Handbook of Asset and Liability Management, Vol. 2, No. suppl (C) • 2007

ISSN: 1872-0978

doi: 10.1016/S1872-0978(06)02016-3

Chapter 16 Integrated Risk Control Using Stochastic Programming ALM Models for Money Management

Abstract

A multistage stochastic programming modeling based approach is developed for asset and liability management for fund managers. Managing a fund of investments in a large pool of possible instruments, such as stocks, requires sophisticated analytical capability both in terms of selecting the pool and also in maintaining the performance of the fund within acceptable levels. Given the uncertainty of the future performance of the underlying stocks, the portfolio must be managed or rebalanced temporally as the market and economic conditions change. Such portfolio rebalancing at various points in time allows the fund manager to manage the riskiness of the fund from both the fund managers and the individual clients viewpoints. In doing so, a fund manager must resort to more-advanced analytical risk-control techniques. I apply a multi-prong risk metric system that is designed for the portfolio to achieve desired performance characteristics. The model incorporates important issues such as market impact costs in trading, fund drawdown, market neutrality, and catastrophic risk, within an integrative framework, modeled via stochastic programming. The model is applied to stock fund management involving a large number of securities and its performance is demonstrated with various strategies for portfolio rebalancing. The integrated dynamic multistage stochastic programming model easily outperforms the standard static mean-variance approach (i.e., the Markowitz model) for portfolio management. Sharpe ratios, percent worst draw downs, recovery periods from drawdown, portfolio rate of returns, etc. are used for performance comparisons.

Keywords

• portfolio optimization • stochastic multistage programming • risk management • integrated risk control • money management

JEL classification

• D81 • G11 • C61

1 Introduction

There is a tremendous growth in the number of individuals who are engaged in money management in the twenty-first century, yet only a few implement disciplined, professional money management strategies. During the stock market bubble of the late 1990s, limiting risk was an afterthought, but given the recent stock market action, more managers are considering more sophisticated approaches to portfolio risk management. Typically, only a few have the ability to view their portfolios from a risk/return integrated perspective. Instead, many individuals take a defensive or reactive view of risk in which risk is measured to avoid losses. What is essential for successful money management is to have an offensive or proactive posture in which risks are actively managed. This paper proposes such an integrated framework for fund management using multistage stochastic programming modeling.

Managing a fund of investments in a large pool of possible instruments (i.e., stocks) requires sophisticated analytical capability both in terms of selecting the pool and also in maintaining the performance of the fund within acceptable levels. Given the uncertainty of the future performance of the underlying stocks, it is imperative that the portfolio of stocks (in the fund) be managed or rebalanced temporally as the market and economic conditions change. Such portfolio rebalancing at various points in time allows the fund manager to control the riskiness of the fund from both the fund managers and the individual clients viewpoints. In doing so, a fund manager must attempt to remove the guesswork based on emotions (or gutt feeling) from the decision making and resort to the more-advanced analytical risk-management techniques.

Reading material on money management is quite abundant—a search on Amazon.com on the Internet returns more than 2100 books. Various professional money management services are also available that offer diverse asset allocation strategies based on common risk and time horizon parameters. These allocations are typically optimized using a static mean-variance framework, following the early work on portfolio optimization by Markowitz (1952, 1987), where a static, deterministic model for trading off portfolio expected return with portfolio variance was proposed. See the chapter by Markowitz and Van Dijk in this volume for a current survey of this approach. Variants of this approach that utilize a mean absolute deviation (MAD) functional, rather than portfolio variance, have been proposed, see, e.g., Konno and Yamazaki (1991) and Konno and Kobayashi (1997).

Asset allocation is the practice of dividing resources among different categories such as stocks, bonds, mutual funds, investment partnerships, real estate, cash equivalents, and private equity. Such models are expected to lessen risk exposure since each asset class has a different correlation to the others; when stocks rise, for example, bonds often fall. At a time when the stock market begins to fall, real estate may begin generating above average returns. Consequently, various allocation styles may be specified for the purposes of, say, preservation of capital, generating income, long-term aggressive growth, or striking a balance between income and growth. However, merely diversifying assets to the prescribed allocation model is not going to alleviate the manager from the need to choose individual issues. Indeed, the asset allocation and the choice of individual securities must occur integratively, consistent with the intended risk specification. A further complication in this case is the need for temporal rebalancing in an effort to bring the portfolio back into balance with the original prescription, or a variation thereof consistent with market evolution and changes in risk preferences.

However, static (myopic) models of portfolio optimization fail to capture two important aspects of portfolio rebalancing: (1) trade-off between short-term and long-term consequences of investment strategy, based on the evolution of stochastic factors, and (2) presence of transactions or market impact costs, taxes, etc. that affect portfolio holdings over time, see Ziemba and Mulvey (1998).

In contrast, a sequential decision theoretic optimization framework for portfolio rebalancing is available via multistage stochastic programming (MSP) modeling. This approach allows modeling various future time periods of portfolio revisions explicitly where stochastic dynamic evolution of random parameters (e.g., security returns) can be incorporated via a so-called scenario tree. Each scenario is a timed-sequence of events through the end of the planning horizon with an associated probability of occurrence. Multistage stochastic programming models have been richly applied in a variety of financial applications; see Kusy and Ziemba (1986) for a bank asset/liability management, Cariño and Ziemba (1998) for an asset/liability management problem of a Japanese insurance company, Mulvey and Vladimirou (1992) for a multiperiod stochastic network model for the purpose of asset allocation, and Golub et al. (1997) for fixed income securities management. For applications of stochastic multistage linear programming with a binomial scenario tree of price uncertainty for financial option pricing, see Edirisinghe, Naik and Uppal (1993), and the extensions in Edirisinghe (2004). This article provides a multistage stochastic programming model that incorporates sequential rebalancing of the portfolio in order to maintain the portfolio performance with respect to a multi-prong risk measurement scheme.

Stochastic programming models have found many applications within asset and liability management (ALM) problems, which are generally of a long term nature. ALM attempts to find the optimal investment strategy under uncertainty in both the asset and liability streams. Simultaneous consideration of assets and liabilities can be very advantageous in terms of increasing returns and reducing risk, especially when they have common risk factors leading to high correlations. ALM-MSP models allow for dynamic portfolio rebalancing while satisfying operational or regulatory restrictions and policy requirements, see, e.g., Holmer and Zenios (1995). Early work on application of stochastic programming for financial planning is by Bradley and Crane (1972) and Ziemba and Vickson (1975). Since 1990, there is an increased momentum in such applications, driven partly by the globalization and innovations in the financial markets, but largely due to tremendous improvement in the solution algorithms and computing hardware advances. See Zenios (1995) and Nielsen and Zenios (1996) for fixed income portfolio management; Cariño et al. (1994), Consigli and Dempster (1998), Høyland (1998), and Mulvey, Gould and Morgan (2000) for insurance companies, Dert (1995) for pension funds, Consiglio, Cocco and Zenios (2001) for minimum guarantee products, as well as Zenios (1993) and Ziemba and Mulvey (1998). Also, see Ziemba (2003) and other chapters in this volume.

I present a stochastic programming model for money management where frequent short-term portfolio rebalancing is commonplace and transactions costs and market impact costs play a significant role in determining trade sizes. Stochastic multiperiod models (of ALM type) are utilized to trade-off returns and transactions costs under various metrics of risk aversion. Indeed, such an approach must be adapted to market evolutionary parameters and optimized for possible errors in parameter forecasts via a specific investment strategy. The model is applied to historical time series of a large stock base and out-of-sample portfolio performance is tracked over daily rollover operation. The main focus is in developing the model and discussing its investment performance, rather than efficient solution algorithms for multistage stochastic programs of this type. The reader interested in the latter aspect is referred to the recent paper by Edirisinghe and Patterson (2007), in which a very efficient solution methodology is developed for real-time solution. Given that high frequency data are readily available on a global basis and computing hardware are becoming more powerful by orders of magnitude, sophisticated modeling techniques as presented here are expected to find broader appeal among the professional investment community.

