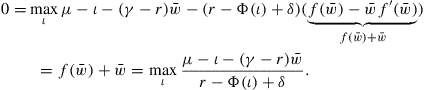

Chapter 2

Dynamic Security Design and Corporate Financing*

Abstract

Keywords

Security design; Dynamic contracts; Moral hazard; Asymmetric information; Signaling; Incentives

1 Introduction

Modigliani and Miller (1958), hereafter MM, argue that under certain idealized assumptions firm capital structure is irrelevant, i.e. it does not affect firm value. These conditions include:

1. There are no taxes or bankruptcy costs.

2. There are no agency problems.

3. There are no differences in information between insiders and outside investors.

4. Capital markets are frictionless, i.e. market participants are perfectly competitive and have no market power, and there is no security mispricing.

Of course, we know that these idealized conditions clearly fail in practice. The important message of the Modigliani–Miller theory is that it rules out certain commonly used arguments about capital structure as incorrect or incomplete. These arguments typically fail to take into account that the riskiness of securities used in capital structure, and thus their required return, depend on the capital structure itself. Here are some typical examples:

A. An argument against higher capital requirements for banks: because equity has a higher required return than debt, requiring banks to hold more equity in their capital structure to absorb risk will make banks less profitable. This argument fails to take into account that a decrease in leverage makes equity less risky, and thus lowers the cost of equity.1

B. An argument that calls on technology firms, such as Apple, to pay out their cash holdings, because cash earns a much lower rate of return than these firms’ cost of capital. This argument fails to take into account that cash is less risky than the rest of the firm and so the required return on cash is significantly lower than the cost of equity.

C. An argument that merging firms can create value for their shareholders through “corporate diversification”. This argument ignores that shareholders can diversify themselves.

Of course, there are valid contributions to these debates that are based on the violations of Modigliani–Miller conditions. These focus on the relationship between leverage/cash holdings and incentives, distinctions between inside and outside equity, and bankruptcy costs. This essay explores the implications of these frictions on capital structure.

The Modigliani–Miller Propositions. Consider a firm that generates a random stream of cash flows:

![]()

at time points 1, 2, etc. Firm capital structure divides these cash flows between debt holders and equity holders, and possibly other security holders, in some way. According to MM, the value of the firm does not depend on how these cash flows are divided among the firm’s stake holders. Behind this result is the principle of arbitrage. Using frictionless financial markets, participants should be able to replicate the payoff of any structured security backed by the firm’s cash flows, with zero transaction costs and zero market impact.

The most basic example that illustrates the MM propositions involves a one-period firm that generates a single random cash flow of ![]() at date 1. Suppose that the firm has debt with face value D and the risk-free interest rate is r. Then at date 1, debt holders get (1 + r)D and equity holders get

at date 1. Suppose that the firm has debt with face value D and the risk-free interest rate is r. Then at date 1, debt holders get (1 + r)D and equity holders get ![]() , assuming that

, assuming that ![]() is always large enough to make debt risk-free. Denote by E the market value of this firm’s equity.

is always large enough to make debt risk-free. Denote by E the market value of this firm’s equity.

MM Proposition 1

Assume that there is an identical all-equity firm 2, with value V. That is, firm 2 also generates a cash flow of![]() at date 1. Then:

at date 1. Then:

![]()

That is, the two firms with different capital structure but the same cash flows have the same value.

Proof.

The proof uses the principle of arbitrage.

If D + E > V, consider selling short a fraction α > 0 of equity of firm 1, borrowing αD, and using αV < αE + αD of the proceeds to buy a fraction α of firm 2. This position can be liquidated at no cost at date 1, since the proceeds ![]() from the stake in firm 2 are just sufficient to repurchase equity of firm 1 for

from the stake in firm 2 are just sufficient to repurchase equity of firm 1 for ![]() and have

and have ![]() left to pay down debt. At the same time, this trading strategy generates an instantaneous profit of αE + αD − αV at date 0. That is, if D + E > V than there is an arbitrage opportunity.

left to pay down debt. At the same time, this trading strategy generates an instantaneous profit of αE + αD − αV at date 0. That is, if D + E > V than there is an arbitrage opportunity.

If D + E < V then this strategy can be executed in reverse to generate an instant profit of αV − αE − αD.

MM Proposition 2 derives how the required return on the firm’s equity changes with capital structure. Let ![]() and denote by:

and denote by:

![]()

the req uired rate of return on the firm’s assets.

MM Proposition 2

The required rate of return on the firm’s equity, ![]() , satisfies

, satisfies

![]()

This proposition implies that, if firm investors require compensation for the firm’s risk, that is, rA > r, then as firm leverage D/E increases, the cost of equity rE increases. That is, as equity becomes riskier with greater leverage, equity holders require a higher compensation for risk.

MM Proposition 2 is related to example A about the amount of equity that banks are required to hold to absorb losses. Under MM assumptions, higher capital requirements would not make banks less profitable because lower leverage would lead to a lower cost of equity. Of course, violations of the MM assumptions immediately enter the debate. A key counterargument is that debt has a tax advantage, and thus leverage can reduce the cost of capital.

The focus of this essay is the relationship between information and capital structure. Insiders, e.g. firm managers, may have information about firm fundamentals that the market does not know. There may also be a conflict of interest, i.e. agency problems, between firm insiders and outside investors. Models of these informational problems predict a specific division of cash flows between insiders and outsiders. A typical result is that insiders must hold an equity-like security backed by the firm’s assets. Such a security allows insiders to signal good information about firm fundamentals in settings with adverse selection, and it gives insiders incentives to take actions that increase firm value in settings of moral hazard.

While models of agency problems and asymmetric information have very clear implications on the division of cash flows between insiders and outsiders, they typically say very little about the division of cash flows among outsiders. Trade-off theory models, such as that of Leland (1994), explore the optimal division of firm cash flows between outside debt and equity holders taking into account tax advantages of debt and bankruptcy costs.

The rest of the essay is organized as follows. In Section 2 we review theories of capital structure based on static models of informational asymmetries. In Section 3 we move on to a dynamic environment based on the model of Leland (1994), in which we explore trade-offs between bankruptcy costs and tax advantages of debt, and incentive properties of simple contracts. In Section 4 we explore the full-blown problem of optimal contracts in dynamic moral hazard environments. In Section 5 we explore dynamic adverse selection and market dynamics.

2 Informational Problems in Static Models

In this section we explore static models of informational problems. One classic early reference on capital structure and the scope of the firm in the presence of agency models is Jensen and Meckling (1976). If a firm manager is risk-neutral, then a 100% managerial equity stake in the firm leads to an efficient outcome. The manager will then take actions that maximize the shareholder value of the firm (which includes the value of non-pecuniary benefits that the manager receives). Moreover, if the manager has private information about firm fundamentals, he does not have any incentive to misrepresent it to the market.

If the manager is risk-averse, then the optimal security design problem becomes nontrivial. The most rudimentary way to capture risk-aversion in a model is by imposing a limited liability constraint—the manager cannot consume negative amounts, and a more general way is by assuming a concave utility function. If so, then it may be necessary and beneficial for the manager to sell some of his equity stake, or another security backed by the firm’s assets, to raise funding for the firm. Selling securities to raise funds can lead to various inefficiencies: reducing the manager’s effort, requiring costly monitoring actions or inefficient project liquidation. It may also be difficult to sell securities due to informational asymmetries. In this section we explore various static models where this happens.

2.1 Moral Hazard

Townsend (1979): Townsend’s costly state verification model, which has been adapted to finance settings by Gale and Hellwig (1985), has been used widely in applications, including macro economics in work of Bernanke and Gertler (1989) and Bernanke, Gertler, and Gilchrist (1999). The costly state verification model captures deadweight costs that outside investors might need to incur to monitor the manager. A monitoring action can be required because the manager privately observes the firm’s profits, which he may divert and refuse to pay back to investors.

Consider an agent with a profitable project, which needs an investment of I > 0. The agent does not have the full amount to invest, and needs to raise some money from an outside investor, the principal.

