Chapter 3

Guest accounting

Introduction

It is the responsibility of front office to prepare the guest's bill, present it, and ensure that it is paid. This involves a lot of record keeping, for a guest may incur a large number of separate charges during his stay, from the cost of the room and various meals through to telephone, laundry and entertainment charges.

The process is complicated by the fact that the hotel industry traditionally gives a guest credit during his stay. The amounts involved can be quite substantial: a room for one night coupled with an evening's business entertaining in a top city centre hotel can come to several hundred pounds. In contrast to many other businesses, this credit often has to be extended to relative unknowns at short notice.

There is also the question of speed. Details of the various transactions must be collected from different departments of the hotel and put onto the guest's bill before he leaves, which is often quite early in the morning. An item omitted is very difficult to recover afterwards, not least because the guest may well live in another legal jurisdiction.

Guest accounting is thus both complex and sensitive. In large hotels it is usually the responsibility of a separate billing or accounting section, with the settlement process being the responsibility of a cashier. In smaller hotels the duties generally have to be combined. Wherever you work, you are likely to find yourself undertaking them at some time, and you need to understand the principles involved.

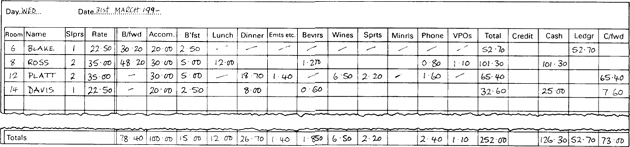

Figure 31 Horizontal tabular ledger

The objectives of the guest accounting procedures are as follows:

![]() To maintain accurate and up-to-date guest accounts.

To maintain accurate and up-to-date guest accounts.

![]() To ensure that payment is received promptly and in full.

To ensure that payment is received promptly and in full.

![]() To provide management with accurate and up-to-date financial reports.

To provide management with accurate and up-to-date financial reports.

We shall be looking at the third objective later on. This chapter is therefore divided into two parts.

Billing systems

There are three main methods of preparing guest bills:

1 The tabular ledger.

2 Mechanical or electronic billing machines.

3 Computerized guest accounting systems.

We shall look at each in turn.

The tabular ledger

This is the oldest and most labour-intensive of the methods. It is still typical of smaller hotels which use manual systems.

The tabular ledger provides a record of all charges incurred by guests during a twenty-four-hour period, analysed according to their nature. A typical layout is shown in Figure 31.

The tab produces:

![]() A record of all charges, credits, payments and outstanding balances.

A record of all charges, credits, payments and outstanding balances.

![]() A separate total for each guest's bill.

A separate total for each guest's bill.

![]() A separate total for each category of item.

A separate total for each category of item.

It is completed as follows:

1 You start by entering all the guests staying over from the previous day. Each individual or family unit requires a separate row. ‘NAME’ and ‘ROOM’ should be self-explanatory. ‘SLPRS’ means ‘sleepers’. It is important to note these on the tab sheet because some charges may be on a ‘per person’ rather than a ‘per room’ basis. The ‘RATE’ agreed should be noted because this helps to prevent over or undercharging. The entries are usually made in room number order. This helps you to find the correct row when entering charges from the departmental vouchers, most of which are marked with the room number rather than the guest's name.

2 Then you bring forward any outstanding charges from the preceding day, and enter these under the heading ‘B/FWD’. Remember that each tab sheet covers one day only, and that guests may have incurred a number of such charges already. These items will be found on the preceding day's tab sheet.

3 Next, enter all the room charges under ‘ACOM’. They may not be the same as the figure in the ‘RATE’ column because many hotels offer inclusive packages (i.e. one charge to cover both room and table d'hôte meals). This charge needs to be split up for accounting purposes, so ‘ACOM’ means the room rate component of the overall charge. Room charges for guests in residence are normally entered at a set time, such as 9 p.m.

4 Enter the various other charges as they come through. This spreads the work out and keeps the bill and tab up to date. In manual systems, all such charges are recorded on ‘checks’ or ‘vouchers’, which originate in the department providing the service and are then passed to the bill office to be ‘posted’ to (i.e. entered on) the tab. It is essential that this is done systematically, and that the vouchers are cancelled as soon as the entries have been made.

– Charges such as ‘BREAKFAST’, ‘LUNCH’ and ‘DINNER’ are self-explanatory. Meals included in inclusive rates should be detailed here.

– ‘BAR’ and ‘PHONE’ are also self-explanatory. There may be more than one entry per guest against these headings, and some tab layouts allow two or more lines for them. Others also provide one or more blank columns which allow you to detail any unusual items.

– ‘VPOS’ (‘visitor paid outs’) cover any ‘disbursements’, i.e. payments made by the hotel on behalf of the guest. You may have to send someone out for toilet articles, for instance, or pay for a COD (cash on delivery) package. These payments have to be recovered from the guest before he leaves.