Section 2 presents an introduction to formulating a multistage stochastic programming (MSP) model. This section also collects the necessary tree notation that will be required for understanding a MSP model. Section 3 provides the basic constructs of the MSP model for the investment optimization problem and several key policy constraints. Section 4 covers various issues with risk metrics and it introduces new and known methodologies for risk control. The multistage stochastic program for trade rebalancing problem is presented in Section 5, and the model application and results analyses are in Section 6. Concluding remarks are in Section 7. The required notation is introduced as it becomes necessary.

2 Multistage stochastic programming (MSP)

Multiperiod stochastic programs can be used to model a sequence of decision-observation processes in which decisions at any point in time are based upon historical observations coupled with beliefs or expectations concerning the uncertainty of future events. The term period is used to refer to the time starting with one decision or set of decisions and lasting until the next decision or set of decisions. See Birge, Edirisinghe and Ziemba (2001) for some applications of stochastic programming models and Birge and Louveaux (1997) for certain terms and definitions concerning stochastic linear programs. For a complete bibliography on stochastic programming, see van der Vlerk (2003).

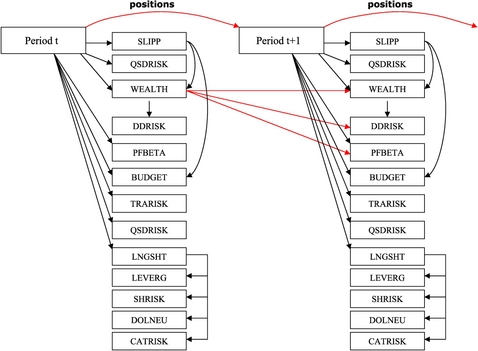

Decision trees, often referred to as event or scenario trees, are a useful tool for visualizing the resulting model. Decision trees demonstrate the nonanticipative requirement of stochastic programs—decisions in a given period must be made without the hindsight (or the anticipation) of a specific future outcome. The notation used in the development and discussion of multistage stochastic programs is not unique in the literature. The following notation that makes explicit the dependence of decisions and random events on historical scenario paths is used. Assume the number of outcomes ![]() possible at any node in period

possible at any node in period ![]() for arbitrary but finite T is the same for all nodes in that period. There are then

for arbitrary but finite T is the same for all nodes in that period. There are then ![]() total nodes in period t and

total nodes in period t and ![]() cumulative nodes in periods 1 through t. Nodes are labeled using a path vector format. The path vector, say

cumulative nodes in periods 1 through t. Nodes are labeled using a path vector format. The path vector, say ![]() , to a node in period t is a row vector of

, to a node in period t is a row vector of ![]() elements where element j,

elements where element j, ![]() , is the index,

, is the index, ![]() , of the outcome in period j along the path of outcomes to the applicable node. The path to a node in period t is called a t-period scenario and each T-period scenario is usually simply called a scenario of the stochastic program. Let

, of the outcome in period j along the path of outcomes to the applicable node. The path to a node in period t is called a t-period scenario and each T-period scenario is usually simply called a scenario of the stochastic program. Let ![]() represent a t-period scenario, i.e., the (historical) path vector to a node at the beginning of period t, see Figure 1. The single first period root node is labeled using the notation

represent a t-period scenario, i.e., the (historical) path vector to a node at the beginning of period t, see Figure 1. The single first period root node is labeled using the notation ![]() , or simply by

, or simply by ![]() for brevity, which represents the absence of any historical scenario path. By convention,

for brevity, which represents the absence of any historical scenario path. By convention, ![]() and

and ![]() appearing in the same expression implies that the former is the parent node of the latter while

appearing in the same expression implies that the former is the parent node of the latter while ![]() is a child node of

is a child node of ![]() .

.

A decision (vector) taken at node ![]() is denoted by

is denoted by ![]() . It is a nonanticipative decision that depends only on the specific history

. It is a nonanticipative decision that depends only on the specific history ![]() , which corresponds to the sequence of observed outcomes of the random vectors

, which corresponds to the sequence of observed outcomes of the random vectors ![]() , respectively. Having made the decision

, respectively. Having made the decision ![]() , the random vector

, the random vector ![]() will be observed whose domain of realizations are indicated by

will be observed whose domain of realizations are indicated by ![]() , which form the set of child nodes emanating from node

, which form the set of child nodes emanating from node ![]() .

.

The path-vector notation is also used to implicitly indicate the dependence of a stochastic array at a node in period t on the occurrence of the specific outcomes listed by the path vector. Let ![]() represent the period t outcome with index

represent the period t outcome with index ![]() ,

, ![]() , and let

, and let ![]() represent a node in period t,

represent a node in period t, ![]() . Then,

. Then,

represents a conditional stochastic matrix at node ![]() . The conditional probability that the outcome with index

. The conditional probability that the outcome with index ![]() ,

, ![]() ,

, ![]() , is observed at the t-period node

, is observed at the t-period node ![]() given the indicated outcomes

given the indicated outcomes ![]() in periods

in periods ![]() is

is ![]() , i.e.,

, i.e.,

where ![]() is the probability operator and

is the probability operator and ![]() . The joint probability,

. The joint probability, ![]() , that the process enters the period t node

, that the process enters the period t node ![]() ,

, ![]() , is the product of the conditional probabilities of the outcomes along the indicated path to that node,

, is the product of the conditional probabilities of the outcomes along the indicated path to that node,

where ![]() , i.e., the single first period (root) node is always entered.

, i.e., the single first period (root) node is always entered.

2.1 MSP model formulation

Using this notation for decision trees, a multiperiod stochastic program can be formulated recursively by considering the nodal decision problems. A linear stochastic programming model is presented for clarity; extensions to a general nonlinear framework is quite straightforward, see, e.g., formulations in Edirisinghe and Ziemba (1992) and Frauendorfer (1996). The decision process up to (tree) node ![]() has observed the realization sequence indexed as

has observed the realization sequence indexed as ![]() , and corresponds to the decision vector sequence

, and corresponds to the decision vector sequence ![]() . The nodal value function

. The nodal value function ![]() for a period t,

for a period t, ![]() , is the optimal profits to be realized after observing the event indexed by

, is the optimal profits to be realized after observing the event indexed by ![]() and by choosing the decision vector

and by choosing the decision vector ![]() to optimally trade off current profits

to optimally trade off current profits ![]() and the expected value of optimal profits at the child nodes, i.e.,

and the expected value of optimal profits at the child nodes, i.e., ![]() for each of

for each of ![]() . This nodal decision problem is formulated as follows, for

. This nodal decision problem is formulated as follows, for ![]() .

.

![]()

The nodal value function, ![]() , for a node at terminal period T, is

, for a node at terminal period T, is

![]()

Array dimensions are not explicitly listed for reasons of brevity and all arrays are assumed to have shapes and sizes compatible with the depicted operation. Then, the multistage stochastic program can be equivalently represented as the following compact recursive value function formulation.

