APPENDIX I

Sponsor/Originator: CNH Capital America LLC.

Servicer: New Holland Credit Company, LLC.

Backup Servicer: Systems & Services Technologies, Inc.

Indenture Trustee: JP Morgan Chase Bank.

Trustee: The Bank of New York.

■ Noteworthy Changes

- Decline in Enhancement Levels: Initial enhancement has been reduced by 65 basis points (bps) for the class A notes and 125 bps for the class B notes from the closing levels in the CNH 2005-B transaction. The 2006-A transaction will not include a class C tranche, which provided subordination for the class A and B notes in the prior transactions. These reductions in enhancement are the net result of changes in the size of the class B notes (decrease of 60 bps), removal of class C notes (decline of 100 bps) and a reduction in the reserve account of 25 bps.

When sizing enhancement levels, Fitch took into consideration, among other things, the continually improving static-loss performance of both new and used agricultural and construction equipment, the collateral characteristics and certain structural features of the 2006-A transaction. These features include a $387 million prefunding amount (approximately 33.6% of initial receivables). Fitch notes that, given the size of the prefunding amount, the addition of new loans should not significantly affect closing date pool characteristics and concentrations. - Shifting Payment Priority: The 2006-A transaction incorporates a shifting payment priority, where initially principal is distributed sequentially between the class A and B notes. However, if the class A notes are ever undercollateralized, interest allocable to the class B notes is made available to pay class A principal (see the Principal Allocation section on page 7). Once collateralization is restored, the class B notes will resume interest payments. The 2005-B transaction included a fully sequential payment priority.

- Reserve Account Step-Down Trigger: Similar to the 2005-B transaction, the 2006-A structure incorporates a reserve step-down feature whereby the reserve account will step down by 25 bps (floored) to 1.25% in month 24 or 30, as long as the collateral performs as expected and does not hit certain defined performance triggers. In the 2005-B transaction, the reserve account stepped down 25 bps (capped) on the 18th, 24th or 30th month. The step-down trigger is fully explained in the Reserve Account section on page 6.

- The Discount Rate: The discount rate utilized in the 2006-A transaction is 7.80%, 80 bps greater than the 2005-B transaction. However, excess spread remains virtually the same in the 2006-A transaction (1.65% per annum [p.a.]) when compared with the 2005-B transaction (1.62% p.a.).

■ CNH Global N.V.

- Role: Parent of seller/servicer.

- Risk to Transaction: As parent company of servicer, bankruptcy may invoke a servicer transfer.

- Mitigants: Strong financial performance and condition.

CNH is a leading manufacturer of agricultural and construction equipment whose products (including brands such as Case, Case IH, New Holland and Kobelco) are sold in more than 160 countries through a network of more than 11,400 dealers and distributors worldwide. CNH was formed in 1999 in connection with New Holland N.V.'s acquisition of Case Corporation.

CNH's three primary business segments are as follows:

- Agricultural Equipment: CNH manufactures a broad range of equipment used in farm and livestock operations, as well as equipment for large-scale growers, utility producers, and orchard and livestock operations.

- Construction Equipment: CNH manufactures heavy construction and light industrial equipment for use in road building, mining, demolition, excavation and commercial building.

- Financial Services: CNH Capital and New Holland Credit provide financing for new and used agricultural, construction and other equipment to dealers and customers. Various forms of insurance are also available to customers and dealers to help support the purchase and lease of equipment.

As of Dec., 31 2005, CNH reported revenues of $12.6 billion. FIAT S.p.A. owns approximately 85% of the stock of CNH. (For more information, see the press release, “Fitch Affirms Fiat's Ratings On Deal With GM,” dated Feb. 14, 2004, and available on Fitch's Web site at www.fitchratings.com.).

■ CNH Capital America LLC

- Role: Seller (CNH Capital)/servicer (New Holland Credit)

- Risk to Transaction: New Holland Credit as servicer, transaction's performance is strongly tied to New Holland maintaining servicing rights.