5 When a new guest arrives you should begin a new row, even if he is occupying a room vacated earlier. This means that you might have two rows with the same room number on the tab sheet. The room charge is entered as the account is opened, and any other charges are added as the vouchers come through.

6 Enter any ‘CREDITS’ (often called ‘allowances’) as and when they arise. These allow you to make any necessary adjustments. If a breakfast charge is wrongly posted to Room 105 instead of Room 150, for example, it will have to be cancelled. It is good practice to maintain an adjustments and allowances book, in which full details of every such entry must be recorded. This should be inspected by management regularly.

7 When a guest checks out, he will settle his bill:

– The ‘CASH’ column records any payments he makes. ‘Cash’ means any ‘bankable’ forms of payment, such as cash itself, cheques, travellers’ cheques or credit cards (e.g. MasterCard or Visa).

– ‘LEDGER’ covers any arrangement whereby the hotel claims back the amount of the guest's bill from someone else. Many group bookings are settled in this way. Obviously, some form of authorization is necessary before an account is transferred to ledger. ‘Ledger’ also covers what are called ‘travel and entertainment company’ credit card payments (e.g. American Express or Diners) and travel agent coupons, because these require you to send a statement to the card company or agent in order to obtain payment.

– It is customary to put a line through any unused portion of the row relating to a guest who has checked out. This prevents any further charges being mistakenly entered in that space.

8 Not all guests will be leaving. The ‘C/FWD’ column allows you to ‘carry forward’ the total of all charges incurred to date. The total will be identical to the ‘B/FWD’ figure for the following day, though the items will not be in exactly the same order because you will be rearranging the stopover guests in room number order.

9 The tab sheet must be ‘balanced’ before it can be accepted as correct. This means adding up all the columns and all the rows. They must come to the same total both ways, thus providing a check on the arithmetical accuracy of the records. The usual time for balancing the tab is some time after 11 p.m., during the quiet period sometimes known as ‘the graveyard shift’. This allows you to check the rows for any guests departing the following morning and to make sure that their ‘TOTALS’ are correct. If the nightly rate is inclusive of breakfast, no further entries should be necessary, unless the guest has papers or an early morning tea. These would have to be added before the bill was presented.

It should be obvious that the ‘guest’ row on the tab sheet contains exactly the same items as the guest's own bill. In very old-fashioned systems these two documents were produced separately, mainly because it was easier to add up both vertically in the days before hand calculators became common. Later, a number of patent systems were introduced to allow both to be completed simultaneously, thus reducing the number of entries required and the possibility of transcription errors. These systems required the bill to be superimposed over the tab, with the duplication being achieved by the use of NCR (no carbon required) paper.

Since bills almost invariably show the items in columnar form (making it easier for the guest to check that the total is correct), this development required an alternative ‘vertical’ method of presentation for the tab sheet. The horizontal rows were now used for the different categories of bill item. These had to be added across before the tab could be balanced, but this process became easier after the introduction of calculators.

A ‘vertical’ tab with superimposed bill is shown in Figure 32. Various ingenious methods were devised to make sure that the bill could be placed over the right column. Each day's bill would require a separate sheet.

Electro-mechanical or electronic billing machines

The hand-written tab remains suitable for small hotels. However, the need to handle large numbers of postings in larger establishments led to the introduction of various models of billing machines. Most of these have now been replaced by computerized guest accounting systems, but you may still find them in operation, or standing by ready for use as a back-up system (one of the advantages of an electromechanical machine is that it can always be operated by turning a handle even if the power goes off).

Figure 32 Vertical tabular ledger with bill superimposed

The billing machine does exactly the same job as the patent bill and tabular ledger combinations we looked at in the last section, but it handles the tab function by ‘storing’ the various charges in ‘registers’ (memories). The guest bill remains much the same, but the tab itself is replaced by a ‘summary sheet’ which simply shows the totals for the various types of charges and allowances. Since the transactions are also listed on an ‘audit roll’, it is possible to check these in detail should this be necessary.

Billing machines offer the following advantages:

![]() All bill entries are simultaneously recorded in the machine's memory and all additions and subtractions are handled automatically. This means that bill and ledger totals are always in agreement, though it is still possible to enter a charge incorrectly.

All bill entries are simultaneously recorded in the machine's memory and all additions and subtractions are handled automatically. This means that bill and ledger totals are always in agreement, though it is still possible to enter a charge incorrectly.

![]() Bills are printed rather than hand-written. In theory, this makes them more legible, though customers trying to puzzle out a bill containing a lot of cryptic abbreviations and produced on a machine with a faded print ribbon might not agree.

Bills are printed rather than hand-written. In theory, this makes them more legible, though customers trying to puzzle out a bill containing a lot of cryptic abbreviations and produced on a machine with a faded print ribbon might not agree.

