Chapter 7

Insurance Requirements

INTRODUCTION

Securing insurance should be the first order of business at the start of any new production, and coverage should be obtained from an insurance broker who specializes in insurance for the entertainment industry and has extensive knowledge of the business. In the whole scheme of things, there aren’t many brokers who do this, and of those who do, most are headquartered in Los Angeles, New York and London. CMM Entertainment (a subsidiary of C.M. Meiers Company, Inc.) is one such company, as is Aon/Albert G. Ruben Insurance Services, Arthur J. Gallagher & Co., DeWitt Stern Group, Marsh USA and Truman Van Dyke Company. If you’re working on a studio show or for a major independent production company, the studio or production company will most likely have an ongoing relationship with specific brokers and insurance carriers as well their own in-house risk manager – the point person for all production-related insurance matters. If you’re not working for a company that has a risk manager, then you’ll deal directly with a broker.

Just as there aren’t many brokers who specialize in entertainment insurance, there aren’t many insurance companies that will write policies required for production. A good broker will obtain quotes from various insurance carriers in order to recommend the one (or ones) that can provide you with the best deal for your project, even if sometimes it turns out to be a combination of policies from more than one company. If your broker can’t get you proposals from all of the companies doing film insurance, then you might want to have another broker secure additional quotes. It’s relatively simple to finalize a deal when it comes to coverages and pricing, but just as important as the cost of the various policies needed is the service your broker can provide. You may want to get bids from two or three different brokerages or from one broker you’ve developed a good working relationship with. Things to consider when making a decision as to which broker to go with is expertise, ability to respond immediately to last-minute needs, ability to get the best claim service and accessibility. With so many incentive programs being offered throughout the country and growing film centers popping up all over the United States, your broker should be licensed in all states. And with so many productions being shot outside of the United States, it’s also important that your broker have the appropriate international contacts.

As films continually become more complicated in terms of action, stunts, effects, technology and the reliance on highly paid actors and directors to carry entire pictures on their names alone, levels of financial exposures increase as well. Insurance companies and the brokers who represent them are taking a much closer look than ever before at each picture, vigorously investigating potential exposure and carefully assessing the risks.

The better brokerage firms employ risk control specialists who prove most helpful on pictures that involve stunts and effects. On films containing action, they might contact stunt coordinators and effects supervisors to discuss the concerns of the underwriter, how each stunt and effect is to be executed, the anticipated use of personnel and the safety procedures to be implemented. These reps are extremely knowledgeable and will offer advice and spend time on the set when action sequences are shot. Their sole purpose is to minimize risks and curb escalating losses suffered by insurance companies on action pictures and communicate with underwriters to help alleviate any concerns the insurance companies might have.

In addition to budgets and schedules, insurance companies examine the track record of the production company, the producer and director; where the show’s to be shot; its financing source; distribution and bond company agreements; cast; storyline; all potential hazards; safety guidelines and protection methods to be utilized; proposed travel; crew specifications and anticipated payroll; rare and expensive set dressing, props or wardrobe to be used; the use of animals, motorcycles, special vehicles and equipment, watercraft, aircraft or railroad cars; and all proposed action, stunts and effects.

Your broker should help you complete the application process, which can sometimes be handled over the phone or online. (You’ll find a sample application at the end of this chapter). Risk managers, brokers and underwriters review all scripts, contracts and budgets, in addition to detailed breakdowns of proposed stunts and effects. The backgrounds and experience levels of stunt coordinators and effects supervisors are scrutinized and proof of pyrotechnic licenses is required as well.

This chapter will touch on the basics of motion picture and television insurance, including both standard and supplemental coverages.

GENERAL INSURANCE GUIDELINES

• Set up a time for your risk manager or broker to come by the production office for an initial meeting with your production staff to go through basic insurance and claim procedures and forms.

• Once your policies are in place, have your risk manager or broker supply you with a list of coverages, limits and deductibles.

• Make sure you have a good supply of claim forms and are aware of all claims reporting procedures.

• E-mail a Request for Certificate of Insurance form (or make copies available) to departments that will need them. Request that they be filled out and e-mailed or submitted to the production office when a certificate is needed (see form at the end of the chapter).

• Make sure you have a good supply of blank certificates of insurance if you’re not going to be preparing certificates as PDF files or online.

• Because your payroll company will be supplying the workers’ compensation coverage for all those on payroll, ask the payroll company for a certificate of insurance (made out to the production and noting the name of your show) evidencing their proof of coverage.

• Have the same contact person at the payroll company send you a supply of Injury/Illness Report forms appropriate to the state(s) or country(ies) where you’ll be filming.

• Have your risk manager or broker supply you with a list of insurance-approved physicians who can perform cast physicals. Select the doctor you wish to use and call his or her office to introduce yourself (and your show) to the doctor’s staff.

• Have all location, lease and rental agreements checked by your project attorney as well as your risk manager or brker to make sure that all insurance requirements are reasonable and met.

• Confirm that all employees driving their own vehicles for business purposes confirm that they carry liability coverage and that their coverage is sufficient. Remind them that should they have an accident while driving for business, their own insurance is primary, and the production company is not responsible for physical damage to their vehicles.

• Talk to your risk manager or broker if you plan to use aircraft, watercraft or railroads as well as animals in your production. Any of these exposures dictate additional insurance considerations.

• Talk to your risk manager or broker about the coverages you’ll need if you’re planning on filming in another country.

• Ask your caterer (and any other independent contractor who has his or her own employees) for a certificate of insurance naming the production as additional insured. It should provide at least $1 million of commercial general and auto liability and show evidence of workers’ compensation and employer’s liability coverage.

• Make sure that your risk manager or broker receives a copy of all travel movements.

• Keep a log of all certificates of insurance issued and retain copies (in alphabetical order) in a three-ring binder.

• Keep a log of all workers’ compensation claims.

• If you’re going to be shipping equipment, materials, props, set dressing, wardrobe, etc. to another country, make sure your risk manager or broker receives a copy of your daily shipping log. (The log should contain date of shipment, origin, destination, general description of contents, method of transport and estimated value of shipment.)

• Determine early on during pre-production who’s going to be responsible for reporting and completing claim forms when auto accidents occur – and they almost always do. Some insurance carriers require that you complete a claim form and submit it to your broker (who will take it from there). Others require that you call a specific telephone number to report the accident and open a claim. Either way, decide whether the transportation department, the production office or both will be responsible for reporting accidents. Sometimes, Transpo will fill out an accident worksheet (see form at the end of this chapter) or call the production office with the details, and it’ll be the production coordinator or assistant coordinator who writes up or calls in to report the claim. And sometimes, Transpo handles it all. Just be sure to designate one individual as the “go-to” person for auto claims – someone who will keep an ongoing log of claims, will stay current as to the status of each and is the contact person for the insurance company’s claims rep. This person should also be distributing copies of the claim log as a way of keeping your risk manager, broker, producer, UPM and production executive advised of all ongoing claims – especially anything serious or any situation that could potentially develop into a lawsuit. This is one of many areas that if not handled properly could get totally out of hand, and you’ll be receiving claims a year or more after your show has wrapped with absolutely no idea of where they came from.

ERRORS AND OMISSIONS (E&O)

This is a coverage you have to “prove” you don’t need before you can obtain. It’s insurance for claims made for libel, slander, invasion of privacy, infringement of copyright, defamation of character, plagiarism, piracy or unfair competition resulting from the alleged unauthorized use of titles, formats, ideas, characters, plots, performances of artists or performers or other materials. It includes coverage for any legal expenses incurred in the defense of any covered claim as well as indemnity.

