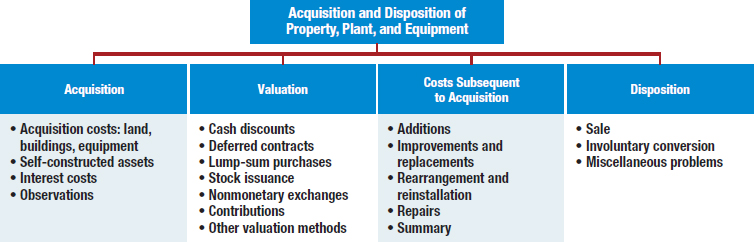

CHAPTER 10 Acquisition and Disposition of Property, Plant, and Equipment

LEARNING OBJECTIVES

After studying this chapter, you should be able to:

- Describe property, plant, and equipment.

- Identify the costs to include in initial valuation of property, plant, and equipment.

- Describe the accounting problems associated with self-constructed assets.

- Describe the accounting problems associated with interest capitalization.

- Understand accounting issues related to acquiring and valuing plant assets.

- Describe the accounting treatment for costs subsequent to acquisition.

- Describe the accounting treatment for the disposal of property, plant, and equipment.

Watch Your Spending

Investments in long-lived assets, such as property, plant, and equipment, are important elements in many companies' balance sheets. As Table 1 shows, capital expenditures on structures and equipment (whether new or used) are starting to grow again after the effects of the 2008 financial crisis.

Unfortunately, Table 1 also shows that capital expenditures' growth is overall stagnant in the last 10 years. However, better times may be ahead. To illustrate, the food and beverage industry increased its capital expenditures by 20 percent in 2011 and is estimated to increase them again by 4 percent in 2012. Table 2 identifies the five companies in this industry with the largest capital expenditures in 2011 and 2012.

![]() CONCEPTUAL FOCUS

CONCEPTUAL FOCUS

![]() INTERNATIONAL FOCUS

INTERNATIONAL FOCUS

- See the International Perspectives on pages 538, 542, 546, 550, and 555.

- IFRS Insights related to property, plant, and equipment are presented in Chapter 11.

Capital expenditures are significant for many companies. For example, at Jet Blue Airways, plant assets are 69 percent of its total assets. For Wal-Mart Stores, Inc., it's 53 percent. Conversely, Microsoft's percentage is just 3 percent. Amounts for companies' capital expenditures are reported on a company's balance sheet and directly affect such items as total assets, depreciation expense, cash flows, and net income. Companies that overspend in this area find that income is reduced as depreciation increases without corresponding increases in revenues. As a result, these companies often lose financial flexibility. That is, they find themselves in a cash bind as their cash flows from operations can no longer meet their obligations.

A good example is Baker Hughes, Inc. (an oilfield-services company), which in the first half of 2012 reported cash flow from operations of $24 million but capital expenditures of $1,442 million. Although the company is presently stable, the unfavorable relationship of cash flow from operations to capital expenditures is a cause for concern.

Companies can also affect income by reducing capital expenditures. For example, Cintas (a uniform rental business) cut back on capital expenditures in recent years. In response, depreciation expense declined to $152 million in 2010 relative to $158 million in the prior year. That lifted its earnings per share by seven cents. Similarly, Norfolk Southern added eight cents per share to its bottom line through lower depreciation charges.

Thus, not only do companies have to be careful in planning the proper amount of capital expenditures, but users must understand the impact of these expenditures on measures of financial performance. As illustrated by the examples above, the level of capital expenditures, depreciation expense, cash flow from operations, and net income all play a role in assessing a company's ability to generate future cash flows.

Sources: Adapted from L. Strauss, “Depreciation: An Appreciation,” Barrons Online (April 30, 2011); and D. Phelps, “Top 100 Capital Spending Report: Greek Yogurt Plants Are Stacking Up,” www.FoodProcessing.com (April 9, 2012).

PREVIEW OF CHAPTER 10

As we indicate in the opening story, a company like Jet Blue Airways has a substantial investment in property, plant, and equipment. Conversely, other companies, such as Microsoft, have a minor investment in these types of assets. In this chapter, we discuss the proper accounting for the acquisition, use, and disposition of property, plant, and equipment. The content and organization of the chapter are as follows.

PROPERTY, PLANT, AND EQUIPMENT

Companies like Boeing, Target, and Starbucks use assets of a durable nature. Such assets are called property, plant, and equipment. Other terms commonly used are plant assets and fixed assets. We use these terms interchangeably. Property, plant, and equipment include land, building structures (offices, factories, warehouses), and equipment (machinery, furniture, tools). The major characteristics of property, plant, and equipment are as follows.

- They are acquired for use in operations and not for resale. Only assets used in normal business operations are classified as property, plant, and equipment. For example, an idle building is more appropriately classified separately as an investment. Land developers or subdividers classify land as inventory.

- They are long-term in nature and usually depreciated. Property, plant, and equipment yield services over a number of years. Companies allocate the cost of the investment in these assets to future periods through periodic depreciation charges. The exception is land, which is depreciated only if a material decrease in value occurs, such as a loss in fertility of agricultural land because of poor crop rotation, drought, or soil erosion.

Underlying Concepts

Underlying ConceptsFair value is relevant to inventory but less so for property, plant, and equipment which, consistent with the going-concern assumption, are held for use in the business, not for sale like inventory.

- They possess physical substance. Property, plant, and equipment are tangible assets characterized by physical existence or substance. This differentiates them from intangible assets, such as patents or goodwill. Unlike raw material, however, property, plant, and equipment do not physically become part of a product held for resale.

Acquisition of Property, Plant, and Equipment

LEARNING OBJECTIVE ![]()

Identify the costs to include in initial valuation of property, plant, and equipment.

Most companies use historical cost as the basis for valuing property, plant, and equipment. Historical cost measures the cash or cash equivalent price of obtaining the asset and bringing it to the location and condition necessary for its intended use. For example, companies like Kellogg Co. consider the purchase price, freight costs, sales taxes, and installation costs of a productive asset as part of the asset's cost. It then allocates these costs to future periods through depreciation. Further, Kellogg adds to the asset's original cost any related costs incurred after the asset's acquisition, such as additions, improvements, or replacements, if they provide future service potential. Otherwise, Kellogg expenses these costs immediately.1

![]() International Perspective

International Perspective

Under international accounting standards, historical cost is the benchmark (preferred) treatment for property, plant, and equipment. However, companies may also use revalued amounts. When using revaluation, companies must revalue the class of assets regularly.

Subsequent to acquisition, companies should not write up property, plant, and equipment to reflect fair value when it is above cost. The main reasons for this position are as follows.

- Historical cost involves actual, not hypothetical, transactions and so is the most reliable.

- Companies should not anticipate gains and losses but should recognize gains and losses only when the asset is sold.

Even those who favor fair value measurement for inventory and financial instruments often take the position that property, plant, and equipment should not be revalued. The major concern is the difficulty of developing a reliable fair value for these types of assets. For example, how does one value a General Motors automobile manufacturing plant or a nuclear power plant owned by Consolidated Edison?

![]() See the FASB Codification section (page 564).

See the FASB Codification section (page 564).

However, if the fair value of the property, plant, and equipment is less than its carrying amount, the asset may be written down. These situations occur when the asset is impaired (discussed in Chapter 11) and in situations where the asset is being held for sale. A long-lived asset classified as held for sale should be measured at the lower of its carrying amount or fair value less costs to sell. In that case, a reasonable valuation for the asset can be obtained, based on the sales price. A long-lived asset is not depreciated if it is classified as held for sale. This is because such assets are not being used to generate revenues. [1]

Cost of Land

All expenditures made to acquire land and ready it for use are considered part of the land cost. Thus, when Wal-Mart Stores, Inc. or Home Depot purchases land on which to build a new store, its land costs typically include (1) the purchase price; (2) closing costs, such as title to the land, attorney's fees, and recording fees; (3) costs incurred in getting the land in condition for its intended use, such as grading, filling, draining, and clearing; (4) assumption of any liens, mortgages, or encumbrances on the property; and (5) any additional land improvements that have an indefinite life.