![]()

3 Investment optimization model

There are N securities that an investor wishes to trade at time ![]() , i.e., at the beginning of period 1. The investor’s initial position (i.e., the number of shares in each security) is

, i.e., at the beginning of period 1. The investor’s initial position (i.e., the number of shares in each security) is ![]() (

(![]() ) and the initial cash position is

) and the initial cash position is ![]() . The price of security j at the first trading node, i.e., the root node

. The price of security j at the first trading node, i.e., the root node ![]() , is $

, is $![]() per share, see Figure 1 for the decision tree. The investor considers trading in multiple periods of time, denoted by the time index

per share, see Figure 1 for the decision tree. The investor considers trading in multiple periods of time, denoted by the time index ![]() . Given the historical price vectors

. Given the historical price vectors ![]() , up until the beginning of trading for period t, the (conditional) rate of return vector for period t is

, up until the beginning of trading for period t, the (conditional) rate of return vector for period t is ![]() . See Figure 2 for an illustration of the nodal trading information. Thus, price of security j changes during the trading period t to

. See Figure 2 for an illustration of the nodal trading information. Thus, price of security j changes during the trading period t to ![]() . Note that

. Note that ![]() since the security prices are nonnegative, i.e.,

since the security prices are nonnegative, i.e., ![]() . Moreover,

. Moreover, ![]() is random and it is observed only at the end of the current period t; however, trade decisions

is random and it is observed only at the end of the current period t; however, trade decisions ![]() must be made at the beginning of period t, i.e., revision of portfolio positions from

must be made at the beginning of period t, i.e., revision of portfolio positions from ![]() to

to ![]() . Therefore,

. Therefore, ![]() is the amount of shares purchased if it is positive; and if it is negative, it is the amount of shares sold in security j. This trade vector is

is the amount of shares purchased if it is positive; and if it is negative, it is the amount of shares sold in security j. This trade vector is ![]() and equals

and equals ![]() where

where ![]() is the absolute value.

is the absolute value.

The investment optimization problem is concerned with determining the trade vectors ![]() such that various risk specifications for the portfolio are met whilst maximizing the portfolio total expected return. Capturing this problem within a multistage framework is advantageous due to at least two important considerations. First, trading (for portfolio rebalancing) is generally not costless. Typically, with larger trade sizes, there is an increasingly diluting effect on the profitability of the trades due to market impact. Thus, it may be beneficial to create an intended position over multiple periods as the trading costs increase. Secondly, due to policy on risk control, portfolio wealth trajectory may have to be monitored, such as the case when portfolio drawdown is an important issue in fund management. Such drawdowns cannot be managed effectively via single period modeling.

such that various risk specifications for the portfolio are met whilst maximizing the portfolio total expected return. Capturing this problem within a multistage framework is advantageous due to at least two important considerations. First, trading (for portfolio rebalancing) is generally not costless. Typically, with larger trade sizes, there is an increasingly diluting effect on the profitability of the trades due to market impact. Thus, it may be beneficial to create an intended position over multiple periods as the trading costs increase. Secondly, due to policy on risk control, portfolio wealth trajectory may have to be monitored, such as the case when portfolio drawdown is an important issue in fund management. Such drawdowns cannot be managed effectively via single period modeling.

3.1 Transactions and slippage costs

Usually, fund managers face transactions costs in executing the trade vector, ![]() , which leads to reducing the portfolio net return. Placing a trade with a broker for execution entails a direct cost per share traded, as well as a fixed cost independent of the trade size. For instance, a $10 fixed cost and a 2-cent per-share cost may be levied. In addition, there is also a significant cost due to the size of trading volume

, which leads to reducing the portfolio net return. Placing a trade with a broker for execution entails a direct cost per share traded, as well as a fixed cost independent of the trade size. For instance, a $10 fixed cost and a 2-cent per-share cost may be levied. In addition, there is also a significant cost due to the size of trading volume ![]() , as well as the broker’s ability to place the trading volume on the market. If a significant volume of shares is traded (relative to the market daily traded volume in the security), then the trade execution price may be adversely affected. A large buy order usually lead to trade execution at a price higher than intended and a large sell order leads to an average execution price that is lower than desired. This dilution of the profits of the trade is termed the market impact loss, or slippage. This slippage loss generally depends on the price at which the trade is desired, trade size relative to the market daily volume in the security, and other company specifics such as market capitalization, and the beta of the security. See Keim and Madhavan (1996, 1997, 1998), Loeb (1983), and Torre and Ferrari (1999), for instance, for a discussion on market impact costs.

, as well as the broker’s ability to place the trading volume on the market. If a significant volume of shares is traded (relative to the market daily traded volume in the security), then the trade execution price may be adversely affected. A large buy order usually lead to trade execution at a price higher than intended and a large sell order leads to an average execution price that is lower than desired. This dilution of the profits of the trade is termed the market impact loss, or slippage. This slippage loss generally depends on the price at which the trade is desired, trade size relative to the market daily volume in the security, and other company specifics such as market capitalization, and the beta of the security. See Keim and Madhavan (1996, 1997, 1998), Loeb (1983), and Torre and Ferrari (1999), for instance, for a discussion on market impact costs.

In our model, a quadratic simplification for the market impact cost is utilized. That is, the slippage costs are proportional to the square of the volume traded in the market, and the constant of proportionality depends directly on the intended execution price, and inversely on the (daily) share volume in that security. For trading ![]() shares of security j (with the intended trade price

shares of security j (with the intended trade price ![]() when the expected total daily volume is

when the expected total daily volume is ![]() shares), thus, leads to a market impact cost of

shares), thus, leads to a market impact cost of

where ![]() is a constant calibrated to the market data. The direct cost of trading is represented by

is a constant calibrated to the market data. The direct cost of trading is represented by ![]() where

where ![]() is the per-share transactions cost. The fixed costs of trading are ignored here, and then, the total transactions and slippage loss function

is the per-share transactions cost. The fixed costs of trading are ignored here, and then, the total transactions and slippage loss function ![]() is

is

(4)

(4)Therefore, the total loss due to portfolio rebalancing at time t, given the historical scenario ![]() of security price evolution, is

of security price evolution, is

(5)

(5)3.2 Budget and portfolio wealth

Portfolio rebalancing from period-to-period is assumed to carry forward any cash that is accumulated (i.e., the riskless security) and the total cost of trading at the beginning of period t is thus limited by the cash carried forward from period ![]() , denoted by the nonnegative variable

, denoted by the nonnegative variable ![]() , and any exogenous funds available at the beginning of period t, denoted by

, and any exogenous funds available at the beginning of period t, denoted by ![]() . Then, the following budget constraint must hold.

. Then, the following budget constraint must hold.

The transposition of the price vector ![]() is suppressed for clarity of exposition in the above expression, as well as throughout the remainder of the chapter. When applying the budget constraint (6) for trading at the root node

is suppressed for clarity of exposition in the above expression, as well as throughout the remainder of the chapter. When applying the budget constraint (6) for trading at the root node ![]() , by convention,

, by convention, ![]() , the initial security positions, and

, the initial security positions, and ![]() , the initial cash position. Note that “cash” carried forward yields a deterministic monetary return from period to period given by the rate

, the initial cash position. Note that “cash” carried forward yields a deterministic monetary return from period to period given by the rate ![]() (⩾1), which is already adjusted to the length of the period t. Thus,

(⩾1), which is already adjusted to the length of the period t. Thus, ![]() is the excess cash carried forward and available for portfolio rebalancing at node

is the excess cash carried forward and available for portfolio rebalancing at node ![]() of period

of period ![]() . In the event that trading is required to be self-financing, one must set

. In the event that trading is required to be self-financing, one must set ![]() . Alternatively, if a certain dollar amount, say

. Alternatively, if a certain dollar amount, say ![]() , must be taken off the stock market (to satisfy a certain known liability at the current time period), then, one must set

, must be taken off the stock market (to satisfy a certain known liability at the current time period), then, one must set ![]() .

.

