CHAPTER 19 Accounting for Income Taxes

LEARNING OBJECTIVES

After studying this chapter, you should be able to:

- Identify differences between pretax financial income and taxable income.

- Describe a temporary difference that results in future taxable amounts.

- Describe a temporary difference that results in future deductible amounts.

- Explain the purpose of a deferred tax asset valuation allowance.

- Describe the presentation of income tax expense in the income statement.

- Describe various temporary and permanent differences.

- Explain the effect of various tax rates and tax rate changes on deferred income taxes.

- Apply accounting procedures for a loss carryback and a loss carryforward.

- Describe the presentation of deferred income taxes in financial statements.

- Indicate the basic principles of the asset-liability method.

How Much Is Enough?

In the wake of the economic downturn due to the financial crisis, a number of companies and numerous banks reported operating losses. As you will learn in this chapter, the tax code allows companies that report operating losses to claim a tax credit related to these losses for taxes paid in the past (referred to as “carrybacks”) and to offset taxable income in periods following the operating loss (referred to as “carryforwards”). When companies use these offsets, they reduce income tax expense, which increases net income. For tax carryforwards, companies also record a deferred tax asset, which measures the expected future net cash inflows from lower taxable income in future periods.

Citigroup is a good example of a company that has used operating loss credits to reduce its tax bill. In 2008, it had deferred tax assets (DTAs) of $28.5 billion, which represented 80 percent of stockholders’ equity and nearly eclipsed the bank's market value of equity. Some analysts have raised concerns about Citi's DTAs and whether these assets will ever be realized by Citi. Why the concerns?

Well, in order to receive the tax deductions in future years, a company like Citigroup needs to be reasonably sure it will have taxable income in the future. In Citi's case, analysts predict that the struggling bank will need to earn $99 billion in taxable income over the next 20 years. Given that Citigroup recorded operating losses of $60 billion in 2008 and 2009, some are skeptical that the DTAs will be realized. As a result, market watchers are debating whether Citi should set up an allowance to reduce its deferred tax assets due to the possibility that the assets will not be realized. Not surprisingly, Citigroup has resisted setting up an allowance as it would reduce its DTAs and increase its income tax expense.

This accounting does not sit well with some market observers. As one critic noted, “Why should auditors, investors, regulators and others rely on Citigroup's projections … to justify the use (realizability) of their DTAs?” Former SEC chief accountant, Lynn Turner, agrees: “Citi's position defies imagination and logic. Instead of talking about making money, what Citi ought to do is to reserve for at least part of the deferred tax assets and reap the benefit of reducing the reserves once it actually makes money.”

![]() CONCEPTUAL FOCUS

CONCEPTUAL FOCUS

![]() INTERNATIONAL FOCUS

INTERNATIONAL FOCUS

- See the International Perspectives on pages 1119, 1128, 1137, 1140, and 1145.

- Read the IFRS Insights on pages 1175–1181 for a discussion of:

- Deferred tax asset (non-recognition)

- Statement of financial position classification

In response, Citigroup, which accumulated deferred tax assets partly because of its huge losses during the financial crisis, said it was “very comfortable with the recording of our deferred tax assets.” And some market analysts sided with the bank, remarking that Citi's accounts were not out of order due to a misstatement of its DTAs. The Citigroup debate has arisen because accounting standards on DTAs are vague, stating that an allowance is not needed if management believes it is “more likely than not” the company will earn enough taxable income in the future.

This debate over Citigroup's accounting highlights the extent to which management judgment plays an important role in the accounting for taxes. After studying this chapter, you should be better able to evaluate Citigroup's accounting as well as the other judgments inherent in the accounting for income taxes.

Sources: Adapted from J. Weil, “Citigroup's Capital Was All Casing, No Meat,” www.bloomberg.net (November 24, 2008); and F. Guerra and J. Eaglesham, “Citi Under Fire Over Deferred Tax Assets,” Financial Times (September 6, 2010).

PREVIEW OF CHAPTER 19

As our opening story indicates, the accounting for income taxes involves significant judgment. Investors need to be knowledgeable of the accounting provisions related to taxes to be able to evaluate these judgments. Thus, companies must present financial information to the investment community that provides a clear picture of present and potential tax obligations and tax benefits. In this chapter, we discuss the basic guidelines that companies must follow in reporting income taxes. The content and organization of the chapter are as follows.

FUNDAMENTALS OF ACCOUNTING FOR INCOME TAXES

Up to this point, you have learned the basic guidelines that corporations use to report information to investors and creditors. Corporations also must file income tax returns following the guidelines developed by the Internal Revenue Service (IRS). Because GAAP and tax regulations differ in a number of ways, so frequently do pretax financial income and taxable income. Consequently, the amount that a company reports as tax expense will differ from the amount of taxes payable to the IRS. Illustration 19-1 highlights these differences.

Pretax financial income is a financial reporting term. It also is often referred to as income before taxes, income for financial reporting purposes, or income for book purposes. Companies determine pretax financial income according to GAAP. They measure it with the objective of providing useful information to investors and creditors.

Taxable income (income for tax purposes) is a tax accounting term. It indicates the amount used to compute income taxes payable. Companies determine taxable income according to the Internal Revenue Code (the tax code). Income taxes provide money to support government operations.

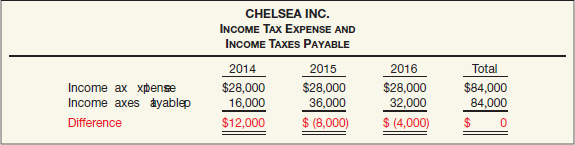

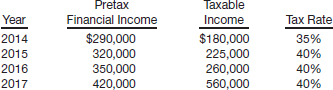

To illustrate how differences in GAAP and IRS rules affect financial reporting and taxable income, assume that Chelsea Inc. reported revenues of $130,000 and expenses of $60,000 in each of its first three years of operations. Illustration 19-2 shows the (partial) income statement over these three years.

For tax purposes (following the tax code), Chelsea reported the same expenses to the IRS in each of the years. But, as Illustration 19-3 shows, Chelsea reported taxable revenues of $100,000 in 2014, $150,000 in 2015, and $140,000 in 2016.

Income tax expense and income taxes payable differed over the three years but were equal in total, as Illustration 19-4 shows.

![]() International Perspective

International Perspective

In some countries, taxable income equals pretax financial income. As a consequence, accounting for differences between tax and book income is insignificant.

The differences between income tax expense and income taxes payable in this example arise for a simple reason. For financial reporting, companies use the full accrual method to report revenues. For tax purposes, they use a modified cash basis. As a result, Chelsea reports pretax financial income of $70,000 and income tax expense of $28,000 for each of the three years. However, taxable income fluctuates. For example, in 2014 taxable income is only $40,000, so Chelsea owes just $16,000 to the IRS that year. Chelsea classifies the income taxes payable as a current liability on the balance sheet.

As Illustration 19-4 indicates, for Chelsea the $12,000 ($28,000 − $16,000) difference between income tax expense and income taxes payable in 2014 reflects taxes that it will pay in future periods. This $12,000 difference is often referred to as a deferred tax amount. In this case, it is a deferred tax liability. In cases where taxes will be lower in the future, Chelsea records a deferred tax asset. We explain the measurement and accounting for deferred tax liabilities and assets in the following two sections.1

Future Taxable Amounts and Deferred Taxes

LEARNING OBJECTIVE ![]()

Describe a temporary difference that results in future taxable amounts.

The example summarized in Illustration 19-4 shows how income taxes payable can differ from income tax expense. This can happen when there are temporary differences between the amounts reported for tax purposes and those reported for book purposes. A temporary difference is the difference between the tax basis of an asset or liability and its reported (carrying or book) amount in the financial statements, which will result in taxable amounts or deductible amounts in future years. Taxable amounts increase taxable income in future years. Deductible amounts decrease taxable income in future years.

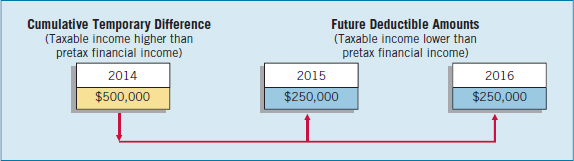

In Chelsea's situation, the only difference between the book basis and tax basis of the assets and liabilities relates to accounts receivable that arose from revenue recognized for book purposes. Illustration 19-5 indicates that Chelsea reports accounts receivable at $30,000 in the December 31, 2014, GAAP-basis balance sheet. However, the receivables have a zero tax basis.

What will happen to the $30,000 temporary difference that originated in 2014 for Chelsea? Assuming that Chelsea expects to collect $20,000 of the receivables in 2015 and $10,000 in 2016, this collection results in future taxable amounts of $20,000 in 2015 and $10,000 in 2016. These future taxable amounts will cause taxable income to exceed pretax financial income in both 2015 and 2016.