![]() Charge vouchers are machine-cancelled automatically. This cuts down the risk of vouchers being posted twice (or not posted at all).

Charge vouchers are machine-cancelled automatically. This cuts down the risk of vouchers being posted twice (or not posted at all).

![]() Control is easier. Since bill and ledger totals are always in agreement, the control procedures at the end of a shift are considerably simplified.

Control is easier. Since bill and ledger totals are always in agreement, the control procedures at the end of a shift are considerably simplified.

There are certain corresponding disadvantages, mainly centred on the training time necessary to produce a competent operator, which is likely to be about a week. Of course, learning how to complete a manual tab also takes time.

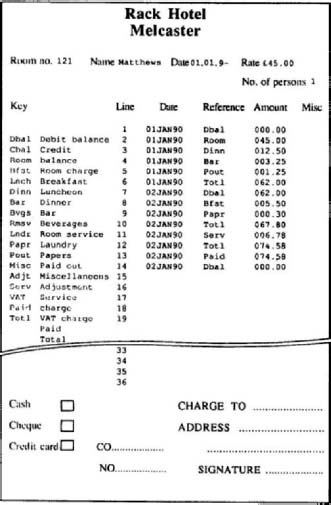

The guest bill produced by a billing machine is usually known as the ‘guest folio’. The most common layout is the columnar one shown in Figure 33.

Guest folios are normally completed in duplicate. The upper portion is the guest bill, while the lower portion is the hotel's duplicate record. This lower portion is usually made of thin card rather than paper. This enables the folio as a whole to stand upright in a guest folio rack (often called the ‘bucket’) which is kept beside the billing machine. The room number is usually shown prominently at the top of the folio, which helps the machine operator to keep the folios in room number order.

The procedures for dealing with a guest folio vary in detail from machine to machine, but will generally follow the following sequence:

1 When a guest arrives, the operator types the guest's name, address, room number, date of arrival, rate and number of persons on a blank folio card (few billing machines have full alphabetic keyboards, so this step has to be done separately).

2 The folio is then placed on the billing machine's ‘platform’ (a kind of horizontal tray projecting from the front). Once inserted, the folio cannot be removed until the sequence of entries has been completed. This acts as a safeguard when (as often happens) the operator is interrupted halfway through the posting process.

3 The folio is opened by entering the room number and the opening balance. That will be zero unless a deposit has been paid. Some systems allocate a reference number at this point: this will remain in force for that room number until cancelled by a final payment or transfer to ledger.

4 The first charge posted will usually be the room rate. The others will be entered from vouchers, just as with the tab. All postings are made in the same way. The folio and the voucher are placed side by side on the ‘platform’. The operator enters the room number and the ‘pick-up’ figure, if any. This is always the last balance to be shown on the folio: you can see that in our example the balance at the end of 1 January was £62.00, and that this has been ‘picked up’ again on the following morning. Once the entry has been made, the billing machine:

– Prints the item on the bill and duplicates it on the folio below.

– Prints the same item (with the relevant room number) on an ‘audit roll’, which can be checked back against the vouchers if necessary.

– Calculates a new balance.

– Cancels the voucher by overprinting it.

5 It should be obvious that if you put a folio which already contains a number of items into the billing machine, it may overprint the existing entries. The ‘line’ column allows the operator to select the line at which new printing will commence.

6 At the end of the shift, the billing machine is balanced. This is usually done by inserting a special key known as the ‘X key’ into the machine and putting a summary sheet on the ‘platform’. The calculation is then as follows:

– Balances brought forward (entered from last summary sheet)

– Plus total debits (maintained by machine)

– Minus total credits (also maintained by machine)

– Should equal total balances carried forward (this figure is obtained by add-listing the last figures shown in all the folios).

7 Since all the calculations are done automatically, balancing is easier than with the manual tab. However, there can still be errors, especially those caused by ‘picking up’ an incorrect balance, which is why the process is necessary. Even this does not guard against certain common types of mistake, such as posting the right amount to the wrong folio, or the wrong amount to the right folio, or labelling a charge wrongly, or omitting it altogether.

8 Once the transactions have been balanced, the operator prints out the totals of all the different charges onto a summary card. The machine's memory is then ‘cleared’ or reset to zero. This is done by inserting another special key known as the ‘Z key’, which is usually held by a senior employee.

9 When the guest is about to leave, the operator puts the appropriate folio onto the ‘platform’ and enters any last minute charges. Then she enters the payment, or alternatively makes an entry to show that the outstanding account has been transferred to a ledger account. Many machines will automatically print a receipt on the top (guest's) copy of the folio at this point.

Figure 33 Guest bill produced by billing machine

Billing machines vary in detail, but most have individual keys for the main types of charge, numerical keys to enter the amounts, and special keys such as ‘PICK UP DEBIT BALANCE’, ‘PICK UP CREDIT BALANCE’, ‘ENTER LINE’, etc. The initial impression produced by all these different keys can be somewhat overpowering, but their use quickly becomes familiar with experience.