Given portfolio rebalancing at the current decision node ![]() to obtain revised positions

to obtain revised positions ![]() , the portfolio gain under (future) return scenario vector

, the portfolio gain under (future) return scenario vector ![]() , is

, is

where ![]() represents the diagonal matrix in which the jth diagonal element is

represents the diagonal matrix in which the jth diagonal element is ![]() . Observe that the uncertainty of the return

. Observe that the uncertainty of the return ![]() , conditional upon the history

, conditional upon the history ![]() being followed, endows the portfolio gain variable

being followed, endows the portfolio gain variable ![]() with uncertainty. Consequently, the projected portfolio wealth, denoted by

with uncertainty. Consequently, the projected portfolio wealth, denoted by ![]() , under return scenario

, under return scenario ![]() satisfies

satisfies

where ![]() denotes the portfolio wealth (consisting of cash and risky securities) at the end of period

denotes the portfolio wealth (consisting of cash and risky securities) at the end of period ![]() , evaluated before trading at the current decision node

, evaluated before trading at the current decision node ![]() using the state price vector

using the state price vector ![]() . When applying (8) for

. When applying (8) for ![]() , the initial portfolio wealth prior to trading at the root node

, the initial portfolio wealth prior to trading at the root node ![]() is

is ![]() . It must be noted that, at some period t under some return scenario

. It must be noted that, at some period t under some return scenario ![]() , it is possible that the portfolio projected wealth variable

, it is possible that the portfolio projected wealth variable ![]() , which thus indicates the termination of the portfolio. Consequently,

, which thus indicates the termination of the portfolio. Consequently,

is specified as a required feasibility condition under all realizations of the scenario tree.

3.3 Limiting positions

The nonnegative trade-size in security j is ![]() . Since the investment objective is to maximize the total portfolio (expected) return, less the convex quadratic slippage loss

. Since the investment objective is to maximize the total portfolio (expected) return, less the convex quadratic slippage loss ![]() in (5), the following linear constraints can be used to replace the nonlinear (absolute-value) expressions for the trade-size vector:

in (5), the following linear constraints can be used to replace the nonlinear (absolute-value) expressions for the trade-size vector:

Positions ![]() , after portfolio revision, must satisfy certain minimum/maximum limits due to policy requirements. This often arises from requiring that no more than (or no less than for the purposes of short positions) a certain dollar allocation be made in a particular security. In share volume terms, these maximum and minimum position limits are

, after portfolio revision, must satisfy certain minimum/maximum limits due to policy requirements. This often arises from requiring that no more than (or no less than for the purposes of short positions) a certain dollar allocation be made in a particular security. In share volume terms, these maximum and minimum position limits are ![]() and

and ![]() , and thus the resulting constraints are

, and thus the resulting constraints are

Alternatively, long and short positions in the portfolio may be controlled in aggregate by using the long leverage and short leverage restrictions. That is, a prespecified nonnegative $ limit ![]() may be applied for the total long position and

may be applied for the total long position and ![]() for the total short position, when trading for period t, which yields

for the total short position, when trading for period t, which yields

A linear representation of the above is obtained by defining pairs of nonnegative (long/short) variables ![]() and

and ![]() , for security j, such that

, for security j, such that

Under the variable description above, the following pair of linear constraints can be used to represent the leverage constraints.

Furthermore, the total short position may be controlled relative to the total long position, and vice versa. The primary reason for such joint control is to limit portfolio risk exposure and it is often dependent on fund manager’s investment style or policy. Consequently, we identify two major forms of portfolio risk control; those arising from direct position control due to policy and those that control investments due to portfolio risk measurement. We consider several forms of direct position control first; in Section 4, several risk metrics for portfolio risk control are discussed.

3.4 Excessive shortsale risk

While position limits or leverage constraints themselves are forms of policy-oriented risk controls, the strategies that belong to this category control relative positions of long and short exposure. The first of this type considered here is excessive shortsale risk, or ESR. In this type of control, the total short position is controlled not to exceed a certain fraction of the total long position, within a pre-identified group of securities. For instance, in order to limit the short-selling risk within a volatile sector, such as the Internet stocks, the managerial policy may be that no more than 30% of the long position in Internet stocks may be tied in short positions within the same sector. Such a policy may also be interpreted as some sort of margin requirement within a certain group of securities.

In a more generalized setting, such margin requirements may apply to different groups of stocks differently. Suppose there are K groups of stocks whose index set is denoted by ![]() , for

, for ![]() , such that

, such that ![]() . Given the value of the allowable shortsale fraction for group

. Given the value of the allowable shortsale fraction for group ![]() of stocks as

of stocks as ![]() , these constraints are

, these constraints are

(14)

(14)Although the allowable fractions ![]() may be specified such that they are dependent on the time period or the historical scenario being followed, such dependencies are ignored here for the ease of exposition. Noting that (14) is nonlinear, an alternative linear formulation is available under the condition that

may be specified such that they are dependent on the time period or the historical scenario being followed, such dependencies are ignored here for the ease of exposition. Noting that (14) is nonlinear, an alternative linear formulation is available under the condition that ![]() .

.

Proposition 3.1 If ![]() for

for ![]() , then the nonlinear margin constraints in (14) have the following equivalent linear representation

, then the nonlinear margin constraints in (14) have the following equivalent linear representation

Proof Let ![]() (

(![]() ) be a feasible solution in (14). Then, construct the nonnegative pair of vectors

) be a feasible solution in (14). Then, construct the nonnegative pair of vectors ![]() such that, for

such that, for ![]() ,

, ![]() and

and ![]() . Observe that the pair

. Observe that the pair ![]() satisfies the inequality in (15); furthermore, it satisfies the equality in (12) since

satisfies the inequality in (15); furthermore, it satisfies the equality in (12) since

hence, a feasible solution to the linear representation of the shortsale constraints.

Conversely, it will be shown that given a pair ![]() that is feasible in (15), one obtains a feasible solution

that is feasible in (15), one obtains a feasible solution ![]() in (14) using the construction:

in (14) using the construction:

Defining, ![]() , it follows that

, it follows that ![]() and

and

(16)

(16)Using this “hat” solution and substituting from (16) in (14):

is feasible in (15)

is feasible in (15)This completes the proof.

The condition that ![]() implies that the total short position in the group cannot exceed the total long position. Thus, the use of ESR constraints allows the fund manager to keep the short investment within the total long investment with respect to a given group of securities. However, often a portfolio is required to be neutral in its long and short investments so as to immune the portfolio from any particular directional risk. Two types of portfolio neutral strategies will be discussed in the next section: beta neutrality and dollar neutrality.

implies that the total short position in the group cannot exceed the total long position. Thus, the use of ESR constraints allows the fund manager to keep the short investment within the total long investment with respect to a given group of securities. However, often a portfolio is required to be neutral in its long and short investments so as to immune the portfolio from any particular directional risk. Two types of portfolio neutral strategies will be discussed in the next section: beta neutrality and dollar neutrality.

3.5 Degree of portfolio neutrality

Portfolio neutrality is provided by hedging strategies that balance investments among carefully chosen long and short positions. Fund managers use such strategies to balance the portfolio so as to buffer it from severe market swings, for instance, see Nicholas (2000) and Jacobs and Levy (2004). Alternatively, a prescribed level of imbalance or nonneutrality may be specified in order for the portfolio to maintain a given bias with respect to market swings. An important metric of portfolio bias relative to the broader market is the portfolio beta. A balanced investment such that portfolio beta is zero is considered a perfectly beta neutral portfolio and such a strategy is uncorrelated with the market return. Beta is the measurement of a stock’s volatility relative to the market. A stock with a beta of 1 moves historically in sync with the market, while a stock with a higher beta tends to be more volatile than the market and a stock with a lower beta can be expected to rise and fall more slowly than the market. Many practitioners of beta neutral long/short trading balance their positions in the same sector or industry. By being sector neutral, the risk of market swings affecting some industries or sectors differently than others may be avoided.