In order to secure E and O coverage, it’s imperative to have a clearance report done on your final script. Some studios have their own clearance departments, but if one isn’t available to you, send your script to a script clearance company. You can simply pay for a clearance report and then have your project attorney handle all necessary clearances and releases, or you can have a clearance person or company secure all necessary approvals, negotiate fees for the use of certain images, magazine covers, film clips, etc. and handle all necessary related releases and agreements. They’ll keep you posted as to which items have been denied clearance, which come with restrictions and which come with fees attached. The clearance company will submit a thorough report based on each item or reference, how it’s to be used, whether it’s been cleared or not and any additional notes associated with that item or reference. As long as you make all necessary script changes based on the items or references that have been denied clearance, you’ll be okay. The insurance company will want confirmation of script clearances before granting E&O coverage, and your distributor will want a copy of the report before agreeing to pick up your film.

Delivery requirements might dictate whether you need a one-or three-year policy. Some insurance companies also offer what’s referred to as a Rights Period Endorsement, which continues coverage for as long as your distribution contract calls for. Check with your broker to see which is the most cost-effective for your film and distribution deal.

I used to recommend that E&O coverage be immediately obtained upon starting pre-production, but as I’ve learned from my friends who do smaller-budgeted films, there are a lot of producers who can’t afford this coverage up front and will wait until their film has been edited and/or they have a distributor in place. Distributors simply require that it be in place before they buy the film.

An E&O application needs to be completed and signed by an authorized member of the production company, and prices for this coverage run from around $7,500 to $12,500, assuming there are no surcharges. There are some underwriters, though, who will negotiate a lower price based on your film’s budget.

If you choose to defer E&O coverage, have your insurance broker furnish you with an application form that contains a list of clearance requirements. These procedures, together with the clearance advice you receive from your project attorney, should be adhered to, because if it’s been determined that you haven’t followed mandated clearance procedures, it could create an impediment to getting an acceptable policy once you do apply. So do your due diligence, and send your script out for a proper clearance report. Then follow up by making sure that anything that needs to be cleared has been, that all necessary approvals have been secured and all release forms have been signed and received.

COMPREHENSIVE GENERAL LIABILITY

This coverage typically provides a combined single limit of $1,000,000 per occurrence and $2,000,000 in the aggregate (aggregate is a limit in an insurance policy stipulating the most it will pay for all covered looses sustained during a specified period of time) for bodily injury and property damage liability. The liability coverage includes: blanket contractual liability, products and completed operations, nonownership watercraft legal liability (usually restricted to vessels up to 26 feet in length), personal injury endorsement and fire damage legal liability.

Until fairly recently, you would have had to buy a minimum one-year general liability policy. Fortunately, many carriers now offer this coverage on a short-term basis, which is great news for your budget. (Short-term policies are available for most kinds of production insurance, but if you go this route, make sure that your workers compensation and general liability policies run long enough to cover any exposures you might have during pre-production, production and post production.)

CERTIFICATES OF INSURANCE

Evidence of insurance coverage is given in the form of a certificate of insurance. They’re issued by the production office (or in some cases, by the insurance broker or risk manager when specific wording is required, like for government entities) to a third party (such as a location or vehicle owner) as evidence of coverage. Certificates will reflect the name and address of the production company and name of the production. Spaces are provided to insert the date as well as the name and the address of the certificate holder – the individual or company you’re issuing the certificate to. Most certificates come with preprinted language on them that includes the certificate holder as Additional Insured and Loss Payee. Don’t add any additional language unless it’s been approved by your broker.

If a certificate holder is named as an additional insured, the insurance coverage will protect the certificate holder for claims arising out of the activities of the production company. A certificate holder who’s named loss payee is the owner of a vehicle or equipment being used on your film. If there’s a claim resulting from the loss or damage to their vehicle or equipment, reimbursement for the loss or damage would be paid to the loss payee.

Your insurance broker may require that you call their office to request additional insured or loss payee certificates when a certificate holder requests this additional coverage. Most often, though, these certificates are issued directly from the production office. What your broker will handle are certificates that require evidence of special coverages such as the use of watercraft, aircraft or a railroad.

Issuing certificates of insurance is becoming easier all the time. They can now be filled out on PDF forms and e-mailed to all appropriate parties. Some insurance companies even have dedicated websites so that the completion and distribution of certificates can be done online.

Copies of each certificate should go to the certificate holder (owner of the vehicle, property or equipment) and to your broker. You may be required to send a copy to your production executive or in-house risk manager, and you should keep a copy for the production files. If the certificate is for a vehicle, a copy should also be kept in the vehicle’s glove compartment.

HIRED, LOANED, DONATED OR NONOWNED AUTO LIABILITY

This coverage provides liability insurance for all hired, loaned, donated and nonowned motor vehicles. Vehicles owned by or leased to the company must be scheduled separately, and a charge is incurred for each vehicle. If an employee should have an accident while driving his or her personal car for company business, his own insurance is primary. The company’s policy would only insure the production should the employee’s coverage be insufficient – and it wouldn’t cover physical damage.

HIRED, LOANED OR DONATED AUTO PHYSICAL DAMAGE

This coverage insures against physical damage to hired, loaned and donated vehicles, including the risks of loss, theft or damage and collision for certain vehicles the production company is contractually responsible for. It’s not generally intended to cover physical damage to employees’ vehicles being used for production activities. If coverage is required, there must be a written rental agreement between the production company and the employee. The agreement must establish that the production company is responsible for the physical damage to the subject’s vehicle. It’s strongly suggested that your risk manager or broker be contacted to confirm coverage for employees cars, and that he or she review all applicable rental agreements. As with the auto liability coverage, vehicles owned by or leased to the company must be scheduled separately.

If a vehicle is damaged as a result of more than one incident, notation must be made as to the specific damage caused during each incident, the date and time of each, what the vehicle was being used for (was it a picture vehicle or a production vehicle?) and how the accident occurred. The insurance company won’t accept miscellaneous vehicle damage accumulated during the length of a production. It treats each occurrence as a separate accident, and a separate deductible applies to each occurrence. If you plan to use a picture vehicle for stunt work, include this information in your breakdown. Be aware that physical damage to vehicles used in stunts is generally not covered.

WORKERS’ COMPENSATION AND EMPLOYER’S LIABILITY

All employees are entitled to workers’ compensation benefits if they’re injured or acquire an illness directly resulting from or during the course of their employment. The benefits are established by state laws, and the premiums are based upon reportable payroll.

Workers’ compensation coverage should be supplied by the employer of record, that is, the paying entity, which is either the payroll service or the production company. Even if all employees are being paid through the payroll service, prudence further dictates that the production company still carry a minimum premium policy, insuring independent contractors, volunteers or interns who might work on your picture. A contingent workers’ compensation policy would also provide employer liability coverage should the need arise.

Independent contractors (or loanouts) – individuals who have their own corporations and aren’t paid through payroll – are supposed to carry their own workers’ comp insurance, and some studios and production companies will ask for proof of their coverage. But not all productions require verification, and not all loanouts carry their own insurance. So make sure your accountant (or payroll accountant) is aware of just how many loanouts on your show don’t carry their own coverage, and that your premium is sufficient to cover the loanouts’ reportable payroll.