For example, when Home Depot purchases land for the purpose of constructing a building, it considers all costs incurred up to the excavation for the new building as land costs. Removal of old buildings—clearing, grading, and filling—is a land cost because this activity is necessary to get the land in condition for its intended purpose. Home Depot treats any proceeds from getting the land ready for its intended use, such as salvage receipts on the demolition of an old building or the sale of cleared timber, as reductions in the price of the land.

In some cases, when Home Depot purchases land, it may assume certain obligations on the land such as back taxes or liens. In such situations, the cost of the land is the cash paid for it, plus the encumbrances. In other words, if the purchase price of the land is $50,000 cash but Home Depot assumes accrued property taxes of $5,000 and liens of $10,000, its land cost is $65,000.

Home Depot also might incur special assessments for local improvements, such as pavements, street lights, sewers, and drainage systems. It should charge these costs to the Land account because they are relatively permanent in nature. That is, after installation, they are maintained by the local government. In addition, Home Depot should charge any permanent improvements it makes, such as landscaping, to the Land account. It records separately any improvements with limited lives, such as private driveways, walks, fences, and parking lots, as Land Improvements. These costs are depreciated over their estimated lives.

Generally, land is part of property, plant, and equipment. However, if the major purpose of acquiring and holding land is speculative, a company more appropriately classifies the land as an investment. If a real estate concern holds the land for resale, it should classify the land as inventory.

In cases where land is held as an investment, what accounting treatment should be given for taxes, insurance, and other direct costs incurred while holding the land? Many believe these costs should be capitalized. The reason: They are not generating revenue from the investment at this time. Companies generally use this approach except when the asset is currently producing revenue (such as rental property).

Cost of Buildings

The cost of buildings should include all expenditures related directly to their acquisition or construction. These costs include (1) materials, labor, and overhead costs incurred during construction, and (2) professional fees and building permits. Generally, companies contract others to construct their buildings. Companies consider all costs incurred, from excavation to completion, as part of the building costs.

But how should companies account for an old building that is on the site of a newly proposed building? Is the cost of removal of the old building a cost of the land or a cost of the new building? Recall that if a company purchases land with an old building on it, then the cost of demolition less its salvage value is a cost of getting the land ready for its intended use and relates to the land rather than to the new building. In other words, all costs of getting an asset ready for its intended use are costs of that asset.

Cost of Equipment

The term “equipment” in accounting includes delivery equipment, office equipment, machinery, furniture and fixtures, furnishings, factory equipment, and similar fixed assets. The cost of such assets includes the purchase price, freight and handling charges incurred, insurance on the equipment while in transit, cost of special foundations if required, assembling and installation costs, and costs of conducting trial runs. Costs thus include all expenditures incurred in acquiring the equipment and preparing it for use.

Self-Constructed Assets

LEARNING OBJECTIVE ![]()

Describe the accounting problems associated with self-constructed assets.

Occasionally, companies construct their own assets. Determining the cost of such machinery and other fixed assets can be a problem. Without a purchase price or contract price, the company must allocate costs and expenses to arrive at the cost of the self-constructed asset. Materials and direct labor used in construction pose no problem. A company can trace these costs directly to work and material orders related to the fixed assets constructed.

However, the assignment of indirect costs of manufacturing creates special problems. These indirect costs, called overhead or burden, include power, heat, light, insurance, property taxes on factory buildings and equipment, factory supervisory labor, depreciation of fixed assets, and supplies.

Companies can handle indirect costs in one of two ways:

- Assign no fixed overhead to the cost of the constructed asset. The major argument for this treatment is that indirect overhead is generally fixed in nature. It does not increase as a result of a company constructing its own plant or equipment. This approach assumes that the company will have the same costs regardless of whether it constructs the asset or not. Therefore, to charge a portion of the overhead costs to the equipment will normally reduce current expenses and consequently overstate income of the current period. However, the company would assign to the cost of the constructed asset variable overhead costs that increase as a result of the construction.

- Assign a portion of all overhead to the construction process. This approach, called a full-costing approach, follows the belief that costs should attach to all products and assets manufactured or constructed. Under this approach, a company assigns a portion of all overhead to the construction process, as it would to normal production. Advocates say that failure to allocate overhead costs understates the initial cost of the asset and results in an inaccurate future allocation.

Companies should assign to the asset a pro rata portion of the fixed overhead to determine its cost. Companies use this treatment extensively because many believe that it results in a better recognition of these costs in periods benefited.

If the allocated overhead results in recording construction costs in excess of the costs that an outside independent producer would charge, the company should record the excess overhead as a period loss rather than capitalize it. This avoids capitalizing the asset at more than its probable fair value.2

Interest Costs During Construction

LEARNING OBJECTIVE ![]()

Describe the accounting problems associated with interest capitalization.

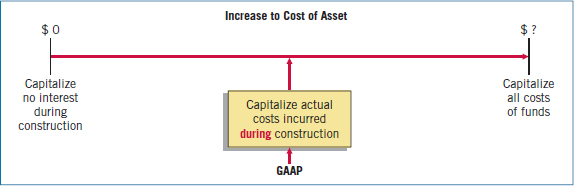

The proper accounting for interest costs has been a long-standing controversy. Three approaches have been suggested to account for the interest incurred in financing the construction of property, plant, and equipment:

- Capitalize no interest charges during construction. Under this approach, interest is considered a cost of financing and not a cost of construction. Some contend that if a company had used stock (equity) financing rather than debt, it would not incur this cost. The major argument against this approach is that the use of cash, whatever its source, has an associated implicit interest cost, which should not be ignored.

- Charge construction with all costs of funds employed, whether identifiable or not. This method maintains that the cost of construction should include the cost of financing, whether by cash, debt, or stock. Its advocates say that all costs necessary to get an asset ready for its intended use, including interest, are part of the asset's cost. Interest, whether actual or imputed, is a cost, just as are labor and materials. A major criticism of this approach is that imputing the cost of equity capital (stock) is subjective and outside the framework of an historical cost system.

- Capitalize only the actual interest costs incurred during construction. This approach agrees in part with the logic of the second approach—that interest is just as much a cost as are labor and materials. But this approach capitalizes only interest costs incurred through debt financing. (That is, it does not try to determine the cost of equity financing.) Under this approach, a company that uses debt financing will have an asset of higher cost than a company that uses stock financing. Some consider this approach unsatisfactory because they believe the cost of an asset should be the same whether it is financed with cash, debt, or equity.

Illustration 10-1 shows how a company might add interest costs (if any) to the cost of the asset under the three capitalization approaches.

GAAP requires the third approach—capitalizing actual interest (with modification). This method follows the concept that the historical cost of acquiring an asset includes all costs (including interest) incurred to bring the asset to the condition and location necessary for its intended use. The rationale for this approach is that during construction, the asset is not generating revenues. Therefore, a company should defer (capitalize) interest costs. [2] Once construction is complete, the asset is ready for its intended use and a company can earn revenues. At this point, the company should report interest as an expense and match it to these revenues. It follows that the company should expense any interest cost incurred in purchasing an asset that is ready for its intended use.

To implement this general approach, companies consider three items:

![]() Underlying Concepts

Underlying Concepts

The objective of capitalizing interest is to obtain a measure of acquisition cost that reflects a company's total investment in the asset and to charge that cost to future periods benefited.

- Qualifying assets.

- Capitalization period.

- Amount to capitalize.

Qualifying Assets

To qualify for interest capitalization, assets must require a period of time to get them ready for their intended use. A company capitalizes interest costs starting with the first expenditure related to the asset. Capitalization continues until the company substantially readies the asset for its intended use.

Assets that qualify for interest cost capitalization include assets under construction for a company's own use (including buildings, plants, and large machinery) and assets intended for sale or lease that are constructed or otherwise produced as discrete projects (e.g., ships or real estate developments).

Examples of assets that do not qualify for interest capitalization are (1) assets that are in use or ready for their intended use, and (2) assets that the company does not use in its earnings activities and that are not undergoing the activities necessary to get them ready for use. Examples of this second type include land remaining undeveloped and assets not used because of obsolescence, excess capacity, or need for repair.

Capitalization Period

![]() International Perspective

International Perspective

Recently, IFRS changed to require companies to capitalize borrowing costs related to qualifying assets. These changes were made as part of the IASB's and FASB's convergence project.

The capitalization period is the period of time during which a company must capitalize interest. It begins with the presence of three conditions:

- Expenditures for the asset have been made.