Computerized billing systems

These represent a further major advance in terms of speed and efficiency. Computers offer all the advantages of billing machines, with a number of additional ones, as follows:

1 A further reduction in the number of entries. Whereas the billing machine stores all the transactions arising in a single shift, the computer can store them throughout the duration of a guest's stay. This means that the tedious process of selecting the correct folio, inserting it in the billing machine, picking up the old balance, entering a batch of transactions and then replacing the folio in the bucket can be eliminated. Since the guest's account is maintained electronically in the computer's memory, all that you have to do is call it up on-screen and add whatever details are necessary. In addition, computers have full alphanumeric keyboards rather than the more limited ‘cash register’ type characteristic of billing machines.

2 Reductions in the number of vouchers. It is possible to connect the central computer to any number of point of sale (POS) terminals, so that charges can be ‘inputted’ directly by the departments concerned, rather than them preparing vouchers which must then be physically transferred to the bill office before being entered on the guest's folio.

3 Easier access to bills. With a computerized system, it is possible for guests to see their bills anywhere and at any time, as long as they have access to a TV screen, such as the one in their room. This allows them to be checked the evening before they leave, thus permitting ‘express check-outs’ and helping to reduce the post-breakfast bottleneck so characteristic of large and busy hotels.

4 Greater detail. It is possible for a computerized bill to show the precise times at which various charges were incurred. This helps to reduce disputes.

5 Even greater accuracy. Arithmetical accuracy can be taken for granted, but computers can also be programmed to check whether entries are within sensible ranges. They can be made to charge the normal rack rate for a room unless instructed otherwise, and to do so automatically on room allocation. They can also ‘pick up’ deposits automatically. All these facilities help to reduce the kinds of operator errors which still afflict machine-produced guest accounts.

Nevertheless, computers are not yet perfect. They are much more complex than the simple handwritten tab or the relatively primitive billing machine, and this leads to two disadvantages:

1 The operators need more training time.

2 The systems are more prone to breakdowns.

This second drawback means that it is still necessary to produce a written ‘audit trail’ so that the accounts can be recreated from scratch in the event of a computer failure. This in turn implies that there should be a back-up system of some kind.

An ‘audit trail’ is also necessary because computer operators are still liable to make incorrect entries, such as charging an item to the wrong room. We shall look at this point again when we consider control.

There are many different types of computerized system available, and we can expect to see more coming onto the market. These systems vary in detail, and it would be absurd to single out just one, or to attempt to describe all the features it might include. The manuals tend to be a hundred or more pages long, and the typical training period a week to ten days. However, most systems will have certain features in common:

1 There will generally be a ‘CASHIER’ or ‘BILLING’ module available. Once you enter this, the system will prompt you to enter the appropriate room number. In many cases you can use the guest's name as an alternative. In either case the system will display the other item to allow you to crosscheck.

2 The system will prompt you to tell it whether you are making a posting, an adjustment or a transfer (postings are bill entries, adjustments are corrections of various kinds, while a transfer facility is necessary because bill items or accounts are sometimes paid by other guests). The computer has to be ‘told’ this because it can't read your mind. It is the equivalent of your choosing the appropriate row or column on the tab.

3 The system will then prompt you for the type of item to be entered. Most will simplify this process as far as possible by using numerical codes or the function keys (the ones at the top on a standard IBM keyboard). Their use quickly becomes automatic, but the system will generally display the available codes for reference, or at least contain a ‘HELP’ function so that you can consult them.

4 Many postings will be made automatically. The computer will have asked you for the room rate when you registered the guest. If you ‘skipped’ this field, it will automatically post the standard rack rate, and it will continue to update this automatically for every additional night (no more forgetting to post room charges on the tab or billing machine folio!). These automatic postings may be known as ‘system’ entries or some similar term. If you discover that the rate is in fact wrong, you can always correct it by an adjustment, though there needs to be a written record in order to provide the necessary ‘audit trail’.

5 You will usually find that you are required to enter an ID (identification) code at some point in the process. This is equivalent to your initialling a form or voucher, and is desirable for control purposes.

6 The system may or may not display the guest's folio at this point. If it doesn't, it will still check that the guest's credit limit has not been exceeded, and display a warning message if it has.

Even if the folio is not displayed, you can always call it up from the menu. As Figure 34 shows, it will generally look very much like the printed version.

Methods of payment

Guests can settle their accounts in a variety of ways, namely:

![]() cash

cash

![]() cheque

cheque

![]() Eurocheque

Eurocheque

![]() foreign currency

foreign currency

![]() travellers’ cheque

travellers’ cheque

![]() credit card

credit card

![]() ‘switch’ card

‘switch’ card

![]() travel agent voucher

travel agent voucher

![]() transfers to ledger account

transfers to ledger account

Let us consider each of these in turn.