If the investment is made, the project has a random gross return ![]() , distributed on

, distributed on ![]() with CDF F. Only the agent observes the true returns. However, the principal can verify returns at a cost c. Both the agent and the principal are risk-neutral, but the agent has limited liability—he cannot be forced to pay back more than what he claims to have, or more than what he actually has if verification takes place. An optimal contract maximizes the principal’s profit subject to giving the agent a specific expected gross payoff of W0. The value of W0 depends on the agent’s contribution towards the up-front investment, and the relative bargaining powers of the principal and the agent. Assuming that the principal must contribute a strictly positive amount to up-front investment,

with CDF F. Only the agent observes the true returns. However, the principal can verify returns at a cost c. Both the agent and the principal are risk-neutral, but the agent has limited liability—he cannot be forced to pay back more than what he claims to have, or more than what he actually has if verification takes place. An optimal contract maximizes the principal’s profit subject to giving the agent a specific expected gross payoff of W0. The value of W0 depends on the agent’s contribution towards the up-front investment, and the relative bargaining powers of the principal and the agent. Assuming that the principal must contribute a strictly positive amount to up-front investment, ![]() .

.

Assuming that the principal can perfectly commit to any contract, we can use the revelation principle to consider only truth-telling contracts, in which the agent directly reports realized output (see Myerson, 1979). We can focus on contracts {V, g(x)}, where V ⊆ [0, X] is the set of reports that the principal commits to verify, and g(x) ≤ x is a transfer that the agent is required to make if he reports x and is not caught lying. If the agent is caught lying then without loss of generality we assume that the principal takes away the agent’s entire output. This transfer rule off the equilibrium path gives the agent the maximal incentive to tell the truth.

In this notation, the optimal contracting problem is written as follows:

The truth-telling constraints require that the agent be at least as well-off telling the truth rather than lying, after any output realization. Rather than writing out all truth-telling constraints explicitly, we provide a lemma that characterizes the set of all contracts that satisfy the truth-telling constraints.

Lemma 1

A feasible contract satisfies the truth-telling constraints if and only if for some constant D:

Proof

(⇒) If the agent chooses to report in the non-verification region, he will choose a report that involves the smallest transfer. Therefore, if (A) fails, it is not incentive-compatible to tell the truth in the non-verification region. Similarly, if (B) fails, then there is x ∈ V with g(x) > D. But then the agent would prefer to report something in the non-verification region than to report x. We conclude that A and B must hold in a truth-telling contract.

(⇐) If x ∈ V, then the agent weakly prefers to tell the truth and pay a transfer of g(x) rather than announce something outside V and pay D or announce something else in V and pay x. If x is outside V, then the agent is indifferent among all announcements that do not trigger verification, but weakly prefers them to any announcement that does lead to verification. Hence, truth-telling incentives hold.

The following theorem solves for the optimal contract, and shows that it takes the form of debt.

Theorem 1

The optimal contract is a standard debt contract, as illustrated inFigure 1, i.e. ∃ D s.t.

Figure 1 Function g(x) and the verification region in the standard debt contract.

Proof

Since the contract must satisfy the truth-telling constraints, there exists D such that g(x) ≤ D for x ∈ V and g(x) = D for x outside V. Then, by the feasibility constraints, the entire interval [0, D) must be a subset of V.

If we have a contract that does not satisfy the conditions outlined in Theorem 1, as illustrated on the left panel of Figure 2, we can strictly improve it in two steps. First, as illustrated on the middle panel, let us (1) move all points in V ∩ [D, X] to the non-verification region, (2) raise g(x) to D on V ∩ [D, X], and (3) raise g(x) to x on [0, D). Then the new contract satisfies the truth-telling constraints and generates higher total surplus (sum of the principal’s and agent’s payoffs), but it generates a strictly lower payoff than W0 to the agent. We then transfer value from the principal to agent, and improve surplus further, by lowering D in the second step (as shown in the right panel of Figure 2), to the point where the agent’s expected payoff equals exactly W0

Figure 2 The proof of Theorem 1.

Remark 1

A moral hazard problem exists when the agent can take an action that yields him private benefit and at the same time reduces the overall value of the project. In this setting, such an action is hiding output. A solution to a moral hazard problem requires the agent to hold some type of equity-like security. Such a security prevents the agent from taking at least some actions that are detrimental to the overall value of the project. In this setting, the agent’s security is equity in the non-verification region, i.e. he gets a marginal payoff of 1 for each incremental dollar of cash flows.

Remark 2

We assumed that only deterministic verification is allowed. If the principal could commit to stochastic verification, he could design a better contract.

Remark 3

We assumed that the principal can fully commit to any contract. This assumption provides a useful benchmark for the analysis of contracting problems. The assumption of commitment can be relaxed. In this setting, if the principal cannot commit to verify the agent, we can instead consider contracts in which the principal can have a right, but not an obligation, to verify. Under this alternative assumption, the revelation principle no longer holds but an equally efficient outcome may be attained under additional conditions.

Remark 4

The moral hazard problem has implications on the optimal amount of investment and the scale of the firm. Generally, the optimal scale rises with the amount of wealth that the agent is able to contribute into the project. In the following example, the project is infeasible if the agent cannot contribute towards up-front investment. If the agent can contribute an amount E > 0, the optimal scale rises linearly in E.

Consider a scalable project, which generates a cash flow uniformly distributed on [0, 3I] when an investment of I is made. Cash flows can be verified at the cost of cI, where ![]() . Then the principal’s payoff as a function of D is:

. Then the principal’s payoff as a function of D is:

![]()

The debt face value that maximizes this expression is D = (3 − c)I, and so the principal’s maximal payoff is (3 − c)2I/6. Consequently, the maximum amount the firm can borrow, i.e. its debt capacity, is also (3 − c)2I/6. Since ![]() , then the project debt capacity is less than I, and so the project is infeasible unless the agent contributes to up-front investment.

, then the project debt capacity is less than I, and so the project is infeasible unless the agent contributes to up-front investment.

Now, suppose the agent is able to contribute E > 0 towards up-front investment. Then investment greater than E/(1 − (3 − c)2/6) is infeasible, because in this case, the amount the agent must borrow, I − E, would exceed the firm’s debt capacity. Optimal investment is in the interval (0, E/(1 − (3 − c)2/6)): it maximizes the agent’s expected payoff

![]()

subject to the constraint that the principal breaks even, i.e. ![]() . Due to the scale invariance of this example, the optimal level of investment is increasing linearly in E.2

. Due to the scale invariance of this example, the optimal level of investment is increasing linearly in E.2

Bolton and Sharfstein (1990) presents a simple two-period model of moral hazard, which provides a useful link from static to fully dynamic infinite-horizon models. One of the implications of this model is that future investment and the probability of continuing the project can depend on past performance even when future NPV is unrelated to past performance.

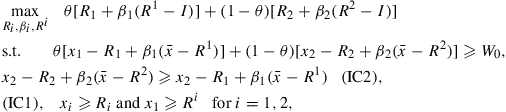

A manager has an opportunity to operate the firm for 2 periods, but needs financing from outside investors. In each period, if the firm gets outside funding to make an investment of I, it gets cash flows x1 ≥ 0 with probability θ and x2 > x1 with probability 1 − θ. Cash flows are i.i.d. over time, and there is no discounting between periods. Figure 3 illustrates possible outcomes if investment is always made.

Figure 3 Possible outcomes in the model of Bolton and Sharfstein (1990).

As in Townsend (1979), the agency problem is that only firm manager, and not the outsiders, observe the true cash flows. The agent cannot pretend that he got a lower cash flow than x1 ≥ 0, since that is the worst cash flow realization. However, costly state verification is not possible, so the manager can always divert the residual x2 − x1 for personal consumption if he receives a high cash flow.

Assume that x1 < I, so that in a one-period version of this model investment is infeasible if the agent cannot contribute his own funds towards investment.

We also assume that

![]()

That is, if cash flows were verifiable it would be profitable to invest in every period.

By the revelation principle we can restrict attention to contracts in which the manager reports true cash flows, and transfers from the manager to the investors and the probability of continued financing depend on the manager’s report. Because in the second period the agent will tell the truth only if he is required to make the same transfer regardless of realized cash flow, we can restrict attention to contracts defined by:

• Ri, the payment the manager makes at the end of period 1 if he reports xi,

• βi, the probability of continued financing in the second period if the report is xi, and

• Ri, the payment at the end of period 2 if the manager reports xi in period 1.