An assumption inherent in a company's GAAP balance sheet is that companies recover and settle the assets and liabilities at their reported amounts (carrying amounts). This assumption creates a requirement under accrual accounting to recognize currently the deferred tax consequences of temporary differences. That is, companies recognize the amount of income taxes that are payable (or refundable) when they recover and settle the reported amounts of the assets and liabilities, respectively. Illustration 19-6 shows the reversal of the temporary difference described in Illustration 19-5 and the resulting taxable amounts in future periods.

Chelsea assumes that it will collect the accounts receivable and report the $30,000 collection as taxable revenues in future tax returns. A payment of income tax in both 2015 and 2016 will occur. Chelsea should therefore record in its books in 2014 the deferred tax consequences of the revenue and related receivables reflected in the 2014 financial statements. Chelsea does this by recording a deferred tax liability.

Deferred Tax Liability

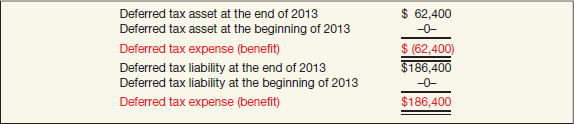

A deferred tax liability is the deferred tax consequences attributable to taxable temporary differences. In other words, a deferred tax liability represents the increase in taxes payable in future years as a result of taxable temporary differences existing at the end of the current year.

Recall from the Chelsea example that income taxes payable is $16,000 ($40,000 × 40%) in 2014 (Illustration 19-4 on page 1119). In addition, a temporary difference exists at year-end because Chelsea reports the revenue and related accounts receivable differently for book and tax purposes. The book basis of accounts receivable is $30,000, and the tax basis is zero. Thus, the total deferred tax liability at the end of 2014 is $12,000, computed as shown in Illustration 19-7.

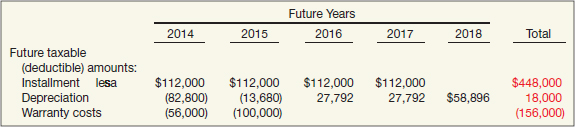

Companies may also compute the deferred tax liability by preparing a schedule that indicates the future taxable amounts due to existing temporary differences. Such a schedule, as shown in Illustration 19-8, is particularly useful when the computations become more complex.

Because it is the first year of operations for Chelsea, there is no deferred tax liability at the beginning of the year. Chelsea computes the income tax expense for 2014 as shown in Illustration 19-9.

This computation indicates that income tax expense has two components—current tax expense (the amount of income taxes payable for the period) and deferred tax expense. Deferred tax expense is the increase in the deferred tax liability balance from the beginning to the end of the accounting period.

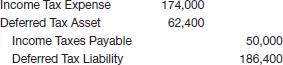

Companies credit taxes due and payable to Income Taxes Payable, and credit the increase in deferred taxes to Deferred Tax Liability. They then debit the sum of those two items to Income Tax Expense. For Chelsea, it makes the following entry at the end of 2014.

![]()

At the end of 2015 (the second year), the difference between the book basis and the tax basis of the accounts receivable is $10,000. Chelsea multiplies this difference by the applicable tax rate to arrive at the deferred tax liability of $4,000 ($10,000 × 40%), which it reports at the end of 2015. Income taxes payable for 2015 is $36,000 (Illustration 19-3 on page 1119), and the income tax expense for 2015 is as shown in Illustration 19-10 (page 1122).

Chelsea records income tax expense, the change in the deferred tax liability, and income taxes payable for 2015 as follows.

![]()

The entry to record income taxes at the end of 2016 reduces the Deferred Tax Liability by $4,000. The Deferred Tax Liability account appears as follows at the end of 2016.

The Deferred Tax Liability account has a zero balance at the end of 2016.

What do the numbers mean? “REAL LIABILITIES”

Some analysts dismiss deferred tax liabilities when assessing the financial strength of a company. But the FASB indicates that the deferred tax liability meets the definition of a liability established in Statement of Financial Accounting Concepts No. 6, “Elements of Financial Statements” because:

- It results from a past transaction. In the Chelsea example, the company performed services for customers and recognized revenue in 2014 for financial reporting purposes but deferred it for tax purposes.

- It is a present obligation. Taxable income in future periods will exceed pretax financial income as a result of this temporary difference. Thus, a present obligation exists.

- It represents a future sacrifice. Taxable income and taxes due in future periods will result from past events. The payment of these taxes when they come due is the future sacrifice.

A study by B. Ayers indicates that the market views deferred tax assets and liabilities similarly to other assets and liabilities. Further, the study concludes that the FASB rules in this area increased the usefulness of deferred tax amounts in financial statements.

Source: B. Ayers, “Deferred Tax Accounting Under SFAS No. 109: An Empirical Investigation of Its Incremental Value-Relevance Relative to APB No. 11,” The Accounting Review (April 1998).

Summary of Income Tax Accounting Objectives

One objective of accounting for income taxes is to recognize the amount of taxes payable or refundable for the current year. In Chelsea's case, income taxes payable is $16,000 for 2014.

A second objective is to recognize deferred tax liabilities and assets for the future tax consequences of events already recognized in the financial statements or tax returns. For example, Chelsea sold services to customers that resulted in accounts receivable of $30,000 in 2014. It reported that amount on the 2014 income statement, but not on the tax return as income. That amount will appear on future tax returns as income for the period when collected. As a result, a $30,000 temporary difference exists at the end of 2014, which will cause future taxable amounts. Chelsea reports a deferred tax liability of $12,000 on the balance sheet at the end of 2014, which represents the increase in taxes payable in future years ($8,000 in 2015 and $4,000 in 2016) as a result of a temporary difference existing at the end of the current year. The related deferred tax liability is reduced by $8,000 at the end of 2015 and by another $4,000 at the end of 2016.

In addition to affecting the balance sheet, deferred taxes impact income tax expense in each of the three years affected. In 2014, taxable income ($40,000) is less than pretax financial income ($70,000). Income taxes payable for 2014 is therefore $16,000 (based on taxable income). Deferred tax expense of $12,000 results from the increase in the Deferred Tax Liability account on the balance sheet. Income tax expense is then $28,000 for 2014.

In 2015 and 2016, however, taxable income will exceed pretax financial income, due to the reversal of the temporary difference ($20,000 in 2015 and $10,000 in 2016). Income taxes payable will therefore exceed income tax expense in 2015 and 2016. Chelsea will debit the Deferred Tax Liability account for $8,000 in 2015 and $4,000 in 2016. It records credits for these amounts in Income Tax Expense. These credits are often referred to as a deferred tax benefit (which we discuss again later on).

Future Deductible Amounts and Deferred Taxes

LEARNING OBJECTIVE ![]()

Describe a temporary difference that results in future deductible amounts.

Assume that during 2014, Cunningham Inc. estimated its warranty costs related to the sale of microwave ovens to be $500,000, paid evenly over the next two years. For book purposes, in 2014 Cunningham reported warranty expense and a related estimated liability for warranties of $500,000 in its financial statements. For tax purposes, the warranty tax deduction is not allowed until paid. Therefore, Cunningham recognizes no warranty liability on a tax-basis balance sheet. Illustration 19-12 shows the balance sheet difference at the end of 2014.

When Cunningham pays the warranty liability, it reports an expense (deductible amount) for tax purposes. Because of this temporary difference, Cunningham should recognize in 2014 the tax benefits (positive tax consequences) for the tax deductions that will result from the future settlement of the liability. Cunningham reports this future tax benefit in the December 31, 2014, balance sheet as a deferred tax asset.

We can think about this situation another way. Deductible amounts occur in future tax returns. These future deductible amounts cause taxable income to be less than pretax financial income in the future as a result of an existing temporary difference. Cunningham's temporary difference originates (arises) in one period (2014) and reverses over two periods (2015 and 2016). Illustration 19-13 diagrams this situation.

Deferred Tax Asset

A deferred tax asset is the deferred tax consequence attributable to deductible temporary differences. In other words, a deferred tax asset represents the increase in taxes refundable (or saved) in future years as a result of deductible temporary differences existing at the end of the current year.

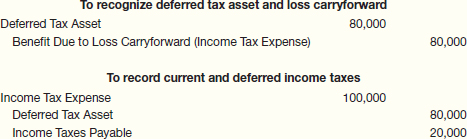

To illustrate, assume that Hunt Co. accrues a loss and a related liability of $50,000 in 2014 for financial reporting purposes because of pending litigation. Hunt cannot deduct this amount for tax purposes until the period it pays the liability, expected in 2015. As a result, a deductible amount will occur in 2015 when Hunt settles the liability (Estimated Litigation Liability), causing taxable income to be lower than pretax financial income. Illustration 19-14 shows the computation of the deferred tax asset at the end of 2014 (assuming a 40 percent tax rate).

Hunt can also compute the deferred tax asset by preparing a schedule that indicates the future deductible amounts due to deductible temporary differences. Illustration 19-15 shows this schedule.

