any given initial position in the interval rbIII < rb< rbIV, rb can be expected to fall, and to rise for any rb in rbII < rb < rbIII. A tendency away from equilibrium can instead be argued when, as we move from left to right, I cuts S from below (see EII and EIV in Figure 1.1).40

18. As we turn to ‘extreme’ values of rb, we may note that if we happened to have S > I in the proximity of rbmin = −1, the fall of rb, which we can assume in the presence of S > I, would imply competitive recontracting to tend to the equilibrium with the zero intertemporal (but not contemporary) prices of both a0 and b0 we saw in par. 16.41

As we could expect, some novel problems are met when we shift our attention to the upper extreme for rb0 ≤ rb ≤ rbmax. We may leave aside the ‘main branch’ of the S and I schedules (where with L = LD and W > 0 we have all the conditions for the out-of-equilibrium behaviour considered in par. 17). In all other (F) positions of that interval, we shall have excess supply of labour with L > LD and a zero wage. The I schedule will tend to finally extend leftward so as to reach the vertical axis for the (F) position corresponding to LD = 0 (cf. par. [14] in Appendix I) and, as we just saw in par.16, any equilibrium will be shown by the two schedules intersecting, and intersecting for the same (F) position.

Outside any such equilibria, if in the given position (F) we have I< S (see e.g. points I″ and S″ in Figure 1.2) it would be natural to suppose that the excess savings, i.e. the excess supply of a0 and b0, will cause the ‘initial’ fall of both Pa0/Pb1 and Pb0/Pb1 we admitted for intermediate levels of rb.

However with W = 0 and the available excess supply of labour making it possible to expand outputs, that temporary ‘initial’ fall of the prices of a0 and b0, relative to those of their outputs a1 and b1 would make it profitable for entrepreneurs to raise outputs, and as adjustments occur we would tend to move along the I schedule towards the right in the direction of an increase of the labour employment LD and therefore of the investment required to equip that labour. Prices Pa0 and Pb0 will have to move in the opposite direction and so may therefore do ra and rb. Unless an equilibrium were to be met in the process, that increase of LD would continue until full labour employment is reached in position (F+) for rb = rb+. Excess savings and the consequent persisting ‘initial’ fall of Pa0/Pb1 and Pb0/Pb1 would then result in a positive wage W, and a fall of rb: the (F) positions would become those already discussed in par. 17, characterised by W > 0.

In the case in which, in that same upper interval of rb and for W = 0, we instead had I > S in the (F) position — as exemplified by points I′ and S′ in Figure 1.2, for the same level rb″ of rb of the just discussed position (F) with excess savings — then, an opposite process of decreases of employment LD and investment would have to be expected. It would lead leftwards along the I schedule to an equilibrium which would then have to exist. As we just recalled, investment I has in fact to change continuously down to zero, while S also changes continuously, though generally without reaching zero. Then, with I starting to the right of S and having to pass finally to its left while going through exactly the same levels of rb, it is inevitable that the two schedules will cross — as exemplified by E2 to the left of the points I′ and S′ in Figure 1.2.

1.5 Alternative techniques and the investment demand

19. System (F), like system (E) which generates it, still rests on the assumption that only one method of production is available for each commodity. It is time to drop that assumption and consider the existence of several alternative methods for each commodity, all sharing the properties we mentioned in par. 3. We may call a set of ‘methods of production’, one for the commodity in question and one for each of its (direct and indirect) means of production, ‘the system of production’ or ‘technique of production’ of the commodity. Here, the ‘technique’ or ‘system’ of production of the commodity will accordingly include two ‘methods of production’, one for the commodity and one for the other commodity as means of production of the former. Thus one ‘technique’ for producing a, will also be a ‘technique’ for producing b, and we may therefore refer to techniques i = 1,…, n without mentioning the commodity they refer to.