If the employer of record is other than the production company or payroll service (for example, stunt coordinators hiring other stunt personnel or special effects supervisors hiring their own effects crew), obtain a certificate of insurance from the employers (department heads) to show evidence of workers’ compensation for their employees. If certificates aren’t obtained by the end of the show, this will come out at the insurance audit when payroll records and 1099s are reviewed. And in such cases, appropriate additional charges would be incurred based on the independent contractors’ payroll.

If your workers’ compensation coverage is coming from more than one source, make sure your set medic, second assistant director and/or studio medical department are informed as to which individuals are not covered under the payroll company’s policy. Make sure they have all the pertinent information on both policies (including policy numbers) and copies of applicable claim forms.

When a staff, cast or crew member is injured on the set, fill out a Worker’s Compensation – First Report of Injury or Illness form and note the incident on the back of the daily production report for that particular day. Send the report directly to the broker or payroll company, keep a copy for the production files and send a copy to your production executive. Also attach an additional copy to the back of the production report. Forward all medical bills, doctor’s reports, etc. to the respective insurance or payroll company.

When applying for workers’ compensation during preproduction, declare the need for coverage for employees hired in your state of operations as well as coverage for any other state where your employees are living at the time of hire (as long as they’re not being covered under the payroll company’s policy). Include an All States’ Endorsement with your Workers’ Compensation policy to protect the company should employees be hired from a state or states you hadn’t initially declared. Injured employees will receive benefits in accordance with the compensation laws of the state in which they were living at the time of hire. Six states (Nevada, Ohio, West Virginia, Wyoming, North Dakota and Washington) are monopolistic, meaning that you must purchase workers’ compensation coverage directly from their state insurance program if you choose to hire employees from their state.

Inform your insurance broker if members of your shooting company are going to be working on or near the water, as USL&H (United States Longshoremen’s and Harbor Workers) or Jones Act coverages might be required. The USL&H covers workers near the water, whereas the Jones Act deals with crew (i.e., vessel crew).

Your broker and/or the state’s workers’ compensation fund will supply you with appropriate injury report forms. Reporting procedures are the same in every state. Should a SAG-COVERED performer be injured in the course of employment with your company, the Screen Actors Guild requires that you send a copy of the accident report to them.

If you’re going to be shooting out of the country, talk to your broker, because you’ll need both foreign workers’ compensation and foreign liability. Check into any additional exposures you might need to cover, such as reparation expenses and injuries to foreign nationals. (Reparation expenses refer to the costs associated with transporting an injured or ill employee back home.)

GUILD/UNION ACCIDENT COVERAGE

Employees traveling on company business are covered under a travel accident policy, which provides coverage as specified in their governing guild or union bargaining agreements. If an employee isn’t a member of a union or guild, coverage is provided for a minimum amount. No employee, while on the company payroll, is allowed to fly as a pilot or as a member of a flight crew unless specifically hired for that duty and scheduled on the insurance policy. Under Guild/Union Travel Accident coverage, each production is required to keep track of: (1) the number of plane and/or helicopter flights taken by any guild/union member on each show, (2) the number of hours each person may spend in a helicopter, (3) the number of days each guild/union member may be exposed to hazardous conditions and (4) the number of days any DGA member may be exposed while filming underwater. This specific information may be requested from the insurance company at the completion of principal photography. Keep an ongoing log of all such occurrences, and keep your risk manager or broker updated.

Coverages for guild members pursuant to guild agreements should be provided by your payroll service if one is involved. And the production company should decide whether it’s going to obtain guild/union accident coverage for nonguild members.

PRODUCTION PACKAGE (PORTFOLIO POLICY)

The Production Package provides coverage for cast insurance; production media (any film, tape, disk or other medium or devices used to record or store sounds or images; faulty stock, camera and processing; props, sets and scenery, costumes and wardrobe; miscellaneous rented equipment and office contents; extra expense and third-party property damage).

The premium for the Production Package is usually based upon what’s referred to as “net insurable costs” – the final budget, minus the costs of post production, story, music and finance charges. Rates currently range from $0.75 to $1.25 (depending on negotiations, exposures, etc.) per each $100 of the net insurable costs. In some instances, however, third parties (i.e., banks or completion bond companies) have requested that story and finance charges be included as covered expenses. Under these circumstances, underwriters are usually willing to charge a lower rate for the premium. Also be aware that insurance costs are sometimes based on the total amount of your budget.

Your selection of optional coverages on any one show will be based on script and budgetary considerations, as well as requirements imposed by distributors and bond companies. Your insurance broker will discuss all variables and policy options with you and help you decide which coverages will provide the best protection for your picture. Also talk to your broker about other pricing choices, as insurance companies are now offering the option of portfolio policies based on your total (gross) budget (opposed to net insurable costs).

Cast Insurance

This coverage is placed on cast members, the director and possibly the producer or director of photography – any key person whose illness, injury or death would cause a shutdown of the production. If an accident or illness of a covered actress, actor, director, etc. creates a postponement, interruption or cancellation of production, the production company, subject to a predetermined deductible, would be reimbursed for the extra expenses incurred. And should a project be abandoned due to an insured cast lost, the production company would recoup all covered expenses (subject to the usual exclusions). This policy might also include coverage for kidnapping occurring during preproduction or filming and can include coverage for the payment of ransom demands. A thorough and complete substantiation of the company’s extra costs incurred due to such occurrences must be presented to the insurance company before a claim can be properly adjusted.

Some cast insurance policies allow coverage for a designated number of cast members within a scheduled period of time and others will cover an unlimited number of key people for an unlimited number of weeks until the production is completed.

The production policy application will usually ask if there are any specific contract requirements, such as stop dates on actors and directors. Typically, underwriters will require that there be a reasonable margin of safety – at least a two-week period to cover possible delays in completing principal photography. Should a show run over schedule, however, causing an artist to be unavailable due to an obligation to another production starting too soon after the original production’s scheduled wrap, the claim would be covered only if the delay was caused by an insured event and only if there is a “reasonable” period of time between the originally scheduled end of one production and the beginning of the next. When this type of claim is covered, it’s known as a stop date loss.

Depending on your policy, physical exams will be mandatory for some or all of those being covered under cast insurance, and your risk manager or broker will let you know how many exams are required. It’s not uncommon for seven performers (with the largest number of filming days) and the director to receive the exams.

You’ll be furnished with the name of a physician (or a choice of physicians) with whom you can set up appointments – all of whom have been approved by the insurance company. If you’re at a location or in a situation where it’s impossible to use a physician from the list, any licensed physician can do the exam, as long as it’s not a performer’s own personal physician. And in these situations, make sure the physician receives a Risk Specialists Exam Form to complete and submit.

Cast exams are arranged and paid for by the production. Appointments should be set up as soon as possible, and until they are, cast members (once officially “declared”) are covered for “accidents” only. Full coverage will follow pending their physicals. It’s usually the assistant production coordinator who coordinates the appointments with the actor’s agents and doctor’s office, and the cost of the exams should be PO’D (purchase orders should be made out for the exams and submitted to Accounting). There will be some actors (and from time to time, a director) who will request to be examined at their home, hotel room or on the set. If approved by the producer, this can be arranged with the doctor’s staff.

If one of your cast members has recently been examined for cast coverage on another show, you may request a waiver (relieving the actor of the obligation to have another exam) if the actor, along with the doctor who had done the prior exam, sign a warranty attesting to the results of the earlier physical. Your risk manager or broker will advise and supply you with the necessary form, which is called a Statement of Declared Artist’s Health.