The degree of market-neutrality of the portfolio measures the level of correlation of performance of the portfolio with an underlying broad-market index. Typically, the S&P 500 index may be used as the market barometer; alternatively, if the portfolio is constructed out of the S&P 100 stocks, the S&P 100 index may serve as the underlying market performance metric. Let ![]() be the beta of the security j given the sequence of historical prices observed, as indicated by scenario

be the beta of the security j given the sequence of historical prices observed, as indicated by scenario ![]() . Then,

. Then, ![]() is the (estimated conditional) covariance of the rates of return between the security j and the chosen market barometer (index), scaled by the variance of the market rate of return. Since

is the (estimated conditional) covariance of the rates of return between the security j and the chosen market barometer (index), scaled by the variance of the market rate of return. Since ![]() is the random variable representing the rate of return of security j, by denoting the market index rate of return by the random variable

is the random variable representing the rate of return of security j, by denoting the market index rate of return by the random variable ![]() , it follows that

, it follows that

At a portfolio rebalancing decision node ![]() , the resulting portfolio beta

, the resulting portfolio beta ![]() can be obtained by

can be obtained by

Proposition 3.2 At some trading node ![]() , having observed the price vector

, having observed the price vector ![]() at the beginning of period t on the portfolio positions

at the beginning of period t on the portfolio positions ![]() , let the portfolio value before trading be

, let the portfolio value before trading be ![]() . Suppose the portfolio is rebalanced at the current node to establish the new security positions

. Suppose the portfolio is rebalanced at the current node to establish the new security positions ![]() . Then, the resulting portfolio beta,

. Then, the resulting portfolio beta, ![]() , is

, is

(18)

(18)Proof Since the projected portfolio value at period t is given by (8), the rate of return of portfolio for period t is the random variable ![]() and thus,

and thus, ![]() . Referring to (7), the conditional covariance given

. Referring to (7), the conditional covariance given ![]() and

and ![]() , is

, is

since the cash rate ![]() is assumed fixed (and thus it has zero correlation with the market). The result in the proposition then follows.

is assumed fixed (and thus it has zero correlation with the market). The result in the proposition then follows.

To control the portfolio beta at a level ![]() , the constraints

, the constraints ![]() must be imposed at each trade rebalancing decision node

must be imposed at each trade rebalancing decision node ![]() . By the nonnegativity in (9), the required portfolio beta constraints are

. By the nonnegativity in (9), the required portfolio beta constraints are

Portfolio beta is set at ![]() with a tolerance level of

with a tolerance level of ![]() . With

. With ![]() , rebalancing strives for a portfolio beta of

, rebalancing strives for a portfolio beta of ![]() . In particular, with

. In particular, with ![]() , the model attempts for a perfectly beta-neutral dynamic investment in the portfolio.

, the model attempts for a perfectly beta-neutral dynamic investment in the portfolio.

In addition to the (degree of) market neutrality afforded by the above beta constraints, fund managers often seek additional neutrality through dollar neutrality. In order to create a portfolio with dollar neutrality, equal amounts of long and short investments are made, or alternatively, a specific dollar imbalance may be prescribed as policy. Given a targeted maximum dollar imbalance of ![]() , the “degree of dollar neutrality” constraint is

, the “degree of dollar neutrality” constraint is

Under the variable description in (12), the equivalent linear constraints are:

If portfolio risk control is solely via market neutral long/short trading as an act of portfolio balancing, then it would generally involve a large amount of buying and selling. Such a strategy naturally leads to additional risks as the fund manager now needs to have the ability to execute trades efficiently as well as to keep brokerage costs from severely affecting trading profits. Furthermore, fund managers must also trade in very liquid stocks, indicating a high level of daily volume, in order to ensure they can get quickly in and out of positions, as happens in frequent trading. Therefore, portfolio risk management should not be viewed solely through such policy or balancing strategies. Furthermore, in order to keep trading costs relatively low, relative to short term rates of returns of securities, a multiperiod trading view must be taken when portfolio rebalancing and risk controls must be applied within such a setting.

4 Portfolio risk metrics

While the foregoing discussion alluded to risk control via policy statements, portfolio risk management is closely tied with the ability to describe future uncertainty of stock returns. This is already apparent in the beta neutrality constraints where a vector of stock (conditional) beta, ![]() , must be estimated at each decision node, given a historical scenario

, must be estimated at each decision node, given a historical scenario ![]() . In addition, there may be other parameters of stock returns that need to be estimated, most notably, the conditional expectation of stock returns,

. In addition, there may be other parameters of stock returns that need to be estimated, most notably, the conditional expectation of stock returns, ![]() , the conditional standard deviation of stock returns,

, the conditional standard deviation of stock returns, ![]() , or the full variance–covariance matrix of returns,

, or the full variance–covariance matrix of returns, ![]() .

.

Once the required parameters have been forecasted at node ![]() , the conditional (descendant) outcomes of security returns for period

, the conditional (descendant) outcomes of security returns for period ![]() must be generated, denoted by

must be generated, denoted by ![]() . That is, a specific scenario generator must also be utilized at decision node

. That is, a specific scenario generator must also be utilized at decision node ![]() to generate the sample of

to generate the sample of ![]() outcomes. It is this scenario generator that endows the decision model with the multistage scenario tree structure. In this section, we assume that all of the required forecasted parameters, as well as a scenario tree depicting an approximated view of decision epochs in the future are available.

outcomes. It is this scenario generator that endows the decision model with the multistage scenario tree structure. In this section, we assume that all of the required forecasted parameters, as well as a scenario tree depicting an approximated view of decision epochs in the future are available.

Portfolio risk control at a current decision node, as well as along any anticipated sequence of decision epochs, has been one of the major subjects of discussion in multistage financial stochastic optimization. Portfolio wealth variation around its expectation is often used as a way of measuring portfolio risk, such as the case in the classical Markowitz mean-variance analysis, Markowitz (1959). An alternative to mean-variance risk trade-off is the expected utility of wealth at a current decision node. The first formal axiomatic treatment of utility was given by von Neumann and Morgenstern (1944). Other objective functions are possible, such as the one proposed by Zhao and Ziemba (2001). Artzner et al. (1999) introduced the concept of coherent risk measures. This landmark paper initiated a wealth of literature to follow on coherent risk measures with several interesting extensions, see, for instance, Jarrow (2002), Delbaen (2000), Roorda, Engwerda and Schumacher (2002), and Follmer and Schied (2002). Coherent risk measures scale linearly if the underlying uncertainty is changed, and due to this linearity, coherency alone does not lead to risk measures that are useful in applications. As discussed in Warachka, Zhao and Ziemba (2004), one important limitation of coherent risk measures is its inability to yield sufficient diversification to reduce portfolio risk. Alternatively, they propose a methodology that defines risk on the domain of portfolio holdings and utilizes quadratic programming to “measure” portfolio risk.

An alternative method of risk measurement is to use the conditional value-at-risk (CVaR), see, e.g., Rockafellar and Uryasev (2000) and Ogryczak and Ruszczynski (2002). Risk measures based on mean and CVaR are coherent, see Rockafellar, Uryasev and Zabarankin (2002). Such risk measures evaluate portfolio risk according to its value in the worst possible scenario or under the probability measure that produces the largest negative outcome. CVaR can also be used, just as in moment-based approximations, see Edirisinghe (1999), for approximating a given sample of scenarios. Such an approach is taken in Bychkov and Edirisinghe (2004) where CVaR is used as a metric for approximating scenarios for financial investment problems.