- Mitigants: Stresses and credit enhancement, as well as New Holland's experience as a servicer on prior transactions.

On Dec. 31, 2004, Case Credit Corporation was converted into CNH Capital, which is an indirect wholly owned subsidiary of CNH and provides financing to customers and dealers for the purchase and lease of CNH equipment. New Holland Credit is an indirect, wholly owned subsidiary of CNH and provides equipment financing to customers and dealers. As servicer of the 2006-A transaction, New Holland Credit will receive a servicing fee each month equal to one-twelfth of 1.00% of the pool balance as of the first day of the preceding calendar month.

■ Legal Structure

Fitch believes the legal structure of the transaction ensures that the bankruptcy of CNH would not impair the timeliness of payments on the securities. Fitch expects to receive and review legal opinions to the effect that the transfer of loans to the trust will constitute a true sale and not a secured financing and that the assets of CNH 2006-A would not be consolidated with the assets of CNH in the event of the bankruptcy of CNH. Furthermore, Fitch expects to receive an opinion of counsel that the trustee will have a first perfected security interest in the assets transferred to CNH 2006-A.

■ Portfolio Performance

CNH Historical Portfolio Performance

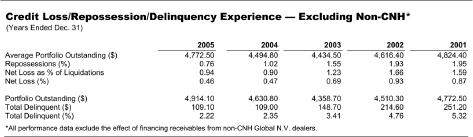

Historical delinquency and loss performance on CNH's captive portfolio is presented in the table on page 9. Delinquency, repossession and loss rates on agricultural and construction equipment have experienced downward trends over the past four years. Total delinquencies were 2.22% of the portfolio at year-end 2005, down from 2.35% at year-end 2004, and 3.41% in 2003. Net losses as a percentage of the CNH's portfolio have remained almost unchanged at 0.46% in 2005, versus year-end 2004 (0.47%). Net losses in 2003 and 2002 were 0.69% and 0.93%, respectively.

As delinquency, repossession and loss rates fluctuate with the economy, Fitch factored into its analysis the effect of a weak economic environment on pool performance when determining an expected base-case loss rate, stress multiples and stressed recovery rates used in the cash flow analysis to size credit-enhancement levels. (For more detail on specific assumptions used, see the Credit Enhancement section on page 5.)

■ Securitization History

CNH 2006-A will be the 14th U.S. public securitization issued by CNH. Fitch has rated eight prior transactions. As part of its funding strategy, CNH comes to the asset-backed securitization (ABS) market several times per year.

■ Collateral Analysis

The notes will be backed primarily by a pool of retail installment sales contracts on new and used agricultural and construction equipment originated by CNH Capital. Noteworthy differences in the underlying collateral of CNH 2006-A from prior transactions are listed below.

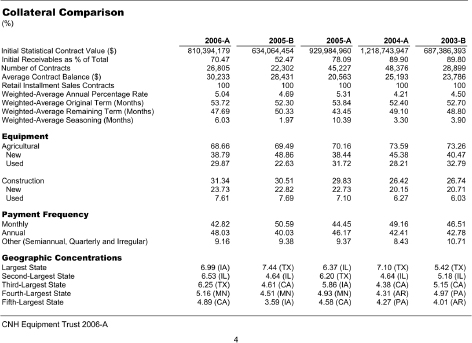

Collateral Attributes

Equipment Type – Stable

The split between agricultural and construction equipment in the 2006-A transaction is comparable with the 2005-B transaction. However, there is a higher percentage of used agricultural equipment: 29.87% versus 22.63% in the 2005-B transaction. The concentration in the 2006-A, however, is consistent with prior transactions, which have been composed of approximately 30% used agricultural equipment. Used agricultural equipment loss experience is similar to new agricultural equipment; therefore, the 2006-A transaction's performance should be in-line with prior transactions.