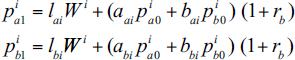

Despite our assumption that all alternative methods of production require the same three factors, there is no assurance that marginal products, even of the discontinuous kind, will exist.42 For the determination of the method that would be the cheapest at current prices and would therefore be chosen by competitive entrepreneurs, we must therefore resort to the more general approach we find in Sraffa’s Production of Commodities: namely, comparing the expenses for producing the commodity by the alternative methods. However, at each level of rb the comparison can only be done in terms of prices Pa0i, Pb0i and the wage Wi holding for the particular technique i ‘in use’ — meaning here by ‘in use’ that the technique is the one whose adoption we assume to be generally planned at the stage reached by the recontracting.43 Maximisation of entrepreneurial profits will then entail that the recontracting proceeds to any method for each commodity which happens to be cheaper at those prices.

A question which is well known from the ‘traditional’, non-intertemporal assumptions then arises, about whether the order of the alternative methods of production of the commodity as to cheapness, might not itself change with the technique ‘in use’: with the possibility of either endless switching between techniques, or of the technique finally adopted depending on the one initially ‘in use’. Our critical intent, however, will again allow us to grant the assumptions most favourable to the theory criticised and therefore to assume what has been demonstrated to be true under the traditional assumptions: that the order of cheapness of an alternative method is the same, whichever the technique in (planned) use at the given level of rb.44 We can thus suppose that entrepreneurs’ choice will always arrive at one and the same method(s) for each of the two commodities, so that at any given rb the cheapest technique(s) or ‘system(s) of production’ can be uniquely determined, together with the corresponding series of the prices, the outputs, and the I and S quantities, where the plurals above take care of the possible co-existence at some rb of two (or more) methods for the same commodity and hence of the technique(s) differing from i by the method of that single commodity which will then entail the same wage and prices for the given level of rb.

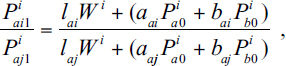

20. We can therefore proceed to reporting below the family (Fi) of systems of equations defining the two schedules under the assumption of a multiplicity of techniques of production j = 1, 2, 3… . Each member of that family is a system of equations like (F) defined in par. 6, but applied now to the technique i which happens to be the one no dearer than any other at the given level of rb. Thus, to any level rb in its relevant interval there will correspond a system (Fi) containing, as well as the relations (F) pertaining to the technique i adopted, as many quadruplets of relations, (8fi) and (9fi), as there are alternative ‘techniques’ or ‘systems of production’ j ≠ i. The first two equations (i.e. 8fi) reckon the production expenses of a1 and b1 with the respective methods j. The second couple of relations, namely (9fi), states that no method j for producing each of the two commodities is cheaper than the method pertaining to the technique i ‘in use’.45

|

(1.1fi) |

| (1.2fi) | |

|

(1.3fi) |

| (1.4fi) | |

| (1.5fi) | |

|

(1.6fi) |

|

(1.7fi) |

|

(1.8fi) |

| (1.9fi) |

where i at the exponent indicates that the variable in question is calculated under the assumption that technique i is being planned for use at the given rb, whereas j at the deponent indicates the alternative technique to which there pertains the variable in question, coefficient of production or price based on such coefficients (no deponent has been given to the same variables pertaining to technique i). The equality signs in (1.9fi) take care of the possible co-existence between technique i and other techniques for same levels of rb, when the equality sign will apply to both the relations (1.9fi).

Correspondingly, also system (E), determining the equilibrium of the system, should now be written in the form of the following family of systems (Ei) allowing for alternative techniques:

|

(1.1ei) |

| (1.2ei) | |

|

(1.3ei) |

|

(1.8ei) |

| (1.9ei) |

where, as for (E) in par. 3, the relations corresponding to equations (1.4fi), (1.5fi), (1.6fi) and (1.7fi) do not need to appear, S = I being implied in (Ei).

21. The main question which the existence of alternative methods of production raises for us here is the changes in the investment requirements I due to changes in the cheapest technique as rb varies. We might perhaps expect that owing to those changes (as well as to those of the relative outputs A1/B1 already determined in system F) the schedule I would generally show a negative slope. However, such an expectation has no better foundation for the present investment-demand schedule than it had for the capital-demand schedule in the ‘traditional’ setting.