Cash

Although travellers no longer carry purses full of gold coins to pay their reckonings with, cash is still the only ‘legal tender’, and a hotelier could insist on payment in notes and coin if he so wished. In fact, cash has long been obsolete as a means of payment, partly because the amounts involved can be quite considerable, and partly because of the inconvenience of having to make the payment long before the banks open. In fact, any hotel insisting on cash payments would probably lose a lot of business.

Figure 34 On-screen display of guest statement

Nevertheless, some guests do make payments by cash, and the cashier must be prepared for these. This means that the hotel must provide a ‘cash float’ to allow the cashier to give change, and the cash received must be stored safely until it can be banked. All this means that there must be adequate accounting records, and the cashier's section must be properly secured.

The bill should be receipted ‘paid by cash’. The issue of a receipt is particularly important in this case because the guest will have no other record of the payment.

Cheques

Most travellers now have bank accounts, and the use of cheques has grown enormously over the past few decades. Cheques are very convenient, since they can be made out there and then for any amount desired, but they have certain disadvantages as far as hotels are concerned.

The obvious ones are the fact that there will be a delay before the amount is credited to the hotel's account, and a small handling charge when it is. These drawbacks are common to all business concerns and are bearable. The real problem is the fact that guests are often complete strangers whose cheques may turn out to be ‘dud’.

In the past, this problem had to be dealt with by imposing a clause in the contract for accommodation to the effect that three days’ notice was required before the hotel would accept a cheque in settlement (this was usually long enough to allow the hotel to confirm the guest's creditworthiness). Nowadays most guests carry cheque guarantee cards, which guarantee anyone who accepts a cheque payment provided that:

![]() Only one cheque is used per transaction.

Only one cheque is used per transaction.

![]() That cheque is signed in the presence of the cashier.

That cheque is signed in the presence of the cashier.

![]() The bank code and signature on the cheque and guarantee card agree.

The bank code and signature on the cheque and guarantee card agree.

![]() The guarantee card is not past its expiry date.

The guarantee card is not past its expiry date.

![]() The card number is noted on the back of the cheque.

The card number is noted on the back of the cheque.

Unfortunately, most guarantees are limited, and a great many bills will come to more than the usual guaranteed amount. This limits the value of cheque guarantee cards as far as many hotels are concerned. However, there are now commercial agencies which will guarantee such cheques for you. In theory, you could also ask for a series of separate cheque payments on the grounds that each night's stay was a separate ‘transaction’.

If payment is made during normal banking hours, the hotel can verify that a cheque will be paid by telephoning its own bank, which will then ring the drawer's bank. This involves a charge, which will have to be borne by the hotel unless it passes it on to the guest. Needless to say, such guests are likely to resent the implied slur on their truthfulness, as well as the extra cost involved.

Even perfectly honest guests can make silly mistakes which will invalidate their cheques, and there are certain simple rules which should be followed whenever you accept one. You should check:

![]() That the date and year are correct. In particular, watch out for ‘postdated cheques’ (i.e. those with future dates) since these will not become payable until the date shown (by which time the account may have nothing in it) or ‘stale’ cheques (i.e. those made out over six months ago).

That the date and year are correct. In particular, watch out for ‘postdated cheques’ (i.e. those with future dates) since these will not become payable until the date shown (by which time the account may have nothing in it) or ‘stale’ cheques (i.e. those made out over six months ago).

![]() That the cheque has been made out to the correct payee.

That the cheque has been made out to the correct payee.

![]() That the amounts shown in words and figures agree.

That the amounts shown in words and figures agree.

![]() That any corrections have been properly signed.

That any corrections have been properly signed.

![]() That the signature is the same as that on the cheque guarantee card. If in doubt, ask for some other form of identification, such as a passport or driver's licence.

That the signature is the same as that on the cheque guarantee card. If in doubt, ask for some other form of identification, such as a passport or driver's licence.

Eurocheques

Eurocheques allow customers to make payments in the local currency (i.e. pounds, euros, francs, deutschmarks, etc.). They are debited to the customer's account in his own currency at whatever the rate of exchange was when the cheque was presented for payment.

Figure 35 (a) Sample cheque; (b) Sample cheque card (courtesy Abbey National)

Eurocheques are accompanied by a special cheque guarantee card known as a Eurocard. The rules are exactly the same as for ordinary cheque cards except that the amount guaranteed is usually higher, and any number of Eurocheques can be made out for one transaction.

This means that Eurocheques are preferable to ordinary cheques as far as hotels are concerned. If one cheque does not cover the full amount of the bill, the guest can write out a second, a third or a fourth. Providing that the various security checks reveal no inconsistency, such cheques are as good as cash. The security checks themselves are the same as for an ordinary cheque guarantee card.