Geographic Concentration – Stable

Consistent with prior transactions, the largest concentrations of loans are located in Iowa (7.0%), Illinois (6.5%), Texas (6.3%), Minnesota (5.2%) California (4.9%) and Indiana (4.0%). No other state accounts for more than 4.0% of the pool. Geographic diversification is important to shield the pool from rolling recessions and regional economic downturns.

Loan Attributes

Seasoning, Contract Balance and APR – Stable to improving

Installment sales contracts in the 2006-A transaction are noticeably more seasoned (approximately 6.18 months versus 1.97 months in the 2005-B transaction). The 2006-A transaction has higher seasoning due to the addition of $64 million in seasoned and significantly amortized contracts from the CNH 2002-A transaction that was called in January 2006. The average contract balance ($30,233) is slightly higher when compared with the 2005-B transaction's average contract balance of $28,431. The weighted-average annual percentage rate in the 2006-A transaction is 5.04%, which is higher than in the 2005-B transaction (4.69%), but still results in the same amount of excess spread.

Payment Frequency – Decreasing

Payment frequency in the 2006-A transaction is slightly lumpier due to an increase in annual pay contracts, comprising 48.03% of the pool, versus 40.03% in the prior transaction. Although the 2006-A annual pay concentration is the highest, dating back to the 2002-A transaction, the increase is mitigated by the fact these contracts historically have performed the best.

■ Credit Analysis

Annual Static Pool Review

Fitch took into consideration both quantitative and qualitative factors in evaluating CNH's credit-enhancement structure. Fitch reviewed historical annual repossession, delinquency and net loss data on CNH's managed portfolio, as well as static pool performance data from prior CHN securitizations to develop an expected loss rate.

Loss Estimate

Fitch expects performance to be consistent with historical managed portfolio net losses, which have ranged from 0.29%–1.54%. On a securitization basis, net losses have ranged from 0.01%–1.48% for transactions dating back to 2000. Based on the collateral characteristics and the economic environment, Fitch anticipates lifetime losses will be consistent with historical averages.

Credit Enhancement

To achieve high investment-grade ratings, credit enhancement is needed to protect securityholders against the realization of losses due to poor collateral performance. Credit-enhancement levels were based on several qualitative and quantitative factors. Risk factors influencing performance may include the following:

Equipment Descriptions

Agricultural Equipment: Agricultural equipment (68.66%) underlying the receivables generally includes tractors, combines, cotton pickers, soil management equipment, planting and seeding equipment, hay and forage equipment, crop care equipment (e.g., sprayers and irrigation) and small telescopic handlers.

Construction Equipment: Construction equipment (31.34%) underlying the receivables generally includes excavators, backhoes, wheel loaders, skid steer loaders, tractor loaders, trenchers, horizontal directional drilling equipment, telescopic handlers, forklifts, compaction equipment, crawlers and cranes.

- National or regional economic downturns;

- Weather, commodity prices and crop yields could affect agricultural equipment borrowers;

- Interest rates, housing starts, and government and private appropriations could affect construction equipment borrowers; and

- Inattentive servicing or a servicing transfer.

The senior notes are supported by subordination (3.10% class B notes), a cash reserve initially set at 1.50% and maintained at the greater of 1.50% of the initial balance and the balance of all subsequent receivables or 1.50% of the outstanding balance, and initial excess spread of approximately 1.65% on an annual basis. Total excess spread over the life of the transaction is expected to be approximately 2.95% (1.65% times a 1.79-year weighted-average life).

Reserve Account

Amounts in the reserve account on each payment date will be available to cover shortfalls in distributions of principal and interest on the notes. On the closing date, the reserve account will be funded with an amount equal to 1.50% of the initial receivables balance. The reserve account will grow and be maintained at greater than 1.50% of the initial receivables balance and the balance of all subsequent receivables or 1.50% of the outstanding receivables balance through the trapping of excess spread. The nondeclining feature of the reserve account provides additional credit enhancement over time to protect noteholders.