An optimal contract maximizes the principal’s profit subject to giving the agent an expected gross payoff of at least W0. The value of W0 is determined by the amount the agent can contribute to up-front investment, and the relative bargaining powers of the principal and agent. Formally, we would like to solve

where the objective function is the principal’s gross profit (after initial investment in period 1). The constraint (IC2) guarantees that if the agent receives a high cash flow of x2, his payoff if he reveals it truthfully, the left-hand side of (IC2), is at least as good as his payoff if he reports cash flow x1 instead. Note also that we did not write out explicitly the analogous truth-telling constraint (IC1) for the low cash flow realization in period 1. We do not expect it to bind, as verified after we derive the optimal contract.

Theorem 2

An optimal contract is as follows: R1 = R2 = x1, β2 = 1 and

Proof

First, without loss of generality we can take R1 = R2 = x1. Indeed, if Ri < x1 then by increasing Ri to x1 and reducing Ri by βi(x1 − Ri), we get a payoff-equivalent contract in which all constraints are still satisfied.

Second, we claim that β2 = 1. If not, let us increase β2 to 1 and R2 by ![]() . Then the left-hand side of (IC2) does not change, and neither does the agent’s payoff. Furthermore, since (IC2) is satisfied, the new value of R2 is less than or equal to

. Then the left-hand side of (IC2) does not change, and neither does the agent’s payoff. Furthermore, since (IC2) is satisfied, the new value of R2 is less than or equal to

![]()

since β1 ≥ 0, ![]() , and R1 ≤ x1.

, and R1 ≤ x1.

Third, if ![]() , then β1 = 1. Otherwise, we can raise β1 by ɛ and improve total surplus while also improving the agent’s payoff by

, then β1 = 1. Otherwise, we can raise β1 by ɛ and improve total surplus while also improving the agent’s payoff by ![]() (

(![]() is assumed to be sufficiently small so that

is assumed to be sufficiently small so that ![]() . We can transfer this payoff from the agent to the principal by raising R1 by

. We can transfer this payoff from the agent to the principal by raising R1 by ![]() . Since the value of the right-hand side of (IC2) does not change, the contract still satisfies all the constraints, and the principal is strictly better off.

. Since the value of the right-hand side of (IC2) does not change, the contract still satisfies all the constraints, and the principal is strictly better off.

Now, if β1 = β2 = 1, then to satisfy (IC2) the agent cannot be required to pay more than R2 = x1 after high output in period 1, so he gets the payoff of at least ![]() . Thus, this case is relevant only when

. Thus, this case is relevant only when ![]() . If so, the contract provided in part (b) satisfies all constraints and attains first-best; therefore it is optimal.

. If so, the contract provided in part (b) satisfies all constraints and attains first-best; therefore it is optimal.

Fourth, if ![]() then β1 < 1, R1 = x1, and we claim that (IC2) must bind. If not, let us increase β1 by ɛ and at the same time increase R2 by

then β1 < 1, R1 = x1, and we claim that (IC2) must bind. If not, let us increase β1 by ɛ and at the same time increase R2 by ![]() . Then the agent’s expected value remains unchanged and, because total surplus improves, the principal’s value improves. Furthermore, if ɛ is small then (IC2) is still satisfied. We conclude that

. Then the agent’s expected value remains unchanged and, because total surplus improves, the principal’s value improves. Furthermore, if ɛ is small then (IC2) is still satisfied. We conclude that ![]() .

.

Fifth, we can pin down the values of β1 and R2 assuming that the agent gets the expected payoff of exactly ![]() . If so, then using (IC2), the agent’s payoff is

. If so, then using (IC2), the agent’s payoff is

![]()

as in part (a) of the theorem. As W0 moves between ![]() and

and ![]() , β1 spans the entire feasible range of [0, 1].

, β1 spans the entire feasible range of [0, 1].

The principal’s profit

![]()

is a decreasing function of W0, and so it follows immediately that the agent’s expected payoff constraint must bind if ![]() .

.

If ![]() , then setting β1 = 0 satisfies the agent’s reservation payoff constraint, and so the optimal contract is given by part (c) of the theorem.

, then setting β1 = 0 satisfies the agent’s reservation payoff constraint, and so the optimal contract is given by part (c) of the theorem.

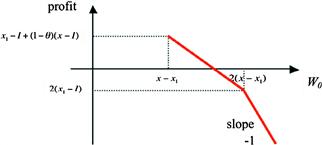

Figure 4 illustrates the principal’s profit as a function of W0. Note the special cases of ![]() and

and ![]() . In the former case, the agent obtains financing for the last period if he pays

. In the former case, the agent obtains financing for the last period if he pays ![]() in the first period. Thus, he is indifferent between paying only x1 in period 1 and paying

in the first period. Thus, he is indifferent between paying only x1 in period 1 and paying ![]() in exchange for a round that lets him receive an expected payoff of

in exchange for a round that lets him receive an expected payoff of ![]() and pay x1 in the last period. In the latter case, the agent pays x1 in both rounds, and receives funding for both rounds for sure. Note that on the interval

and pay x1 in the last period. In the latter case, the agent pays x1 in both rounds, and receives funding for both rounds for sure. Note that on the interval ![]() , the slope of the principal’s profit is flatter than −1 because

, the slope of the principal’s profit is flatter than −1 because ![]() . As W0 increases, so does the total surplus because inefficiency due to the agency problem becomes less severe. The inefficiency depends on the probability with which the project does not get funded in the second period. In Section 4, when we discuss the model of DeMarzo and Sannikov (2006), we will see how the slope of the principal’s value function changes in a dynamic setting.

. As W0 increases, so does the total surplus because inefficiency due to the agency problem becomes less severe. The inefficiency depends on the probability with which the project does not get funded in the second period. In Section 4, when we discuss the model of DeMarzo and Sannikov (2006), we will see how the slope of the principal’s value function changes in a dynamic setting.

Figure 4 The principal’s profit as a function of the agent’s payoff in the model of Bolton and Sharfstein (1990).

Remark 1

In this model, for all W0 the optimal contract is renegotiation-proof. If the cash flow is low in period 1 so that the contract prescribes project termination (in case R1 = x1 and β1 < 1), the principal and the agent cannot renegotiate to continue the project. Indeed, because the agent just paid out the entire cash flow to the principal, he has no cash left to contribute towards investment in period 2. Thus, the principal always finds it unprofitable to fund new investment.

However, in more complex dynamic models, the optimal contract can easily be not renegotiation-proof, as we will see in Section 4.

Remark 2

If ![]() , then the contract exhibits ex post inefficiency. Bad performance in period 1 may lead to a lack of financing in period 2, even though the profitability of the second period does not depend on performance in period 1.

, then the contract exhibits ex post inefficiency. Bad performance in period 1 may lead to a lack of financing in period 2, even though the profitability of the second period does not depend on performance in period 1.

Remark 3

The optimal contract can be implemented as follows. Initially the firm is funded with 2I − x1. The agent holds equity and the principal holds debt with promised repayments R2 − x1 and x1. In period 1, if the cash flow is high, available cash balance of x2 + I − x1 is sufficient to both make the debt payment and fund investment. If the cash flow is low, then cash balance I is insufficient to both pay debt and fund investment. The principal allows the agent to skip a payment with probability β1, and with probability 1 − β1 triggers default.

2.2 Adverse Selection

If a firm manager has private information about firm fundamentals, it may be difficult to sell informationally sensitive securities, especially equity, to raise funds for investment or share risk. Typically, insiders must retain some of firm’s cash flows in order to signal to the market the quality of the firm. Leland and Pyle (1977) provide a classic model in which firm insiders signal their private information about the quality of fundamentals by retaining shares of equity.

Myers and Majluf (1984) studies the effect of private information on investment decisions. It assumes that financing can be raised only in the form of equity, and that the management acts in the interest of old shareholders. It finds that “if managers have inside information there must be some cases in which that information is so favorable that management, if it acts in the interest of the old stockholders, will refuse to issue shares even if it means passing up a good investment opportunity” (p. 188).