The insurance company will pay closer attention to a cast member’s medical history when that person is either over-or underage or has had previous health issues. When employing minors, your broker needs to be aware of the childhood diseases they’ve had, because the diseases (such as chicken pox, measles and mumps) they haven’t yet had may be excluded from the policy. There may also be specific exclusions imposed upon principals who have had a history of alcohol or substance abuse. If any of these circumstances do exist, they should be brought to the attention of the producer as soon as possible, as a higher deductible, a higher premium or exclusions may be imposed.

Cast insurance usually starts three to four weeks prior to the commencement of principal photography, although additional prep coverage is often required. An example of this would be a key actor who’s involved with the project from the very early stages of pre-production.

If at any point during pre-production or production, the director, producer or one of the designated actors becomes ill, is injured or is incapacitated in any way, call your insurance representative immediately. If one of them feels ill yet continues working, but you’re not sure how he or she will be on the following day or how the schedule may be affected later in the week, alert your risk manager or broker as to the possibility of an interruption in filming. And if there’s ever a question as to whether you should call, call!

If a cast claim is submitted, the director or performer who is ill or injured should be seen by a doctor as soon as possible. Use the doctor who performed the initial cast exam if possible, but if it isn’t, be sure to submit the name of and contact information for the examining doctor to your broker. His or her report will be a necessary factor in substantiating the claim.

Essential Elements

This coverage is an optional endorsement that’s becoming more and more popular, especially with high-budget productions. An essential element would be an actor, actress, producer or director who carries an entire show on their name alone – someone without whom, if this person were to die or become ill or injured, the picture couldn’t be completed and delivered. At times, more than one key person may be designated as an essential element. If there’s essential element coverage, the inability of an essential element to continue working now gives the producer the option of abandoning the project and recouping all expenses. If it’s determined, however, that the essential element, after suffering an illness or injury, is likely to recover and resume his or her assigned role or position, the insurance company has the option to delay the abandonment of the insured production for a predetermined period of time.

The additional insurance would typically begin four weeks prior to principal photography and should be carried until at least two weeks after the completion of principal photography. In the case of an essential director, coverage might have to stay in effect through the director’s cut.

Before anyone is granted the status of essential element, their name must be on an “A” list of artists, or they must be approved by the underwriter. It’s mandatory that they have an extensive medical exam and also sign a warranty agreeing to refrain from hazardous activities on and off the set during the entire span of his contract. The payment schedule of the artists being insured is examined, as are any previous disabling illnesses or injuries.

Bereavement Coverage

This is another optional endorsement that would reimburse the production for expenses incurred when a key member of the cast or the director must interrupt his or her working schedule due to the death or severe illness or an unforeseen emergency involving an immediate family member.

Production Media (Film, Digital Elements or Other Medium)/Direct Physical Loss

Subject to specific exclusions, most of which are covered under a policy for faulty stock, camera and processing (described in the following section), this coverage protects against the direct physical loss, damage or destruction to all negative, videotape and digital elements, including work prints, cutting copies, fine-grain prints, sound tracks, audiotapes, videotapes, cassettes, hard drives, CDS and DVDS. In addition, coverage is included for accidental magnetic erasure on videotape production and has been adapted to cover the most up-to-date technological developments of videotape and digital production. It also includes coverage on all negative and videotape/digital elements while in transit.

Faulty Stock, Camera and Processing

Subject to certain exclusions, this coverage insures against the loss, damage or destruction of raw film stock or tape stock, exposed film, recorded videotape, digital elements and sound tracks/tapes caused by or resulting from fogging or the use of faulty equipment, faulty developing or faulty processing. It doesn’t cover losses due to mistakes made by the camera or sound crew.

Props, Sets and Scenery; Costumes and Wardrobe; Miscellaneous Rented Equipment; Office Contents

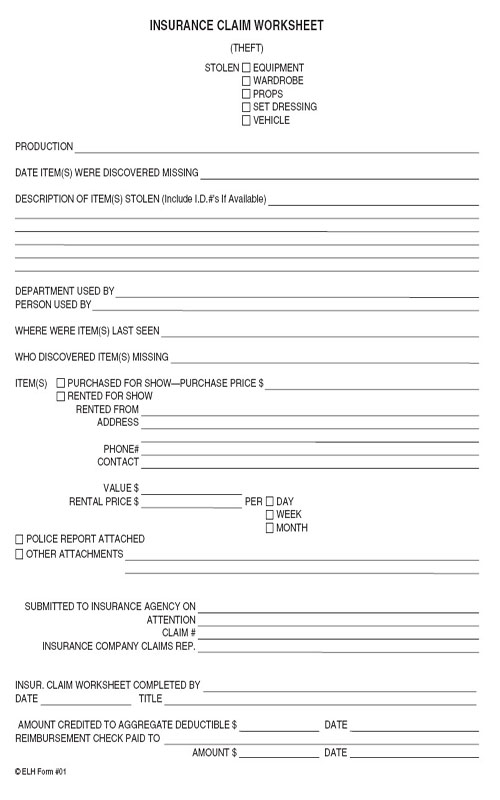

Subject to specified exclusions, these provide coverage against direct physical loss, damage or destruction to all property (contents, equipment, cameras, sets, wardrobe, lighting equipment, office furnishings, props, supplies, etc.) used in connection with the covered production. Keep running inventories of all set dressing, props, wardrobe, equipment, etc. that are purchased and/or rented for each show. If anyone on your crew notices that something is missing or damaged, inform the insurance agency, make a note of it on the inventory log and on the back of the daily production report and file a police report if applicable. At the end of the show, the insurance company may not honor claims on lost or damaged equipment, props, set dressing or wardrobe without sufficient documentation. Advise all department heads to inform the production manager or production coordinator of loss and damages as they occur and to not wait until the completion of principal photography to submit invoices for repairs and replacement costs.

In specific cases of missing equipment, props, set dressing or wardrobe, there must clearly be a theft for a claim to be honored. As soon as an item is discovered missing, file a police report to substantiate the theft. If at the end of principal photography, however, you discover you’re short a few pieces of equipment, a few props or some pieces of wardrobe and have no idea when any of these items were taken, this is considered “mysterious disappearance.” Without a police report and documentation indicating when each item was discovered missing, who discovered it missing, etc., a claim of mysterious disappearance isn’t covered.

No insurance reimbursements are issued for the loss of employees’ personal belongings, such as purses or clothing. If an employee is using his or her own personal computer, it’s rarely covered. Coverage would only occur if the computer is substantiated in an individual’s deal memo (and scheduled on his or her box rental inventory) or if there’s a specific contract stating that the production is responsible for these items. The problem can be with the deductible, as most policies have a deductible of at least $1,000.

Extra Expense

Claims of this type typically involve the damage or destruction of sets, props, wardrobe, vehicles, equipment, locations or facilities that actually interrupt, delay or cause the cancellation of production. It also covers additional expenses resulting from the short circuiting, electrical injury or failure of any electrical generator (portable or otherwise) used in production. This added protection covers expenditures over and above the total cost normally incurred to complete principal photography when any real and/or personal property is lost due to damage or the destruction of this property.

Third-Party Property Damage

This policy covers the production against accidental injury to or destruction of property of others while the property is in the care, custody or control of the production company (practical locations, for example).

Your insurance representative will advise you as to the specific limits and deductibles of this coverage and any additional optional coverages you might require based on the needs of your production.

SUPPLEMENTAL (OR OPTIONAL) COVERAGES

Umbrella (Excess Liability)

There will be times, with locations, for example, when higher limits than those provided under general liability and/or third-party property damage are mandatory. This coverage carries limits of liability in excess of $1,000,000. An umbrella liability policy will indemnify the insured for the ultimate net loss in excess of the underlying limit or the self-insured retention, whichever is the greater, because of bodily injury, personal injury or property damage to which the insurance applies.