Similar to the 2005-B transaction, the reserve account in the 2006-A transaction incorporates a reserve step-down feature whereby the reserve account will step down by 25 bps (floored) at a predefined period, as long as the collateral performs as expected and does not hit certain defined performance triggers. The required reserve account amount will decrease 25 bps from 1.50% to 1.25%, with a target of 1.50% of the outstanding pool balance at month 24. The step-down feature in the 2005-B transaction began in month 18 and also in months 24 and 30 if the step down feature was not utilized earlier. The specified spread account reduction triggers are shown in the table at right.

Excess Spread

Annual excess spread in the CNH 2006-A transaction is anticipated to be approximately 1.65%, which, as mentioned earlier, is slightly higher than the 1.62% annual excess spread in the CNH 2005-B transaction.

Expected Initial Annual Excess Spread (%)

7.80 WAC on collateral

(5.13) WA note coupon (expected) 2.67

(1.02) Servicing and back-up servicing fee (annual) 1.65 Initial annual excess spread (expected)

WAC - Weighted-average coupon. WA - Weighted average.

■ Cash Flow Modeling

Fitch analyzed cash flows reflecting stressed default rates, recovery rates and recovery timing lags under several default timing scenarios. Fitch derived an expected loss rate based on an analysis of annual performance data (see the table on page 9) and static pool performance data from CNH's managed portfolio and prior securitizations (as shown in the chart on page 3). As the 2006-A pool will not include receivables originated by non-CNH dealers, Fitch also took into consideration the more favorable historical performance of receivables originated by CNH dealers.

In addition, Fitch's analysis took into consideration the current nature of the agricultural industry and the cyclicality of the construction industry to assess the effect of an economic downturn on the frequency of repossessions and on recovery rates (and timing lags) on repossessed equipment.

Modeling Comments

- Recovery rate of 40%.

- Six-month recovery lag.

- Even, back-end and front-end loaded loss-timing scenarios.

- Delinquency rate stress (50 bps) applied to servicing fee.

- Stresses on expected prepayment speeds (20%) to reduce the availability of excess spread.

Specified Spread Account Reduction Triggers

![]()

Expected Credit Enhancement

Stress Scenarios Results

The break-even losses sustained by the enhancement structure were then compared with Fitch's expected loss rate stressed by a multiplier consistent with the rating being sought. Under Fitch's ‘AAA’ scenario, the class A notes were able to withstand 5.0 times (x) the expected net loss rate. The class B notes sustained more than a 3.Ox stress scenario. Fitch reviewed all cash flow runs to verify that each class of notes would be paid in full by its respective legal final maturity date.

■ Structural Considerations

Prefunding Account

Approximately $387 million of the proceeds from the sale of the notes was deposited into a segregated trust account that will be used from time to time to purchase additional receivables, subject to certain eligibility criteria, for addition to the trust pool. Funds remaining in the account after June 15, 2006, will be used to make principal payments on the notes. A capitalized interest account was also funded with proceeds from the sale of the notes. This account will be used to cover interest shortfalls attributable to any negative carry during the prefunding period. Funds remaining after the end of the prefunding period will be released to the seller.

Based on historical origination volume, subsequent receivables added to the trust during the prefunding period have characteristics comparable with the initial receivables as of the transaction's closing date

Named Back-Up Servicer

Systems & Services Technologies, Inc. (SST) is the named back-up servicer for the 2006-A transaction. Initially, the back-up servicer will obtain data and systems information from the servicer's servicing system, in addition to confirming that such data are readable by the back-up servicer, and will map the data to its systems. Additionally, the servicer will provide the back-up servicer with data from the servicer's servicing system on a monthly basis. Within 10 business days of the receipt of the data, the back-up servicer is expected to use its best efforts to identify any discrepancies or confirm that the information concerning delinquency aging, defaults and month-end contract value contained in the monthly servicer report distributed by the servicer corresponds with the monthly data provided to the backup servicer. SST will receive a fee of 2 bps for these activities. In the event SST was to take over servicing, it would receive the greater of the following: one-twelfth of 2 bps of the pool balance as of the first day of the preceding calendar month; $8.50 per contract in the trust as of the first day of the applicable calendar month; or $4,000. A servicer transfer will be triggered if CNH files for bankruptcy or an event of default occurs. A $150,000 reserve account will also be funded upon closing and available only to pay certain expenses and fees associated with the back-up servicer.