Foreign currency

This is sometimes offered by foreign visitors, especially if they come from a country with a strong currency (indeed, there are stories of American visitors who simply didn't know that the dollar was not used everywhere). Such currencies present no problem, but others may be very difficult to convert into cash except at a substantial discount, and cashiers need to be careful about which to accept.

There is no obligation to accept any foreign currency since it is not legal tender, but there is an obvious goodwill aspect. Apart from this, hotels can often make a profit by doing so, especially if their rate of exchange is less favourable to the guest than that offered by the local banks. This is both legal and normal. The justification is that the unfavourable rates cover the extra cost of providing the service and also guard against the risk of a sudden fall in the banks’ rate (hotels are not expert foreign exchange dealers, after all). If a guest objects, he should be told that he is perfectly free to exchange his currency elsewhere.

Some large hotels apply for registration as authorized foreign exchange dealers. This imposes certain obligations on them, but they do it in order to be able to provide an additional service for their international clientele. Cashiers in such hotels have to observe currency regulations and must be aware of current rates of exchange, which may change daily or even hourly.

If a hotel is NOT registered as a foreign exchange dealer, it can only receive foreign currency, not sell it. This means that it would be illegal to give change in it, even if the guest requested this.

Cashiers need to be able to recognize the major foreign currency notes in order to avoid the risk of being tricked by relatively crude forgeries (it is not normal practice to accept foreign coins). In larger hotels there should be a notice board showing the current exchange rates as set by head office or the chief cashier. Smaller hotels can deal with this problem on the ‘exception principle’, namely by checking with their bank or even a daily newspaper whenever the need arises.

Foreign currency accepted in payment of a guest's bill should be recorded at the value set on it by the hotel. This may be either higher or lower than the amount finally credited to the hotel's account by the bank when it is paid in (though it will usually be higher for the reasons already given). This ‘profit or loss on foreign exchange’ is shown as a separate item in the hotel's accounts: in other words, it is treated as a purely financial transaction and not credited or debited to the guest's account.

Travellers’ cheques

Travellers’ cheques are issued by major banks and financial institutions in various major currencies and in fixed denominations, such as £10, £20 and £50, or $10, $20 and $50. Those in foreign currencies can be offered as payment or converted into the local money like foreign exchange.

Customers have to sign their travellers’ cheques when they are issued, but they do not become valid until they are signed a second time in the presence of the receiving cashier. Once properly signed, the cheque becomes the equivalent of cash and is treated as such in the accounts.

Travellers’ cheques bear a service charge which is used to defray the cost of administration and to cover additional insurance against accidental loss or theft. This charge is paid by the customer. As far as the hotel is concerned, travellers’ cheques only incur the same handling charges as ordinary cheques, though they offer greater security.

Since travellers’ cheques bear the original purchaser's signature, a skilful forger can easily convert stolen cheques to his own use, so it is common to ask for additional documentary evidence of identity, such as a passport. Lists of lost or stolen travellers’ cheques are circulated regularly to hotels, and cashiers should check these before accepting any such cheques.

Cashiers receiving travellers’ cheques in payment should observe certain simple rules:

![]() Check the denomination and work out the exchange value, if any.

Check the denomination and work out the exchange value, if any.

![]() Check that the date and payee entries are correct.

Check that the date and payee entries are correct.

![]() Insist that the traveller's cheque is signed in your presence, and then compare the two signatures.

Insist that the traveller's cheque is signed in your presence, and then compare the two signatures.

![]() Check the cheque number against the current stop list.

Check the cheque number against the current stop list.

It is also common practice to note the room number on the reverse side, just in case there are any queries later.

Credit cards

Credit cards now represent one of the main methods by which bills are settled (so much so, indeed, that many American hotels now regard guests offering to pay by cash with some suspicion) .

Credit cards are issued by the major banks, who are affiliated to either the MasterCard or Visa networks, or else by major travel and entertainment organizations such as American Express (Amex) and Diners Club International (Diners). The terms and conditions upon which they are issued vary somewhat, but this need not concern the cashier. What is important is that the issuing organization issues a franchise to the hotel, entitling it to accept card payments in exchange for services offered.

This franchise includes a ‘floor limit’, which restricts the amount the hotel can accept any one card for without special authorization. This floor limit will be bigger for large hotels than for smaller ones. It is quite independent of the cardholder's credit limit. If a bill exceeds the floor limit, the cashier must obtain authorization by calling a toll-free number.

The issuing organizations guarantee payment of all bills run up by the holder up to his credit limit. This limit is almost always much higher than the cheque card one, which makes the credit card a very useful means for settling hotel bills.

Unfortunately, credit card fraud is widespread, and cashiers have to be vigilant, since ‘payments’ made on the basis of an invalid card will not be honoured by the issuing company. Rewards are paid for recovery of lost or stolen cards.