In the sequel, we view a risk metric at a decision node ![]() as either Static Risk Control (SRC), or Dynamic Risk Control (DRC). In SRC, the computation of risk, for taking a rebalancing decision

as either Static Risk Control (SRC), or Dynamic Risk Control (DRC). In SRC, the computation of risk, for taking a rebalancing decision ![]() , requires only the forecasted parameters of a distribution (of uncertainty). That is, such a risk metric does not require a distributional assumption or a specific approximated random sample from the distribution, but risk can be specified through a closed-form expression. As an example, one may consider variance of the portfolio as a static risk metric, as in mean-variance analysis. One advantage of SRC is that risk computation remains independent of the scenario samples being generated. Then, scenario trees can be generated to guide the rebalancing decisions carefully, without imparting a sample bias in risk computation. With small sample scenario tress, the resulting multistage stochastic optimization models become computationally more attractive. In contrast, with DRC risk controls, computing the risk associated with a rebalancing decision

, requires only the forecasted parameters of a distribution (of uncertainty). That is, such a risk metric does not require a distributional assumption or a specific approximated random sample from the distribution, but risk can be specified through a closed-form expression. As an example, one may consider variance of the portfolio as a static risk metric, as in mean-variance analysis. One advantage of SRC is that risk computation remains independent of the scenario samples being generated. Then, scenario trees can be generated to guide the rebalancing decisions carefully, without imparting a sample bias in risk computation. With small sample scenario tress, the resulting multistage stochastic optimization models become computationally more attractive. In contrast, with DRC risk controls, computing the risk associated with a rebalancing decision ![]() would require further distributional knowledge of the random vector

would require further distributional knowledge of the random vector ![]() , and also possibly of the random vectors

, and also possibly of the random vectors ![]() . As an example of DRC, consider CVaR which would require a sample of outcomes for

. As an example of DRC, consider CVaR which would require a sample of outcomes for ![]() . If one hopes to eliminate possible sampling bias, a sufficiently large number of outcomes (i.e.,

. If one hopes to eliminate possible sampling bias, a sufficiently large number of outcomes (i.e., ![]() ) must be generated at each decision node for computation of CVaR. In multistage stochastic programming, such a practice would lead to enormous computational difficulties. Therefore, from a pure computational standpoint, SRC risk metrics may appear appealing. However, as it turns out, each risk metric endows the portfolio with different characteristics, as will be discussed later.

) must be generated at each decision node for computation of CVaR. In multistage stochastic programming, such a practice would lead to enormous computational difficulties. Therefore, from a pure computational standpoint, SRC risk metrics may appear appealing. However, as it turns out, each risk metric endows the portfolio with different characteristics, as will be discussed later.

Several static controls and dynamic controls will be developed in the remaining sections and applied in the investment optimization model.

4.1 Static risk control (SRC)

Two types of risk metrics are considered in the context of SRC, where risk expressions can be obtained in closed-form based on the forecasted parameters of uncertainty at a given decision node ![]() . Such SRC may be applied at all rebalancing nodes in the decision (scenario) tree. The first is a variant of portfolio variance, and the second is what is termed the portfolio catastrophic risk.

. Such SRC may be applied at all rebalancing nodes in the decision (scenario) tree. The first is a variant of portfolio variance, and the second is what is termed the portfolio catastrophic risk.

The use of portfolio variance as a risk expression and using it within a static mean variance trade-off optimization model date back to Markowitz (1959). Its multistage extensions, where mean-variance trade-off is specified at each of the decision nodes in a scenario tree, too are considered in the literature, see, e.g., Steinbach (2001) and the many references therein, and also Gulpinar, Rustem and Settergren (2003). The mean-variance trade-off is a quadratic programming model, and thus, the application of quadratic programming on a multistage stochastic programming model is computationally tedious.

In our development here, a generalized approach to portfolio (quadratic) tracking penalty is considered and portfolio variance is obtained as a special case. Consider a target return that portfolio wishes to track. Such targets can be either deterministic or stochastic, and also, they can be exogenously or endogenously specified, see Geyer et al. (2003). For instance, tracking the portfolio mean is a target specified endogenously, but deterministic. An example of a stochastic (and exogenous) target is the return on a broad market index, which may be correlated with the portfolio securities. Index target is considered exogenous because it is assumed that portfolio rebalancing does not affect the broader market index to any appreciable extent. Benchmark tracking for portfolio management has been well-studied in the literature, see, for example, Dembo and King (1992), Frino and Gallagher (2001), Jansen and van Dijk (2002), Roll (1992), and El-Hassan and Kofman (2003). However, the approach taken here is slightly different, as discussed below.

4.1.1 Tracking risk control

Consider a benchmark (stochastic) target, such as the return on a broad market index, say the S&P 500 index. Let the conditional rate of return (RoR) on the benchmark index, at time t at the rebalancing decision node ![]() , be

, be ![]() , which is a univariate random variable. In a pure investment in the benchmark index, the total investment in the portfolio, given by

, which is a univariate random variable. In a pure investment in the benchmark index, the total investment in the portfolio, given by ![]() , yields the target total $ return

, yields the target total $ return ![]() as

as

![]() is a univariate random variable and it serves as the target return for the portfolio for period t. The conditional expectation of the quadratic tracking penalty for portfolio return on risky investments not following the above target return is

is a univariate random variable and it serves as the target return for the portfolio for period t. The conditional expectation of the quadratic tracking penalty for portfolio return on risky investments not following the above target return is

Denoting the portfolio standard deviation by ![]() , its variance is

, its variance is

where ![]() is the (conditional) variance–covariance matrix of the random vector

is the (conditional) variance–covariance matrix of the random vector ![]() .

.

Proposition 4.1 An upper bounding risk metric on the tracking penalty in (22) is

(24)

(24)where ![]() is the index rate of return and

is the index rate of return and ![]() is the index standard deviation.

is the index standard deviation.

Proof Note that

Using the expression

and upon algebraic manipulation, it follows that

due to the nonnegativity of the second term in the above equality expression.

Observe that the risk metric ![]() can be interpreted as the sum of the three components,

can be interpreted as the sum of the three components,

In particular, when the target being tracked is simply the portfolio mean itself, then the above risk metric is

Corollary 4.2 If the target is specified as ![]() , then the risk metric becomes

, then the risk metric becomes ![]() , i.e., the usual portfolio variance.

, i.e., the usual portfolio variance.

The risk metric ![]() in (24) is of static-type as it is computable under the forecasted parameters, and also it is convex quadratic in the portfolio positions

in (24) is of static-type as it is computable under the forecasted parameters, and also it is convex quadratic in the portfolio positions ![]() . The use of such a risk metric in the portfolio model is to seek a trade-off between the risk metric and the portfolio expected net return after rebalancing. This objective, at the current rebalancing node, is

. The use of such a risk metric in the portfolio model is to seek a trade-off between the risk metric and the portfolio expected net return after rebalancing. This objective, at the current rebalancing node, is

where the function ![]() is defined in (7), and

is defined in (7), and ![]() is herein termed a (static) tracking risk aversion (TRA) coefficient, which is nonnegative.

is herein termed a (static) tracking risk aversion (TRA) coefficient, which is nonnegative.

4.1.2 Catastrophic risk control

A second form of significant portfolio risk is next considered, largely motivated by practitioners. This form of risk is concerned with the direction of (the future) price of a security being opposite to the sign of the established position in the portfolio. That is, securities in a long portfolio fall in price while the securities in a short portfolio rise in price. Such risk is often the result of error in forecasting the direction of stock price movement. This would entail observing a drop in price for long securities and an increase in price for shorted securities. Generally, there is no formal mechanism to safeguard against the risk posed by such a catastrophic event. Controlling the portfolio variance, or more generally the tracking risk metric ![]() discussed above, does not necessarily counter the effects of catastrophic risk, abbreviated herein as Cat risk. The effects of Cat risk control in a portfolio is demonstrated under the section on model application.

discussed above, does not necessarily counter the effects of catastrophic risk, abbreviated herein as Cat risk. The effects of Cat risk control in a portfolio is demonstrated under the section on model application.