The model is as follows. There is no discounting. At time 0 the management has an investment opportunity that requires investment I. The firm has financial slack S < I (cash + marketable securities) and must raise E = I − S by issuing new equity if it decides to go ahead. If the investment is not made at time 0, the investment opportunity evaporates.

The management knows the value y that the investment opportunity generates and the value x of assets in place. However, from the point of view of the market, these are random variables ![]() . With this information, the market requires the management to sell a fraction α of firm equity in order to raise E.

. With this information, the market requires the management to sell a fraction α of firm equity in order to raise E.

It is assumed that following a decision to issue, the old shareholders remain passive. That is, they “sit tight” if stock is issued; thus the issue goes to a different group of investors.

Definition

An equilibrium consists of a fraction α of equity that has to be issued to raise E, and the investment region M ⊆ [0, ∞) × [0, ∞) such that:

The following simple example illustrates equilibrium.

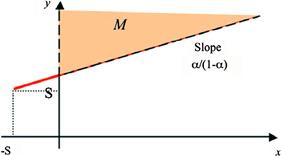

Example

There are two equally likely states of the world. In state 1, assets in place are worth x = 150, and an investment of I = 100 generates a cash flow of y = 120. In state 2, assets in place are worth x = 50, and an investment of I = 100 generates a cash flow of y = 110. The firm has no financial slack, i.e. S = 0.

In this example there is no equilibrium in which both types of firms invest. An investment by both types would require α = 100/215, since E[x + y] = 215 and E = 100. But then (1 − α) (150 + 120) = (115/215)270 = 144.42 < 150.

There is an equilibrium in which the firm invests only in state 2, by selling the fraction of equity α = 100/160. Since the investment has positive NPV, (1 − α) 160= 60 > 50. In this equilibrium, in state 1 the firm forgoes a positive-NPV project due to the asymmetric information problem.

In general, the investment region ![]() as illustrated in Figure 5.

as illustrated in Figure 5.

Figure 5 The set of parameters (x, y) for which the firm sells equity.

Assuming that the joint distribution of (x, y) over [0, ∞) × [0, ∞) is characterized by a strictly positive density, the equation

![]()

must have at least one solution. Indeed, note that the left-hand side is continuous in α, and it goes from 0 at α = 0 to infinity as α → 1 and the slope of the lower boundary of M gets steeper.

Theorem 3

In equilibrium firms with low asset value x may issue equity to finance a project with negative NPV, and firms with a high asset value may forgo a project with positive NPV.

Proof

First, we argue that in equilibrium α < E/I. Otherwise, if α ≥ E/I then x + y ≥ I in region M as illustrated in the left panel of Figure 6.

Figure 6 The Proof of Theorem 3.

If so, then

![]()

violating the equilibrium definition.

Since α < E/I, the low corner of M is at a point (0, y) with y < I, as illustrated in the right panel. Therefore, region M includes negative-NPV projects for firms with low asset value x. Also, since α > 0, some positive-NPV projects are not taken by firms with high x.

Of course, it is difficult to issue equity in the presence of informational asymmetries, because equity is very sensitive to private information. In the model of Myers and Majluf (1984), it is assumed that the firm cannot raise funds through other securities, such as debt or hybrid securities. We next discuss a model that investigates optimal security design under asymmetric information, using general securities.

DeMarzo and Duffie (1999) consider a setting in which an issuer owns assets with random cash flows, and wants to raise capital by issuing asset-backed securities. The issuer receives superior private information about the assets’ cash flows after security design stage but before sale. We saw in the overview of Myers and Majluf (1984) that it is difficult to sell equity in the presence of private information, because equity is quite information-sensitive. Here we will allow for general securities, and solve for optimal security design. The desire to issue is motivated by the assumption that the issuer is less patient than the market, e.g. because the issuer has superior investment opportunities. This is captured by assuming that the issuer discounts cash flows at the rate of δ < 1, while the market does not discount.

The model has one period, and the issuer’s assets generate a random cash flow of ![]() at the end of the period. A security is characterized by a non-decreasing function g : [0, ∞) →[0, ∞), which gives the payout to investors at the end of the period as a function of realized cash flow, x. Function g has to satisfy the feasibility constraint g(x) ≤ x. Formally the timeline is as follows:

at the end of the period. A security is characterized by a non-decreasing function g : [0, ∞) →[0, ∞), which gives the payout to investors at the end of the period as a function of realized cash flow, x. Function g has to satisfy the feasibility constraint g(x) ≤ x. Formally the timeline is as follows:

• the issuer designs a security g;

• the issuer learns private information z;

• the issuer chooses the quantity q ∈ [0, 1] of the security to sell;

• the market prices the securities sold at Pg(q) depending, on the quantity sold;

• cash flows are realized, investors are paid according to g, and the issuer receives the remaining cash flow.

The issuer’s expected payoff is given by

![]()

Note that the issuer does not discount the proceeds from the sale of the security, but discounts at rate δ the cash flows received upon the maturity of the assets.

The issuer would like to design a security to maximize her ex ante expected payoff. Formally, given a security g, the perfect Bayesian equilibrium consists of a map z → q such that (1) the issuer chooses q to maximize her expected payoff, (2) given q, the market forms its belief about the issuer’s type according to Bayes rule, and (3) given the belief, the market prices the security at its expected payoff.

The issuer’s optimization problem with respect to q in equilibrium is

![]()

where f = E[g(x)|z] is the expected payoff of the security. Since the issuer’s expected payoff depends on her type z only through f after the security g has been designed, it is convenient to think of f as the issuer’s type in the signaling equilibrium, in which the quantity q is chosen.

Assuming that in equilibrium, quantity sold q( f ) is a continuous function of the value of the security f, the schedule q( f ) can be characterized from the first-order condition

![]()

Using the fact that in equilibrium Pg(q) = f is the inverse of q( f ), so that ![]() , we have:

, we have:

![]()

The constant of integration is pinned down by the condition that the worst type f0 sells q = 1, and so:

From this expression, we see the trade-offs involved in optimal security design. Equity g(x) = x maximizes f0 since it sells all cash flows of the worst type to investors. However, equity is also very informationally sensitive. Therefore, as asset fundamentals z improve, f = E[g(x)|z] rises very fast, leading to very low payoffs for issuers with good fundamentals. It may be possible to raise the expected payoff of issuers with good fundamentals by designing a less informationally sensitive security, that is, making g(x) less sensitive to the cash flow x. However, that has a cost, as the value of f0 ends up lower. It follows that, in comparison with equity, less informationally sensitive securities give lower payoffs to issuers with low-quality assets, but may give significantly higher payoffs to issuers with high-quality assets. Below, we characterize conditions when equity is the optimal security, and when risky debt is.

Intuitively, it is optimal to sell equity if the seller’s private information is small.

Theorem 4

If![]() then g(x) = x is optimal.

then g(x) = x is optimal.

Proof

See Proposition 6 in DeMarzo and Duffie (1999).

If the seller’s private information is not that small, then debt turns out to be optimal under an additional condition.

Definition

Type z0 is called a uniform worst case if ![]() is increasing in x.

is increasing in x.

Theorem 5

If there is a uniform worst case then standard debt is optimal (among securities, for which g(x) is non-decreasing).

Proof

Consider an arbitrary security, characterized by a non-decreasing payoff function g(x). Let us compare it with debt D(x), whose face value is chosen so that

![]()

Then, let us show that for all z ≠ z0,

![]()

Then it follows immediately that the payoff for each type under standard debt is

its payoff under security g.

Since g(x) ≤ x is a security with a non-decreasing payoff, there exists a point x* such that g(x) ≤ D(x) for x ≤ x* and g(x) ≥ D(x) for x > x*, as illustrated in Figure 7.

Figure 7 The Proof of Theorem 5.

We have

![]()

since for all x, ![]() .

.

Intuitively, debt is optimal because if the issuer’s private info changes from z0 to z, then standard debt, in the class of monotone securities, is one that minimizes the increase in the issuer’s private valuation, and thus illiquidity costs.

3 Simple Securities in Dynamic Models

In this section, we explore simple securities in a fully dynamic model, before we consider optimal dynamic security design in the next section. In particular, we focus on the model of Leland (1994), which builds upon the dynamic models of Merton, 1974 and Black and Cox (1976) to explore the trade-offs between the tax advantages of debt and bankruptcy costs.