Interest Allocation

Interest will be allocated pro rata among the class A and B notes on the 15th of every month (or the next business day), starting in April 2006.

Principal Allocation

Principal will be allocated sequentially among the class A and B notes on the 15th of every month, starting in April 2006. In addition, if the class A notes are ever undercollateralized or if the maturity of the notes has been accelerated after an event of default, interest allocable to the class B notes is made available to pay class A principal. Once collateralization is restored, the class B notes will resume interest payments.

Payment Waterfall

The trustee will generally distribute funds in the following order of priority:

- Back-up servicing fee (2.0 bps).

- Servicing fee.

- Administration fee, payable to the administrator.

- Class A interest

- To pay principal on the class A notes in an amount equal to the excess of (x) the outstanding principal balances of the class A notes over (y) the asset balance.

- Class B interest.

- To pay principal on the notes in an amount equal to the note monthly principal distributable amount.

- Reserve account deposit, up to the required amount.

- Certain indemnities of a successor servicer and any accrued expenses of the back-up servicer.

- The remaining balance, if any, to the certificateholders, initially CNH.

Events of Default

To protect the bondholders from issuer insolvency or deterioration in credit, the structure includes several events of default. Fitch believes the occurrence of these events is unlikely.

Any of the following constitutes an event of default under the indenture, which can result in all accrued interest and unpaid principal becoming due and payable immediately:

- A default in the payment of interest to the rated notes for five consecutive business days.

- A default in the payment of principal when due and payable.

- Failure to perform any covenant or agreement of the trust in the indenture within specified cure periods.

- Failure to cure any incorrect representation or warranty made by the trust in the indenture within specified cure periods.

- Certain events of bankruptcy, insolvency, receivership or liquidation of the trust.

Following an event of default related to either a default in payment of principal or a default for five days or more in the payment of interest on any class of notes that has resulted in an acceleration of the notes, class B noteholders will not receive interest until payment in full of principal and interest on the class A notes.

Loss Allocation

Losses stemming from defaulted receivables will be covered by the enhancement in the following order:

- Excess spread.

- Reserve account.

- Class B notes.

- Class A notes.

■ Operations Review

Originations

The collateral in the 2006-A transaction was initially originated through independently owned dealerships that have entered into a retail financing agreement allowing them to sell contracts and leases to CNH Capital. Approximately 1,400 Case Credit and New Holland Credit dealers are located in the United States. Dealerships are subject to periodic financial review and may be terminated due to either a lack of volume or a violation of the dealer responsibilities in the retail financing agreement.

Underwriting

Credit applications are sent to one central finance office for review and risk-rating assessment. Part of this review includes credit scoring by a credit model that incorporates variables predictive of future loan performance. Previously, CNH Capital utilized a Fair, Isaac & Co., Inc. (FlCO)-based scoring system installed in 1994, and New Holland Credit used an Experian-based scoring system that was originally installed in 1997. However, in April 2002, an integrated Experian-based model, developed using CNH Capital's customer database, was implemented for both CNH Capital and New Holland Credit applications. Additionally, the underwriting criteria now focus solely on receivables originated through the captive dealer network.

In addition to the credit-scoring model, credit bureau reports, bank or trade references and, in some cases, financial statements are reviewed during the underwriting process. Credit managers have an average of more than 10 years of underwriting experience and are aligned by usage (agricultural and construction) rather than by brand. Collateral- and application-specific guidelines are also incorporated into the underwriting process. Guidelines for used equipment (which represents approximately 38.56% of the 2006-A pool) typically require shorter terms and higher down payments. Obligors are also required to obtain physical damage insurance on the equipment.