Assuming that 2014 is Hunt's first year of operations and income taxes payable is $100,000, Hunt computes its income tax expense as follows.

The deferred tax benefit results from the increase in the deferred tax asset from the beginning to the end of the accounting period (similar to the Chelsea example earlier). The deferred tax benefit is a negative component of income tax expense. The total income tax expense of $80,000 on the income statement for 2014 thus consists of two elements—current tax expense of $100,000 and a deferred tax benefit of $20,000. For Hunt, it makes the following journal entry at the end of 2014 to record income tax expense, deferred income taxes, and income taxes payable.

![]()

At the end of 2015 (the second year), the difference between the book value and the tax basis of the litigation liability is zero. Therefore, there is no deferred tax asset at this date. Assuming that income taxes payable for 2015 is $140,000, Hunt computes income tax expense for 2015 as shown in Illustration 19-17.

The company records income taxes for 2015 as follows.

![]()

The total income tax expense of $160,000 on the income statement for 2015 thus consists of two elements—current tax expense of $140,000 and deferred tax expense of $20,000. Illustration 19-18 shows the Deferred Tax Asset account at the end of 2015.

What do the numbers mean? “REAL ASSETS”

A key issue in accounting for income taxes is whether a company should recognize a deferred tax asset in the financial records. Based on the conceptual definition of an asset, a deferred tax asset meets the three main conditions for an item to be recognized as an asset:

- It results from a past transaction. In the Hunt example, the accrual of the loss contingency is the past event that gives rise to a future deductible temporary difference.

- It gives rise to a probable benefit in the future. Taxable income exceeds pretax financial income in the current year (2014). However, in the next year the exact opposite occurs. That is, taxable income is lower than pretax financial income. Because this deductible temporary difference reduces taxes payable in the future, a probable future benefit exists at the end of the current period.

- The entity controls access to the benefits. Hunt can obtain the benefit of existing deductible temporary differences by reducing its taxes payable in the future. Hunt has the exclusive right to that benefit and can control others’ access to it.

Market analysts’ reactions to the write-off of deferred tax assets also supports their treatment as assets. When Bethlehem Steel reported a $1 billion charge to write off a deferred tax asset, analysts believed that Bethlehem was signaling that it would not realize the future benefits of the tax deductions. Thus, Bethlehem should write down the asset like other assets.

Source: J. Weil and S. Liesman, “Stock Gurus Disregard Most Big Write-Offs but They Often Hold Vital Clues to Outlook,” Wall Street Journal Online (December 31, 2001).

Deferred Tax Asset—Valuation Allowance

LEARNING OBJECTIVE ![]()

Explain the purpose of a deferred tax asset valuation allowance.

Companies recognize a deferred tax asset for all deductible temporary differences. However, a company should reduce a deferred tax asset by a valuation allowance if, based on available evidence, it is more likely than not that it will not realize some portion or all of the deferred tax asset. “More likely than not” means a level of likelihood of at least slightly more than 50 percent.

Assume that Jensen Co. has a deductible temporary difference of $1,000,000 at the end of its first year of operations. Its tax rate is 40 percent, which means it records a deferred tax asset of $400,000 ($1,000,000 × 40%). Assuming $900,000 of income taxes payable, Jensen records income tax expense, the deferred tax asset, and income taxes payable as follows.

![]()

After careful review of all available evidence, Jensen determines that it is more likely than not that it will not realize $100,000 of this deferred tax asset. Jensen records this reduction in asset value as follows.

![]()

This journal entry increases income tax expense in the current period because Jensen does not expect to realize a favorable tax benefit for a portion of the deductible temporary difference. Jensen simultaneously establishes a valuation allowance to recognize the reduction in the carrying amount of the deferred tax asset. This valuation account is a contra account. Jensen reports it on the financial statements in the following manner.

Jensen then evaluates this allowance account at the end of each accounting period. If, at the end of the next period, the deferred tax asset is still $400,000 but now the company expects to realize $350,000 of this asset, Jensen makes the following entry to adjust the valuation account.

![]()

Jensen should consider all available evidence, both positive and negative, to determine whether, based on the weight of available evidence, it needs a valuation allowance. For example, if Jensen has been experiencing a series of loss years, it reasonably assumes that these losses will continue. Therefore, Jensen will lose the benefit of the future deductible amounts. We discuss the use of a valuation account under other conditions later in the chapter.

Income Statement Presentation

LEARNING OBJECTIVE ![]()

Describe the presentation of income tax expense in the income statement.

Circumstances dictate whether a company should add or subtract the change in deferred income taxes to or from income taxes payable in computing income tax expense. For example, a company adds an increase in a deferred tax liability to income taxes payable. On the other hand, it subtracts an increase in a deferred tax asset from income taxes payable. The formula in Illustration 19-20 is used to compute income tax expense (benefit).

In the income statement or in the notes to the financial statements, a company should disclose the significant components of income tax expense attributable to continuing operations. Given the information related to Chelsea on page 1121, Chelsea reports its income statement as follows.

As illustrated, Chelsea reports both the current portion (amount of income taxes payable for the period) and the deferred portion of income tax expense. Another option is to simply report the total income tax expense on the income statement and then indicate in the notes to the financial statements the current and deferred portions. Income tax expense is often referred to as “Provision for income taxes.” Using this terminology, the current provision is $16,000, and the provision for deferred taxes is $12,000.

Specific Differences

LEARNING OBJECTIVE ![]()

Describe various temporary and permanent differences.

Numerous items create differences between pretax financial income and taxable income. For purposes of accounting recognition, these differences are of two types: (1) temporary, and (2) permanent.

Temporary Differences

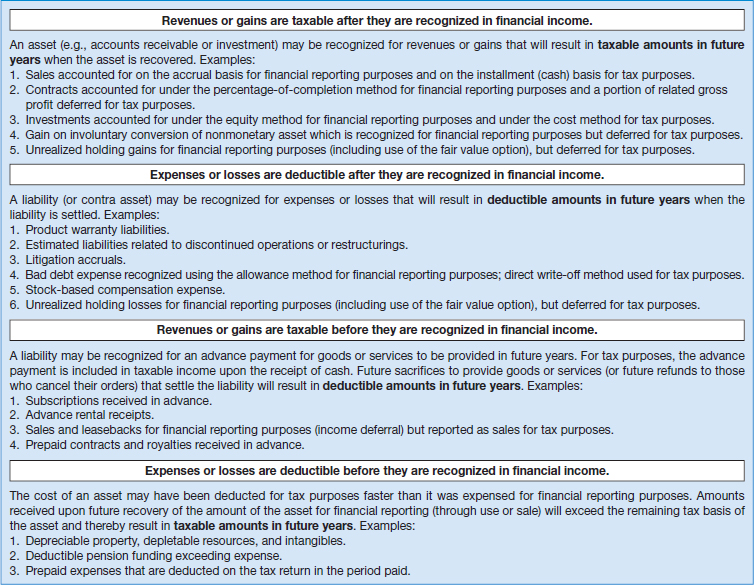

Taxable temporary differences are temporary differences that will result in taxable amounts in future years when the related assets are recovered. Deductible temporary differences are temporary differences that will result in deductible amounts in future years, when the related book liabilities are settled. As discussed earlier, taxable temporary differences give rise to recording deferred tax liabilities. Deductible temporary differences give rise to recording deferred tax assets. Illustration 19-22 provides examples of temporary differences.

Determining a company's temporary differences may prove difficult. A company should prepare a balance sheet for tax purposes that it can compare with its GAAP balance sheet. Many of the differences between the two balance sheets are temporary differences.

Originating and Reversing Aspects of Temporary Differences. An originating temporary difference is the initial difference between the book basis and the tax basis of an asset or liability, regardless of whether the tax basis of the asset or liability exceeds or is exceeded by the book basis of the asset or liability. A reversing difference, on the other hand, occurs when eliminating a temporary difference that originated in prior periods and then removing the related tax effect from the deferred tax account.

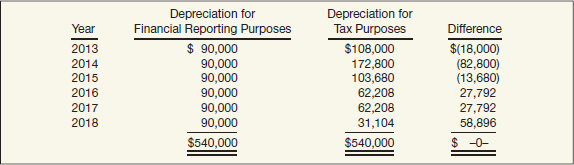

For example, assume that Sharp Co. has tax depreciation in excess of book depreciation of $2,000 in 2012, 2013, and 2014. Further, it has an excess of book depreciation over tax depreciation of $3,000 in 2015 and 2016 for the same asset. Assuming a tax rate of 30 percent for all years involved, the Deferred Tax Liability account reflects the following.

The originating differences for Sharp in each of the first three years are $2,000. The related tax effect of each originating difference is $600. The reversing differences in 2015 and 2016 are each $3,000. The related tax effect of each is $900.