Merton (1974), Black and Cox (1976), and Leland (1994) investigate the model of a firm that pays no dividends and whose asset value, under the risk-neutral probability measure, follows the geometric Brownian motion:

![]() (1)

(1)

In Eqn (1), Zt is a standard Brownian motion under the risk-neutral measure and r is the risk-free rate. Below, we first describe the classic risky debt valuation model of Merton (1974), in which debt has fixed maturity, and then describe Leland (1994), which focuses on perpetual debt.

Importantly, using both of these models, we are also able to discuss the incentive properties of a particular capital structure. This discussion, which focuses on the sensitivities of the value of equity to the value and volatility of assets, serves as a precursor to the next section that considers optimal security design.

Merton (1974) considers a capital structure that consists of zero-coupon debt with promised payment D and fixed maturity T. The firm defaults at time T if VT < D. If the firm does not default, then equity holders pay off debt (e.g. by borrowing again). As a result, the payoff of equity holders is

![]()

Effectively, equity is a call option on firm assets with maturity T and strike D, and so its value is given by the Black–Scholes formula:

![]()

where ![]() , and N is normal CDF.

, and N is normal CDF.

This simple capital structure highlights incentive problems that typically arise when a firm raises outside financing. The Delta of an option measures the sensitivity of option value to the price of the underlying Vt. The Delta of equity with respect to assets, N(d1), is less than 1. This can lead to debt overhang. Equity holders will not take projects that cost them more than Delta per 1 added to firm value.

Option Vega measures the sensitivity of option value to volatility. Since the Vega > 0 for call options, there is asset substitution. Given the fixed-debt contract in place, equity holders would like to increase the risk of assets, and gradually will if they can.

Leland (1994) explores trade-offs between the tax advantages of debt and bankruptcy costs in a model with perpetual debt, in which the firm’s assets also follow (1). Debt with a continuous coupon rate of C is set at time 0. Due to tax effects, the effective cost of these coupon payments to equity holders is ![]() , where

, where ![]() is the tax rate and

is the tax rate and ![]() is the interest tax shield.3

is the interest tax shield.3

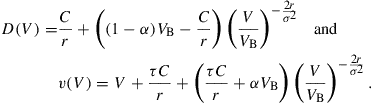

In the version of the model with an endogenous bankruptcy choice, equity holders decide at each moment of time whether to keep paying coupons or default and forfeit the assets to debt holders. Effectively equity holders have a perpetual American put option to sell the firm’s assets for ![]() . It is exercised only when the value of assets drops to the critical boundary VB, which we derive below.

. It is exercised only when the value of assets drops to the critical boundary VB, which we derive below.

The stationary nature of this setting implies that the prices of all securities are functions of V. Since the required rate of return under the risk-neutral measure is r, the value of any security F(V) must satisfy the equation

![]() (2)

(2)

where CF is the cash flow that the security pays and ![]() is the drift of F(V). The appropriate value of CF is C for debt, −(1 − τ)C for equity, and τC for the firm as a whole. Using (1) and Ito’s lemma,

is the drift of F(V). The appropriate value of CF is C for debt, −(1 − τ)C for equity, and τC for the firm as a whole. Using (1) and Ito’s lemma, ![]() , and so the security-pricing Eqn (2) becomes

, and so the security-pricing Eqn (2) becomes

![]()

For any value of CF, this equation has a general solution of the form

![]()

Matching the boundary conditions at the bankruptcy boundary VB and infinity, equity has value

![]()

To find the value of the firm’s debt D(V), as well as the value of the whole firm v(V) = E(V) + D(V), assume that in bankruptcy a fraction α of firm assets VB is lost due to bankruptcy costs. Then

The boundary VB, at which equity holders exercise their option to abandon the assets in the endogenous bankruptcy case, can be determined by the smooth-pasting condition

![]()

This leads to

![]() (3)

(3)

Given C and τ, the point at which equity holders default is independent of the initial value of the assets V0 or bankruptcy costs α. VB is proportional to the debt burden (1 − τ)C, and VB decreases as asset volatility goes up.

Equity holders choose the boundary VB to maximize their payoff, without taking into account the payoff of debt holders. This leads to a conflict of interest. When determining the optimal capital structure in endogenous bankruptcy case ex ante, market participants recognize that ex post equity holders default at the boundary given by (3). Maximizing the value of the firm

with respect to C, we find that

Naturally, the optimal coupon rate is proportional to V0.

As in the Merton model, equity Delta with respect to assets in this model is less than 1. Delta decreases to 0 as V drops towards VB. This phenomenon can cause severe agency problems to arise when equity holders are under water in a richer model where equity holders can take costly actions that may improve the value of the firm. For example, if equity holders were also controlling investment, they would refuse positive-NPV projects when V gets close to VB.

Under alternative conditions determining bankruptcy, such as in the presence of protective debt covenants, agency problems can be less severe near bankruptcy. Equity Delta with respect to asset value could be large near bankruptcy if bankruptcy is forced by the contract, rather than determined by the equity holders’ decision to walk away from the assets. The optimal design of the security held by the “agent”—the firm’s insiders—is the subject of the next section. Section 4 presents several explicit models that capture how the agent’s actions can affect the firm’s value in a dynamic setting.

4 Optimal Dynamic Security Design under Moral Hazard

The foundation of optimal security design under dynamic moral hazard lies in dynamic agency theories, which have been studied by Radner (1985), Rogerson (1985), Green (1987), Spear and Srivastava (1987), Abreu, Pearce, and Stacchetti (1990), and Phelan and Townsend (1991). In corporate finance, discrete-time models of dynamic financing under moral hazard include the work of Albuquerque and Hopenhayn (2004), Clementi and Hopenhayn (2006) and DeMarzo and Fishman (2007a, 2007b). Continuous-time principal-agent models (see Sannikov, 2008), offer particularly tractable methods that have been adopted in corporate finance. Biais et al. (2007) is an important paper that illustrates the relationship between continuous-time and discrete-time methods.

We begin this section by reviewing the work of DeMarzo and Sannikov (2006), which characterizes optimal security design under dynamic moral hazard using continuous-time methods, and that of DeMarzo et al. (2011), which investigates the relationship between agency problems and investment dynamics. After that, we briefly review a number of other models that adopt the dynamic agency framework to study a broader set of issues.

DeMarzo and Sannikov (2006) (hereafter DS) model the same type of moral hazard as the two-period model of Bolton and Scharfstein (1990) which we have already reviewed, in infinite horizon.

The agent has a profitable investment opportunity that, if funded with an initial investment of I > 0, would generate a cash flow stream of the form

![]()

where Zt is a standard Brownian motion. The agent would like to write a contract with the principal (an investor) to fund this project and use it as a collateral to fund the agent’s consumption. The agent would like to borrow money against this project because he has a higher discount rate γ than the market rate r, and also because he may not have sufficient funds to finance the up-front investment.

However, an agency problem exists because the agent privately observes the true cash flows Yt. Thus, the agent may divert some of the cash flows for personal consumption or as perks. The principal only learns about cash flows that are left ![]() after the agent’s diversion action, possibly through the agent’s report. Assume that the cumulative amount of cash diverted

after the agent’s diversion action, possibly through the agent’s report. Assume that the cumulative amount of cash diverted

![]()

must be a continuous non-decreasing process (i.e. the agent cannot send the principal a higher cash flow than realized). It is inefficient to divert cash, so that the agent is able to enjoy only a fraction λ ∈ (0, 1] of diverted cash. In order to solve the agency problem, the contract between the principal and the agent may force a termination of the project in the event that the observed cash flows ![]() are insufficient. In the event of termination, the principal receives the project’s assets, which he values at L, and the agent pursues his outside option with value R. Termination is inefficient, i.e.

are insufficient. In the event of termination, the principal receives the project’s assets, which he values at L, and the agent pursues his outside option with value R. Termination is inefficient, i.e.

![]()

DS derive the optimal contract between the agent and the principal in this setting, which maximizes the principal’s profit subject to a set of constraints, including the incentive constraints. There are no restrictions regarding the form of contracts allowed. That is, contracts can specify in the most general way how the termination time τ and the agent’s compensation dCt depend on the history of observed cash flows ![]() .