- Activities that are necessary to get the asset ready for its intended use are in progress.

- Interest cost is being incurred.

Interest capitalization continues as long as these three conditions are present. The capitalization period ends when the asset is substantially complete and ready for its intended use.

Amount to Capitalize

The amount of interest to capitalize is limited to the lower of actual interest cost incurred during the period or avoidable interest. Avoidable interest is the amount of interest cost during the period that a company could theoretically avoid if it had not made expenditures for the asset. If the actual interest cost for the period is $90,000 and the avoidable interest is $80,000, the company capitalizes only $80,000. Or, if the actual interest cost is $80,000 and the avoidable interest is $90,000, it still capitalizes only $80,000. In no situation should interest cost include a cost of capital charge for stockholders' equity. Furthermore, GAAP requires interest capitalization for a qualifying asset only if its effect, compared with the effect of expensing interest, is material. [3]

To apply the avoidable interest concept, a company determines the potential amount of interest that it may capitalize during an accounting period by multiplying the interest rate(s) by the weighted-average accumulated expenditures for qualifying assets during the period.

Weighted-Average Accumulated Expenditures. In computing the weighted-average accumulated expenditures, a company weights the construction expenditures by the amount of time (fraction of a year or accounting period) that it can incur interest cost on the expenditure.

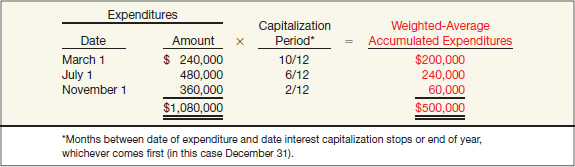

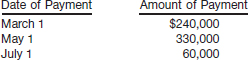

To illustrate, assume a 17-month bridge construction project with current-year payments to the contractor of $240,000 on March 1, $480,000 on July 1, and $360,000 on November 1. The company computes the weighted-average accumulated expenditures for the year ended December 31 as follows.

To compute the weighted-average accumulated expenditures, a company weights the expenditures by the amount of time that it can incur interest cost on each one. For the March 1 expenditure, the company associates 10 months' interest cost with the expenditure. For the expenditure on July 1, it incurs only 6 months' interest costs. For the expenditure made on November 1, the company incurs only 2 months of interest cost.

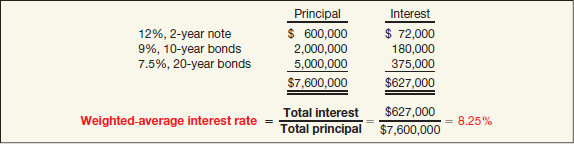

Interest Rates. Companies follow the below principles in selecting the appropriate interest rates to be applied to the weighted-average accumulated expenditures:

- For the portion of weighted-average accumulated expenditures that is less than or equal to any amounts borrowed specifically to finance construction of the assets, use the interest rate incurred on the specific borrowings.

- For the portion of weighted-average accumulated expenditures that is greater than any debt incurred specifically to finance construction of the assets, use a weighted average of interest rates incurred on all other outstanding debt during the period.3

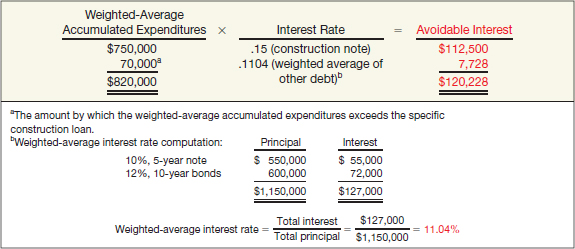

Illustration 10-3 shows the computation of a weighted-average interest rate for debt greater than the amount incurred specifically to finance construction of the assets.

Comprehensive Example of Interest Capitalization

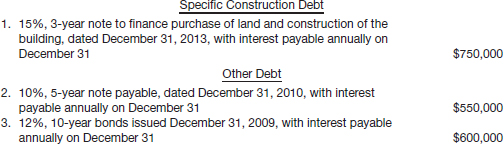

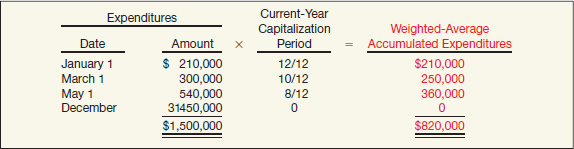

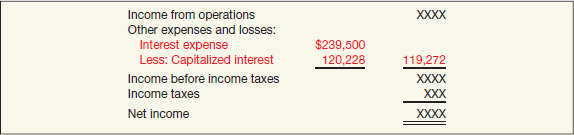

To illustrate the issues related to interest capitalization, assume that on November 1, 2013, Shalla Company contracted Pfeifer Construction Co. to construct a building for $1,400,000 on land costing $100,000 (purchased from the contractor and included in the first payment). Shalla made the following payments to the construction company during 2014.

![]()

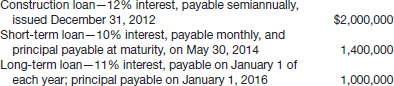

Pfeifer Construction completed the building, ready for occupancy, on December 31, 2014. Shalla had the following debt outstanding at December 31, 2014.

Shalla computed the weighted-average accumulated expenditures during 2014 as shown in Illustration 10-4.

Note that the expenditure made on December 31, the last day of the year, does not have any interest cost.

Shalla computes the avoidable interest as shown in Illustration 10-5.

The company determines the actual interest cost, which represents the maximum amount of interest that it may capitalize during 2014, as shown in Illustration 10-6.

The interest cost that Shalla capitalizes is the lesser of $120,228 (avoidable interest) and $239,500 (actual interest), or $120,228.

Shalla records the following journal entries during 2014:

Shalla should write off capitalized interest cost as part of depreciation over the useful life of the assets involved and not over the term of the debt. It should disclose the total interest cost incurred during the period, with the portion charged to expense and the portion capitalized indicated.

At December 31, 2014, Shalla discloses the amount of interest capitalized either as part of the nonoperating section of the income statement or in the notes accompanying the financial statements. We illustrate both forms of disclosure, in Illustrations 10-7 and 10-8.4

What do the numbers mean? WHAT’S IN YOUR INTEREST?

The requirement to capitalize interest can significantly impact financial statements. For example, when earnings of building manufacturer Jim Walter's Corporation dropped from $1.51 to $1.17 per share, the company offset 11 cents per share of the decline by capitalizing the interest on coal mining projects and several plants under construction.

How do statement users determine the impact of interest capitalization on a company's bottom line? They examine the notes to the financial statements. Companies with material interest capitalization must disclose the amounts of capitalized interest relative to total interest costs. For example, Anadarko Petroleum Corporation capitalized nearly 30 percent of its total interest costs in a recent year and provided the following footnote related to capitalized interest.

Financial Footnotes

Total interest costs incurred during the year were $82,415,000. Of this amount, the Company capitalized $24,716,000. Capitalized interest is included as part of the cost of oil and gas properties. The capitalization rates are based on the Company's weighted-average cost of borrowings used to finance the expenditures.

Special Issues Related to Interest Capitalization

Two issues related to interest capitalization merit special attention:

- Expenditures for land.

- Interest revenue.

![]() International Perspective

International Perspective

IFRS requires that interest revenue earned on specific borrowings should offset interest costs capitalized. The rationale is that the interest revenue earned is directly related to the interest cost incurred on the specific borrowing.

Expenditures for Land. When a company purchases land with the intention of developing it for a particular use, interest costs associated with those expenditures qualify for interest capitalization. If it purchases land as a site for a structure (such as a plant site), interest costs capitalized during the period of construction are part of the cost of the plant, not the land. Conversely, if the company develops land for lot sales, it includes any capitalized interest cost as part of the acquisition cost of the developed land. However, it should not capitalize interest costs involved in purchasing land held for speculation because the asset is ready for its intended use.

Interest Revenue. Companies frequently borrow money to finance construction of assets. They temporarily invest the excess borrowed funds in interest-bearing securities until they need the funds to pay for construction. During the early stages of construction, interest revenue earned may exceed the interest cost incurred on the borrowed funds.

Should companies offset interest revenue against interest cost when determining the amount of interest to capitalize as part of the construction cost of assets? In general, companies should not net or offset interest revenue against interest cost. Temporary or short-term investment decisions are not related to the interest incurred as part of the acquisition cost of assets. Therefore, companies should capitalize the interest incurred on qualifying assets whether or not they temporarily invest excess funds in short-term securities. Some criticize this approach because a company can defer the interest cost but report the interest revenue in the current period.