Permanent Differences

![]() International Perspective

International Perspective

If companies switch to IFRS, the impact on tax accounting methods will require consideration. For example, in cases in which GAAP and tax rules are the same, what happens if IFRS is different from GAAP? Should the tax method change to IFRS? And what might happen at the state level, due to changes in the financial reporting rules?

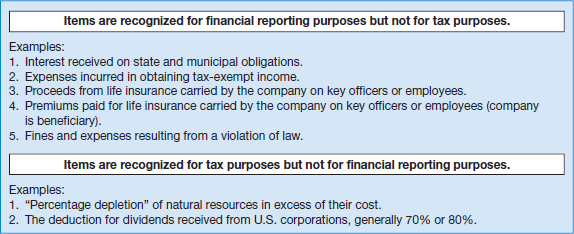

Some differences between taxable income and pretax financial income are permanent. Permanent differences result from items that (1) enter into pretax financial income but never into taxable income, or (2) enter into taxable income but never into pretax financial income.

Congress has enacted a variety of tax law provisions to attain certain political, economic, and social objectives. Some of these provisions exclude certain revenues from taxation, limit the deductibility of certain expenses, and permit the deduction of certain other expenses in excess of costs incurred. A corporation that has tax-free income, nondeductible expenses, or allowable deductions in excess of cost has an effective tax rate that differs from its statutory (regular) tax rate.

Since permanent differences affect only the period in which they occur, they do not give rise to future taxable or deductible amounts. As a result, companies recognize no deferred tax consequences. Illustration 19-24 shows examples of permanent differences.

Examples of Temporary and Permanent Differences

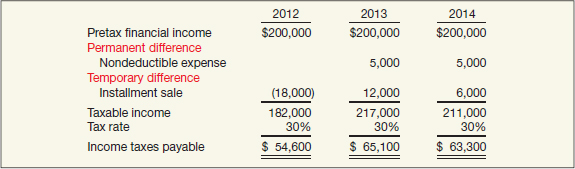

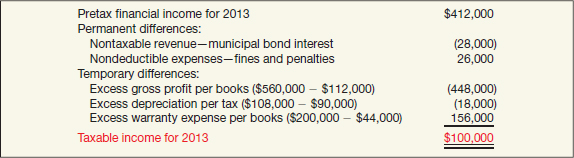

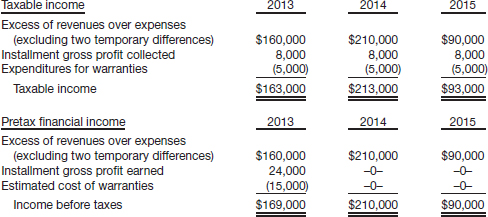

To illustrate the computations used when both temporary and permanent differences exist, assume that Bio-Tech Company reports pretax financial income of $200,000 in each of the years 2012, 2013, and 2014. The company is subject to a 30 percent tax rate and has the following differences between pretax financial income and taxable income.

- Bio-Tech reports gross profit of $18,000 from an installment sale in 2012 for tax purposes over an 18-month period at a constant amount per month beginning January 1, 2013. It recognizes the entire amount for book purposes in 2012.

- It pays life insurance premiums for its key officers of $5,000 in 2013 and 2014. Although not tax-deductible, Bio-Tech expenses the premiums for book purposes.

The installment sale is a temporary difference, whereas the life insurance premium is a permanent difference. Illustration 19-25 shows the reconciliation of Bio-Tech's pretax financial income to taxable income and the computation of income taxes payable.

Note that Bio-Tech deducts the installment-sales gross profit from pretax financial income to arrive at taxable income. The reason: Pretax financial income includes the installment-sales gross profit; taxable income does not. Conversely, it adds the $5,000 insurance premium to pretax financial income to arrive at taxable income. The reason: Pretax financial income records an expense for this premium, but for tax purposes the premium is not deductible. As a result, pretax financial income is lower than taxable income. Therefore, the life insurance premium must be added back to pretax financial income to reconcile to taxable income.

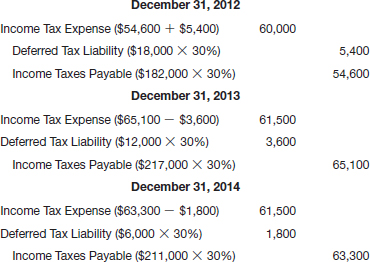

Bio-Tech records income taxes for 2012, 2013, and 2014 as follows.

Bio-Tech has one temporary difference, which originates in 2012 and reverses in 2013 and 2014. It recognizes a deferred tax liability at the end of 2012 because the temporary difference causes future taxable amounts. As the temporary difference reverses, Bio-Tech reduces the deferred tax liability. There is no deferred tax amount associated with the difference caused by the nondeductible insurance expense because it is a permanent difference.

Although an enacted tax rate of 30 percent applies for all three years, the effective rate differs from the enacted rate in 2013 and 2014. Bio-Tech computes the effective tax rate by dividing total income tax expense for the period by pretax financial income. The effective rate is 30 percent for 2012 ($60,000 ÷ $200,000 = 30%) and 30.75 percent for 2013 and 2014 ($61,500 ÷ $200,000 = 30.75%).

Tax Rate Considerations

LEARNING OBJECTIVE ![]()

Explain the effect of various tax rates and tax rate changes on deferred income taxes.

In our previous illustrations, the enacted tax rate did not change from one year to the next. Thus, to compute the deferred income tax amount to report on the balance sheet, a company simply multiplies the cumulative temporary difference by the current tax rate. Using Bio-Tech as an example, it multiplies the cumulative temporary difference of $18,000 by the enacted tax rate, 30 percent in this case, to arrive at a deferred tax liability of $5,400 ($18,000 × 30%) at the end of 2012.

Future Tax Rates

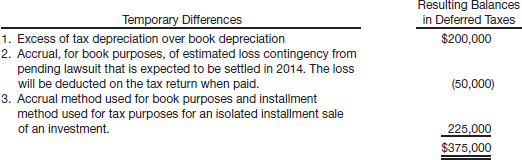

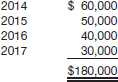

What happens if tax rates are expected to change in the future? In this case, a company should use the enacted tax rate expected to apply. Therefore, a company must consider presently enacted changes in the tax rate that become effective for a particular future year(s) when determining the tax rate to apply to existing temporary differences. For example, assume that Warlen Co. at the end of 2011 has the following cumulative temporary difference of $300,000, computed as shown in Illustration 19-26.

Furthermore, assume that the $300,000 will reverse and result in taxable amounts in the future, with the enacted tax rates shown in Illustration 19-27.

The total deferred tax liability at the end of 2011 is $108,000. Warlen may only use tax rates other than the current rate when the future tax rates have been enacted, as is the case in this example. If new rates are not yet enacted for future years, Warlen should use the current rate.

In determining the appropriate enacted tax rate for a given year, companies must use the average tax rate. The Internal Revenue Service and other taxing jurisdictions tax income on a graduated tax basis. For a U.S. corporation, the IRS taxes the first $50,000 of taxable income at 15 percent, the next $25,000 at 25 percent, with higher incremental levels of income at rates as high as 39 percent. In computing deferred income taxes, companies for which graduated tax rates are a significant factor must therefore determine the average tax rate and use that rate.

What do the numbers mean? GLOBAL TAX RATES

If you are concerned about your tax rate and the taxes you pay, you might want to consider moving to Switzerland, which has a personal tax rate of anywhere from zero percent to 13.2 percent. You don't want to move to Denmark though. Yes, the people of Denmark are regularly voted to be the happiest people on Earth but it's uncertain how many of these polls take place at tax time. The government in Denmark charges income tax rates ranging from 38 percent to 59 percent. So, taxes are a major item to many individuals, wherever they reside.

Taxes are also a big deal to corporations. For example, the Organisation for Economic Co-operation and Development (OECD) is an international organization of 30 countries that accepts the principles of a free-market economy. Most OECD members are high-income economies and are regarded as developed countries. However, companies in the OECD can be subject to significant tax levies, as indicated in the following list of the ten highest corporate income tax rates for the OECD countries.

On the low end of the tax rate spectrum are Iceland and Ireland, with tax rates of 15 percent and 12.5 percent, respectively. Indeed, corporate tax rates have been dropping around the world as countries attempt to spur capital investment, which in turn spurs international tax competition. However, with stagnant global economic growth, there is concern that governments will target increases in corporate tax rates as a source of revenues to address budget shortfalls. In addition, further expansion of value-added taxes (VAT) is being considered. Indirect taxes such as VAT are charged on consumption of goods and services, which is much more stable than the corporate tax.

If these tax proposals result in changes in the tax rates applied to future deductible and taxable amounts, be prepared for significant remeasurement of deferred tax assets and liabilities.