.

Because the marginal benefit to the agent from diverting cash is a constant λ, and because the agent can divert cash at an unbounded rate, the optimal contract should not allow any cash flow diversion. Intuitively, it is cheaper to allow the agent to consume some of the project’s cash flows directly, rather than through cash flow diversion behind the principal’s back.

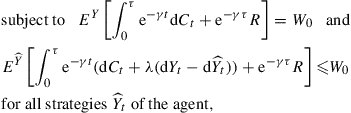

Formally, the optimal contract solves the following constrained optimization problem:

![]() (4)

(4)

where superscripts Y and ![]() over the expectation highlight that the agent’s compensation dCt, as well as the termination time τ, depend on the agent’s reports. Parameter W0 in the first constraint is the agent’s expected payoff, which is determined by the relative bargaining powers of the principal and agent. Problem (4) is feasible whenever W0 ≥ R.

over the expectation highlight that the agent’s compensation dCt, as well as the termination time τ, depend on the agent’s reports. Parameter W0 in the first constraint is the agent’s expected payoff, which is determined by the relative bargaining powers of the principal and agent. Problem (4) is feasible whenever W0 ≥ R.

The second set of constraints restricts contracts to those in which the agent prefers to abstain from cash flow diversion. This set of contracts can be characterized via a simple condition on the sensitivity of the agent’s continuation payoff to observed cash flows ![]() . For a given contract {τ, C}, the agent’s continuation payoff when he refrains from cash flow diversion is given by

. For a given contract {τ, C}, the agent’s continuation payoff when he refrains from cash flow diversion is given by

![]()

Theorem 6

For any contract {τ, C} there exists a process βt such that

![]() (5)

(5)

and it is optimal for the agent to refrain from cash flow diversion if and only if βt ≥ λ for all t ≤ τ. Also conversely, if a process Wt ≤ R follows(5)until time τ, at which Wτ = R, and satisfies the transversality condition E[1t≤τ e−γt Wt] → 0 as t → ∞, then Wt is the agent’s continuation payoff.

Proof

See DS.

The representation (5) can be derived using the Martingale Representation Theorem, by focusing on the martingale:

![]()

The terms ![]() in the law of motion of Wt are due to simple accounting for the agent’s discount rate, and payoff received by the agent through consumption.

in the law of motion of Wt are due to simple accounting for the agent’s discount rate, and payoff received by the agent through consumption.

The incentive condition is βt ≥ λ because the agent refrains from cash flow diversion if he receives at least λ in the present value of his future payoff for each dollar of cash flow reported to the principal.

Due to Theorem 6, the principal’s problem (4) can be reduced to a stochastic control problem.

Corollary

There is a one-to-one correspondence between contracts {τ, C} that satisfy the constraints of problem(4)and controlled processes

![]()

that satisfy the transversality condition under controls (Ct, βt ≥λ), with τ defined as the first time when Wt hits R.

The control problem is to maximize the principal’s objective (4) by a choice of controls (Ct, βt ≥ λ) that drive the state Wt according to (5), subject to the constraint that time τ occurs when Wt hits R for the first time as well as the transversality condition. To solve the control problem, we can follow an intuitive line of reasoning to conjecture a solution, and then verify that the solution is optimal.

Intuitively, contracting in this setting involves inefficiencies because the agent needs incentives to report cash flows truthfully. The principal provides these incentives by tying the agent’s continuation payoff to performance through the sensitivity coefficient βt ≥ λ. This introduces volatility in the agent’s payoff. A bad history of cash flows drives Wt down to R, and necessitates inefficient termination. Due to this intuition, the choice βt = λ, which minimizes the volatility of Wt while still satisfying the incentive constraints, is optimal.

The choice of the agent’s compensation also involves an interesting trade-off. Because the agent’s discount rate γ is higher than r, it is expensive for the principal to postpone payments to the agent. However, according to (5), early payments to the agent reduce the agent’s continuation payoff Wt and increase the chance that Wt hits R due to a cash flow drawdown. This concern is particularly pressing when Wt is low, so that the chance of termination is significant. Therefore, we conjecture that there is a critical level of ![]() such that it is optimal to pay nothing to the agent when

such that it is optimal to pay nothing to the agent when ![]() , and pay immediately any accumulated continuation payoff in excess of

, and pay immediately any accumulated continuation payoff in excess of ![]() .

.

To summarize, we conjecture a contract of the following form:

In the optimal contract, the agent’s continuation payoff evolves according to

![]()

on the interval ![]() . The agent is paid only when

. The agent is paid only when ![]() , i.e. dCt = 0 if

, i.e. dCt = 0 if ![]() , and otherwise payments dCt are chosen so that Wt is a reflecting process that never exceeds

, and otherwise payments dCt are chosen so that Wt is a reflecting process that never exceeds ![]() . If

. If ![]() , then at time 0 the agent receives a lump-sum payment of

, then at time 0 the agent receives a lump-sum payment of ![]() . Termination occurs when Wt hits the boundary R for the first time.

. Termination occurs when Wt hits the boundary R for the first time.

We still need to determine the optimal level of ![]() . We can do that by valuing the security that the principal is holding under this contract, and then finding

. We can do that by valuing the security that the principal is holding under this contract, and then finding ![]() that maximizes the value of that security. The value of this security is a function of current Wt. As in Leland (1994), we can value the principal’s security through equation

that maximizes the value of that security. The value of this security is a function of current Wt. As in Leland (1994), we can value the principal’s security through equation

![]()

where CF is the cash flow that the security pays and ![]() is the drift of F(W). On

is the drift of F(W). On ![]() , dCt = 0 and so the principal’s expected cash flow is μ. Thus, using Ito’s lemma, F(W) must satisfy

, dCt = 0 and so the principal’s expected cash flow is μ. Thus, using Ito’s lemma, F(W) must satisfy

(6)

(6)

for all ![]() . This second-order ordinary differentialequation requires two boundary conditions to solve. First, F(R) = L, because the value of the assets to the principal is L when termination occurs. Second,

. This second-order ordinary differentialequation requires two boundary conditions to solve. First, F(R) = L, because the value of the assets to the principal is L when termination occurs. Second, ![]() , because at the point where the agent gets paid it costs the principal one dollar to give the agent an extra dollar of utility. For any choice of

, because at the point where the agent gets paid it costs the principal one dollar to give the agent an extra dollar of utility. For any choice of ![]() , the corresponding solution gives the principal’s value of the contract, in which payments to the agent are made at point

, the corresponding solution gives the principal’s value of the contract, in which payments to the agent are made at point ![]() .

.

So, what is the optimal choice of ![]() ? To answer this question, in Figure 8 we illustrate the phase diagram of solutions to Eqn (6) starting with boundary condition F(R) = L, for different levels of F’(R). For any W ≥ R, it can be shown that F’(W) is increasing in F’(R).4

? To answer this question, in Figure 8 we illustrate the phase diagram of solutions to Eqn (6) starting with boundary condition F(R) = L, for different levels of F’(R). For any W ≥ R, it can be shown that F’(W) is increasing in F’(R).4

Figure 8 Functions F(W), such that F(R) = L, which solve Eqn (6) with different boundary conditions F’(R).

In this diagram, ![]() maximizes the principal’s profit. This choice corresponds to the top solution, which has a single inflection point

maximizes the principal’s profit. This choice corresponds to the top solution, which has a single inflection point ![]() where

where ![]() . That solution is concave on the interval

. That solution is concave on the interval ![]() , and then it becomes convex. For any other value of

, and then it becomes convex. For any other value of ![]() , the principal’s security has lower value. The bottom solution corresponds to two different choices of

, the principal’s security has lower value. The bottom solution corresponds to two different choices of ![]() , and

, and ![]() . The slope at the inflection point, which is between

. The slope at the inflection point, which is between ![]() and

and ![]() , is steeper than −1. The bottom solution does not correspond to the optimal contract because, by continuity of solutions to differential equations in initial conditions, a solution with a slightly higher slope F’(R) still reaches slope −1 at some point

, is steeper than −1. The bottom solution does not correspond to the optimal contract because, by continuity of solutions to differential equations in initial conditions, a solution with a slightly higher slope F’(R) still reaches slope −1 at some point ![]() , and it is therefore superior (i.e. it is higher than the bottom solution at every point W, and it represents the principal’s value function under the contract, in which the agent is paid at point

, and it is therefore superior (i.e. it is higher than the bottom solution at every point W, and it represents the principal’s value function under the contract, in which the agent is paid at point ![]() ).5

).5

Note also that since ![]() and solution F has an inflection point at

and solution F has an inflection point at ![]() , i.e.