Observations

The interest capitalization requirement is still debated. From a conceptual viewpoint, many believe that, for the reasons mentioned earlier, companies should either capitalize no interest cost or all interest costs, actual or imputed.

VALUATION OF PROPERTY, PLANT, AND EQUIPMENT

LEARNING OBJECTIVE ![]()

Understand accounting issues related to acquiring and valuing plant assets.

Like other assets, companies should record property, plant, and equipment at the fair value of what they give up or at the fair value of the asset received, whichever is more clearly evident. However, the process of asset acquisition sometimes obscures fair value. For example, if a company buys land and buildings together for one price, how does it determine separate values for the land and buildings? We examine these types of accounting problems in the following sections.

Cash Discounts

When a company purchases plant assets subject to cash discounts for prompt payment, how should it report the discount? If it takes the discount, the company should consider the discount as a reduction in the purchase price of the asset. But should the company reduce the asset cost even if it does not take the discount?

Two points of view exist on this question. One approach considers the discount—whether taken or not—as a reduction in the cost of the asset. The rationale for this approach is that the real cost of the asset is the cash or cash equivalent price of the asset. In addition, some argue that the terms of cash discounts are so attractive that failure to take them indicates management error or inefficiency.

Proponents of the other approach argue that failure to take the discount should not always be considered a loss. The terms may be unfavorable, or it might not be prudent for the company to take the discount. At present, companies use both methods though most prefer the former method.

Deferred-Payment Contracts

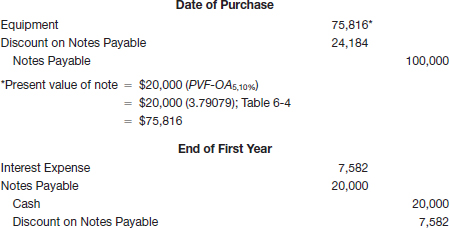

Companies frequently purchase plant assets on long-term credit contracts, using notes, mortgages, bonds, or equipment obligations. To properly reflect cost, companies account for assets purchased on long-term credit contracts at the present value of the consideration exchanged between the contracting parties at the date of the transaction.

For example, Greathouse Company purchases an asset today in exchange for a $10,000 zero-interest-bearing note payable four years from now. The company would not record the asset at $10,000. Instead, the present value of the $10,000 note establishes the exchange price of the transaction (the purchase price of the asset). Assuming an appropriate interest rate of 9 percent at which to discount this single payment of $10,000 due four years from now, Greathouse records this asset at $7,084.30 ($10,000 × .70843). [See Table 6-2 (page 337) for the present value of a single sum, PV = $10,000 (PVF4,9%).]

When no interest rate is stated or if the specified rate is unreasonable, the company imputes an appropriate interest rate. The objective is to approximate the interest rate that the buyer and seller would negotiate at arm's length in a similar borrowing transaction. In imputing an interest rate, companies consider such factors as the borrower's credit rating, the amount and maturity date of the note, and prevailing interest rates. The company uses the cash exchange price of the asset acquired (if determinable) as the basis for recording the asset and measuring the interest element.

To illustrate, Sutter Company purchases a specially built robot spray painter for its production line. The company issues a $100,000, five-year, zero-interest-bearing note to Wrigley Robotics, Inc. for the new equipment. The prevailing market rate of interest for obligations of this nature is 10 percent. Sutter is to pay off the note in five $20,000 installments, made at the end of each year. Sutter cannot readily determine the fair value of this specially built robot. Therefore, Sutter approximates the robot's value by establishing the fair value (present value) of the note. Entries for the date of purchase and dates of payments, plus computation of the present value of the note, are as follows.

Interest expense in the first year under the effective-interest approach is $7,582 [($100,000 − $24,184) × 10%]. The entry at the end of the second year to record interest and principal payment is as follows.

Interest expense in the second year under the effective-interest approach is $6,340 [($100,000 − $24,184) − ($20,000 − $7,582)] × 10%.

If Sutter did not impute an interest rate for deferred-payment contracts, it would record the asset at an amount greater than its fair value and overstate depreciation expense. In addition, Sutter would understate interest expense in the income statement for all periods involved.

Lump-Sum Purchases

A special problem of valuing fixed assets arises when a company purchases a group of plant assets at a single lump-sum price. When this common situation occurs, the company allocates the total cost among the various assets on the basis of their relative fair values. The assumption is that costs will vary in direct proportion to fair value. This is the same principle that companies apply to allocate a lump-sum cost among different inventory items.

To determine fair value, a company should use valuation techniques that are appropriate in the circumstances. In some cases, a single valuation technique will be appropriate. In other cases, multiple valuation approaches might have to be used.5

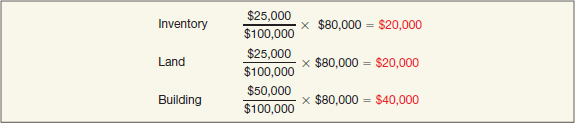

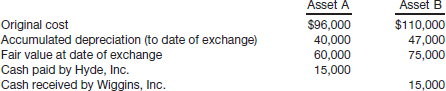

To illustrate, Norduct Homes, Inc. decides to purchase several assets of a small heating concern, Comfort Heating, for $80,000. Comfort Heating is in the process of liquidation. Its assets sold are:

Norduct Homes allocates the $80,000 purchase price on the basis of the relative fair values (assuming specific identification of costs is impracticable) in the following manner.

Issuance of Stock

When companies acquire property by issuing securities, such as common stock, the par or stated value of such stock fails to properly measure the property cost. If trading of the stock is active, the market price of the stock issued is a fair indication of the cost of the property acquired. The stock is a good measure of the current cash equivalent price.

For example, Upgrade Living Co. decides to purchase some adjacent land for expansion of its carpeting and cabinet operation. In lieu of paying cash for the land, the company issues to Deedland Company 5,000 shares of common stock (par value $10) that have a fair value of $12 per share. Upgrade Living Co. records the following entry.

![]()

If the company cannot determine the market price of the common stock exchanged, it establishes the fair value of the property. It then uses the value of the property as the basis for recording the asset and issuance of the common stock.

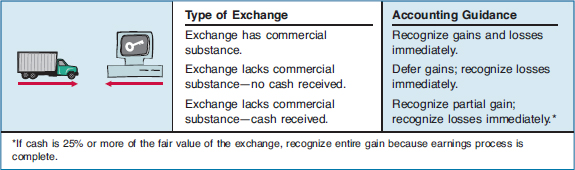

Exchanges of Nonmonetary Assets

The proper accounting for exchanges of nonmonetary assets, such as property, plant, and equipment, is controversial.6 Some argue that companies should account for these types of exchanges based on the fair value of the asset given up or the fair value of the asset received, with a gain or loss recognized. Others believe that they should account for exchanges based on the recorded amount (book value) of the asset given up, with no gain or loss recognized. Still others favor an approach that recognizes losses in all cases but defers gains in special situations.

Ordinarily, companies account for the exchange of nonmonetary assets on the basis of the fair value of the asset given up or the fair value of the asset received, whichever is clearly more evident. [5] Thus, companies should recognize immediately any gains or losses on the exchange. The rationale for immediate recognition is that most transactions have commercial substance, and therefore gains and losses should be recognized.

Meaning of Commercial Substance

![]() International Perspective

International Perspective

The FASB changed its accounting for exchanges to converge with IFRS. Previously, the FASB used a “similar in nature” criterion for exchanged assets to determine whether gains should be recognized. With use of the commercial substance test, GAAP and IFRS are now very similar.

As indicated above, fair value is the basis for measuring an asset acquired in a nonmonetary exchange if the transaction has commercial substance. An exchange has commercial substance if the future cash flows change as a result of the transaction. That is, if the two parties' economic positions change, the transaction has commercial substance.

For example, Andrew Co. exchanges some of its equipment for land held by Roddick Inc. It is likely that the timing and amount of the cash flows arising for the land will differ significantly from the cash flows arising from the equipment. As a result, both Andrew Co. and Roddick Inc. are in different economic positions. Therefore, the exchange has commercial substance, and the companies recognize a gain or loss on the exchange.