Umbrella liability policies providing limits from $1 million to $25 million (and higher) are available. If, however, increased limits of liability are required for a short period of time only, excess limits can be obtained to comply with specific location or contract requirements. If your operations include filming at museums, airports or major office or manufacturing locations, umbrella liability is a must.

Use of Aircraft

Inform your insurance agency as soon as possible if you plan to use any type of aircraft in your show. In order to supply all the pertinent information needed on the aircraft, the owner of the aircraft and all proposed flying activities, you may be asked to have an “Aircraft Questionnaire” completed before adequate nonowned aircraft liability and/or hull coverages can be secured. Insurance is also needed to cover the use of hot air balloons, gliders, sailplanes and other types of aircraft.

To add protection for the possible negligence of the owner of the aircraft, it’s also strongly advisable that the owner be asked to name your production company as additional insured under his owner’s hull and liability insurance policies. The production should secure a Hold Harmless and Waiver of Subrogation with respect to loss or damage to the hull of the aircraft, so that the production isn’t responsible for any damage to it. Request a certificate of insurance from the owner of the aircraft evidencing the Waiver of Subrogation and including the production company as an additional insured.

Depending on contractual obligations, there are times when the production company may be responsible to insure the hull. It’s therefore necessary to furnish your broker or risk manager with a copy of your agreement with the aircraft provider.

Use of Watercraft

If you’re are going to be using a boat (watercraft) for the purpose of filming or carrying a film crew and/or equipment, discuss the details with your broker or risk manager to determine whether and what type of marine coverages are necessary, and provide him or her with copies of all pertinent agreements. And as with the use of any type of aircraft, you may be required to complete a “Watercraft Questionnaire” or supply additional information.

Use of Railroads or Railroad Facilities

For the use of railroads or railroad facilities, the production company is often required to indemnify the railroad for the production’s negligence as well as the railroad’s negligence.

Your broker or risk manager will need to review all contracts and agreements entered into with regard to the use of aircraft, watercraft or railroads before proper coverage can be determined.

Use of Valuables

Inform your broker or risk manager if you’re going to be using any fine arts, jewelry, furs or expensive antiques, and the values of each, so that limits can be increased as required. How these items are to be used must be discussed, so that appropriate coverage can be arranged.

Use of Livestock or Animals

If insurance coverage is necessary for livestock or animals to be used in a production, it’s arranged on a case-by-case basis and is based on contractual obligations and the value of the animal(s). Animal mortality insurance covers the death or destruction of any animal specifically insured. At no time would the limit of coverage be more than the value of the animal covered and before coverage is issued, a veterinarian certificate on the animal is necessary. Under certain circumstances, an animal may be insured under Extra Expense, and some carriers will use the cast insurance section of the policy to provide the coverage. This coverage reimburses the production company for extra expenses incurred due to the accident, illness or death of a covered animal. Depending on the value of the animal, the insurance company may require that you use backup animals (photo doubles).

Keep in mind that if you’re planning a scene that incorporates one type of animal (such as cattle) but you need another type of animal (such as horses) to wrangle the cattle, the horses would need to be covered as well as the cattle.

Signal Interruption Insurance

Insurance coverage is available to protect against exposures in the transmission of signals by satellite or closed circuit television. This coverage indemnifies the insured for loss of revenues resulting from the necessary interruption of business due to breakdown, failure or malfunction of any equipment that prevents the telecasting or presentation of the scheduled event.

Foreign Package Policy

When a production is filming outside of the United States, its territories or possessions, special coverages are necessary. Under these circumstances, it’s important to procure foreign liability, foreign workers’ compensation and foreign auto coverage. A domestic policy, however, won’t protect you against lawsuits filed in foreign countries.

Political Risk Insurance

This coverage is recommended for production companies planning to shoot in certain (potentially dangerous) foreign countries. Under this policy, the insurance company pays for loss due to physical property damage to insured assets caused by war, civil war and insurrection. It includes forced project relocation coverage, which pays the additional costs incurred solely and directly as a result of and following relocation of the production to another country. This coverage also includes any production-related confiscation or expropriation by a foreign government.

Weather Insurance

Weather insurance is available to protect against additional costs incurred in the event that your production is interrupted, postponed or canceled as a result of weather-related problems. The policy can include not only coverage for precipitation, but can be extended to include coverage for wind, fog, temperature and any other measurable weather conditions. The premium for this policy would be based on both the value of the days (or portion thereof) you wish to insure and the degree of bad weather you wish to insure against. The rate is determined by applying an agreed rate to the daily limit of insurance, taking into consideration the time of year, location and the agreed-upon measurements of weather that could trigger an insured event.

COMPLETION BONDS

Completion guarantees, also referred to as completion bonds, insure motion picture financiers against cost overruns in excess of their approved budget. In addition, they insure that the film will be delivered in accordance with all specifications contained in the financing and distribution agreements and in other related contracts that define the deal.

Major studios with the resources to finance pictures, including overages, don’t require bonding, as the functions provided by a bond company are handled in-house. Bond companies do service smaller studios and independent production companies, whose financiers and distributors require that their picture be bonded prior to the start of principal photography.

The formal issuance of a completion guaranty involves two separate documents. The producer’s agreement is signed by the producer and guarantor and is an acknowledgment and warranty by the producer to produce the film in accordance with the approved script, schedule and budget. The producer also agrees to take or cause no action that would void the approved insurance coverages or that would otherwise threaten the timely and efficient production of the film. In the event of default by the producer, this document gives the guarantor the ultimate right to take over the film and to complete and deliver it in the producer’s stead.

The completion guaranty is signed by the financier(s) and the guarantor. In this document, the guarantor agrees to deliver the film in accordance with the approved script, schedule, budget and contractual specifications and to pay any additional costs in excess of the approved budget required to deliver the project. In the event that the film can’t be delivered as guaranteed, the guarantor agrees to repay all funds that have been therefore advanced by the financier(s) to cover the costs of the approved budget. If the project has to be abandoned, financiers aren’t put in the position of having spent money on a project that wasn’t completed. In the event that the picture can’t be completed, financiers are repaid their investments. Though not able to collect additional revenues from box office grosses, he hasn’t lost anything either.

As do the insurance underwriters, completion guarantors carefully assess each project before committing to a bond. They want to know that you have a script with an adequate schedule and budget and a reputable and insurable cast and crew. They’ll review all major contracts relating to cast, locations, special effects, insurance, travel, etc. They’ll assign members of their staff to oversee projects from the beginning of pre-production through delivery; and at times, will hire an outside person to oversee a particular picture. Bond reps will receive copies of scripts, budgets, schedules, call sheets, production reports, weekly cost reports, etc. Some will attend a production meeting or two and make occasional visits to the set during production. Other bond reps will be more hands-on and remain with the shooting company on a daily basis, involved in all major decisions pertaining to the production. Much will depend on the bond company and its particular style of involvement, the relationship and track record between the production company or producer and the bond company and how each film is progressing. The ones that encounter the most difficulties are the ones more closely watched.

The traditional point where a bond company would take over a film is after the production has gone through their entire budget plus the full 10 percent contingency prior to the completion of the picture. This rarely happens, as the bond company’s job is to anticipate potential problems before they occur. It works diligently with the producer, director, cast and crew to keep things on schedule and on budget. Unless you have one company that you prefer working with, shop around for a completion guarantor, as rates are competitive and often negotiable.