Collections and Servicing

Servicing, collection and customer service activities are based out of regional centers in Wisconsin and Pennsylvania. Delinquent customers are generally contacted by phone at 10 days past due; however, they may be contacted sooner if the obligors have had problems in the past. Letters are also sent if telephone contact is not successful. The local dealer is typically contacted at 45 days past due and may assist in the collection process by visiting the obligor and/or developing collection strategies specific to an obligor and that obligor's financial situation. At 60 days past due, general procedures to prepare for repossession are initiated. Outside companies may also be utilized to locate a customer and/or the equipment.

Credit Loss/Repossession/Delinquency Experience – Excluding Non-CNH*

(Years Ended Dec. 31)

Repossession

At 90 days past due, repossession of the equipment will generally take place, often with the assistance of the local dealership. Once repossessed, the equipment is generally taken to a secure location and inspected to assess its value. Repairs may also be done at this point to enhance the resale value of the equipment. Dealerships are notified of used equipment that is currently or will soon be available. Most recoveries on repossessed equipment are realized through resale on the equipment at auctions.

Loss Recognition

At 120 days past due, a receivable is treated as nonperforming. For purposes of the securitization, losses will be recognized when a receivable is liquidated through sale or other disposition, which typically occurs within 30-60 days after the equipment is repossessed.

Extensions

An obligor experiencing a temporary cash flow problem may request an extension or deferral of one or more installment payments. Extensions are given on a case-by-case basis and will only be granted if it can be determined that the obligor can meet its obligation once rescheduled and that there is sufficient security in the equipment. Loans with seasonal payment schedules require a minimum curtailment of the original installment amount as a condition of extension. The allowed duration of the extension is a function of the outstanding balance and requires various levels of authorization. Extensions and modifications are rarely granted.

Copyright © 2006 by Fitch, Inc., Fitch Ratings Ltd. and its subsidiaries. One State Street Plaza, NY, NY 10004.

Telephone: 1-800-753-4824, (212) 908-0500. Fax: (212) 480-4435. Reproduction or retransmission in whole or in part is prohibited except by permission. All rights reserved. All of the information contained herein is based on information obtained from issuers, other obligors, underwriters, and other sources which Fitch believes to be reliable. Fitch does not audit or verify the truth or accuracy of any such information. As a result, the information in this report is provided “as is” without any representation or warranty of any kind. A Fitch rating is an opinion as to the creditworthiness of a security. The rating does not address the risk of loss due to risks other than credit risk, unless such risk is specifically mentioned. Fitch is not engaged in the offer or sale of any security. A report providing a Fitch rating is neither a prospectus nor a substitute for the information assembled, verified and presented to investors by the issuer and its agents in connection with the sale of the securities. Ratings may be changed, suspended, or withdrawn at anytime for any reason in the sole discretion of Fitch. Fitch does not provide investment advice of any sort. Ratings are not a recommendation to buy, sell, or hold any security. Ratings do not comment on the adequacy of market price, the suitability of any security for a particular investor, or the tax-exempt nature or taxability of payments made in respect to any security. Fitch receives fees from issuers, insurers, guarantors, other obligors, and underwriters for rating securities. Such fees generally vary from USD 1,000 to USD750.000 (or the applicable currency equivalent) per issue. In certain cases, Fitch will rate all or a number of issues issued by a particular issuer, or insured or guaranteed by a particular insurer or guarantor, for a single annual fee. Such fees are expected to vary from USD 10,000 to USD 1,500,000 (or the applicable currency equivalent). The assignment, publication, or dissemination of a rating by Fitch shall not constitute a consent by Fitch to use its name as an expert in connection with any registration statement filed under the United States securities laws, the Financial Services and Markets Act of 2000 of Great Britain, or the securities laws of any particular jurisdiction. Due to the relative efficiency of electronic publishing and distribution. Fitch research may be available to electronic subscribers up to three days earlier than to print subscribers.