, i.e. ![]() , Eqn (6) implies that

, Eqn (6) implies that

![]()

This equation, which corresponds to the dashed line in Figure 8, can be taken as a condition that determines the optimal level of ![]() . It can be interpreted as follows: it makes sense to postpone payments to the agent to reduce the likelihood of termination, but only up to the point where the expected cash flows exhaust the required returns of the principal and the agent.

. It can be interpreted as follows: it makes sense to postpone payments to the agent to reduce the likelihood of termination, but only up to the point where the expected cash flows exhaust the required returns of the principal and the agent.

We can verify that this contract, which we guessed using intuitive reasoning, is indeed optimal using an argument that we sketch below:

A sketch of the verification argument. Let function F, together with the point ![]() , be determined on

, be determined on ![]() by Eqn (6) and boundary conditions F(R) = L,

by Eqn (6) and boundary conditions F(R) = L, ![]() and

and ![]() . Let us extend F beyond

. Let us extend F beyond ![]() linearly with slope −1. We will show that there is no contract with value higher than F(W0) to the principal.

linearly with slope −1. We will show that there is no contract with value higher than F(W0) to the principal.

For an arbitrary contract {C, τ}, in which the agent’s continuation value follows:

![]()

consider the process ![]() .

.

We claim that Gt is a super-martingale. Differentiating Gt with respect to t, we get

Using the fact that F"(Wt) ≤ 0, and F’(Wt) ≥ −1, we see that Gt is a super-martingale by focusing on its drift.

Therefore, the principal’s profit from this contract is:

![]()

We finish discussing DS by outlining one particular capital structure that implements the optimal contract, and mentioning a few comparative statics results.

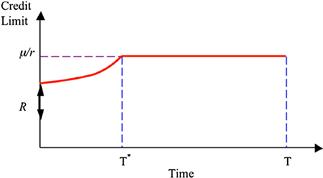

The optimal contract can be implemented in many ways, but one particularly attractive implementation involves a credit line. To construct the implementation, we map Wt into the outstanding balance Mt on a credit line, so that point ![]() corresponds to balance Mt = 0, and point R corresponds to the credit limit

corresponds to balance Mt = 0, and point R corresponds to the credit limit ![]() . Then

. Then ![]() evolves according to

evolves according to

![]()

This leads to a capital structure consisting of a credit line, perpetual debt and equity. The agent holds a fraction λ of equity. The principal holds perpetual debt, which receives a flow of payments of ![]() , and the credit line, which receives the project cash flows net of the perpetual debt payments and dividends, and the fraction 1 − λ of equity.6 Total dividends on equity are

, and the credit line, which receives the project cash flows net of the perpetual debt payments and dividends, and the fraction 1 − λ of equity.6 Total dividends on equity are ![]() , and they are paid only when Mt = 0, i.e. the credit line is fully paid off. The interest rate on the credit line equals to the agent’s discount rate γ. The contract triggers termination when the credit line is drawn to the limit.

, and they are paid only when Mt = 0, i.e. the credit line is fully paid off. The interest rate on the credit line equals to the agent’s discount rate γ. The contract triggers termination when the credit line is drawn to the limit.

Note that the cash flows on the securities held by the principal (perpetual debt, credit line, and equity) are the same as in the optimal contract based on Wt. Indeed, when ![]() then the principal receives just the reported cash flows

then the principal receives just the reported cash flows ![]() . Perpetual debt pays a flow of

. Perpetual debt pays a flow of ![]() , and the credit line receives the payments of

, and the credit line receives the payments of ![]() net of the coupon payments on perpetual debt

net of the coupon payments on perpetual debt ![]() . The interest rate charged on the credit line increases its balance, but does not generate an actual cash flow. At point

. The interest rate charged on the credit line increases its balance, but does not generate an actual cash flow. At point ![]() , the agent receives dCt in each contract, and the principal receives the rest,

, the agent receives dCt in each contract, and the principal receives the rest, ![]() .

.

DS verify that under this implementation, the agent has incentives to refrain from cash flow diversion, and instead chooses to use firm cash flows to pay down the credit line, and pay dividends only when the credit line is fully paid off.

The continuous-time formulation makes analytic comparative statics possible in this dynamic contracting setting. For example, the optimal mix of credit line and debt depends on the volatility of cash flows σ and the agent’s discount rate γ.The implementation uses a longer credit line when σ is larger or γ is smaller. See DS for details, and other comparative statics results.

Besides creating a convenient methodology that is applicable to study a range of issues, the model of DS has a number of important economic implications. The optimal contract clearly divides the risks between the agent, the firm insider, and outside investors. The model does not have specific predictions regarding the division of cash flows among outside investors: the Modigliani–Miller theorem holds with respect to those cash flows. The implementation of the optimal contract in the form of a credit line suggests one way to divide these cash flows between outside equity holders and debt holders. Certainly, the implementation is not unique, e.g. Biais et al. (2007) provide an alternative implementation that maps the agent’s continuation payoff Wt into the firm’s cash balance. In any case, it is convenient to link Wt to some measure of the firm’s financial slack.

In this interpretation, the model has a number of important predictions. Past performance is positively related to the firm’s payouts, and the firm’s financial slack. Following poor performance, firms stop paying dividends and may be liquidated inefficiently, even when past performance is uncorrelated with future profitability. The firm’s manager should be exposed to the risk of the firm—he should be compensated with a non-tradable stake of the firm’s equity.

Remark

DS also present a variation of the model, in which the agency problem involves costly effort input rather than cash flow diversion. Specifically, they assume that the principal observes cash flows

![]()

The agent gets a private benefit of B = λA if he shirks.

They show that the optimal contract is the same as in the baseline model (with cash flow diversion), and it gives the agent incentives to work until the termination time τ, if and only if the following condition is satisfied:

![]() (7)

(7)

Zhu (2011) solves for the optimal contract with shirking in this variation of the DS model, when condition (7) is violated. We summarize the findings of Zhu (2011) in Section 4.1.

DeMarzo et al. (2011) (hereafter DFHW) investigate how dynamic agency problems affect the scale of the firm. They use the agency model of DS, and add investment decisions that are observable and contractible.

The firm’s capital stock evolves according to

![]()

where ιt is the cost of investment per unit of capital, and function Φ satisfies Φ(0) = 0, Φ’ > 0 and Φ” ≤ 0. In the absence of investment, capital simply depreciates at rate δ. The concavity of function Φ reflects adjustment costs.7

After accounting for investment and adjustment costs, the firm’s cumulative cash flow process takes the form

![]()

The agent’s action at ≤ 1 reduces the mean of cash flows. Setting at < 1 is inefficient, but it gives the agent a private benefit flow of λ(1 − at)Kt. In the event of termination, which may be required to solve the agency problem, the agent receives the payoff of R = 0, and the principal receives value ![]() from the project’s assets, where

from the project’s assets, where ![]() because the firm can always liquidate by disinvesting. The agent’s discount rate γ is higher than the principal’s discount rate r.

because the firm can always liquidate by disinvesting. The agent’s discount rate γ is higher than the principal’s discount rate r.

The range of possible contracts specify how the cash flows that the agent is allowed to keep Ct, the termination time τ, and the rate of investment ιt depend on the entire history of firm performance {Ys, s ∈ [0, t]}. For the same reasons as in DS, we know that the optimal contract has to create incentives for the agent to always choose at = 1. Formally, the optimal contracting problem is:

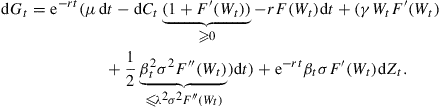

In this setting, for an arbitrary contract (τ, C, ι), the law of motion of the agent’s continuation payoff when he follows the strategy {at = 1} is

![]()

The incentive constraint is βt ≥ λ.