We define Cat risk as the anticipated total dollar wealth loss in the event stock returns move against the portfolio positions by one standard deviation, denoted by ![]() , where the positions

, where the positions ![]() are established at event node

are established at event node ![]() for period t. That is,

for period t. That is,

(26)

(26)which is thus a form of static risk control. While the Cat risk expression is free of correlations among securities, it can be shown that it provides an upper bound on the portfolio standard deviation.

Proposition 4.3 The portfolio standard deviation is a lower bound on the catastrophic risk, i.e., ![]() where

where ![]() is given by (23).

is given by (23).

Proof

Defining the random variable ![]() , variance of the portfolio is

, variance of the portfolio is ![]() . Denoting the standard deviation of

. Denoting the standard deviation of ![]() by

by ![]() and the correlation between

and the correlation between ![]() and

and ![]() by

by ![]() ,

,

Noting that ![]() , and since the prices are nonnegative, we have

, and since the prices are nonnegative, we have ![]() . Therefore, it follows that the portfolio variance is bounded from above by

. Therefore, it follows that the portfolio variance is bounded from above by ![]() .

.

Since portfolio standard deviation is only a lower bound on Cat risk, controlling portfolio variance, as in Markowitz-style, is not guaranteed to provide adequate protection against catastrophic risk. In contrast, controlling Cat risk will certainly control the portfolio variance directly, and thus, Cat risk metric plays a dual role in portfolio rebalancing. The two risk metrics, ![]() and

and ![]() , however, have distinct characteristics in shaping portfolio positions, as will be demonstrated numerically later. Geometrically, Cat risk (as a function of portfolio positions) bounds the portfolio standard deviation by a polyhedral convex cone with apex at the origin.

, however, have distinct characteristics in shaping portfolio positions, as will be demonstrated numerically later. Geometrically, Cat risk (as a function of portfolio positions) bounds the portfolio standard deviation by a polyhedral convex cone with apex at the origin.

While it is possible to incorporate ![]() in to the objective function with a risk aversion coefficient, similar to (25), it is easier to specify the maximum allowable $ loss in the portfolio for a catastrophic move (of, say, one standard deviation) as a constraint. The Cat risk constraint is then

in to the objective function with a risk aversion coefficient, similar to (25), it is easier to specify the maximum allowable $ loss in the portfolio for a catastrophic move (of, say, one standard deviation) as a constraint. The Cat risk constraint is then

where $![]() is the pre-specified dollar loss. Since

is the pre-specified dollar loss. Since ![]() is nonlinear in its arguments, a linear representation is obtained by appealing to the pairs of nonnegative (long/short) variables given in (12). Then, the following linear constraint replaces the Cat risk constraint in (27),

is nonlinear in its arguments, a linear representation is obtained by appealing to the pairs of nonnegative (long/short) variables given in (12). Then, the following linear constraint replaces the Cat risk constraint in (27),

Since it is possible to easily argue that (27) and (28) provide equivalent expressions for risk control, details are skipped here. Note that (28) limits positions (long or short) in securities with high volatility (as measured by ![]() ), and thus provides a form of indirect position control.

), and thus provides a form of indirect position control.

4.2 Dynamic risk control (DRC)

As defined earlier, in DRC, risk metric computation requires the availability of a scenario sample (conditional upon the history ![]() ), in addition to the forecasted parameters, at a rebalancing decision node

), in addition to the forecasted parameters, at a rebalancing decision node ![]() . In the tracking risk metric, portfolio wealth variation around a target is penalized in either direction. In the case when the target is the portfolio mean, the result is the Markowitz mean-variance trade-off. Mean-variance optimal portfolios are shown to be (stochastically) dominated by carefully constructed portfolios. Such is the case when one penalizes only the variation of portfolio value on the downside, i.e., the risk metrics based on downside deviation.

. In the tracking risk metric, portfolio wealth variation around a target is penalized in either direction. In the case when the target is the portfolio mean, the result is the Markowitz mean-variance trade-off. Mean-variance optimal portfolios are shown to be (stochastically) dominated by carefully constructed portfolios. Such is the case when one penalizes only the variation of portfolio value on the downside, i.e., the risk metrics based on downside deviation.

The relative merits of using Markowitz mean-variance type models and those that trade off mean with downside semi-deviation are examined in Ogryczak and Ruszczynski (1999). The semi-deviation risk trade-off approach yields superior portfolios that are efficient with respect to the standard stochastic dominance rules, see Whitmore and Findlay (1978). When quadratic penalty is applied on the downside deviations, with target defined at the portfolio mean, it is called the downside semi-variance risk metric. The concept of semi-variance was described by Markowitz (1959, Chapter IX). Semi-variance fails to satisfy the positive homogeneity property required for a coherent risk measure, see Artzner et al. (1999) and Rockafellar, Uryasev and Zabarankin (2002).

4.2.1 Quadratic downside risk control

The approach of downside deviation, as applied in this chapter, is slightly more general than the downside semi-variance. A target is specified by translating the portfolio mean by an amount determined by the relative volatilities of the underlying securities. The translation could be on the upside or the downside of the mean. Define the volatility-adjusted-mean (VAM), denoted by ![]() , as

, as

(29)

(29)and specify the wealth target by

(30)

(30)where θ is a (positive or negative) scalar. For ![]() , the target is specified above the mean, and for

, the target is specified above the mean, and for ![]() , target is below the portfolio mean; however, the resulting target being dependent on the relative risk of an individual security, as measured by

, target is below the portfolio mean; however, the resulting target being dependent on the relative risk of an individual security, as measured by ![]() . Then, the quadratic risk metric for downside deviation from this target is

. Then, the quadratic risk metric for downside deviation from this target is

For ![]() ,

, ![]() is the usual downside semi-variance risk metric. Note that

is the usual downside semi-variance risk metric. Note that ![]() yields more risk aversion (

yields more risk aversion (![]() yields less risk aversion) than the standard semi-variance metric. The computation of (31) requires distributional information of the (conditional) security returns, or at least to have a discrete scenario sample to compute it as a finite summation. In the sequel,

yields less risk aversion) than the standard semi-variance metric. The computation of (31) requires distributional information of the (conditional) security returns, or at least to have a discrete scenario sample to compute it as a finite summation. In the sequel, ![]() is computed based on the descendant outcome sample of scenarios

is computed based on the descendant outcome sample of scenarios ![]() at node

at node ![]() . Therefore, choosing a relatively small sample size (

. Therefore, choosing a relatively small sample size (![]() ) would certainly lead to significant sample bias in the risk metric, while increasing the size of

) would certainly lead to significant sample bias in the risk metric, while increasing the size of ![]() leads to a heavy computational burden. The reason for the latter computational difficulty becomes clear when incorporating

leads to a heavy computational burden. The reason for the latter computational difficulty becomes clear when incorporating ![]() in to the trade optimization at node

in to the trade optimization at node ![]() , i.e.,

, i.e.,

where the function ![]() is defined in (7), and

is defined in (7), and ![]() is herein termed the (dynamic) quadratic risk aversion (QRA) coefficient, which is nonnegative. To evaluate the risk term in (32), the expectation in (31) must be specified in computable terms, by defining downside deviation variables,

is herein termed the (dynamic) quadratic risk aversion (QRA) coefficient, which is nonnegative. To evaluate the risk term in (32), the expectation in (31) must be specified in computable terms, by defining downside deviation variables, ![]() , over the domain of

, over the domain of ![]() as

as

Then, the optimization in (32) becomes

where the deviation variables satisfy the constraints

and these constraints will be imposed along each sample outcome ![]() , for

, for ![]() . Thus, as the sample size is increased at node

. Thus, as the sample size is increased at node ![]() , the size of the resulting nodal optimization model will also increase (unlike in the case of SRC).