The older procedure for dealing with credit card payments is as follows:

![]() The customer hands over his card and the cashier checks that it bears the correct name and a valid expiry date.

The customer hands over his card and the cashier checks that it bears the correct name and a valid expiry date.

![]() The cashier also checks the card against the card company's current ‘stop’ list.

The cashier also checks the card against the card company's current ‘stop’ list.

![]() The cashier checks that the amount is not over the floor limit.

The cashier checks that the amount is not over the floor limit.

![]() The cashier makes out a sales voucher, usually in triplicate, and enters the authorization number (if any).

The cashier makes out a sales voucher, usually in triplicate, and enters the authorization number (if any).

![]() The cashier then uses a special machine (called an ‘imprinter’) to make an imprint of the card on the sales voucher.

The cashier then uses a special machine (called an ‘imprinter’) to make an imprint of the card on the sales voucher.

![]() This done, the customer signs the voucher with a ballpoint pen. The signature must be checked against that on the card. This done, the customer is given a copy of the voucher plus his card back.

This done, the customer signs the voucher with a ballpoint pen. The signature must be checked against that on the card. This done, the customer is given a copy of the voucher plus his card back.

![]() Finally, the cashier should offer to destroy any carbon paper used in the preparation of the voucher (this is because it bears both the card number and a copy of the signature and could be passed on to a third party by an unscrupulous cashier).

Finally, the cashier should offer to destroy any carbon paper used in the preparation of the voucher (this is because it bears both the card number and a copy of the signature and could be passed on to a third party by an unscrupulous cashier).

Nowadays, much of this process is being replaced by a simple card ‘swipe’ through an electronic point of sale terminal which carries out the checking process electronically and authorizes payment. The customer still needs to sign a printed voucher for the payment to be valid.

All credit card companies deduct commission before the final payment is made. However, the procedures for dealing with them differ. Vouchers for bank-issued cards like Access and Visa are simply paid into the hotel's bank and are cleared like ordinary cheques. The only difference is that you have to use a separate paying-in slip, and your bank deducts the card company's commission before crediting the hotel's account. Travel and entertainment card vouchers such as Diners or American Express are collected together and sent off in batches to the respective companies for payment. This process takes longer than with the bank-issued cards, though the companies claim that the delay is seldom more than two or three days.

Switch cards

This type of ‘smart’ card is increasing in importance. They resemble cash cards in that they allow holders to make payments directly from their current accounts to establishments equipped with appropriate terminals. Hotels thus equipped can have the money paid directly into their own accounts without delay. The advantages are obvious, though cardholders have to sign a sales voucher and this still has to be forwarded to their bank to provide a written record.

Switch cards are likely to be used in other ways, too. One possibility is that they might replace the present electronic room key (receptionists would pass the card through a reader which would automatically program the door lock to respond to that particular magnetically coded number), or be used to record and pay for hotel mini bar purchases.

Travel agents’ vouchers

Many guests present travel agents’ vouchers in whole or part payment of their bills. These vary much more than the other forms of payment we have been considering, and need to be examined carefully.

Travel agents’ vouchers arise when the guest pays the agency for his food and accommodation in advance. The agency then prepares two copies of the voucher. One copy goes to the hotel to confirm the booking, and the other is given to the guest for him to present to the hotel when he registers.

The cashier should have the first copy of the voucher as part of the reservation documents. When the guest arrives and presents his copy, she should compare the two to make sure that there have been no alterations. She should also make sure that she knows exactly what the voucher covers, and whether there are likely to be any ‘extras’ (laundry, for instance, or bar bills). If there are, she should open an ‘extras’ bill and make sure that the guest understands the arrangement. Guests are normally asked to sign their bills to show that they have actually stayed at the hotel and incurred the charges stated.

Not all vouchers actually show the price agreed, so this may have to be established from other documents. The vouchers are then collected and sent off to the travel agents for payment.

Special problems arise when dealing with overseas travel agents. Since payment will be delayed, there is always the possibility of a loss on foreign exchange. It is sensible practice to require that payment be made in sterling. This means that it is the travel agent who has to accept the risk.

Group tours organized by travel agents are often paid for by group vouchers. The principle is exactly the same, but the tour courier is generally expected to agree the number of persons, meals and so forth prior to departure. Individual ‘extras’ bills are likely with this kind of business, and it is the cashier's task to make sure that these are presented and paid by the guests.

Transfers to ledger account

Large companies responsible for a lot of bookings find it tiresome to make separate payments. In such cases it is more sensible for the hotel to transfer the amounts to accounts in the general debtors ledger and then invoice the companies at regular intervals (usually monthly). This allows them to settle a number of fairly small debts with one cheque or bank transfer. It also reduces the cash-handling task for the hotel at the expense of a little extra book-keeping.

Disputed bills, discounts and refunds

Sometimes a guest objects to a bill, either because the amount is not what he agreed to pay, or because he has not received one or more of the items charged, or simply because he feels he has not had adequate service.

In such cases, the first thing to do is to take the guest aside and ask him (very politely) to wait while his complaint is investigated. Ideally, this task should be handled by a senior member of staff. Unfortunately, the nature of the hotel's business being what it is, this is not always possible. It may be early in the morning, with the guest in a hurry to leave and the dispute centring upon items in a restaurant bill from the night before. In these circumstances, hotels often give cashiers discretion to strike off the contested item or items. The idea is that it is better to avoid creating an unfavourable impression in the minds of other guests by having a noisy argument with a guest at a busy period. In theory, the hotel could always write to the guest asking for payment if it found that it had been right all along. In practice, this hardly ever happens and the amount is simply written off.

Another possible cause for complaint is disturbance or inconvenience. Not all hotel rooms are ideally located, and by no means all guests are well behaved. A noisy party in a bar may keep some guests awake, while boisterous revellers staggering along a corridor at two o'clock in the morning may disturb others. While a guest must accept that he is sharing the hotel with others, some cases of disturbance can be so extreme that he is prevented from enjoying what he is paying for. In such circumstances the hotel should be prepared to make a reduction.

Such reductions or discounts are classed as ‘adjustments’, ‘allowances’ or ‘refunds’, and they must be recorded in the hotel's accounts as well as on the guest's bill. This is essential because otherwise the receipts figure will not agree with the amount due: it is easy to forget to do it because the guest is in a hurry and the most important thing may seem to be to make a quick hand-written correction on his copy of the bill and then speed him on his way.

The tab usually has a row or column for ‘allowances’, while computerized accounting systems will also have provision for this type of entry. It is desirable to obtain approval for any such reduction as quickly as possible, and some systems may require entry of a management code number to prove authorization. It is also a good idea to ask the guest to sign an adjustment/allowance slip and attach this to the hotel's copy of the final bill.

Assignments

1 Describe the type of guest accounting system you would expect to find in the Tudor Hotel.

2 Describe the type of guest accounting system you would expect to find in the Pancontinental Hotel.

3 Obtain specimens of the type of guest accounting documents and an outline of the procedures used at a selection of local hotels, and compare these with one another, relating their characteristics to the type of hotel involved.

4 Outline a training scheme for cashiers in a 100-bedroom hotel converting from a manual guest accounting system to a computerized one.

5 From the following information, prepare tabular ledger entries for the guests currently in residence, enter all the following transactions, and close and balance the ‘tab’ as at the end of the day's business, adding and reconciling all totals.

Tariff:

| Room and breakfast: | £25.50 (inclusive of breakfast £4.50) per person |

| Inclusive rate | £41.00 (inclusive of all meals £20.00) per person |

| Table d'hôte lunch | £4.75 |

| Table d'hôte dinner | £10.75 |

| Coffees/Teas | 60p per person |

Guests in residence:

| Room | Type | Name | Terms | B/Forward |

| 102 | Double | Mr/s Hughes | Inc | £106.80 |

| 111 | Single | Mr Booth | R&B | £30.25 |

| 205 | Double | Mr/s Sykes | Inc | £86.50 |

| 206 | Single | Dr Haines | R&B | £35.00 |

Transactions:

| 07.30 | Early morning teas to all residents Newspapers: 205 (35p), 111 (45p, 206 (35p) |

| 07.40 | Telephone calls: 205 (£1.50), 206 85p), 111 (£6.50). |

| 07.45 | Disbursements: 102 Laundry (£2.50), 206 Ticket (£12.50). |

| 08.00 | Breakfasts served to all residents. |

| 09.00 | Mr/s Sykes check out and pay in full by cash. Dr Haines checks out: account transferred to ledger. Mr/s Hughes pay £50 on account by cheque. |

| 10.00 | Mr Booth moves to Room 202 on R&B terms. |

| 11.00 | Morning coffees for 102 (two persons) and 202 (one person). |

| 13.00 | 102 two lunches plus cigar (£1.75), 202 one lunch plus beer (£1.20). |

| 15.30 | Adjustment: Mr Booth wrongly charged for lunch yesterday. |

| 17.30 | Arrival: Mr/s Cummings, Room 208 (Double), inclusive terms. |

| 18.45 | Arrival: Mr/s Jones, Room 100 (Double), R&B terms. |

| 21.30 | 100: Two dinners plus wine (£9.50), spirits (£6.25). 102: Two dinners plus wine (£7.75), cigar (£1.75). 202: One dinner plus beer (£1.60). 208: Two dinners plus wine (£9.95), cigar (£3.70). |

| 23.00 | Arrival: Mr Power, Room 103 (Single), inclusive terms. |

| 23.30 | Adjustment: Morning paper (35p) should be charged to 102 and not 206 as noted earlier. |