Source: The rates reported reflect the base corporate rate in effect in 2012. Effective rates paid may vary depending on country-specific additional levies for such items as unemployment and local taxes, and, in the case of Japan, earthquake damage assessments. Effective rates may be lower due to credits for investments and capital gains. See http://www.kpmg.com/global/en/services/tax/tax-tools-and-resources/pages/tax-rates-online.aspx. See also P. Toscano, “The World's Highest Tax Rates,” http://www.cnbc.com/id/30727913 (May 13, 2009).

Revision of Future Tax Rates

When a change in the tax rate is enacted, companies should record its effect on the existing deferred income tax accounts immediately. A company reports the effect as an adjustment to income tax expense in the period of the change.

Assume that on December 10, 2011, a new income tax act is signed into law that lowers the corporate tax rate from 40 percent to 35 percent, effective January 1, 2013. If Hostel Co. has one temporary difference at the beginning of 2011 related to $3 million of excess tax depreciation, then it has a Deferred Tax Liability account with a balance of $1,200,000 ($3,000,000 × 40%) at January 1, 2011. If taxable amounts related to this difference are scheduled to occur equally in 2012, 2013, and 2014, the deferred tax liability at the end of 2011 is $1,100,000, computed as follows.

Hostel, therefore, recognizes the decrease of $100,000 ($1,200,000 − $1,100,000) at the end of 2011 in the deferred tax liability as follows.

![]()

Corporate tax rates do not change often. Therefore, companies usually employ the current rate. However, state and foreign tax rates change more frequently, and they require adjustments in deferred income taxes accordingly.2

ACCOUNTING FOR NET OPERATING LOSSES

LEARNING OBJECTIVE ![]()

Apply accounting procedures for a loss carryback and a loss carryforward.

Every management hopes its company will be profitable. But hopes and profits may not materialize. For a start-up company, it is common to accumulate operating losses while expanding its customer base but before realizing economies of scale. For an established company, a major event such as a labor strike, rapidly changing regulatory and competitive forces, a disaster such as 9/11, or a general economic recession can cause expenses to exceed revenues—a net operating loss.

A net operating loss (NOL) occurs for tax purposes in a year when tax-deductible expenses exceed taxable revenues. An inequitable tax burden would result if companies were taxed during profitable periods without receiving any tax relief during periods of net operating losses. Under certain circumstances, therefore, the federal tax laws permit taxpayers to use the losses of one year to offset the profits of other years.

Companies accomplish this income-averaging provision through the carryback and carryforward of net operating losses. Under this provision, a company pays no income taxes for a year in which it incurs a net operating loss. In addition, it may select one of the two options discussed below and on the following pages.

Loss Carryback

Through use of a loss carryback, a company may carry the net operating loss back two years and receive refunds for income taxes paid in those years. The company must apply the loss to the earlier year first and then to the second year. It may carry forward any loss remaining after the two-year carryback up to 20 years to offset future taxable income. Illustration 19-29 diagrams the loss carryback procedure, assuming a loss in 2014.

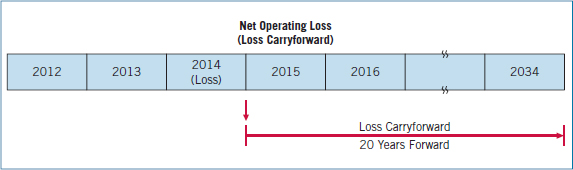

Loss Carryforward

A company may forgo the loss carryback and use only the loss carryforward option, offsetting future taxable income for up to 20 years. Illustration 19-30 shows this approach.

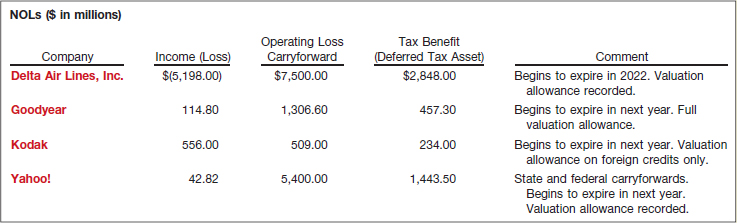

Operating losses can be substantial. For example, Yahoo! at one time had net operating losses of approximately $5.4 billion. That amount translates into tax savings of $1.4 billion if Yahoo! is able to generate taxable income before the NOLs expire.

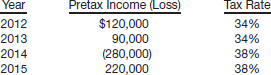

Loss Carryback Example

To illustrate the accounting procedures for a net operating loss carryback, assume that Groh Inc. has no temporary or permanent differences. Groh experiences the following.

In 2014, Groh incurs a net operating loss that it decides to carry back. Under the law, Groh must apply the carryback first to the second year preceding the loss year. Therefore, it carries the loss back first to 2012. Then, Groh carries back any unused loss to 2013. Accordingly, Groh files amended tax returns for 2012 and 2013, receiving refunds for the $110,000 ($30,000 + $80,000) of taxes paid in those years.

For accounting as well as tax purposes, the $110,000 represents the tax effect (tax benefit) of the loss carryback. Groh should recognize this tax effect in 2014, the loss year. Since the tax loss gives rise to a refund that is both measurable and currently realizable, Groh should recognize the associated tax benefit in this loss period.

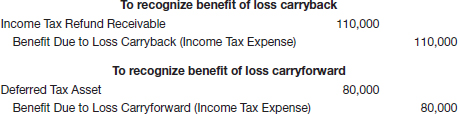

Groh makes the following journal entry for 2014.

![]()

Groh reports the account debited, Income Tax Refund Receivable, on the balance sheet as a current asset at December 31, 2014. It reports the account credited on the income statement for 2014 as shown in Illustration 19-31.

Since the $500,000 net operating loss for 2014 exceeds the $300,000 total taxable income from the 2 preceding years, Groh carries forward the remaining $200,000 loss.

Loss Carryforward Example

If a carryback fails to fully absorb a net operating loss, or if the company decides not to carry the loss back, then it can carry forward the loss for up to 20 years.3 Because companies use carryforwards to offset future taxable income, the tax effect of a loss carryforward represents future tax savings. Realization of the future tax benefit depends on future earnings, an uncertain prospect.

The key accounting issue is whether there should be different requirements for recognition of a deferred tax asset for (a) deductible temporary differences, and (b) operating loss carryforwards. The FASB's position is that in substance these items are the same—both are tax-deductible amounts in future years. As a result, the Board concluded that there should not be different requirements for recognition of a deferred tax asset from deductible temporary differences and operating loss carryforwards.4

Carryforward without Valuation Allowance

To illustrate the accounting for an operating loss carryforward, return to the Groh example from the preceding section. In 2014, the company records the tax effect of the $200,000 loss carryforward as a deferred tax asset of $80,000 ($200,000 × 40%), assuming that the enacted future tax rate is 40 percent. Groh records the benefits of the carryback and the carryforward in 2014 as follows.

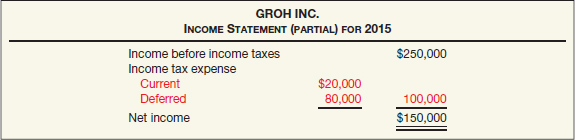

Groh realizes the income tax refund receivable of $110,000 immediately as a refund of taxes paid in the past. It establishes a Deferred Tax Asset account for the benefits of future tax savings. The two accounts credited are contra income tax expense items, which Groh presents on the 2014 income statement shown in Illustration 19-32.

ILLUSTRATION 19-32 Recognition of the Benefit of the Loss Carryback and Carryforward in the Loss Year

The current tax benefit of $110,000 is the income tax refundable for the year. Groh determines this amount by applying the carryback provisions of the tax law to the taxable loss for 2014. The $80,000 is the deferred tax benefit for the year, which results from an increase in the deferred tax asset.

For 2015, assume that Groh returns to profitable operations and has taxable income of $250,000 (prior to adjustment for the NOL carryforward), subject to a 40 percent tax rate. Groh then realizes the benefits of the carryforward for tax purposes in 2015, which it recognized for accounting purposes in 2014. Groh computes the income taxes payable for 2015 as shown in Illustration 19-33.

Groh records income taxes in 2015 as follows.

![]()

The benefits of the NOL carryforward, realized in 2015, reduce the Deferred Tax Asset account to zero.

The 2015 income statement that appears in Illustration 19-34 does not report the tax effects of either the loss carryback or the loss carryforward because Groh had reported both previously.

ILLUSTRATION 19-34 Presentation of the Benefit of Loss Carryforward Realized in 2015, Recognized in 2014

Carryforward with Valuation Allowance

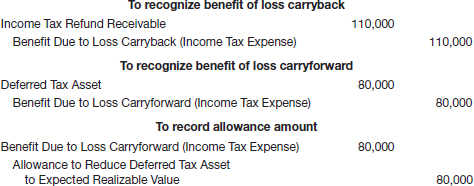

Let us return to the Groh example. Assume that it is more likely than not that Groh will not realize the entire NOL carryforward in future years. In this situation, Groh records the tax benefits of $110,000 associated with the $300,000 NOL carryback, as we previously described. In addition, it records Deferred Tax Asset of $80,000 ($200,000 × 40%) for the potential benefits related to the loss carryforward, and an allowance to reduce the deferred tax asset by the same amount. Groh makes the following journal entries in 2014.