, the size of the resulting nodal optimization model will also increase (unlike in the case of SRC).

4.2.2 Drawdown risk control (DDR)

A second type of dynamic risk control of paramount importance to fund managers is the so-called portfolio drawdown control. Investors and fund managers do not wish to see the value of the portfolio decline considerably over time. Such drastic declines in portfolio value may lead to perceptions that the fund is too risky; it may even lead to losing important client accounts from the fund. Portfolio drawdown is defined as the relative equity loss from the highest peak to the lowest valley of a portfolio value decline within a given window of observation. Mathematically, given the current rebalancing node ![]() and the portfolio wealth trajectory

and the portfolio wealth trajectory ![]() , for

, for ![]() where

where ![]() , the maximum portfolio value in the

, the maximum portfolio value in the ![]() time window is

time window is

The portfolio, under the revised portfolio positions ![]() , is said to have

, is said to have ![]() -period drawdown under return vector

-period drawdown under return vector ![]() if

if ![]() holds, and in this case, the relative drawdown is measured by

holds, and in this case, the relative drawdown is measured by

For instance, suppose a fund manager has logged the portfolio wealth at the beginning of a year at $5 million, which reaches a peak in June to $8 million, and then loses its value to $6 million by the end of the year. Thus, for the period of one year, the fund had a relative drawdown of ![]() , or 25%, while the fund has an annual RoR of

, or 25%, while the fund has an annual RoR of ![]() , or 20%. Portfolio performance, as measured by the reward-to-drawdown (RTD) ratio, is

, or 20%. Portfolio performance, as measured by the reward-to-drawdown (RTD) ratio, is ![]() , and in this example, it is indicative of poor portfolio performance. Successful money managers strive for ratios of 2 or better. Another important issue in portfolio drawdown is the time it takes to recover from the (drawdown) losses, termed as the drawdown recovery time, relative to the drawdown duration time. Indeed, shorter recovery times are preferable in money management. Aiming for the highest portfolio return, usually, does not translate to a high RTD ratio. While individuals may have the intention for fast portfolio growth with a “stomach” for large and repeated drawdowns, a low RTD ratio is not a trait of a successful money manager.

, and in this example, it is indicative of poor portfolio performance. Successful money managers strive for ratios of 2 or better. Another important issue in portfolio drawdown is the time it takes to recover from the (drawdown) losses, termed as the drawdown recovery time, relative to the drawdown duration time. Indeed, shorter recovery times are preferable in money management. Aiming for the highest portfolio return, usually, does not translate to a high RTD ratio. While individuals may have the intention for fast portfolio growth with a “stomach” for large and repeated drawdowns, a low RTD ratio is not a trait of a successful money manager.

Regulatory control in portfolio drawdown makes fund manager’s task quite challenging. For instance, according to Chekhlov, Uryasev and Zabarankin (2003), “it is highly uncommon, for a Commodity Trading Advisor (CTA) to still hold a client whose account was in a drawdown, even of small size, for longer than 2 years. By the same token, it is unlikely that a particular client will tolerate a 50% drawdown in an account with an average- or small-risk CTA. Similarly, in an investment bank setup, a proprietary system trader will be expected to make money in 1 year at the longest, i.e., he cannot be in a drawdown for longer than a year. Also, he/she may be shut down if a certain maximal drawdown condition will be breached, which, normally, is around 20% of his backing equity. Additionally, he will be given a warning drawdown level at which he will be reviewed for letting him keep running the system (around 15%). Obviously, these issues make managed accounts practitioners very concerned about both the magnitude and duration of their clients’ accounts drawdowns.”

Despite this apparent significance of drawdown, theoretical development on a drawdown risk metric is relatively sparse. Grossman and Zhou (1993) consider an exact analytical solution of a maximal drawdown problem for a one-dimensional case under lognormality assumptions. Subsequently, Cvitanic and Karatzas (1995) generalized this work for multiple dimensions. In contrast, Chekhlov, Uryasev and Zabarankin (2003) developed a metric, termed the conditional drawdown-at-risk (CDaR), and applied it along sample paths of portfolio returns with no assumptions on underlying distributions. Nevertheless, all these deal with either a static model that is rolled over in time, or holding constant portfolio weights over the duration of the sample paths.

Since the portfolio drawdowns in multiple periods in the future are affected by the current rebalancing decisions (in the presence of trading costs), applying drawdown risk control within a multistage framework is expected to improve portfolio reward-to-drawdown (RTD) ratio considerably. This is highlighted in the numerical experiments reported in Section 6. To develop our drawdown risk (DDR) metric, it is assumed, without loss of generality, that the drawdown window begins from the root node ![]() at time

at time ![]() , i.e.,

, i.e., ![]() holds in (36) for maximum portfolio value. Define the drawdown random variable at node

holds in (36) for maximum portfolio value. Define the drawdown random variable at node ![]() by

by ![]() , i.e.,

, i.e.,

Our drawdown risk metric is determined with respect to a prescribed level of acceptable relative drawdown in the portfolio, herein denoted by the (nonnegative) fraction π. Thus, the DDR metric, denoted by ![]() , takes on value zero if

, takes on value zero if ![]() , and it is positive otherwise. Therefore, defining the ($) violations from the acceptable level of drawdown by

, and it is positive otherwise. Therefore, defining the ($) violations from the acceptable level of drawdown by ![]() ,

,

The drawdown (quadratic) risk metric is then

Therefore, the nodal trade optimization problem with drawdown risk control at node ![]() has the objective

has the objective

where the function ![]() is defined in (7), and

is defined in (7), and ![]() is herein termed a (dynamic) drawdown risk aversion (DRA) coefficient, which is nonnegative. The constraints that must be imposed to determine the drawdown risk correctly are

is herein termed a (dynamic) drawdown risk aversion (DRA) coefficient, which is nonnegative. The constraints that must be imposed to determine the drawdown risk correctly are

where ![]() must satisfy the following linear constraints along the scenario path up to node

must satisfy the following linear constraints along the scenario path up to node ![]()

The drawdown constraints in (41)-(42) are free of the drawdown variables ![]() in (37). Moreover, the constraints (41) must be imposed along each scenario outcome descendant from node

in (37). Moreover, the constraints (41) must be imposed along each scenario outcome descendant from node ![]() , i.e., for all

, i.e., for all ![]() ,

, ![]() , which thus makes the computation of the risk metric

, which thus makes the computation of the risk metric ![]() directly dependent on the generated scenario tree of security returns.

directly dependent on the generated scenario tree of security returns.

5 Multistage portfolio rebalancing model

In the preceding two sections, the basic constructs of the model for the portfolio rebalancing problem were discussed, as viewed from a given rebalancing decision node ![]() of the scenario tree. In this section, these model components are collected to construct the multistage dynamic rebalancing stochastic programming model, which allows the manager to determine the optimized portfolio positions at the root node

of the scenario tree. In this section, these model components are collected to construct the multistage dynamic rebalancing stochastic programming model, which allows the manager to determine the optimized portfolio positions at the root node ![]() . Indeed, it is the optimal security positions

. Indeed, it is the optimal security positions ![]() , revised from the initial positions

, revised from the initial positions ![]() , that will be implemented, considering the anticipated future of T periods as depicted by the generated scenario tree of security returns.

, that will be implemented, considering the anticipated future of T periods as depicted by the generated scenario tree of security returns.

At each rebalancing node ![]() , define the value function

, define the value function ![]() , which is the optimal objective value after undertaking the optimized portfolio rebalancing.

, which is the optimal objective value after undertaking the optimized portfolio rebalancing. ![]() depends on the information available prior to initiating portfolio rebalancing, i.e., portfolio holdings

depends on the information available prior to initiating portfolio rebalancing, i.e., portfolio holdings ![]() , cash position