What if companies exchange similar assets, such as one truck for another truck? Even in an exchange of similar assets, a change in the economic position of the company can result. For example, let's say the useful life of the truck received is significantly longer than that of the truck given up. The cash flows for the trucks can differ significantly. As a result, the transaction has commercial substance, and the company should use fair value as a basis for measuring the asset received in the exchange.

However, it is possible to exchange similar assets but not have a significant difference in cash flows. That is, the company is in the same economic position as before the exchange. In that case, the company recognizes a loss but generally defers a gain.

As we will see in the following examples, use of fair value generally results in recognizing a gain or loss at the time of the exchange. Consequently, companies must determine if the transaction has commercial substance. To make this determination, they must carefully evaluate the cash flow characteristics of the assets exchanged.7

Illustration 10-10 summarizes asset exchange situations and the related accounting.

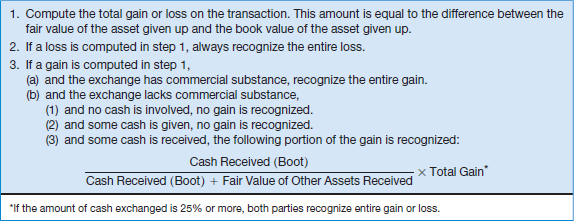

As Illustration 10-10 indicates, companies immediately recognize losses they incur on all exchanges. The accounting for gains depends on whether the exchange has commercial substance. If the exchange has commercial substance, the company recognizes the gain immediately. However, the profession modifies the rule for immediate recognition of a gain when an exchange lacks commercial substance: If the company receives no cash in such an exchange, it defers recognition of a gain. If the company receives cash in such an exchange, it recognizes part of the gain immediately.

To illustrate the accounting for these different types of transactions, we examine various loss and gain exchange situations.

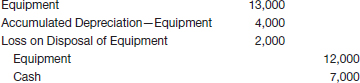

Exchanges—Loss Situation

When a company exchanges nonmonetary assets and a loss results, the company recognizes the loss immediately. The rationale: Companies should not value assets at more than their cash equivalent price. If the loss were deferred, assets would be overstated. Therefore, companies recognize a loss immediately whether the exchange has commercial substance or not.

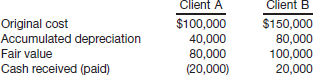

For example, Information Processing, Inc. trades its used machine for a new model at Jerrod Business Solutions Inc. The exchange has commercial substance. The used machine has a book value of $8,000 (original cost $12,000 less $4,000 accumulated depreciation) and a fair value of $6,000. The new model lists for $16,000. Jerrod gives Information Processing a trade-in allowance of $9,000 for the used machine. Information Processing computes the cost of the new asset as follows.

Information Processing records this transaction as follows.

We verify the loss on the disposal of the used machine as follows.

Why did Information Processing not use the trade-in allowance or the book value of the old asset as a basis for the new equipment? The company did not use the trade-in allowance because it included a price concession (similar to a price discount). Few individuals pay list price for a new car. Dealers such as Jerrod often inflate trade-in allowances on the used car so that actual selling prices fall below list prices. To record the car at list price would state it at an amount in excess of its cash equivalent price because of the new car's inflated list price. Similarly, use of book value in this situation would overstate the value of the new machine by $2,000.8

Exchanges—Gain Situation

Has Commercial Substance. Now let's consider the situation in which a nonmonetary exchange has commercial substance and a gain is realized. In such a case, a company usually records the cost of a nonmonetary asset acquired in exchange for another nonmonetary asset at the fair value of the asset given up and immediately recognizes a gain. The company should use the fair value of the asset received only if it is more clearly evident than the fair value of the asset given up.

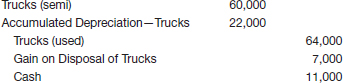

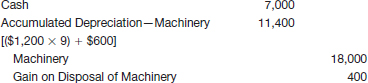

To illustrate, Interstate Transportation Company exchanged a number of used trucks plus cash for a semi-truck. The used trucks have a combined book value of $42,000 (cost $64,000 less $22,000 accumulated depreciation). Interstate's purchasing agent, experienced in the secondhand market, indicates that the used trucks have a fair value of $49,000. In addition to the trucks, Interstate must pay $11,000 cash for the semi-truck. Interstate computes the cost of the semi-truck as follows.

Interstate records the exchange transaction as follows.

The gain is the difference between the fair value of the used trucks and their book value. We verify the computation as follows.

In this case, Interstate is in a different economic position, and therefore the transaction has commercial substance. Thus, it recognizes a gain.

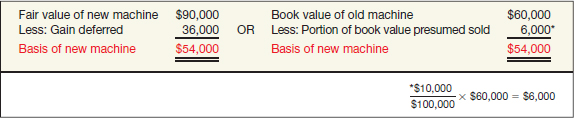

Lacks Commercial Substance—No Cash Received. We now assume that the Interstate Transportation Company exchange lacks commercial substance. That is, the economic position of Interstate did not change significantly as a result of this exchange. In this case, Interstate defers the gain of $7,000 and reduces the basis of the semi-truck. Illustration 10-15 shows two different but acceptable computations to illustrate this reduction.

Interstate records this transaction as follows.

If the exchange lacks commercial substance, the company recognizes the gain (reflected in the basis of the semi-truck) through lower depreciation expense or when it later sells the semi-truck, not at the time of the exchange.

Lacks Commercial Substance—Some Cash Received. When a company receives cash (sometimes referred to as “boot”) in an exchange that lacks commercial substance, it must immediately recognize a portion of the gain.9 Illustration 10-16 shows the general formula for gain recognition when an exchange includes some cash.

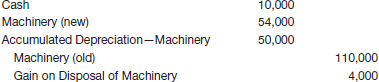

To illustrate, assume that Queenan Corporation traded in used machinery with a book value of $60,000 (cost $110,000 less accumulated depreciation $50,000) and a fair value of $100,000. It receives in exchange a machine with a fair value of $90,000 plus cash of $10,000. Illustration 10-17 shows calculation of the total gain on the exchange.

Generally, when a transaction lacks commercial substance, a company defers any gain. But because Queenan received $10,000 in cash, it recognizes a partial gain. The portion of the gain a company recognizes is the ratio of monetary assets (cash in this case) to the total consideration received. Queenan computes the partial gain as follows.

ILLUSTRATION 10-18 Computation of Gain Based on Ratio of Cash Received to Total Consideration Received

![]()

Because Queenan recognizes only a gain of $4,000 on this transaction, it defers the remaining $36,000 ($40,000 − $4,000) and reduces the basis (recorded cost) of the new machine. Illustration 10-19 shows the computation of the basis.

Queenan records the transaction with the following entry.

The rationale for the treatment of a partial gain is as follows. Before a nonmonetary exchange that includes some cash, a company has an unrecognized gain, which is the difference between the book value and the fair value of the old asset. When the exchange occurs, a portion of the fair value is converted to a more liquid asset. The ratio of this liquid asset to the total consideration received is the portion of the total gain that the company realizes. Thus, the company recognizes and records that amount.

Illustration 10-20 presents in summary form the accounting requirements for recognizing gains and losses on exchanges of nonmonetary assets.10

Companies disclose in their financial statements nonmonetary exchanges during a period. Such disclosure indicates the nature of the transaction(s), the method of accounting for the assets exchanged, and gains or losses recognized on the exchanges. [7]

What do the numbers mean? ABOUT THOSE SWAPS

In a press release, Roy Olofson, former vice president of finance for Global Crossing, accused company executives of improperly describing the company's revenue to the public. He said the company had improperly recorded long-term sales immediately rather than over the term of the contract, had improperly booked as cash transactions swaps of capacity with other carriers, and had fired him when he blew the whistle.

The accounting for the swaps involves exchanges of similar network capacity. Companies have said they engage in such deals because swapping is quicker and less costly than building segments of their own networks, or because such pacts provide redundancies to make their own networks more reliable. In one expert's view, an exchange of similar network capacity is the equivalent of trading a blue truck for a red truck—it shouldn't boost a company's revenue.

But Global Crossing and Qwest, among others, counted as revenue the money received from the other company in the swap. (In general, in transactions involving leased capacity, the companies booked the revenue over the life of the contract.) Some of these companies then treated their own purchases as capital expenditures, which were not run through the income statement. Instead, the spending led to the addition of assets on the balance sheet (and an inflated bottom line).