CLAIMS REPORTING PROCEDURES

If an accident, injury or theft occurs; if the director or a cast member becomes ill and unable to work; or if you have a scratched negative or damage to equipment, props, set dressing or any of your sets, report it to your risk manager or insurance broker as soon as possible. Back up each reported occurrence in writing by completing an appropriate claim form, noting such on the back of the daily production report for that particular day and/or by writing a letter to the insurance agency containing as much detail as possible – when the incident occurred (date of loss), where it occurred, how it happened, who was there at the time, etc. Report any major theft or accident to the police and attach a copy of the police report to your letter to the insurance agency. Even if you’re not sure a loss would be covered, advise your insurance representative as to the possibility of a claim.

If a serious accident occurs, promptly record the names and phone numbers of witnesses (including staff, cast and crew members), so that an accurate description of the incident can be determined at a later date. Statements or reports should only be taken by authorized representatives of the production company, and in turn, should be submitted to your insurance representative.

When a claim occurs while a production is filming outside of the United States, a fluctuation in exchange rates can either be a deterrent or advantage. Claims can be covered at a predetermined exchange rate or at the exchange rate in effect at the time of the loss.

Submitting Claims

When an incident occurs resulting in an insurance claim, the accounting department should begin to tag each related invoice, indicating specific costs (or portions of costs) that were directly incurred as a result of the claim. When the claim is submitted, all related costs and overages should be presented budget-style, starting with a budget top sheet indicating the exact impact to each account. Copies of invoices should be coded and placed behind the top sheet in the correct order of accounts.

In addition to applicable police and doctor reports and copies of invoices, backup should also include call sheets; production reports; both original and revised schedules, day-out-ofdays, cast lists, etc. – anything to substantiate the changes created by the claim. Depending on the claim, copies of cast and crew deal memos, time cards, travel movement lists, equipment rental agreements and/or location agreements may also be required. For complicated or ongoing claims, it’s a good idea for the producer or production manager to either maintain a log of events pertaining to the claim on a day-to-day basis or to write memos to the file on a regular basis.

Begin each claim with a cover letter referencing the production, date of occurrence, claim number (if available), a description of the claim and a brief summary of the backup you’re providing. (I suggest binding the backup with brads or in file folders secured with Acco™ fasteners.) Start processing insurance claims as soon as they occur. Submit the full claim to the insurance agency as soon as costs can be assessed and backup provided. Don’t wait until the end of principal photography to start processing your claims.

Once a claim is reported to your insurance representative, it’s then turned over to an insurance agency claims representative. When all of the information is in order, the claim is then submitted to the insurance company, who may or may not (depending on the claim) assign it to an independent insurance auditor. It’s often advantageous for the production manager and production accountant to meet with the insurance auditor shortly after the incident occurs to better define the parameters of the claim and to know exactly what backup will be necessary.

For further information regarding any aspect of insurance, contact your insurance agent.

Assistance for this chapter was kindly provided by Marc J. Federman, Senior Vice President of CMM Entertainment, a subsidiary of C. M. Meiers Company, Inc., a Los Angeles–based insurance brokerage firm. Marc and I worked together many years ago; he’s been my insurance guru ever since and has been helping me with this chapter since the book was first published in 1993.

FORMS IN THIS CHAPTER

• Sample Insurance Application

• Request for Certificate of Insurance

The following forms are printed by Accord™ and are standard insurance forms used in our industry. You can use these, your insurance broker can send you a supply of blank forms, or you can check with your broker to see if they’re available as PDF files or online.

• Certificate of Insurance

• Property Loss Notice

• Automobile Loss Notice

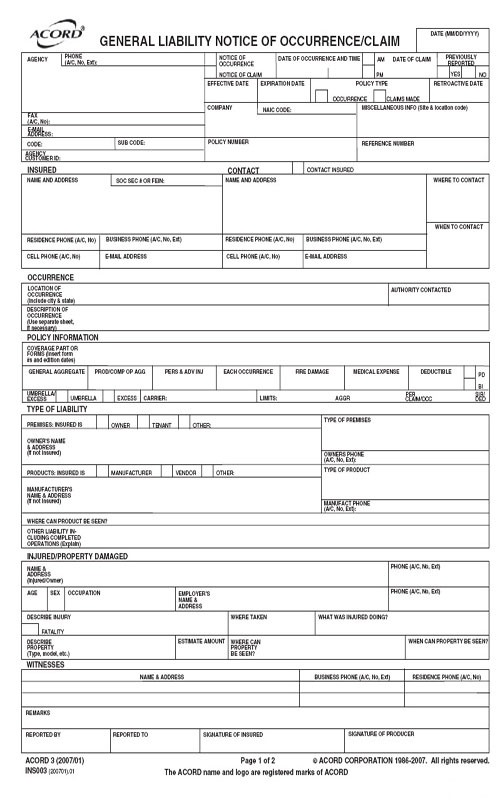

• General Liability Notice of Occurrence/Claim.

• Workers’ Compensation – First Report of Injury or Illness

The following four are worksheets that should be helpful when collecting information needed for the submission of claims:

• Insurance Claim Worksheet (Theft)

• Insurance Claim Worksheet (Damage)

• Insurance Claim Worksheet (Cast/Extra Expense/Faulty Stock)

• Insurance Claim Worksheet (Automobile Accident)

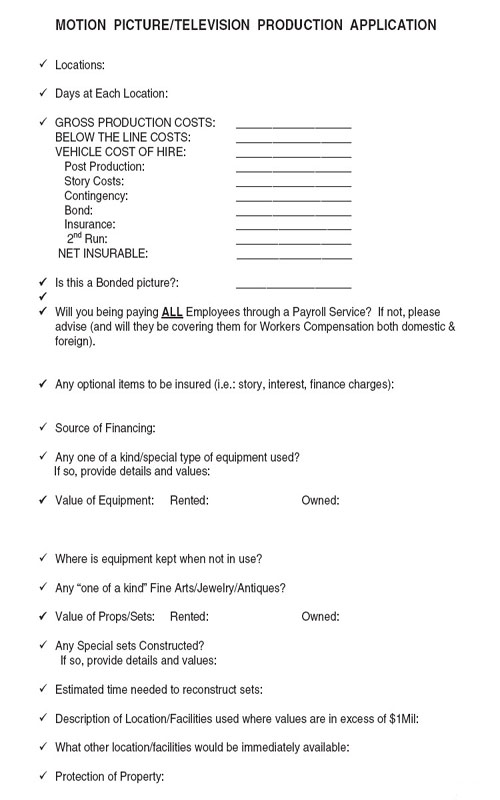

MOTION PICTURE/TELEVISION PRODUCTION APPLICATION

STUNT/PYRO/HAZARDOUS ACTIVITY QUESTIONNAIRE

NAMED INSURED: ________________________________________________________

PRODUCTION: ________________________________________________________

IN ORDER TO PROPERLY EVALUATE THE HAZARDS INVOLVING STUNTS USED IN FILMING, PLEASE PROVIDE THE ADDITIONAL INFORMATION REQUESTED. ADDITIONAL INFORMATION MAY ALSO BE REQUIRED.

1. TYPE OF SCENES BEING FILMED:

2. TYPE OF STUNT

3. PROTECTIVE MEASURES USED TO PROTECT PARTICIPANTS

4. PROTECTIVE MEASURES USED TO PROJECT PUBLIC

5. NAME OF EMPLOYER OF RECORD OF PERSON(S) PERFORMING STUNTS

6. HOW MANY PEOPLE INVOLVED IN STUNT SCENES?

7. PLEASE ATTACH RESUME OF STUNT COORDINATORS, FX COORDINATORS, FIRE COORDINATORS AND SO FORTH AS PERTAINS TO YOUR PLANNED ACTIVITY.