A simple line of reasoning seems sufficient to show this. As has been pointed out,46 the roots of reverse capital deepening, as well as those of the re-switching of techniques, lie in the effect of changes in distribution (rate of profits) upon the relative value of the alternative sets of capital goods required by the processes of production which are being compared — whether such processes are alternative methods of production for the same consumption good, or the methods for two different consumption goods. In the traditional, non-intertemporal setting, it is the changing relative value of such two sets of capital goods that can make a more ‘capital-intensive’ technique become more profitable, or a more capital-intensive consumption good fall in price, as the interest rate rises. And it is that same change in the relative value of the alternative sets of capital goods that can bring about ‘re-switching’ among alternative techniques. Now, the same variability of the relative value of alternative sets of capital goods is clearly present in an intertemporal setting.

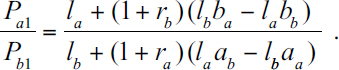

To see the thing in more definite terms, let us consider first the case of alternative techniques as distinct from that of competing consumption goods. From equations (8fi) and (9fi) we may see how, at the given level of rb, the choice between the cheapest technique i and any other alternative technique j differing, say, by the method of production of a alone, hinges on the following relative costs of the two methods:

|

(1.10) |

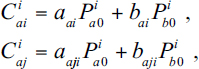

the method of technique i for a1 being more profitable than the j one at the given rb when Pai1i/Paj1j < 1. Defining now

where the Cai’s are the respective capital expenses estimated at the given level of rband for i prices. We may then write the relative production expenses (1.10) of the two methods as follows:

|

(1.10a) |

With (Caii /Iai) and (Caji /Iaj) as the respective ratios of capital to labour in the (direct) production of a1, we then have

|

(1.10b) |

Assume now, without loss of generality, that Caii/Iai > Caji /Iaj . Should the Cai’s be measured so that they are independent of changes in W, clearly Pai1/Paj1 could only fall as W rises (and rb falls: point III, par. 14). Any changes of method could only be in favour of the more “capital intensive” one (from j to i in our case). Since however the Cai’s and therefore the key ratio Caii/Caij are not so independent, the rise of W (fall of rb) need not entail the fall of Pai1i/Pai1j we might have expected: a sufficient rise of Caii/Caji may well make Pai1i/Paj1i rise, and not fall as Wi rises. This means that the rise of W may well result in the less capital-intensive method j becoming the more profitable one of the two, and therefore being adopted.

The same change of Caii/Caji in the relative value of the sets of capital goods of the two alternative processes of production may entail, as can be shown by replacing Paj1i with Pbi1i, that the less ‘capital-intensive’ consumption good b1 may become cheaper relative to a1 as W rises (rb falls) so that regular substitution in consumption has “perverse” effects on factor demands. Hence the freedom with which we were able to draw the shape of the I schedule in our Figures 1.1, 1.2 or 1.3.47

1.6 Some conclusions

22. We can now use the schedules to see some properties of a general inter temporal equilibrium and thereby how ‘capital’ as a single ‘quantity’ enters intertemporal equilibrium. The question may usefully be approached by showing how misleading is the widespread idea is that savings and investment in an inter temporal equilibrium raise no more problems than do relative demands for contem porary commodities and can therefore be subsumed under a single theory of consumer choice.48

It is of course true that if we assume no capital to be left at the final date, the (gross) savings at t must consist of demand for consumer goods at future dates (t + τ), at the expense of demand for the same or other consumer goods at t. It is then equally true that any excess of saving decisions over investment decisions at t must necessarily take the form of an excess supply of consumer goods at t, and an excess demand for them at future dates. Thus, imagine that initial recontracting had brought the economy to the position (![]() ) of quantities and prices which the system (Fi) associates with the interest rate

) of quantities and prices which the system (Fi) associates with the interest rate ![]() b (see Figure 1.3), and suppose that (

b (see Figure 1.3), and suppose that (![]() ) would coincide with an equilibrium (Ê) except for a positive excess of savings Δ

) would coincide with an equilibrium (Ê) except for a positive excess of savings Δ![]() = (

= (![]() − Î), (

− Î), (![]() ) and (Î) being estimated at the prices of (

) and (Î) being estimated at the prices of (![]() ).

).