The latter entry indicates that because positive evidence of sufficient quality and quantity is unavailable to counteract the negative evidence, Groh needs a valuation allowance.

Illustration 19-35 shows Groh's 2014 income statement presentation.

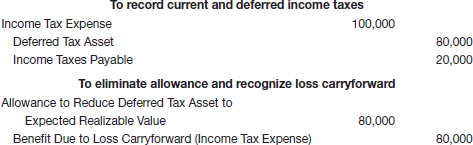

In 2015, assuming that Groh has taxable income of $250,000 (before considering the carryforward) subject to a tax rate of 40 percent, it realizes the deferred tax asset. It thus no longer needs the allowance. Groh records the following entries.

Groh reports the $80,000 Benefit Due to the Loss Carryforward on the 2015 income statement. The company did not recognize it in 2014 because it was more likely than not that it would not be realized. Assuming that Groh derives the income for 2015 from continuing operations, it prepares the income statement as shown in Illustration 19-36.

Another method is to report only one line for total income tax expense of $20,000 on the face of the income statement and disclose the components of income tax expense in the notes to the financial statements.

Valuation Allowance Revisited

A company should consider all positive and negative information in determining whether it needs a valuation allowance. Whether the company will realize a deferred tax asset depends on whether sufficient taxable income exists or will exist within the carryforward period available under tax law. Illustration 19-37 shows possible sources of taxable income that may be available under the tax law to realize a tax benefit for deductible temporary differences and carryforwards.5

![]() See the FASB Codification section (page 1156).

See the FASB Codification section (page 1156).

If any one of these sources is sufficient to support a conclusion that a valuation allowance is unnecessary, a company need not consider other sources.

Forming a conclusion that a valuation allowance is not needed is difficult when there is negative evidence such as cumulative losses in recent years. Companies may also cite positive evidence indicating that a valuation allowance is not needed. Illustration 19-38 presents examples (not prerequisites) of evidence to consider when determining the need for a valuation allowance.6

![]() International Perspective

International Perspective

Under IFRS (IAS 12), a company may not recognize a deferred tax asset unless realization is “probable.” However, “probable” is not defined in the standard, leading to diversity in the recognition of deferred tax assets.

The use of a valuation allowance provides a company with an opportunity to manage its earnings. As one accounting expert notes, “The ‘more likely than not’ provision is perhaps the most judgmental clause in accounting.” Some companies may set up a valuation account and then use it to increase income as needed. Others may take the income immediately to increase capital or to offset large negative charges to income.

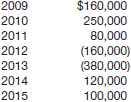

What do the numbers mean? NOLs: GOOD NEWS OR BAD?

Here are some net operating loss numbers reported by several notable companies.

All of these companies are using the carryforward provisions of the tax code for their NOLs. For many of them, the NOL is an amount far exceeding their reported profits. Why carry forward the loss to get the tax deduction? First, the company may have already used up the carryback provision, which allows only a two-year carryback period. (Carryforwards can be claimed up to 20 years in the future.) In some cases, management expects the tax rates in the future to be higher. This difference in expected rates provides a bigger tax benefit if the losses are carried forward and matched against future income. Is there a downside? To realize the benefits of carryforwards, a company must have future taxable income in the carryforward period in order to claim the NOL deductions. As we learned, if it is more likely than not that a company will not have taxable income, it must record a valuation allowance (and increased tax expense). As the data above indicate, recording a valuation allowance to reflect the uncertainty of realizing the tax benefits has merit. But for some, the NOL benefits begin to expire in the following year, which may be not enough time to generate sufficient taxable income in order to claim the NOL deduction.

Source: Company annual reports.

FINANCIAL STATEMENT PRESENTATION

Balance Sheet

LEARNING OBJECTIVE ![]()

Describe the presentation of deferred income taxes in financial statements.

Deferred tax accounts are reported on the balance sheet as assets and liabilities. Companies should classify these accounts as a net current amount and a net noncurrent amount. An individual deferred tax liability or asset is classified as current or noncurrent based on the classification of the related asset or liability for financial reporting purposes.

A company considers a deferred tax asset or liability to be related to an asset or liability if reduction of the asset or liability causes the temporary difference to reverse or turn around. A company should classify a deferred tax liability or asset that is unrelated to an asset or liability for financial reporting, including a deferred tax asset related to a loss carryforward, according to the expected reversal date of the temporary difference.

To illustrate, assume that Morgan Inc. records bad debt expense using the allowance method for accounting purposes and the direct write-off method for tax purposes. It currently has Accounts Receivable and Allowance for Doubtful Accounts balances of $2 million and $100,000, respectively. In addition, given a 40 percent tax rate, Morgan has a debit balance in the Deferred Tax Asset account of $40,000 (40% × $100,000). It considers the $40,000 debit balance in the Deferred Tax Asset account to be related to the Accounts Receivable and the Allowance for Doubtful Accounts balances because collection or write-off of the receivables will cause the temporary difference to reverse. Therefore, Morgan classifies the Deferred Tax Asset account as current, the same as the Accounts Receivable and Allowance for Doubtful Accounts balances.

In practice, most companies engage in a large number of transactions that give rise to deferred taxes. Companies should classify the balances in the deferred tax accounts on the balance sheet in two categories: one for the net current amount, and one for the net noncurrent amount. We summarize this procedure as follows.

- Classify the amounts as current or non-current. If related to a specific asset or liability, classify the amounts in the same manner as the related asset or liability. If not related, classify them on the basis of the expected reversal date of the temporary difference.

- Determine the net current amount by summing the various deferred tax assets and liabilities classified as current. If the net result is an asset, report it on the balance sheet as a current asset; if a liability, report it as a current liability.

- Determine the net non-current amount by summing the various deferred tax assets and liabilities classified as noncurrent. If the net result is an asset, report it on the balance sheet as a noncurrent asset; if a liability, report it as a long-term liability.

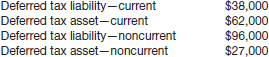

To illustrate, assume that K. Scott Company has four deferred tax items at December 31, 2014. Illustration 19-39 shows an analysis of these four temporary differences as current or noncurrent.

K. Scott classifies as current a deferred tax asset of $9,000 ($42,000 + $12,000 − $45,000). It also reports as noncurrent a deferred tax liability of $214,000. Consequently, K. Scott's December 31, 2014, balance sheet reports deferred income taxes as shown in Illustration 19-40.

As we indicated earlier, a deferred tax asset or liability may not be related to an asset or liability for financial reporting purposes. One example is an operating loss carry-forward. In this case, a company records a deferred tax asset, but there is no related, identifiable asset or liability for financial reporting purposes. In these limited situations, deferred income taxes are classified according to the expected reversal date of the temporary difference. That is, a company should report the tax effect of any temporary difference reversing next year as current, and the remainder as noncurrent. If a deferred tax asset is noncurrent, a company should classify it in the “Other assets” section.

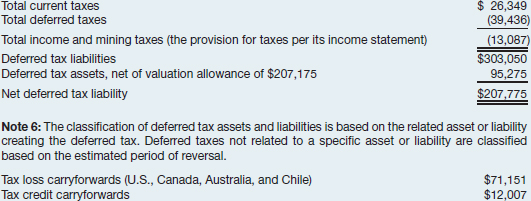

The total of all deferred tax liabilities, the total of all deferred tax assets, and the total valuation allowance should be disclosed. In addition, companies should disclose the following: (1) any net change during the year in the total valuation allowance, and (2) the types of temporary differences, carryforwards, or carrybacks that give rise to significant portions of deferred tax liabilities and assets.

![]() International Perspective

International Perspective

IFRS requires that deferred tax assets and liabilities be classified as noncurrent, regardless of the classification of the underlying asset or liability.

Income taxes payable is reported as a current liability on the balance sheet. Corporations make estimated tax payments to the Internal Revenue Service quarterly. They record these estimated payments by a debit to Prepaid Income Taxes. As a result, the balance of the Income Taxes Payable offsets the balance of the Prepaid Income Taxes account when reporting income taxes on the balance sheet.

What do the numbers mean? IMAGINATION AT WORK

Here's one thing you can say that's true about U.S. corporate taxes: The statutory rate (35 percent at the federal level, 39.2 percent when you average in state rates) is the highest on earth (see the “What Do the Numbers Mean?” box on page 1131). Here's another thing you can say that's true about U.S. corporate taxes: The average effective tax rate is more like 25 percent, and many corporations generally pay much less than that. How do they do it? Take Apple, for example. It uses a tax structure known as the “Double Irish with a Dutch Sandwich,” which reduces taxes by routing profits through Irish subsidiaries and the Netherlands and then to the Caribbean. As a result of using this tactic, Apple paid cash taxes of $3.3 billion around the world on its reported profits of $34.2 billion in a recent year, a tax rate of just 9.8 percent. Google uses the same strategy to reduce its overseas tax rate to 2.4 percent, the lowest of the top five U.S. technology companies by market capitalization, according to regulatory filings in six countries.