The SEC questioned some of these capacity exchanges, because it appeared they were a device to pad revenue. This reaction was not surprising, since revenue growth was a key factor in the valuation of companies such as Global Crossing and Qwest during the craze for tech stocks in the late 1990s and 2000.

Source: Adapted from Henny Sender, “Telecoms Draw Focus for Moves in Accounting,” Wall Street Journal (March 26, 2002), p. C7.

Accounting for Contributions

Companies sometimes receive or make contributions (donations or gifts). Such contributions, nonreciprocal transfers, transfer assets in one direction. A contribution is often some type of asset (such as cash, securities, land, buildings, or use of facilities), but it also could be the forgiveness of a debt.

When companies acquire assets as donations, a strict cost concept dictates that the valuation of the asset should be zero. However, a departure from the historical cost principle seems justified; the only costs incurred (legal fees and other relatively minor expenditures) are not a reasonable basis of accounting for the assets acquired. To record nothing is to ignore the economic realities of an increase in wealth and assets. Therefore, companies use the fair value of the asset to establish its value on the books.

![]() International Perspective

International Perspective

IFRS provides detailed guidance on how to account for contributions and government grants.

What then is the proper accounting for the credit in this transaction? Some believe the credit should be made to Donated Capital (an additional paid-in capital account). This approach views the increase in assets from a donation as contributed capital, rather than as earned revenue.

Others argue that companies should report donations as revenues from contributions. Their reasoning is that only the owners of a business contribute capital. At issue in this approach is whether the company should report revenue immediately or over the period that the asset is employed. For example, to attract new industry a city may offer land, but the receiving enterprise may incur additional costs in the future (e.g., transportation or higher state income taxes) because the location is not the most desirable. As a consequence, some argue that the company should defer the revenue and recognize it as the costs are incurred.

The FASB's position is that in general, companies should recognize contributions received as revenues in the period received. [8]11 Companies measure contributions at the fair value of the assets received. [9] To illustrate, Max Wayer Meat Packing, Inc. has recently accepted a donation of land with a fair value of $150,000 from the Memphis Industrial Development Corp. In return, Max Wayer Meat Packing promises to build a packing plant in Memphis. Max Wayer's entry is:

![]()

When a company contributes a nonmonetary asset, it should record the amount of the donation as an expense at the fair value of the donated asset. If a difference exists between the fair value of the asset and its book value, the company should recognize a gain or loss. To illustrate, Kline Industries donates land to the city of Los Angeles for a city park. The land cost $80,000 and has a fair value of $110,000. Kline Industries records this donation as follows.

![]()

In some cases, companies promise to give (pledge) some type of asset in the future. Should companies record this promise immediately or when they give the assets? If the promise is unconditional (depends only on the passage of time or on demand by the recipient for performance), the company should report the contribution expense and related payable immediately. If the promise is conditional, the company recognizes expense in the period benefited by the contribution, generally when it transfers the asset.

Other Asset Valuation Methods

The exception to the historical cost principle for assets acquired through donation is based on fair value. Another exception is the prudent cost concept. This concept states that if for some reason a company ignorantly paid too much for an asset originally, it is theoretically preferable to charge a loss immediately.

For example, assume that a company constructs an asset at a cost much greater than its present economic usefulness. It would be appropriate to charge these excess costs as a loss to the current period, rather than capitalize them as part of the cost of the asset. In practice, the need to use the prudent cost approach seldom develops. Companies typically either use good reasoning in paying a given price or fail to recognize that they have overpaid.

What happens, on the other hand, if a company makes a bargain purchase or internally constructs a piece of equipment at a cost savings? Such savings should not result in immediate recognition of a gain under any circumstances.

COSTS SUBSEQUENT TO ACQUISITION

LEARNING OBJECTIVE ![]()

Describe the accounting treatment for costs subsequent to acquisition.

After installing plant assets and readying them for use, a company incurs additional costs that range from ordinary repairs to significant additions. The major problem is allocating these costs to the proper time periods. In general, costs incurred to achieve greater future benefits should be capitalized, whereas expenditures that simply maintain a given level of services should be expensed. In order to capitalize costs, one of three conditions must be present:

- The useful life of the asset must be increased.

- The quantity of units produced from the asset must be increased.

- The quality of the units produced must be enhanced.

For example, a company like Boeing should expense expenditures that do not increase an asset's future benefits. That is, it expenses immediately ordinary repairs that maintain the existing condition of the asset or restore it to normal operating efficiency.

![]() Underlying Concepts

Underlying Concepts

Expensing long-lived wastepaper baskets is an application of the materiality concept.

Companies expense most expenditures below an established arbitrary minimum amount, say, $100 or $500. Although conceptually this treatment may be incorrect, expediency demands it. Otherwise, companies would set up depreciation schedules for an item such as a wastepaper basket.

The distinction between a capital expenditure (asset) and a revenue expenditure (expense) is not always clear-cut. Yet, in most cases, consistent application of a capital/expense policy is more important than attempting to provide general theoretical guidelines for each transaction. Generally, companies incur four major types of expenditures relative to existing assets.

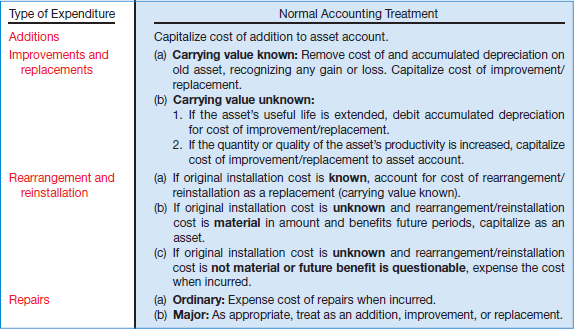

MAJOR TYPES OF EXPENDITURES

ADDITIONS. Increase or extension of existing assets.

IMPROVEMENTS AND REPLACEMENTS. Substitution of an improved asset for an existing one.

REARRANGEMENT AND REINSTALLATION. Movement of assets from one location to another.

REPAIRS. Expenditures that maintain assets in condition for operation.

What do the numbers mean? DISCONNECTED

It all started with a check of the books by an internal auditor for WorldCom Inc. The telecom giant's newly installed chief executive had asked for a financial review, and the auditor was spot-checking records of capital expenditures. She found the company was using an unorthodox technique to account for one of its biggest expenses: charges paid to local telephone networks to complete long-distance calls.

Instead of recording these charges as operating expenses, WorldCom recorded a significant portion as capital expenditures. The maneuver was worth hundreds of millions of dollars to WorldCom's bottom line. It effectively turned a loss for all of 2001 and the first quarter of 2002 into a profit. The graph below compares WorldCom's accounting to that under GAAP. Soon after this discovery, WorldCom filed for bankruptcy.

Source: Adapted from Jared Sandberg, Deborah Solomon, and Rebecca Blumenstein, “Inside WorldCom's Unearthing of a Vast Accounting Scandal,” Wall Street Journal (June 27, 2002), p. A1.

Additions

Additions should present no major accounting problems. By definition, companies capitalize any addition to plant assets because a new asset is created. For example, the addition of a wing to a hospital, or of an air conditioning system to an office, increases the service potential of that facility. Companies should capitalize such expenditures and match them against the revenues that will result in future periods.

One problem that arises in this area is the accounting for any changes related to the existing structure as a result of the addition. Is the cost incurred to tear down an old wall, to make room for the addition, a cost of the addition or an expense or loss of the period? The answer is that it depends on the original intent. If the company had anticipated building an addition later, then this cost of removal is a proper cost of the addition. But if the company had not anticipated this development, it should properly report the removal as a loss in the current period on the basis of inefficient planning. Normally, the company retains the carrying amount of the old wall in the accounts, although theoretically the company should remove it.

Improvements and Replacements

Companies substitute one asset for another through improvements and replacements. What is the difference between an improvement and a replacement? An improvement (betterment) is the substitution of a better asset for the one currently used (say, a concrete floor for a wooden floor). A replacement, on the other hand, is the substitution of a similar asset (a wooden floor for a wooden floor).