(PLEASE USE SEPARATE PAPER IF NECESSARY OR IF DOING ON COMPUTER, ADD PAGES TO END OF THIS DOCUMENT)

________________________________

INSURED’S SIGNATURE/DATE

For your protection, Arizona law requires the following statement to appear on this form. Any person who knowingly presents a false or fraudulent claim for payment of a loss is subject to criminal and civil penalties.

Applicable in Arkansas, District of Columbia, Kentucky, Louisiana, Maine, Michigan, New Jersey, New Mexico, New York, Pennsylvania and Virginia

Any person who knowingly and with intent to defraud any insurance company or another person, files a statement of claim containing any materially false information, or conceals for the purpose of misleading, information concerning any fact, material thereto, commits a fraudulent insurance act, which is a crime, subject to criminal prosecution and [NY: substantial] civil penalties. In ME, D. C., LA, and VA, insurance benefits may also be denied.

Applicable in California

Any person who knowingly files a statement of claim containing any false or misleading information is subject to criminal and civil penalties.

Applicable in Colorado

It is unlawful to knowingly provide false, incomplete, or misleading facts or information to an insurance company for the purpose of defrauding or attempting to defraud the company. Penalties may include imprisonment, fines, denial of insurance, and civil damages. Any insurance company or agent of an insurance company who knowingly provides false, incomplete, or misleading facts or information to a policy holder or claimant for the purpose of defrauding or attempting to defraud the policy holder or claimant with regard to a settlement or award payable from insurance proceeds shall be reported to the Colorado Division of Insurance within the Department of Regulatory Agencies.

Applicable in Florida and Idaho

Any person who Knowingly and with the intent to injure, Defraud, or Deceive any Insurance Company Files a Statement of Claim Containing any False, Incomplete or Misleading information is Guilty of a Felony.*

* In Florida - Third Degree Felony

Applicable in Hawaii

For your protection, Hawaii law requires you to be informed that presenting a fraudulent claim for payment of a loss or benefit is a crime punishable by fines or imprisonment, or both.

Applicable in Indiana

A person who knowingly and with intent to defraud an insurer files a statement of claim containing any false, incomplete, or misleading information commits a felony.

Applicable in Minnesota

A person who files a claim with intent to defraud or helps commit a fraud against an insurer is guilty of a crime.

Applicable in Nevada

Pursuant to NRS 686A.291, any person who knowingly and willfully files a statement of claim that contains any false, incomplete or misleading information concerning a material fact is guilty of a felony.

Applicable in New Hampshire

Any person who, with purpose to injure, defraud or deceive any insurance company, files a statement of claim containing any false, incomplete or misleading information is subject to prosecution and punishment for insurance fraud, as provided in RSA 638:20.

Applicable in Ohio

Any person who, with intent to defraud or knowing that he/she is facilitating a fraud against an insurer, submits an application or files a claim containing a false or deceptive statement is guilty of insurance fraud.

Applicable in Oklahoma

WARNING: Any person who knowingly and with intent to injure, defraud or deceive any insurer, makes any claim for the proceeds of an insurance policy containing any false, incomplete or misleading information is guilty of a felony.

For your protection, Arizona law requires the following statement to appear on this form. Any person who knowingly presents a false or fraudulent claim for payment of a loss is subject to criminal and civil penalties.

Applicable in Arkansas, Delaware, District of Columbia, Kentucky, Louisiana, Maine, Michigan, New Jersey, New Mexico, North Dakota, Pennsylvania, South Dakota, Tennessee, Texas, Virginia and West Virginia

Any person who knowingly and with intent to defraud any insurance company or another person, files a statement of claim containing any materially false information, or conceals for the purpose of misleading, information concerning any fact, material thereto, commits a fraudulent insurance act, which is a crime, subject to criminal prosecution and [NY: substantial] civil penalties. In DC, LA, ME, TN and VA, insurance benefits may also be denied.

Applicable in California

For your protection, California law requires the following to appear on this form: Any person who knowingly presents a false or fraudulent claim for payment of a loss is guilty of a crime and may be subject to fines and confinement in state prison.

Applicable in Colorado

It is unlawful to knowingly provide false, incomplete, or misleading facts or information to an insurance company for the purpose of defrauding or attempting to defraud the company. Penalties may include imprisonment, fines, denial of insurance, and civil damages. Any insurance company or agent of an insurance company who knowingly provides false, incomplete, or misleading facts or information to a policy holder or claimant for the purpose of defrauding or attempting to defraud the policy holder or claimant with regard to a settlement or award payable from insurance proceeds shall be reported to the Colorado Division of Insurance within the Department of Regulatory Agencies.

Applicable in Florida and Idaho

Any person who knowingly and with the intent to injure, Defraud, or Deceive any Insurance Company Files a Statement of Claim Containing any False, Incomplete or Misleading information is Guilty of a Felony.*

* In Florida - Third Degree Felony

Applicable in Hawaii

For your protection, Hawaii law requires you to be informed that presenting a fraudulent claim for payment of a loss or benefit is a crime punishable by fines or imprisonment, or both.

Applicable in Indiana

A person who knowingly and with intent to defraud an insurer files a statement of claim containing any false, incomplete, or misleading information commits a felony.

Applicable in Minnesota

A person who files a claim with intent to defraud or helps commit a fraud against an insurer is guilty of a crime.

Applicable in Nevada

Pursuant to NRS 686A.291, any person who knowingly and willfully files a statement of claim that contains any false, incomplete or misleading information concerning a material fact is guilty of a felony.

Applicable in New Hampshire

Any person who, with purpose to injure, defraud or deceive any insurance company, files a statement of claim containing any false, incomplete or misleading information is subject to prosecution and punishment for insurance fraud, as provided in RSA 638:20.

Applicable in New York

Any person who knowingly and with intent to defraud any insurance company or other person files an application for commercial insurance or a statement of claim for any commercial or personal insurance benefits containing any materially false information, or conceals for the purpose of misleading, information concerning any fact material thereto, and any person who in connection with such application or claim knowingly makes or knowingly assists, abets, solicits or conspires with another to make a false report of the theft, destruction, damage or conversion of any motor vehicle to a law enforcement agency, the Department of Motor Vehicles or an insurance company, commits a fraudulent insurance act, which is a crime, and shall also be subject to a civil penalty not to exceed five thousand dollars and the value of the subject motor vehicle or stated claim for each violation.

Applicable in Ohio

Any person who, with intent to defraud or knowing that he/she is facilitating a fraud against an insurer, submits an application or files a claim containing a false or deceptive statement is guilty of insurance fraud.

Applicable in Oklahoma

WARNING: Any person who knowingly and with intent to injure, defraud or deceive any insurer, makes any claim for the proceeds of an insurance policy containing any false, incomplete or misleading information is guilty of a felony.

A person who wilfully makes a false or misleading statement or representation for the purpose of obtaining or denying a benefit or payment is guilty of theft by deception.

Applicable in Arizona

For your protection, Arizona law requires the following statement to appear on this form. Any person who knowingly presents a false or fraudulent claim for payment of a loss is subject to criminal and civil penalties.