From the households budget equations in (Fi) for ![]() b we obtain

b we obtain

|

(1.5b) |

where the ΔD’s indicate the differences in the respective quantities demanded between positions ![]() and Ê (where savings would have been equal to Î); which, for simplicity, we have supposed to be both negative in t = 0 and positive in t= 1.49 Undoubtedly, equation (1.5b) looks similar to that holding in the case of

and Ê (where savings would have been equal to Î); which, for simplicity, we have supposed to be both negative in t = 0 and positive in t= 1.49 Undoubtedly, equation (1.5b) looks similar to that holding in the case of

contemporary commodities, should (![]() ) have failed to be an equilibrium simply because of an excess demand of b0 relative to a0, giving

) have failed to be an equilibrium simply because of an excess demand of b0 relative to a0, giving

| (1.5c) |

23. However, the analogy between equations (1.5b) and (1.5c) remains at the surface of the two phenomena and hides a basic difference between them which emerges as soon as we consider the adjustments which should lead to a new equilibrium and therefore the forces warranting it in the two cases. That basic difference can be best brought out if, for a moment, we extend our two-year model to the three years (−1), (0), (1), with the commodities a0 and b0 accordingly coming from production in t = −1 by means of L−1 labour and A−1s, B−1s initial stocks.

Now for the contemporary commodities of equation (1.5c), the question of achieving a neighbouring equilibrium will be the comparatively simple one of shift ing the labour and means of production of (t − 1) freed by (−ΔDa0) to producing ΔDb0 and no obvious obstacle stands in the way of achieving that as a consequence of the competitive rise of Pb0/Pa0, which would plausibly follow from initial competitive bidding in the situation.

The position is entirely different in the intertemporal (savings/investment) case of equation (1.5b). Obviously, it will not be possible to shift the labour and the means of production of period t = −1, set free by the reduced consumption of t = 0, to directly producing the increments ΔDa1, ΔDb1 of equation (1.5b): the labour and means of production of t = −1 are not those of t = 0, which can directly produce ΔDa1 and ΔDb1. Even less will it be possible to devote to the direct production of ΔDa1 and ΔDb1 any of the labour and means of production of t = 0, which could directly produce them, but unlike those of t = −1 are assumed to be already fully employed. No competitive rise of Pb1/Pb0 plausibly following from the relative rise of consumption demands in t = 1 can achieve either of those two feats.

How, then, can we raise the t= 1 outputs and consumptions and, moreover, do so at the expense of the consumptions of t = 0, as required by the excess savings of equation (1.5b)? The answer clearly remains that of traditional, non-inter temporal theory. This change of relative outputs over time can only be achieved by raising the gross productivity of the already fully employed labour L0, by means of an increase, in some sense, of the quantity of means of production cooperating with it. It is a question, that is, of producing in t = −1 quantities ΔIa and ΔIb while decreasing production by quantities ΔDa0 and ΔDb0, and then using the increments of investment with the constant quantity of labour L0 to produce increments ΔDa1 and ΔDb1 of consumption. But, and here comes the essential point, those increments of investment can only be motivated by the rise of the intertemporal prices of a1 and b1, relative to b0 and a0, i.e. by the fall of the interest rates: no question of the increments of investment being caused directly by the additional consumptions ΔDa1, ΔDb1 entailed in the savings of equation (1.5b) — contrary to the case for the contemporary consumptions of equation (1.5c).

The idea that savings and investment in intertemporal equilibrium cause no more problems than relative demands for (contemporary) commodities should rather be turned upside down into the one that intertemporal equilibrium raises the problem of savings and investment in basically the same terms as traditional equilibrium does.

24. The problem then is of course that what the capital controversies taught about ‘capital reversing’ and ‘re-switching’ in traditional equilibrium — and has been confirmed for the present context in par. 19 — entails that the rise of the intertemporal prices Pi,t+1/Pi,t (i = a, b), i.e. a fall of the own rates of interest ri,t might fail to provide the entrepreneurs with a motive for that increase ‘in some sense’ of Ii which is required for the intertemporal adjustments in consumption. The result might then be the striking one that, however small the initial excess savings, the theory could force us to admit movement to an equilibrium with drastic changes in wages and prices (cf. in Figure 1.3 above, the equilibrium E1 to which there would be a tendency starting from the position ![]() for