General Electric (GE) is generally viewed as the most skilled at reducing its tax burden. GE uses a maze of shelters, tax credits, and subsidiaries to pay far less than the stated tax rate. In a recent year, it reported worldwide profits of $14.2 billion, and said $5.1 billion of the total came from its operations in the United States. Its American tax bill? Zero. In fact, GE claimed a tax benefit of $3.2 billion. GE's giant tax department is viewed by some as the world's best tax law firm. Indeed, the company's slogan, “Imagination at Work,” fits this department well. The team includes former officials not just from the Treasury, but also from the IRS and virtually all the tax-writing committees in Congress. The strategies employed by Apple, Google, and GE, as well as changes in tax laws that encouraged some businesses and professionals to file as individuals, have pushed down the corporate share of the nation's tax receipts from 30 percent of all federal revenue in the mid-1950s to 6.6 percent in 2009.

One IRS provision designed to curb excessive tax avoidance is the alternative minimum tax (AMT). Companies compute their potential tax liability under the AMT, adjusting for various preference items that reduce their tax bills under the regular tax code. (Examples of such preference items are accelerated depreciation methods and the installment method for revenue recognition.) Companies must pay the higher of the two tax obligations computed under the AMT and the regular tax code. But, as indicated by the cases above, some profitable companies avoid high tax bills, even in the presence of the AMT. Indeed, a recent study by the Government Accounting Office found that roughly two-thirds of U.S. and foreign corporations paid no federal income taxes from 1998–2005. Many citizens and public-interest groups cite corporate avoidance of income taxes as a reason for more tax reform.

Sources: D. Kocieniewski, “G.E.'s Strategies Let It Avoid Taxes Altogether,” The New York Times (March 24, 2011); and J. Fox, “Why Some Multinationals Pay Such Low Taxes,” HBR Blog Network (March 27, 2012).

Income Statement

Companies should allocate income tax expense (or benefit) to continuing operations, discontinued operations, extraordinary items, and prior period adjustments. This approach is referred to as intraperiod tax allocation.

In addition, companies should disclose the significant components of income tax expense attributable to continuing operations:

- Current tax expense or benefit.

- Deferred tax expense or benefit, exclusive of other components listed below.

- Investment tax credits.

- Government grants (if recognized as a reduction of income tax expense).

- The benefits of operating loss carryforwards (resulting in a reduction of income tax expense).

- Tax expense that results from allocating tax benefits either directly to paid-in capital or to reduce goodwill or other noncurrent intangible assets of an acquired entity.

- Adjustments of a deferred tax liability or asset for enacted changes in tax laws or rates or a change in the tax status of a company.

- Adjustments of the beginning-of-the-year balance of a valuation allowance because of a change in circumstances that causes a change in judgment about the realizability of the related deferred tax asset in future years.

In the notes, companies must also reconcile (using percentages or dollar amounts) income tax expense attributable to continuing operations with the amount that results from applying domestic federal statutory tax rates to pretax income from continuing significant reconciling items. Illustration 19-41 (page 1142) presents an example from the 2011 annual report of PepsiCo, Inc.

These income tax disclosures are required for several reasons:

- Assessing quality of earnings. Many investors seeking to assess the quality of a company's earnings are interested in the reconciliation of pretax financial income to taxable income. Analysts carefully examine earnings that are enhanced by a favorable tax effect, particularly if the tax effect is nonrecurring. For example, the tax disclosure in Illustration 19-41 indicates that PepsiCo's effective tax rate increased from 23 percent in 2010 to 26.8 percent in 2011 (due to acquisitions of PBG and PAS and “other”). This decrease in the effective tax rate increased income for 2011.

- Making better predictions of future cash flows. Examination of the deferred portion of income tax expense provides information as to whether taxes payable are likely to be higher or lower in the future. In PepsiCo's case, analysts expect future taxable amounts and higher tax payments, primarily from lower depreciation and amortization in the future. PepsiCo expects future deductible amounts and lower tax payments due to deductions for carryforwards, employee benefits, and state taxes. These deferred tax items indicate that actual tax payments for PepsiCo will be higher than the tax expense reported on the income statement in the future.7

- Predicting future cash flows for operating loss carryforwards. Companies should disclose the amounts and expiration dates of any operating loss carryforwards for tax purposes. From this disclosure, analysts determine the amount of income that the company may recognize in the future on which it will pay no income tax. For example, the PepsiCo disclosure in Illustration 19-41 indicates that PepsiCo has $10.0 billion in net operating loss carryforwards that it can use to reduce future taxes. However, the valuation allowance indicates that $1.264 million of deferred tax assets may not be realized in the future.

Loss carryforwards can be valuable to a potential acquirer. For example, as mentioned earlier, Yahoo! has a substantial net operating loss carryforward. A potential acquirer would find Yahoo! more valuable as a result of these carryforwards. That is, the acquirer may be able to use these carryforwards to shield future income. However the acquiring company has to be careful because the structure of the deal may lead to a situation where the deductions will be severely limited.

Much the same issue arises in companies emerging from bankruptcy. In many cases, these companies have large NOLs but the value of the losses may be limited. This is because any gains related to the cancellation of liabilities in bankruptcy must be offset against the NOLs. For example, when Kmart Holding Corp. emerged from bankruptcy in early 2004, it disclosed NOL carryforwards approximating $3.8 billion. At the same time, Kmart disclosed cancellation of debt gains that reduced the value of the NOL carryforward. These reductions soured the merger between Kmart and Sears Roebuck because the cancellation of the indebtedness gains reduced the value of the Kmart carryforwards to the merged company by $3.74 billion.8

Evolving Issue UNCERTAIN TAX POSITIONS

Evolving Issue UNCERTAIN TAX POSITIONS

Whenever there is a contingency, companies determine if the contingency is probable and can be reasonably estimated. If both of these criteria are met, the company records the contingency in the financial statements. These guidelines also apply to uncertain tax positions. Uncertain tax positions are tax positions for which the tax authorities may disallow a deduction in whole or in part. Uncertain tax positions often arise when a company takes an aggressive approach in its tax planning. Examples are instances in which the tax law is unclear or the company may believe that the risk of audit is low. Uncertain tax positions give rise to tax benefits either by reducing income tax expense or related payables or by increasing an income tax refund receivable or deferred tax asset.

Unfortunately, companies have not applied these provisions consistently in accounting and reporting of uncertain tax positions. Some companies have not recognized a tax benefit unless it is probable that the benefit will be realized and can be reasonably estimated. Other companies have used a lower threshold, such as that found in the existing authoritative literature. As we have learned, the lower threshold—described as “more likely than not”—means that the company believes it has at least a 51 percent chance that the uncertain tax position will pass muster with the taxing authorities. Thus, there has been diversity in practice concerning the accounting and reporting of uncertain tax positions.

As a result, the FASB has issued rules for companies to follow to determine whether it is “more likely than not” that tax positions will be sustained upon audit. [3] If the probability is more than 50 percent, companies may reduce their liability or increase their assets. If the probability is less than 50 percent, companies may not record the tax benefit. In determining “more likely than not,” companies must assume that they will be audited by the tax authorities. If the recognition threshold is passed, companies must then estimate the amount to record as an adjustment to their tax assets and liabilities. (This estimation process is complex and is beyond the scope of this textbook.)

Companies will experience varying financial statement effects upon adoption of these rules. Those with a history of conservative tax strategies may have their tax liabilities decrease or their tax assets increase. For example, PepsiCo recorded a $7 million increase to retained earnings upon adoption of the guidelines. Others that followed more aggressive tax planning may have to increase their liabilities or reduce their assets, with a resulting negative effect on net income.

REVIEW OF THE ASSET-LIABILITY METHOD

LEARNING OBJECTIVE ![]()

Indicate the basic principles of the asset-liability method.

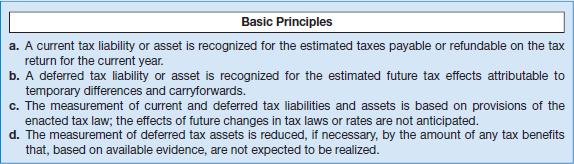

The FASB believes that the asset-liability method (sometimes referred to as the liability approach) is the most consistent method for accounting for income taxes. One objective of this approach is to recognize the amount of taxes payable or refundable for the current year. A second objective is to recognize deferred tax liabilities and assets for the future tax consequences of events that have been recognized in the financial statements or tax returns.

To implement the objectives, companies apply some basic principles in accounting for income taxes at the date of the financial statements, as listed in Illustration 19-42. [4]

Illustration 19-43 diagrams the procedures for implementing the asset-liability method.