Applicable in Arkansas

Any person or entity who willfully and knowingly makes any material false statement or representation for the purpose of obtaining any benefit or payment, or for the purpose of defeating or wrongfully decreasing any claim for benefit or payment or obtaining or avoiding workers’ compensation coverage or avoiding payment of the proper insurance premium (or who aids and abets for either said purpose), under this chapter shall be guilty of a Class D. felony.

Applicable in California

Any person who knowingly files a statement of claim containing any materially false or misleading information ia subject to criminal and civil penalties.

Applicable in Colorado

It is unlawful to knowingly provide false, incomplete, or misleading facts or information to an insurance company for the purpose of defrauding or attempting to defraud the company. Penalties may include imprisonment, fines, denial of insurance, and civil damages. Any insurance company or agent of an insurance company who knowingly provides false, incomplete, or misleading facts or information to a policy holder or claimant for the purpose of defrauding or attempting to defraud the policy holder or claimant with regard to a settlement or award payable from insurance proceeds shall be reported to the Colorado Division of Insurance within the Department of Regulatory Agencies.

Applicable in Connecticut

This form must be completed in its entirety. Any person who intentionally misrepresents or intentionally fails to disclose any material fact related to a claimed injury may be guilty of a felony.

Applicable in Delaware and Oklahoma

Any person who knowingly and with intent to injure, defraud, or deceive any insurer, files a statement of claim containg any false, incomplete or misleading information is guilty of a felony. The lack of such a statement shall not constitute a defense against prosecution under this section. *Delaware Statutes Regulations: Del#C Section 913(B)

Applicable in Florida

Any person who, knowingly and with intent to injure, defraud or deceive any employer or employee, insurance company of self-insured program, files any statement of claim containing any false or misleading information is guilty of a felony of

Applicable in Idaho

Any person who Knowingly and with the intent to injure, Defraud, or Deceive any Insurance Company Files a Statement of Claim Containing any False, Incomplete or Misleading information is Guilty of a Felony.

Applicable in Indiana

A person who knowingly and with intent to defraud an insurer files a statement of claim containing any false, incomplete, or misleading information commits a felony.

Applicable in Kentucky, Michigan, New Jersey, New York and Pennsylvania

Any person who knowingly and with intent to defraud any insurance company or another person files a statement of claim containing any materially false information, or conceals for the purpose of misleading, information concerning any fact material thereto, commits a fraudulent insurance act, which is a crime, and subjects the person to criminal and [ny: substantial] civil penalties.

Applicable in Minnesota

A person who files a claim with intent to defraud or helps commit a fraud against an insurer is guilty or a crime.

Applicable in Nevada

Pursuant to NRS 686A, 291, any person who knowingly and willfully files a statement of claim that contains any false, incomplete or misleading information concerning a material fact is guilty of a felony.

Applicable in New Hampshire

Any person who, with purpose to injure, defraud or deceive any insurance company, files a statement of claim containing any false, incomplete or misleading information is subject to prosecution and punishment for insurmance fraud, as provided in RSA 638:20.

Applicable in Ohio

Any person who, with intent to defraud or knowing that he/she is facilitating a fraud against an insurer, submits an application or files a claim containing a false or deceptive statement is guilty of insurance fraud.

Applicable in Tennessee

It is crime to knowing provide false, incomplete or misleading information to any party to a workers compensation transaction for the purpose or committing fraud. Penalties include imprisonment, fines and denial of insurance benefits.

Applicable in Utah

Any person who knowingly presents false or fraudulent underwriting information, files or causes to be filed a false or fraudulent claim for disability compensation or medical benefits, or submits a false or fraudulent report or billing for health care fees or other professional services is guilty of a crime and may be subject to fines and confinement in state prison.

EMPLOYEE SIGNATURE:___________________________________

DO NOT ENTER DATA IN SHADED FIELDS

DATES:

Enter all dates in MM/DD/YY format.

SIC CODE:

This is the code which represents the nature of the employer’s business which is contained in the Standard industrial Classification Manual published by the Federal Office of Management and Budget.

CARRIER:

The licensed business entity issuing a contract of insurance and assuming financial responsibility on behalf of the employer of the claimant.

CLAIMS ADMINISTRATOR:

Enter the name of the carrier, third party administrator, state fund, or self-insured responsible for administering the claim.

AGENT NAME & CODE NUMBER:

Enter the name of your insurance agent and his/her code number if known. This information can be found on your insurance policy.

OCCUPATION/JOB TITLE:

This is the primary occupation of the claimant at the time of the accident or exposure.

EMPLOYMENT STATUS:

Indicate the employee’s work status. The valid choices are:

Full-Time On Strike Unknown Volunteer Part-Time Disabled Apprenticeship Full-Time Seasonal Not Employed Retired Apprenticeship Part-Time Piece Worker

DATE DISABILITY BEGAN:

The first day on which the claimant originally lost time from work due to the occupation injury or disease or as otherwise deigned by statute.

CONTACT NAME/PHONE NUMBER:

Enter the name of the individual at the employer’s premises to be contacted for additional information.

TYPE OF INJURY/ILLNESS:

Briefly describe the nature of the injury or illness, (eg. Lacerations to the forearm).

PART OF BODY AFFECTED:

Indicate the part of body affected by the injury/illness. (eg. Right foream, lower back.)

DEPARTMENT OR LOCATION WHERE ACCIDENT OR ILLNESS EXPOSURE OCCURRED:

(eg. Maintenance Department of Client’s office at 452 Monroe St., Washington, DC 26210)

If the accident or illness exposure did not occur on the employer’s premises, enter address or location. Be specific.

ALL EQUIPMENT, MATERIAL OR CHEMICALS EMPLOYEE WAS USING WHEN ACCIDENT OR ILLNESS EXPOSURE OCCURRED:

(eg. Acetylene cutting torch, metal plate)

List all of the equipment, materials, and/or chemicals the employee was using, applying, handling or operating when the injury or illness occurred. Be specific, for example: decorator’s scaffolding, electric sander, paintbrush, and paint.

Enter “NA” for not applicable if no equipment, materials, or chemicals were being used. NOTE: The items listed do not have to be directly involved in the employee’s injury or illness.

SPECIFIC ACTIVITY THE EMPLOYEE WAS ENGAGED IN WHEN THE ACCIDENT OR ILLNESS EXPOSURE OCCURRED:

(eg. Cutting metal plate for flooring)

Describe the specific activity the employee was engaged in when the accident or illness exposure occurred, such as sanding ceiling woodwork in preparation for painting.

WORK PROCESS THE EMPLOYEE WAS ENGAGED IN WHEN ACCIDENT OR ILLNESS EXPOSURE OCCURRED:

Describe the work process the employee was engaged in when the accident or illness exposure occurred, such as building maintenance. Enter “NA” for not applicable if employee was not engaged in a work process (eg. walking along a hallway).

HOW INJURY OR ILLNESS/ABNORMAL HEALTH CONDITION OCCURRED. DESCRIBE THE SEQUENCE OF EVENTS AND INCLUDE ANY OBJECTS OR SUBSTANCES THAT DIRECTLY INJURED THE EMPLOYEE OR MADE THE EMPLOYEE ILL:

(Worker stepped back to inspect work and slipped on some scrap metal. As worker fell, brushed against the hot metal.)

Describe how the injury or illness/abnormal health condition occurred. Include the sequence of events and name any abjects or substance that directly injured the employee or made the employee ill. For example: Worker stepped to the edge of scaffolding to inspect work, lost balance and fell six feet to the floor. The worker‘s right wrist was broken in the fall.

DATE RETURN(ED) TO WORK:

Enter the date following the most recent disability period on which the employee returned to work.