for ![]() b in our original two-year model). Further, if the position

b in our original two-year model). Further, if the position ![]() with excess savings happened to be that for

with excess savings happened to be that for ![]() b < rb″ in Figure 1.1 (par. II, p. 125) the theory would force us to admit a tendency to negative interest rates if not to the zero intertemporal prices Pa0 and Pb0 for our economy with non-storable goods.50 And as indicated in par. [12] of Appendix I such zero intertemporal prices far from being a result of satiety, would mean that the attempt of some individuals to take care of even more acute scarcities in t = 1 runs counter to the inability of the market forces, as envisaged in the theory, to transfer consumption from t = 0 to t= 1.51

b < rb″ in Figure 1.1 (par. II, p. 125) the theory would force us to admit a tendency to negative interest rates if not to the zero intertemporal prices Pa0 and Pb0 for our economy with non-storable goods.50 And as indicated in par. [12] of Appendix I such zero intertemporal prices far from being a result of satiety, would mean that the attempt of some individuals to take care of even more acute scarcities in t = 1 runs counter to the inability of the market forces, as envisaged in the theory, to transfer consumption from t = 0 to t= 1.51

Alternatively we might find an equilibrium in which it is W0 which has to become zero,52 with the attending labour unemployment, when the initial con tracting had brought to a level rb for which ![]() >

> ![]() (see in Figure 1.3), the equilibrium E2 to which there would be a tendency when the economy happened to start from rb =

(see in Figure 1.3), the equilibrium E2 to which there would be a tendency when the economy happened to start from rb = ![]() b.

b.

25. The above difference between the cases of contemporary and intertemporal consumptions allows us to begin seeing how the concept of a quantity of capital enters intertemporal general equilibrium. What we have analysed in parr. 23–24 is no less and no more than the process of substitution between labour and “capital”, the single factor, which underlies the determination of distribution between wages and profits in the traditional versions of the theory, exemplified by our reference to Wicksell’s Lectures in par. 2. The process was there viewed as involving the entire capital and labour endowments, whereas here it has been dealt with from the viewpoint of flows and not funds. But if ‘capital’ was what Wicksell and traditional theorists dealt with for their determination of wages, interest and prices, then — as indeed we foresaw in par. 2 — ‘capital’ is also what we have dealt with when studying the forces that should correct a surplus or deficit of savings over investment, thus determining the prices, in particular the own interest rates, of our simple intertemporal equilibrium and their properties.

Thus we duly found there the central relevance of an inverse relation between the own interest rates and the ‘amount’ of means of production, i.e. of capital per worker in the economy: as we saw, only if that inverse relation holds, can entrepreneurs operate adjustments towards plausible equilibria in intertemporal consumptions. And that inverse relation is of course the same which was required to ensure adjustments to plausible equilibria in the market for ‘capital’ and the other factors in the traditional version of the theory. Also the consequences of the impossibility of measuring that ‘amount’, i.e. ‘capital’, in terms independent of distribution are then essentially the same as in the traditional versions of the theory. Also the consequences of the impossibility of measuring that ‘amount’, i.e. ‘capital’, in terms independent of distribution are then essentially the same as in the traditional versions of the theory. As we recalled in par. 21, that impossibility undermines the inverse relation between interest rates and capital intensity and therefore the uniqueness, stability and overall plausibility of the resulting equilibria.54

No important difference is on the other hand made by the fact that in the intertemporal versions the inverse relation concerns a set of own rates (intertemporal relative prices) rather than the traditional single interest rate. A tendency of the own rates to move in the same direction can be argued and, more importantly, any contrasting movements among the own rates can be seen to be due to intratemporal phenomena hardly relevant for intertemporal adjustments (cf. parr. [7]–[9] in Appendix I).