Many times improvements and replacements result from a general policy to modernize or rehabilitate an older building or piece of equipment. The problem is differentiating these types of expenditures from normal repairs. Does the expenditure increase the future service potential of the asset? Or does it merely maintain the existing level of service? Frequently, the answer is not clear-cut. Good judgment is required to correctly classify these expenditures.

If the expenditure increases the future service potential of the asset, a company should capitalize it. The accounting is therefore handled in one of three ways, depending on the circumstances:

- Use the substitution approach. Conceptually, the substitution approach is correct if the carrying amount of the old asset is available. It is then a simple matter to remove the cost of the old asset and replace it with the cost of the new asset.

To illustrate, Instinct Enterprises decides to replace the pipes in its plumbing system. A plumber suggests that the company use plastic tubing in place of the cast iron pipes and copper tubing. The old pipe and tubing have a book value of $15,000 (cost of $150,000 less accumulated depreciation of $135,000), and a scrap value of $1,000. The plastic tubing costs $125,000. If Instinct pays $124,000 for the new tubing after exchanging the old tubing, it makes the following entry:

The problem is determining the book value of the old asset. Generally, the components of a given asset depreciate at different rates. However, generally no separate accounting is made. For example, the tires, motor, and body of a truck depreciate at different rates, but most companies use one rate for the entire truck. Companies can set separate depreciation rates, but it is often impractical. If a company cannot determine the carrying amount of the old asset, it adopts one of two other approaches.

- Capitalize the new cost. Another approach capitalizes the improvement and keeps the carrying amount of the old asset on the books. The justification for this approach is that the item is sufficiently depreciated to reduce its carrying amount almost to zero. Although this assumption may not always be true, the differences are often insignificant. Companies usually handle improvements in this manner.

- Charge to accumulated depreciation. In cases when a company does not improve the quantity or quality of the asset itself but instead extends its useful life, the company debits the expenditure to Accumulated Depreciation rather than to an asset account. The theory behind this approach is that the replacement extends the useful life of the asset and thereby recaptures some or all of the past depreciation. The net carrying amount of the asset is the same whether debiting the asset or accumulated depreciation.

Rearrangement and Reinstallation

Companies incur rearrangement and reinstallation costs to benefit future periods. An example is the rearrangement and reinstallation of machines to facilitate future production.

If a company like The Coca-Cola Company can determine or estimate the original installation cost and the accumulated depreciation to date, it handles the rearrangement and reinstallation cost as a replacement. If not, which is generally the case, Coca-Cola should capitalize the new costs (if material in amount) as an asset to be amortized over future periods expected to benefit. If these costs are immaterial, if they cannot be separated from other operating expenses, or if their future benefit is questionable, the company should immediately expense them.

Repairs

A company makes ordinary repairs to maintain plant assets in operating condition. It charges ordinary repairs to an expense account in the period incurred, on the basis that it is the primary period benefited. Maintenance charges that occur regularly include replacing minor parts, lubricating and adjusting equipment, repainting, and cleaning. A company treats these as ordinary operating expenses.

It is often difficult to distinguish a repair from an improvement or replacement. The major consideration is whether the expenditure benefits more than one year or one operating cycle, whichever is longer. If a major repair (such as an overhaul) occurs, several periods will benefit. A company should handle the cost as an addition, improvement, or replacement.12

An interesting question is whether a company can accrue planned maintenance overhaul costs before the actual costs are incurred. For example, assume that Southwest Airlines schedules major overhauls of its planes every three years. Should Southwest be permitted to accrue these costs and related liability over the three-year period? Some argue that this accrue-in-advance approach better matches expenses to revenues and reports Southwest's obligation for these costs. However, reporting a liability is inappropriate. To whom does Southwest owe? In other words, Southwest has no obligation to an outside party until it has to pay for the overhaul costs, and therefore it has no liability. As a result, companies are not permitted to accrue in advance for planned major overhaul costs either for interim or annual periods. [10]

Summary of Costs Subsequent to Acquisition

Illustration 10-21 summarizes the accounting treatment for various costs incurred subsequent to the acquisition of capitalized assets.

DISPOSITION OF PROPERTY, PLANT, AND EQUIPMENT

LEARNING OBJECTIVE ![]()

Describe the accounting treatment for the disposal of property, plant, and equipment.

A company, like Intel, may retire plant assets voluntarily or dispose of them by sale, exchange, involuntary conversion, or abandonment. Regardless of the type of disposal, depreciation must be taken up to the date of disposition. Then, Intel should remove all accounts related to the retired asset. Generally, the book value of the specific plant asset does not equal its disposal value. As a result, a gain or loss develops.

The reason: Depreciation is an estimate of cost allocation and not a process of valuation. The gain or loss is really a correction of net income for the years during which Intel used the fixed asset.

Intel should show gains or losses on the disposal of plant assets in the income statement along with other items from customary business activities. However, if it sold, abandoned, spun off, or otherwise disposed of the “operations of a component of a business,” then it should report the results separately in the discontinued operations section of the income statement (as discussed in Chapter 4). That is, Intel should report any gain or loss from disposal of a business component with the related results of discontinued operations.

Sale of Plant Assets

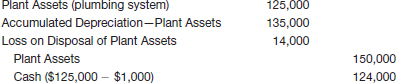

Companies record depreciation for the period of time between the date of the last depreciation entry and the date of sale. To illustrate, assume that Barret Company recorded depreciation on a machine costing $18,000 for 9 years at the rate of $1,200 per year. If it sells the machine in the middle of the tenth year for $7,000, Barret records depreciation to the date of sale as:

![]()

The entry for the sale of the asset then is:

The book value of the machinery at the time of the sale is $6,600 ($18,000 − $11,400). Because the machinery sold for $7,000, the amount of the gain on the sale is $400.

Involuntary Conversion

Sometimes an asset's service is terminated through some type of involuntary conversion such as fire, flood, theft, or condemnation. Companies report the difference between the amount recovered (e.g., from a condemnation award or insurance recovery), if any, and the asset's book value as a gain or loss. They treat these gains or losses like any other type of disposition. In some cases, these gains or losses may be reported as extraordinary items in the income statement if the conditions of the disposition are unusual and infrequent in nature.

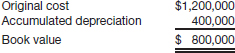

To illustrate, Camel Transport Corp. had to sell a plant located on company property that stood directly in the path of an interstate highway. For a number of years, the state had sought to purchase the land on which the plant stood, but the company resisted. The state ultimately exercised its right of eminent domain, which the courts upheld. In settlement, Camel received $500,000, which substantially exceeded the $200,000 book value of the plant and land (cost of $400,000 less accumulated depreciation of $200,000). Camel made the following entry.

If the conditions surrounding the condemnation are judged to be unusual and infrequent, Camel's gain of $300,000 is reported as an extraordinary item.

Some object to the recognition of a gain or loss in certain involuntary conversions. For example, the federal government often condemns forests for national parks. The paper companies that owned these forests must report a gain or loss on the condemnation. However, companies such as Georgia-Pacific contend that no gain or loss should be reported because they must replace the condemned forest land immediately and so are in the same economic position as they were before. The issue is whether condemnation and subsequent purchase should be viewed as one or two transactions. GAAP requires “that a gain or loss be recognized when a nonmonetary asset is involuntarily converted to monetary assets even though an enterprise reinvests or is obligated to reinvest the monetary assets in replacement nonmonetary assets.” [11]

Miscellaneous Problems

If a company scraps or abandons an asset without any cash recovery, it recognizes a loss equal to the asset's book value. If scrap value exists, the gain or loss that occurs is the difference between the asset's scrap value and its book value. If an asset still can be used even though it is fully depreciated, it may be kept on the books at historical cost less depreciation.

Companies must disclose in notes to the financial statements the amount of fully depreciated assets in service. For example, Petroleum Equipment Tools Inc. in its annual report disclosed, “The amount of fully depreciated assets included in property, plant, and equipment at December 31 amounted to approximately $98,900,000.”

KEY TERMS

avoidable interest, 542

capital expenditure, 557

capitalization period, 542

commercial substance, 550

fixed assets, 538

historical cost, 538

improvements (betterments), 558

involuntary conversion, 561

lump-sum price, 548

major repairs, 559

nonmonetary assets, 550

nonreciprocal transfers, 555

ordinary repairs, 559

plant assets, 538

property, plant, and equipment, 538

prudent cost, 556

rearrangement and reinstallation costs, 559

replacements, 558

revenue expenditure, 557

self-constructed asset, 540

weighted-average accumulated expenditures, 543

SUMMARY OF LEARNING OBJECTIVES

![]() Describe property, plant, and equipment. The major characteristics of property, plant, and equipment are as follows. (1) They are acquired for use in operations and not for resale. (2) They are long-term in nature and usually subject to depreciation. (3) They possess physical substance.