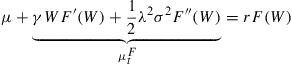

The principal’s value function F(Wt, Kt) under the optimal policy depends on both Wt and Kt. It must satisfy the Bellman equation

![]()

Due to the scale-invariance properties of the model, DFHW conjecture that the value function has the form F(W, K) = f(w)K, where w = W/K. Then wt = Wt/Kt follows:

![]()

and the Bellman equation reduces to

![]()

The solution to this equation can be found using similar logic as we used in the discussion of DS.

Theorem 7

The principal’s value function is of the form F(W, K) = Kf(W/K). Function f is concave, and satisfies the equation

![]() (8)

(8)

on the interval![]() determined by the boundary conditions

determined by the boundary conditions

![]()

In the optimal contract, the agent’s compensation, investment and termination time τ are determined by two state variables: Kt and Wt. The law of motion of Wt is determined contractually by

![]()

where payments dCt are set to 0 for![]() and chosen to reflect Wt at the boundary

and chosen to reflect Wt at the boundary![]()

![]()

. The investment rate ιt maximizesand τ is the time when Wt hits 0 for the first time.

Proof

See DFHW.

How does the investment rate under the optimal contract depend on w, and how does it compare to the first-best investment rate? Because f is a concave function, ![]() is increasing in w, and so ι increases with w (see Figure 9 for a geometric interpretation).

is increasing in w, and so ι increases with w (see Figure 9 for a geometric interpretation).

Figure 9 Since f(w) is a concave function, f(w) − wf’(w) increases in w.

Moreover, the first-best investment rate and the corresponding value of capital can be found from

![]()

At the same time, from Eqn (8) and the boundary conditions at ![]() ,

,

It follows that at ![]() , the optimal rate of investment is less than first-best, and the value of the firm per unit of capital (measured as the sum of the principal’s and agent’s payoffs) is also less than qFB.

, the optimal rate of investment is less than first-best, and the value of the firm per unit of capital (measured as the sum of the principal’s and agent’s payoffs) is also less than qFB.

Both the average Tobin’s q of the firm’s assets

![]()

and the marginal q

![]()

are increasing in w. Moreover, because f’(w) ≥ −1, it follows that

![]()

Empirically, the average q (which is easy to measure) is often used empirically as a proxy for the marginal q, following the results of Hayashi (1982). However, even though the model of DFHW exhibits the same homogeneity properties as Hayashi (1982), here the marginal and average q are not the same, due to agency costs. The difference between average and marginal q’s depend on w, and thus the history of firm performance.

The model has the following predictions about the relationship between investment, Tobin’s q, and the firm’s financial slack w:

• Financial slack is positively related to past performance.

• Average and marginal q, as well as investment, are increasing with financial slack.

• The agent’s cash compensation increases with financial slack.

• The maximal level of financial slack is higher for firms with more volatile cash flows and lower liquidation values.

In general, the model predicts that investment is positively correlated with profits, past investment, financial slack, and managerial compensation, even with time-invariant investment opportunities.

DS as well as DFHW serve as a microfoundation of financing frictions that exist in the presence of agency problems. Many papers assume a set of financial frictions, instead of deriving them, and instead devote attention to the implications of these frictions on the issues of investment and financing policies as well as risk management. For example Rampini and Vishwanathan (2010, 2012) assume financing frictions in the form of collateral constraints in a partial equilibrium setting. Brunnermeier and Sannikov (2011) and He and Krishnamurthy (2012) assume constraints with respect to equity issuance, together with restrictions on hedging of certain aggregate risks, to study the implications of frictions on the issues financial stability in general equilibrium settings.

The models of Bolton, Chen, and Wang (2011, 2012) (hereafter BCW) are particularly close to DFHW in how they model the firm’s production technology, but they assume financial frictions directly instead of explicitly modeling an agency problem. Specifically, BCW assume that the firm’s production and investment technology is governed by equations

![]()

These equations are identical to those of DFHW, assuming that the managerial compensation contract in place enforces full effort, at = 1. Instead of modeling the agent’s incentives explicitly, BCW assume financial frictions that are related to the features of the optimal contract that motivate effort. Specifically, they assume that the firm maintains a cash balance (recall the implementations of the optimal contract in DS and Biais et al. (2007)) and that it is costly to issue new equity when the firm runs out of cash. In DS, new equity is issued only when the old manager is fired and replaced with a new manager. In addition, BCW assume that it is costly to keep cash inside the firm instead of paying it out to shareholders, just as in DS it is costly to postpone payments to the agent as the agent is less patient than the principal. Under the optimal policy in BCW, the firm’s financial slack is sensitive to the firm’s cash flows, and evolves between endpoints where dividend payouts are made after good performance and new equity is issued under poor performance. Thus, BCW present a simple dynamic model that captures many of the features of the optimal contract of DS and DFHW without delving into the details of an agency problem explicitly.

4.1 Other Models that Involve Dynamic Moral Hazard

A number of papers adapt a continuous-time dynamic agency framework to study the interaction between agency problems and various other issues. We briefly review several of them here. We focus, for the most part, on the technical elements of these models.

Piskorski and Tchistyi (2010), who consider the problem of optimal mortgage design, have a number of important contributions. First, they adapt a model similar to that of DS to the study of mortgages. Second, they investigate what happens in the optimal contract when market conditions exogenously change. They focus specifically on changes of market interest rates and find that it is optimal to tighten the agent’s access to credit when interest rates rise.

The market interest rate in the model of Piskorski and Tchistyi (2010) is a Poisson switching process with two levels {rL, rH}, and the switching intensity from interest rate ri to rj, j ≠ i, given by δ(ri). The cash flow process

![]()

is interpreted as the borrower’s income, which is unobservable. It is assumed that the borrower can hide income without any cost, so parameter λ in DS is set to 1.

In any incentive-compatible contract the agent’s continuation value follows:

![]()

where ![]() is the agent’s continuation value conditional on the event that the interest rate switches at time t, and the incentive constraint is βt ≥ 1.

is the agent’s continuation value conditional on the event that the interest rate switches at time t, and the incentive constraint is βt ≥ 1.

The principal’s value function Fi(Wt) depends on two state variables—the agent’s continuation value Wt and the current interest rate rt = ri. It is characterized by the system of two equations:

for i = L, H and j ≠ i, with the familiar boundary conditions

![]()

Under the optimal contract, the agent’s continuation value jumps from Wt to ![]() whenever the interest rate switches. A key equation that determines the jump in the agent’s continuation value, when the interest rate jumps from rt− = ri to rt = rj at time t, is the first-order condition

whenever the interest rate switches. A key equation that determines the jump in the agent’s continuation value, when the interest rate jumps from rt− = ri to rt = rj at time t, is the first-order condition

![]() (9)

(9)

We would like to emphasize that condition (9) arises very commonly in models where a state switches via a Poisson process.

Piskorski and Tchistyi (2010) offer several implementations of the optimal contract. In particular, the variable Wt can be mapped into the balance on the homeowner’s home equity line of credit. The changes in the value of Wt in response to interest rate shifts can be linked to some properties of adjustable-rate mortgages. In particular, it is a feature of the optimal contract that the agent’s default probability rises when the interest rates increase.

Hoffmann and Pfeil (2010) consider a dynamic agency model, in which firm profitability experiences observable shocks. Their model builds upon DS, except that they allow for Poisson shocks that change the expected rate of cash flows μ. One of the key messages of Hoffmann and Pfeil (2010) is that, despite conventional intuition, the optimal contract rewards the agent for luck when it is correlated with the firm’s future profitability.

Here we review a variation of their model. Assume that the expected rate of cash flows is a Poisson switching process with values {μL, μH}, so that

![]()

The switching intensity from state μi to μj, j ≠ i, is given by δ(μi).8 The agency problem is the same as in DS: the agent can divert cash flows, and he receives benefit equal to a fraction λ ∈ (0, 1] of the diverted cash flows.

The optimal contract depends on μt and the agent’s continuation value Wt, which follows:

![]()

The principal’s value function solves the system of two equations

for i = L, H and j ≠ i, with the familiar boundary conditions

![]()