26. This re-emergence of the neoclassical need for a ‘quantity of capital’ in intertemporal equilibria goes back ultimately to the basic fact that the demand for capital goods obeys principles altogether different from those governing the demand for consumption goods (par. 12). Whereas the latter comes from preferences that are specific to the goods demanded, the former results from savers’ preferences that are non-specific to the individual capital goods, and are only specific with regard to the aggregates of them. This is lucidly expressed by Walras when he introduces savings in his general equilibrium as the demand of the particular commodity which he calls ‘perpetual future income’,55 with a price of its own which is the reciprocal of the (effective) interest rate. That of course means that, in proportion to their value, capital goods are perfect substitutes for the saver as means of transferring income in time.56

The question of a ‘quantity of capital’ in neoclassical theory is indeed no more than an application of Jevons’s ‘law of indifference’ concerning the single competitive price and hence a single magnitude by which we must refer to any commodity which individuals, in this case wealth holders, treat as homogeneous. Just as one chooses according to the principle of the minimum price between alternative sources of, e.g. ‘corn’ — so one chooses between the alternative sources of ‘perpetual net income’, the different capital goods, according to the minimum price of such ‘future income’ — i.e. the maximum of the effective net rates of return. Capital goods are no more distinct commodities for savers than physically homogeneous ‘corn’ from different farms is for its consumers.

In the case of capital goods, this basic fact is however obscured by a second fact, which mixes the market for the single commodity ‘future income’ with a second layer of markets and where, furthermore, a quite different kind of substitutability emerges among capital goods. Unlike homogeneous corn where the allocation of consumers’ demand among different merchants or farms is theoretically uninteresting beyond the application of Jevons’s law of the tendency to a single price, the allocation of the demand for future income among potential sources of supply involves nothing less than the entire theory of production — in order to determine the rentals of the several capital goods and their ratio to the respective supply price. This gives central visibility to that allocation and substitutability in production which, however, is ultimately no more relevant for an explanation of the rate of interest, or system of own rates of interest (intertemporal relative prices), than the analogous allocation of the aggregate demand for corn among the several farmers is for the explanation of the price of corn. Just as it is only the aggregate demand and the supply of corn that is relevant for determining the price of corn, so it is only the demand and supply of aggregates of capital goods that is relevant for the determination of the rates of interest.

27. The presence at some stage of the theory of a quantity representing aggregates of capital goods is therefore as inevitable for the neoclassical determination of prices on the basis of the demand and supply decisions of individuals,57 as is the presence of the quantity of each consumption good. Individual demand and supply decisions about capital goods are ultimately taken in terms of that ‘quantity’ just as the similar decisions about corn consumption are taken in terms of the quantity of corn. It is on a single commodity ‘capital’ and not on individual capital goods that savers’ preferences operate, whether in the traditional ‘fund’ context, or in the intertemporal ‘flow’ context.

The traditional versions of the theory, with their equilibrium condition of a uniform effective net rate of return on the supply prices of the capital goods, entailed already taking care of that single commodity at the level of the endowment of factors,58 and those authors did so by expressing the endowment of capital directly as a single ‘quantity of capital’, its allocation in a capital-goods vector being then an unknown of the system. The abandonment of that traditional long-period notion of the equilibrium — not to be confused, recall, with a stationary or steady state59 — and of its specific condition of a uniform effective rate on capital good supply prices has meant getting rid of the single commodity ‘perpetual net income’ and of its bearer, ‘homogeneous capital’, but only at the cost of assuming away, at the level of the factor endowments, the perfect substitutability of capital goods for the saver, and Jevons’s indifference law with it: no surprise, then, for the methodological problems which are raised by today’s pure theory.60

However, those high methodological costs may have been borne in vain. They have been borne, that is, for what may turn out to have been getting rid of the obviously inconsistent notion of a ‘quantity of capital’ at the level of the demands and supplies of the immediately visible factors of production, and therefore at the level of the endowments, in order to have it re-enter the theory at the less immediately visible but theoretically equivalent level of investment-demand and savings-supply.

Appendix I: The determination of the I and S schedules

[1] In par. 7 of the text1 we had a first check of the consistency of system (F) by counting independent relations and unknowns. The existence of economically meaningful solutions for the unknown prices and quantities of (F) in the economically relevant interval of rb, rbmin ≤ rb ≤ rbmax to be presently specified, is demonstrated in the Mathematical Note at the end of this volume (p. 469). However, an intuitive account of the demonstration is necessary for a better understanding of the argument which we have conducted, and of the assumptions we have introduced.