As an aid to understanding deferred income taxes, we provide the following glossary.

![]() International Perspective

International Perspective

IFRS on income taxes is based on the same principles as GAAP—comprehensive recognition of deferred tax assets and liabilities.

KEY DEFERRED INCOME TAX TERMS

CARRYBACKS. Deductions or credits that cannot be utilized on the tax return during a year and that may be carried back to reduce taxable income or taxes paid in a prior year. An operating loss carryback is an excess of tax deductions over gross income in a year. A tax credit carryback is the amount by which tax credits available for utilization exceed statutory limitations.

CARRYFORWARDS. Deductions or credits that cannot be utilized on the tax return during a year and that may be carried forward to reduce taxable income or taxes payable in a future year. An operating loss carryforward is an excess of tax deductions over gross income in a year. A tax credit carryforward is the amount by which tax credits available for utilization exceed statutory limitations.

CURRENT TAX EXPENSE (BENEFIT). The amount of income taxes paid or payable (or refundable) for a year as determined by applying the provisions of the enacted tax law to the taxable income or excess of deductions over revenues for that year.

DEDUCTIBLE TEMPORARY DIFFERENCE. Temporary differences that result in deductible amounts in future years when recovering or settling the related asset or liability, respectively.

DEFERRED TAX ASSET. The deferred tax consequences attributable to deductible temporary differences and carryforwards.

DEFERRED TAX CONSEQUENCES. The future effects on income taxes as measured by the enacted tax rate and provisions of the enacted tax law resulting from temporary differences and carryforwards at the end of the current year.

DEFERRED TAX EXPENSE (BENEFIT). The change during the year in a company's deferred tax liabilities and assets.

DEFERRED TAX LIABILITY. The deferred tax consequences attributable to taxable temporary differences.

INCOME TAXES. Domestic and foreign federal (national), state, and local (including franchise) taxes based on income.

INCOME TAXES CURRENTLY PAYABLE (REFUNDABLE). Refer to current tax expense (benefit).

INCOME TAX EXPENSE (BENEFIT). The sum of current tax expense (benefit) and deferred tax expense (benefit).

TAXABLE INCOME. The excess of taxable revenues over tax-deductible expenses and exemptions for the year as defined by the governmental taxing authority.

TAXABLE TEMPORARY DIFFERENCE. Temporary differences that result in taxable amounts in future years when recovering or settling the related asset or liability, respectively.

TAX-PLANNING STRATEGY. An action that meets certain criteria and that a company implements to realize a tax benefit for an operating loss or tax credit carryforward before it expires. Companies consider tax-planning strategies when assessing the need for and amount of a valuation allowance for deferred tax assets.

TEMPORARY DIFFERENCE. A difference between the tax basis of an asset or liability and its reported amount in the financial statements that will result in taxable or deductible amounts in future years when recovering or settling the reported amount of the asset or liability, respectively.

VALUATION ALLOWANCE. The portion of a deferred tax asset for which it is more likely than not that a company will not realize a tax benefit.

![]() You will want to read the IFRS INSIGHTS on pages 1175–1181 for discussion of IFRS related to income taxes.

You will want to read the IFRS INSIGHTS on pages 1175–1181 for discussion of IFRS related to income taxes.

KEY TERMS

alternative minimum tax (AMT), 1140

asset-liability method, 1144

average tax rate, 1130

current tax expense (benefit), 1121, 1134

deductible amounts, 1120

deductible temporary difference, 1127

deferred tax asset, 1123

deferred tax expense (benefit), 1121, 1124

deferred tax liability, 1120

effective tax rate, 1130

enacted tax rate, 1130

Income Tax Refund Receivable, 1133

loss carryback, 1132

loss carryforward, 1132

more likely than not, 1125

net current amount, 1139

net noncurrent amount, 1139

net operating loss (NOL), 1132

originating temporary difference, 1128

permanent difference, 1128

pretax financial income, 1118

reversing difference, 1128

taxable amounts, 1120

taxable income, 1118

taxable temporary difference, 1127

tax effect (tax benefit), 1133

temporary difference, 1120

uncertain tax positions, 1143

valuation allowance, 1125

SUMMARY OF LEARNING OBJECTIVES

![]() Identify differences between pretax financial income and taxable income. Companies compute pretax financial income (or income for book purposes) in accordance with generally accepted accounting principles. They compute taxable income (or income for tax purposes) in accordance with prescribed tax regulations. Because tax regulations and GAAP differ in many ways, so frequently do pretax financial income and taxable income. Differences may exist, for example, in the timing of revenue recognition and the timing of expense recognition.

Identify differences between pretax financial income and taxable income. Companies compute pretax financial income (or income for book purposes) in accordance with generally accepted accounting principles. They compute taxable income (or income for tax purposes) in accordance with prescribed tax regulations. Because tax regulations and GAAP differ in many ways, so frequently do pretax financial income and taxable income. Differences may exist, for example, in the timing of revenue recognition and the timing of expense recognition.

![]() Describe a temporary difference that results in future taxable amounts. Revenue recognized for book purposes in the period earned but deferred and reported as revenue for tax purposes when collected results in future taxable amounts. The future taxable amounts will occur in the periods the company recovers the receivable and reports the collections as revenue for tax purposes. This results in a deferred tax liability.

Describe a temporary difference that results in future taxable amounts. Revenue recognized for book purposes in the period earned but deferred and reported as revenue for tax purposes when collected results in future taxable amounts. The future taxable amounts will occur in the periods the company recovers the receivable and reports the collections as revenue for tax purposes. This results in a deferred tax liability.

![]() Describe a temporary difference that results in future deductible amounts. An accrued warranty expense that a company pays for and deducts for tax purposes, in a period later than the period in which it incurs and recognizes it for book purposes, results in future deductible amounts. The future deductible amounts will occur in the periods during which the company settles the related liability for book purposes. This results in a deferred tax asset.

Describe a temporary difference that results in future deductible amounts. An accrued warranty expense that a company pays for and deducts for tax purposes, in a period later than the period in which it incurs and recognizes it for book purposes, results in future deductible amounts. The future deductible amounts will occur in the periods during which the company settles the related liability for book purposes. This results in a deferred tax asset.

![]() Explain the purpose of a deferred tax asset valuation allowance. A deferred tax asset should be reduced by a valuation allowance if, based on all available evidence, it is more likely than not (a level of likelihood that is at least slightly more than 50 percent) that it will not realize some portion or all of the deferred tax asset. The company should carefully consider all available evidence, both positive and negative, to determine whether, based on the weight of available evidence, it needs a valuation allowance.

Explain the purpose of a deferred tax asset valuation allowance. A deferred tax asset should be reduced by a valuation allowance if, based on all available evidence, it is more likely than not (a level of likelihood that is at least slightly more than 50 percent) that it will not realize some portion or all of the deferred tax asset. The company should carefully consider all available evidence, both positive and negative, to determine whether, based on the weight of available evidence, it needs a valuation allowance.

![]() Describe the presentation of income tax expense in the income statement. Significant components of income tax expense should be disclosed in the income statement or in the notes to the financial statements. The most commonly encountered components are the current expense (or benefit) and the deferred expense (or benefit).

Describe the presentation of income tax expense in the income statement. Significant components of income tax expense should be disclosed in the income statement or in the notes to the financial statements. The most commonly encountered components are the current expense (or benefit) and the deferred expense (or benefit).

![]() Describe various temporary and permanent differences. Examples of temporary differences are (1) revenues or gains that are taxable after recognition in financial income; (2) expenses or losses that are deductible after recognition in financial income; (3) revenues or gains that are taxable before recognition in financial income; and (4) expenses or losses that are deductible before recognition in financial income. Examples of permanent differences are (1) items recognized for financial reporting purposes but not for tax purposes, and (2) items recognized for tax purposes but not for financial reporting purposes.

Describe various temporary and permanent differences. Examples of temporary differences are (1) revenues or gains that are taxable after recognition in financial income; (2) expenses or losses that are deductible after recognition in financial income; (3) revenues or gains that are taxable before recognition in financial income; and (4) expenses or losses that are deductible before recognition in financial income. Examples of permanent differences are (1) items recognized for financial reporting purposes but not for tax purposes, and (2) items recognized for tax purposes but not for financial reporting purposes.

![]() Explain the effect of various tax rates and tax rate changes on deferred income taxes. Companies may use tax rates other than the current rate only after enactment of the future tax rates. When a change in the tax rate is enacted, a company should immediately recognize its effect on the deferred income tax accounts. The company reports the effects as an adjustment to income tax expense in the period of the change.

Explain the effect of various tax rates and tax rate changes on deferred income taxes. Companies may use tax rates other than the current rate only after enactment of the future tax rates. When a change in the tax rate is enacted, a company should immediately recognize its effect on the deferred income tax accounts. The company reports the effects as an adjustment to income tax expense in the period of the change.