Describe property, plant, and equipment. The major characteristics of property, plant, and equipment are as follows. (1) They are acquired for use in operations and not for resale. (2) They are long-term in nature and usually subject to depreciation. (3) They possess physical substance.

![]() Identify the costs to include in initial valuation of property, plant, and equipment. The costs included in initial valuation of property, plant, and equipment are as follows.

Identify the costs to include in initial valuation of property, plant, and equipment. The costs included in initial valuation of property, plant, and equipment are as follows.

Cost of land: Includes all expenditures made to acquire land and to ready it for use. Land costs typically include (1) the purchase price; (2) closing costs, such as title to the land, attorney's fees, and recording fees; (3) costs incurred in getting the land in condition for its intended use, such as grading, filling, draining, and clearing; (4) assumption of any liens, mortgages, or encumbrances on the property; and (5) any additional land improvements that have an indefinite life.

Cost of buildings: Includes all expenditures related directly to their acquisition or construction. These costs include (1) materials, labor, and overhead costs incurred during construction, and (2) professional fees and building permits.

Cost of equipment: Includes the purchase price, freight and handling charges incurred, insurance on the equipment while in transit, cost of special foundations if required, assembling and installation costs, and costs of conducting trial runs.

![]() Describe the accounting problems associated with self-constructed assets. Indirect costs of manufacturing create special problems because companies cannot easily trace these costs directly to work and material orders related to the constructed assets. Companies might handle these costs in one of two ways. (1) Assign no fixed overhead to the cost of the constructed asset, or (2) assign a portion of all overhead to the construction process. Companies use the second method extensively.

Describe the accounting problems associated with self-constructed assets. Indirect costs of manufacturing create special problems because companies cannot easily trace these costs directly to work and material orders related to the constructed assets. Companies might handle these costs in one of two ways. (1) Assign no fixed overhead to the cost of the constructed asset, or (2) assign a portion of all overhead to the construction process. Companies use the second method extensively.

![]() Describe the accounting problems associated with interest capitalization. Only actual interest (with modifications) should be capitalized. The rationale for this approach is that during construction, the asset is not generating revenue and therefore companies should defer (capitalize) interest cost. Once construction is completed, the asset is ready for its intended use and revenues can be recognized. Any interest cost incurred in purchasing an asset that is ready for its intended use should be expensed.

Describe the accounting problems associated with interest capitalization. Only actual interest (with modifications) should be capitalized. The rationale for this approach is that during construction, the asset is not generating revenue and therefore companies should defer (capitalize) interest cost. Once construction is completed, the asset is ready for its intended use and revenues can be recognized. Any interest cost incurred in purchasing an asset that is ready for its intended use should be expensed.

![]() Understand accounting issues related to acquiring and valuing plant assets. The following issues relate to acquiring and valuing plant assets. (1) Cash discounts: Whether taken or not, they are generally considered a reduction in the cost of the asset; the real cost of the asset is the cash or cash equivalent price of the asset. (2) Deferred-payment contracts: Companies account for assets purchased on long-term credit contracts at the present value of the consideration exchanged between the contracting parties. (3) Lump-sum purchase: Allocate the total cost among the various assets on the basis of their relative fair values. (4) Issuance of stock: If the stock is actively traded, the market price of the stock issued is a fair indication of the cost of the property acquired. If the market price of the common stock exchanged is not determinable, establish the fair value of the property and use it as the basis for recording the asset and issuance of the common stock. (5) Exchanges of nonmonetary assets: The accounting for exchanges of nonmonetary assets depends on whether the exchange has commercial substance. See Illustrations 10-10 (page 551) and 10-20 (page 554) for summaries of how to account for exchanges. (6) Contributions: Record at the fair value of the asset received, and credit revenue for the same amount.

Understand accounting issues related to acquiring and valuing plant assets. The following issues relate to acquiring and valuing plant assets. (1) Cash discounts: Whether taken or not, they are generally considered a reduction in the cost of the asset; the real cost of the asset is the cash or cash equivalent price of the asset. (2) Deferred-payment contracts: Companies account for assets purchased on long-term credit contracts at the present value of the consideration exchanged between the contracting parties. (3) Lump-sum purchase: Allocate the total cost among the various assets on the basis of their relative fair values. (4) Issuance of stock: If the stock is actively traded, the market price of the stock issued is a fair indication of the cost of the property acquired. If the market price of the common stock exchanged is not determinable, establish the fair value of the property and use it as the basis for recording the asset and issuance of the common stock. (5) Exchanges of nonmonetary assets: The accounting for exchanges of nonmonetary assets depends on whether the exchange has commercial substance. See Illustrations 10-10 (page 551) and 10-20 (page 554) for summaries of how to account for exchanges. (6) Contributions: Record at the fair value of the asset received, and credit revenue for the same amount.

![]() Describe the accounting treatment for costs subsequent to acquisition. Illustration 10-21 (page 560) summarizes how to account for costs subsequent to acquisition.

Describe the accounting treatment for costs subsequent to acquisition. Illustration 10-21 (page 560) summarizes how to account for costs subsequent to acquisition.

![]() Describe the accounting treatment for the disposal of property, plant, and equipment. Regardless of the time of disposal, companies take depreciation up to the date of disposition and then remove all accounts related to the retired asset. Gains or losses on the retirement of plant assets are shown in the income statement along with other items that arise from customary business activities. Gains or losses on involuntary conversions, if unusual and infrequent, may be reported as extraordinary items.

Describe the accounting treatment for the disposal of property, plant, and equipment. Regardless of the time of disposal, companies take depreciation up to the date of disposition and then remove all accounts related to the retired asset. Gains or losses on the retirement of plant assets are shown in the income statement along with other items that arise from customary business activities. Gains or losses on involuntary conversions, if unusual and infrequent, may be reported as extraordinary items.

DEMONSTRATION PROBLEM

Columbia Company, which manufactures machine tools, had the following transactions related to plant assets in 2014.

Asset A: On June 2, 2014, Columbia purchased a stamping machine at a retail price of $12,000. Columbia paid 6% sales tax on this purchase. Columbia paid a contractor $2,800 for a specially wired platform for the machine, to ensure noninterrupted power to the machine. Columbia estimates the machine will have a 4-year useful life, with a salvage value of $2,000 at the end of 4 years. The machine was put into use on July 1, 2014.

Asset B: On January 1, 2014, Columbia, Inc. signed a fixed-price contract for construction of a warehouse facility at a cost of $1,000,000. It was estimated that the project will be completed by December 31, 2014. On March 1, 2014, to finance the construction cost, Columbia borrowed $1,000,000 payable April 1, 2015, plus interest at the rate of 10%. During 2014, Columbia made deposit and progress payments totaling $750,000 under the contract; the weighted-average amount of accumulated expenditures was $400,000 for the year. The excess-borrowed funds were invested in short-term securities, from which Columbia realized investment revenue of $13,000. The warehouse was completed on December 1, 2014, at which time Columbia made the final payment to the contractor. Columbia estimates the warehouse will have a 25-year useful life, with a salvage value of $20,000.

Columbia uses straight-line depreciation and employs the “half-year” convention in accounting for partial-year depreciation. Columbia's fiscal year ends on December 31.

Instructions

(a) At what amount should Columbia record the acquisition cost of the machine?

(b) What amount of capitalized interest should Columbia include in the cost of the warehouse?

(c) On July 1, 2016, Columbia decides to outsource its stamping operation to Medek, Inc. As part of this plan, Columbia sells the machine (and the platform) to Medek, Inc. for $7,000. What is the impact of this disposal on Columbia's 2016 income before taxes?

Solution

(a) Historical cost is measured by the cash or cash equivalent price of obtaining the asset and bringing it to the location and condition for its intended use. For Columbia, this is:

(b) $40,000 ($400,000 × .10)—Weighted-Average Accumulated Expenditures × Interest Rate = Avoidable Interest