We start by noting the lower limit of the relevant interval of values of rb. Due to our assumption that no storage is possible for either commodity,2 the ‘intertemporal price’ Pb0/Pb1 can fall to zero and equation (1.6f) of par. 7 will accordingly give

| (1.6b) |

The specification of the upper limits of rb where W = 0 will, on the other hand, require a better acquaintance with the properties of system (F) and we shall come to it in par. [6] below. 4

[2] As we proceed to the intermediate range of rb, equations (1.2f) and (1.6f) of system (F) in par. 7 of the text allow us to write the second price equation (1.1f) as follows:

| (1.1a) |

where, having used equation (1.2f), Pa0 is now in effect the intertemporal price Pa0/Pb1 as, of course, is Pb0 = (1+rb).

Two implications of equation (1.1a) are of interest here.

(a) It is only for bb(1+rb) ≤ 1, i.e. for rb ≤ (1−bb)/bb that we may have non-negative values of both W and Pa0. Considering also rbmin from equation (1.6b), we may therefore begin to restrict our attention to the interval

|

(1.6c) |

of our independent variable, where (1−bb), and hence (1−bb)/bb, are evidently positive whenever the method of production of b is viable (par. 3 in the text).

(b) Equation (1.1a) above will then entail that for any rb in the interval (1.6c), non-negative levels of W require Pa0 to stay in the interval

|

(1.1b) |

Given, then, rb and Pa0 in the respective intervals (1.6c), (1.1b), equation (1.1a) will determine the corresponding non-negative level of W. Consequently the first of equations (1.1f) determines Pa1. Thus the entire series of prices and the wage will be uniquely determined by equations (1.1f), (1.2f) and (1.6f), once Pa0 is given, besides rb.

To that unique series of prices and the wage, there will correspond the quantities demanded expressed by the functions Da0, Db0, Da1, Db1. The amount of total savings S in equation (1.5f) with its physical components Sa, Sb of (1.5f) will then be determined as well. The methods of production of the two commodities, being given, the same will be the case for the amount of investment I of equation (1.4f) and its physical components Ia, Ib. Such quantities need be neither single-valued, nor continuous functions of Pa0.3 It will however follow common practice and not be unduly restrictive to make the following assumption:

Assumption (i) Given rb in the interval (1.6c), the quantities demanded Da0, Db0, Da1, Db1, and hence the aggregate quantities demanded A0D and B0D are single-valued, continuous functions of Pa0 in the interval (1.1b).4

[3] Thus, then, given a level of rb in the relevant interval, any level of Pa0 in the interval (1.1b) will entail a ratio δ = A0D/B0D which will generally differ from the ratio δ = A0S/B0S, equality with which is imposed by equation (1.7f). As we then change Pa0 in the interval (1.1b), there are three possibilities (cf. Figure 1.4 in the Mathematical Note to this chapter).

(a) At one or more levels of Pa0, δ = γ. Equation (1.7f) will be satisfied and we shall have a solution of (F) for each of those values of Pa0.

(b) Over the entire interval (1.1b) of Pa0, δ < γ. This will mean that at the given level of rb it will be impossible to use a0 in as high a proportion to b0 as that in which we find the two commodities in the endowment. This means then that a0 would be a free good in an equilibrium occurring at that level of rb, when, that is, A0D = A0S.

(c) Finally, over the entire relevant interval of Pa0, we shall have δ > γ. This is the case symmetrical to (b), in which b0 cannot be used in as high a proportion to a0 as B0S/A0S (in as low a proportion as AS/BS) and b0 would be a free good in an equilibrium occurring at that particular level of rb, which would then have to be rb = −1, because of Pb0 = 0.

Cases (b) and (c) would exclude an economic solution of system (F) as formulated in the text, with equalities in the first two relations (1.3f), but the simple economic rationale of the cases, i.e. the non-scarcity of either a0, or b0 when equality between demand and supply were to be achieved for the other, indicates that a solution could be ensured by a slight formal modification of (F).5 However, that would complicate the exposition and risk obscuring the main points we wish to bring out, which are altogether independent of that kind of excess supplies. We shall therefore leave aside cases (b) and (c), as on the other hand we implied already by assuming two (scarce) goods in our model, for period t = 0, no less than for t = 1. We may therefore render explicit the following assumption: