Valuation

Introduction

Valuation is no mystery. The trap that people can fall into is thinking that there is a single mathematical route to calculating value and one single, ‘right’, number applicable to a company’s value. There is no single number and no right number. It is an old cliché but the value of a company is the price agreed between a willing buyer and a willing seller. Value, then, can only be worked out in hindsight, which is not much good if you are the person struggling to calculate a price for an indicative offer prior to a deal.

Let us first of all deal with a couple of the myths of valuation and then turn to how to do it in practice.

Valuation is not best left to the experts

Valuation is not difficult if you understand the techniques and principles. It should certainly not be just handed over to the consultants or experts. The benefit of being fully involved with the valuation process is that it forces you to get down to the details of what drives the value of the target company, where those drivers are going, where the synergies are going to come from and how they are going to be realised. The merger and acquisition (M&A) market is very efficient. Good deals are hard to come by and will result only from highly disciplined deal making, including really understanding what it is you are buying and just how you are going to add value to the business and so recoup the premium you will pay. Valuation also tells you where the risks and sensitivities in the deal are.

There is no single number

There is no such thing as the correct valuate of a business. ‘Value’ is the amount a purchaser is willing to pay for the business. This can vary enormously: the evidence shows that when at least four provisional written offers are made for a business, the highest one is likely to be at least 50 per cent more than the lowest offer. Occasionally it can be more than double. Clearly buyers and sellers are going to have very different ideas about value. You will come up with a different number depending on whether you are buying or selling. But, you might ask, how can this be when both sides are working from the same data and using the same valuation methods? The answer is they are doing neither. Each one will use valuation methods that give the best answer. For example, a seller is going to be very interested in multiples achieved by previous sellers because these establish the nearest thing there is to ‘market value’. The buyer on the other hand, at least if rational, will want to pay the lowest possible price but one which is high enough to persuade the owners to sell and which is more than anyone else is willing to pay. In turn this means offering a price which is enough to persuade the sellers and anyone else who might be interested that the buyer is willing to pay more than the sellers think the business is worth. The buyer’s upper limit is what the business is worth to it. There is absolutely no point in a buyer paying more.

EXAMPLE Acquisition pricing in action

A good example of acquisition pricing in action is the bid for William Low by Tesco in 1994 when shareholders benefited by £93 million – an uplift of 60 per cent on the original Tesco offer – thanks to Sainsbury.

After hard negotiating, Tesco made an initial offer of 225p per share. This valued the company at £154 million and was accepted by William Low. That would have been the end of the story, had J Sainsbury not intervened. J Sainsbury launched a hostile bid at 305p per share topping Tesco’s offer by 35.5 per cent and valuing William Low at £210 million. It was widely believed that Sainsbury’s only motive for entering the bidding was to drive up the price for Tesco. However Tesco’s advisers recognised that Sainsbury would not have entered without willingness to take the business on.

Tesco’s management was convinced that its greater presence and experience in the region put them in the best position to obtain maximum value out of William Low. Tesco therefore decided to make a second offer of 360p per share, topping the first offer by no less than 60 per cent, and thus valuing the Scottish supermarket operator at £247 million!

Therefore, do not be seduced by complex mathematical modelling. Instead bear in mind that:

- A buyer in exclusive negotiations has every chance of obtaining a better deal.

- The shareholders of a seller are better off if there are competing buyers.

- The value of a company is whatever a buyer is prepared to pay for it. (In the example, William Low was worth £93 million more to Tesco than its original offer had indicated.)

- There is no rule as to what price a company is worth or will be sold for.

The valuation process – a summary

The valuation process described above is summarised (and considerably simplified) in Figure 7.1. This shows the process as having five steps:

- Establish an intrinsic value, i.e. the value of the business as a standalone entity. To do this the buyer needs to project its underlying performance and thereby estimate future profits and cash flows. At the same time the buyer should also assess the realisable value of any surplus assets as these will add to the valuation.

- Deduct transaction costs and reorganisation costs. Both of these can be considerable but are often underestimated or even forgotten in the heat of the transaction.1

- Assess synergy benefits – in detail. These are the source of value you the buyer will add to the business and the justification for the premium you are inevitably going to pay. If you cannot say where these benefits are going to come from or how they are going to be realised you should be asking yourself not just how much you should pay for the company but whether you should be acquiring it at all.

- Estimate what the business might be worth to other interested parties.

- Calculate the ‘going rate’ for the type of business under consideration based on previous transactions and the ratings of comparable companies (see below).

Assuming there is such a thing as an ‘intrinsic’ value for the business, a subject to which we will return later, the buyer will be willing to pay up to a maximum of this intrinsic value plus any post-acquisition synergies available to it. This must be more than other potential purchasers are willing to pay, otherwise it will be outbid. It must also be more than the seller thinks that the business is worth, or it will seek alternative buyers or not sell. For example, Pearson abandoned the sale of its business publishing arm in 2002 after a very public auction and management buy-out attempt because it reckoned that all the various offers were less than the value it could extract from the business.

What the seller thinks the business is worth is somewhere between the intrinsic value of the business and what it thinks the market will pay. Fashion can improve the market value of a business considerably while desperation to sell quickly or a previous sale that did not go through can create soiled goods whose market value is depressed.

Valuation is not just about modelling

Another reason we can never say that a business is worth £x or €y is that valuations have a habit of changing. Often this is to do with expectations about the underlying performance of the business. A business, after all, is bought for its future performance and, as stock market movements show, expectations of the future change on a daily basis. Sellers of internet or telecoms businesses in 1998–99 got some very good prices indeed. By March 2000 they would be lucky to find any buyers at all. Referring back to Figure 7.1, the size of column 1, which after all is nothing more than the expectation of future performance translated into current value, fell considerably, as did the size of column 5. Why? Who knows, except that by March 2000 potential buyers had probably got enough of a feel for internet companies to realise that they could not live up to the expectations built into their valuations.

It should be clear from this example that expectations are everything. But expectations are not hard facts. Sure they can be dressed up as hard facts by being represented as numbers but, when all is said and done, they are someone’s assessment of what that person thinks is going to happen. So, before the potential buyer or seller opens its spreadsheet it has to have a view about the future. There are a number of ways in which some of the uncertainty about the future can be reduced, such as using a real options approach to valuation,2 but all acquirers should recognise that valuation has too many subjective elements to it to make it a coldly rational mathematical process.

Businesses are bought for their future prospects. History alone will not tell you about the future, but history cannot be ignored altogether. First it will give you a starting point for projections. History will also put the forecasts into context. If gross margin has been shrinking for five years is there not something extraordinary happening in a forecast if the trend suddenly starts to reverse? Erratic profits and losses during the past three years will tell you that a smoothly progressing ‘hockey stick’ projection is nonsense. Historic overhead costs will tell you what scope there is for cost savings if two businesses are to be brought together.

To really understand the future you have to understand the fundamentals. This means getting down to the details of:

- What is happening in the market?

- Can this company continue to compete effectively?

- How big are those synergy benefits?

- How are we going to realise them post-acquisition?

The other reason why valuation is more than just numbers is to do with the gap between columns 3 and 5 in Figure 7.1. The size of that gap is purely a matter of negotiation. Ideally the buyer does not want to give away any of the synergy benefits available. Why should it when it is the only one that can actually realise them? On the other hand, the seller knows that the company is worth more to the buyer than it thinks it is worth and will therefore be keen to get a share of the synergies.

Work done in this area suggests that sellers do much better than buyers in an acquisition. The evidence suggests that buyers are either not very good at negotiating the premium above ‘intrinsic value’ or do not add much in the way of value to the acquisitions they do make.

Calculating synergies

Synergies are easier to imagine than to realise. Acquirers and advisers routinely exaggerate the amount of synergy to be had and the speed with which it can be captured. It is essential to calculate in as much detail as possible the size of each hoped for synergy benefit and precisely how and over what period each will be unlocked and by whom. It is not good enough to accept the bland assertion of ambitious directors or incentivised advisers, for example that ‘10 per cent of combined overheads can be saved’. It is also important to remember that many synergies come at a cost – a new computer system or redundancy costs. The one-off costs of achieving synergy benefits have to be calculated too. Once calculated, benefits arising from synergy should be shown separately otherwise there is a risk that these benefits will be negotiated away.

Valuation techniques

With so much emphasis placed on negotiating, judgement and horse-trading, why are numeric-based valuation techniques so important? The answer is that you have to start somewhere. Acquirers need to use valuation models to calculate a realistic expectation of the worth of a business and sellers do not usually indicate an asking price until they have received a detailed written offer.

The traditional techniques to consider are (in approximate order of utility):

- Discounted cash flow (DCF)

- Return on investment

- Price/earnings (P/E) and other profit ratios

- Comparable transactions

- Sector-specific valuation benchmarks

- Impact on earnings per share

- Net asset backing.

Having examined these techniques in detail, we will then go on to consider some of the techniques used to value special cases. An example of a special case might be a start-up company that does not have a trading record or has a particularly strong portfolio of brands.

Choosing the valuation method

Empirical research suggests that cash flow, not accounting earnings, drives value.3 In the earnings approach, companies are valued based on a multiple of accounting earnings. Or, in other words, a multiple of the profit figure calculated by the accountants, as opposed to the hard cash a company made. In effect this earnings method is saying a number of things which do not make sense:

- Only last year’s, this year’s or next year’s earnings matter. A single P/E ratio cannot possibly capture an entire business cycle.

- The timing of returns does not matter. A company which has done badly this year, and will recover next year, could be valued the same as one which has done exceptionally well.

- The investment required to generate those earnings does not matter. In other words, if two companies produce the same earnings they should be valued the same, regardless of the resources required to generate earnings. This has to be nonsense. Does the building society offer you the same cash interest on deposits of £50 as it does on deposits of £100?

- Different accounting treatments do not matter. They do. The classic example concerned Daimler’s accounts at the time of the Chrysler merger. Under German GAAP, profits were DM1 billion. Under US GAAP, this was transformed into a US$1 billion loss.

- Different financial structures do not matter. They do. Gearing increases potential reward to shareholders but also increases risk. In the discounted cash flow (DCF) approach, the value of the business is the expected cash flow discounted at a rate that reflects the riskiness of the cash flow.

- Short-term stock market prices reflect a company’s intrinsic value. They do not. There is an awful lot of speculation wrapped up in a share price.

Use more than one method

Because there is no such thing as a true value, both buyers and sellers will use more than one technique. Three techniques is often held to be a good number as this allows a triangulation on value (see Figure 7.2).

Another reason for using more than one method is to give a reference point. Reference points might be given by prices paid in similar deals such as the multiple of operating profit (acquisition price divided by operating profit) or the multiple of EBITDA (earnings before interest, tax, depreciation and amortisation). EBITDA is often used as a surrogate for cash flow. These can at least reassure the buyer that the agreed price is in line with ‘market’ price.

FIGURE 7.2 Triangulating value using three different valuation methods

1. Discounted cash flow (DCF)

The DCF approach says that value is added if an investment generates a return which is more than can be generated elsewhere for the same risk. That sounds like it might be complicated but all it is really saying is that if the going rate for ultra-safe, instant access deposits is 4 per cent and you can get 5 per cent, go for it. Similarly, if the going rate for return on investments in electric-arc slab cast steelmaking in Eastern Europe is 10 per cent and you think you can get 11 per cent, then you should go ahead with the investment.

The process

Assumptions

Some maintain the cash flow approach suffers less from the subjectivity that bedevils other valuation methods as it makes explicit assumptions and estimates. Others regard it as just as subjective and error prone. According to one leading UK private equity investor, DCF actually stands for ‘deceit by computer forecast’.

As ever, the truth lies somewhere between the two. DCF does rely on a whole host of assumptions and valuations can be moved by significant amounts depending on the assumptions or how the maths is done. On the other hand, DCF does force the acquirer to look in detail at the particulars of the investment and this is its main advantage. Unlike the other approaches, it encourages the explicit estimation of:

- Sales volumes and prices. These are rarely as smooth and positive as presented in an information memorandum.

- The cost base. An acquisition may give better purchasing power or spread fixed costs over a bigger sales volume.

- Individual profit streams. Companies rarely sell one homogenous product to the same group of buyers. DCF forces the buyer to consider all the different profit streams. Often these have very different characteristics.

- Any additional capital expenditure that may be required. Businesses are often sold because they have reached a point where they need new investment or a new approach. Alternatively, they are often bought to achieve economies of scale by rationalising operations so that lower levels of capital expenditure may be needed once the initial rationalisation has been carried out.

- Changes in working capital, which reflect, for example, turnover growth or better financial management.

Because you have to project sales and profits forward for five or ten years, DCF forces you to understand the underlying economic value drivers of the business to arrive at a value. The resulting computer model then gives the platform for carrying out sensitivity analyses to assess the impact of changes in assumptions.

Computer modelling

PCs allow very detailed computer models. There is always a danger that analysts get so deep into the details that they miss the bigger picture.

The general rules for building computer models need to be kept in mind. Models should be sufficiently well planned and documented for someone else to be able to understand and use. Other generally-accepted conventions are:

- Assumptions and other numbers which might be flexed, for example the cost of financing, should be explicitly stated in a section of their own.

- There should be only one source for each number. This means that numbers which are input are done so only once and if used in more than one location in the spreadsheet, for example in different versions of the model, should be read across into the other sections. If numbers are calculated in one section and used in another then these should also be read across. This not only minimises the likelihood of keying errors but also provides an audit trail.

- The base year should be reconciled back to statutory or management accounts. It is best to have a run of three to five years’ history with key ratios calculated for each year to act as a sanity check on the model’s projection of these same ratios.

- DCF models should be designed to calculate balance sheet values. If the balance sheet does not balance you know there is something wrong. To do this, the model must calculate cash flows for every period and adjust the closing debt figure in the last period by the amount of the cash generated. If cash is independently calculated this way and not, as some accountants favour, simply taken as the difference between two balance sheets, you have a check that the model is working correctly.

One financial analyst modelled a large public company which was not performing well. He proudly took the results to the chairman and informed him that he had nothing to worry about as the company could easily afford all the capital expenditure needed over the coming years. The chairman looked up from the figures and told him that, while he was very impressed with all his computer handy work, sadly capital expenditure meant paying out money, not receiving it. The analyst had made a simple mistake in the model and put the sign for capital expenditure the wrong way round. He did not notice his mistake because he did not include a balance sheet in his model.

A mathematical check does not, of course, dispense with the need for sanity checks:

- Capital expenditure is an expense, as is an increase in stock and an increase in debtors.

- There tend to be industry norms for most ratios.

- Margins tend to erode over time.

- Selling prices tend to fall over time.

The maths

The mathematics behind discounting is much simpler than all those squiggles in the formulae would suggest. A few minutes invested in understanding the basic principles, however unappealing that may sound, is well worth the (limited) brain power needed. All you need to know about discounting is set out in the following 300 or so simple words.

Lend me a pound and I’ll pay you back with interest this time next year. At the present interest rate of about 4 per cent you would expect to get £1.04 back.

Now turn that proposition round. I’ll give you a pound this time next year if you give me 95p now. Is this a good deal? Yes it is for you, because if you put that 95p in the bank it would be worth only 98.8p 12 months hence. You would be much better off lending it to me and getting £1 back, assuming you regard lending to me as no more risky than lending to a bank. Suppose I offered you £1 in 12 months for 97p now? This is not a good deal. At 4 per cent interest, 97p would be worth £1.0088 in a year and as an astute financier you would negotiate the 97p down to 96.1538p.

Interest rates are going to stick at 4 per cent. How much would you give me now if I promise to give you £1 in two years’ time? The answer is roughly 92½ p. Your logic would be

| Value now | Value next year | Value the year after |

| 92.4556 | 96.1538 | £1 |

92.4556p invested for one year at 4 per cent is worth 96.1538p

(= 92.4556 × 1.04)

and

96.1538p invested for a further year at 4 per cent is worth £1

(= 96.1538 × 1.04)

but because you need to calculate the value today of the £1 you will receive two years hence, you need to invert the calculation.

| Value now | Value next year | Value the year after |

| (£1 ÷ 1.04) ÷ 1.04 = 92.4556 | £1 ÷ 1.04 = 96.1538 | £1 |

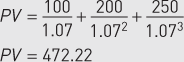

This is the principal behind discounting, but it is always made to look much more complicated as we can see from the normal discounting formula:

All the formula is saying is that the present value of a business (PV) is the sum of each year’s free cash flow (CFt) divided by 1 plus the discount rate (1 + r) raised to the power of the year number in question (t), which when expanded looks like this:

Which with cash flows of £100, £200 and £250 and a discount rate of 7 per cent (based on an assumption of base rate plus 3 per cent risk) looks like this:

Free cash flow

Free cash flow does not mean ‘not paid for’ but cash which the company is free to use as it pleases; it is:

Profit before interest and tax with non-cash charges (such as depreciation) added back

Less

Investments in operating assets such as working capital, property, plant and equipment

It does not include any financing-related cash flows such as interest or dividends paid or received. Many people find this a hard concept to grasp, but it is easily understood if it is related to everyday experience. Imagine you are buying a house. Would you expect to pay more if you were funding part of the purchase with a mortgage? Would you expect to pay less? No, you would expect to pay the same whether you used all cash, all debt or a mixture of the two. Why, then, would you keep debt in a DCF calculation? What a business is worth and how you fund it are two completely separate decisions. A house is worth what a willing buyer and a willing seller decide it is worth. That value is not different if the buyer pays cash or takes out a 100 per cent mortgage. The same with companies. DCF values the company based on future cash flows generated by the business from operations. Just like in house buying, whether the business takes out loans or uses equity to finance itself is totally irrelevant to the basic valuation of the business as a going concern. Table 7.1 shows how free cash flow is calculated.

Using the right numbers

Before we can start to project free cash flows we must remove as many accounting adjustments as possible from the numbers. The cleaned-up numbers will form the basis of our projections. In an ideal world, profits will equal cash. In most sets of accounts the two numbers are very different. There are good reasons for this, the need to build stock because of growth for example, and there are other reasons. The application of accounting policies can have a huge impact on reported numbers. Getting the ‘right’ set of numbers for a DCF model is often a case of undoing what accountants have done to the figures. The accounting policies of the acquirer – for example, the treatment of items such as depreciation and the valuation of work in progress – may be different from what the acquirer regards as appropriate.

The next set of adjustments that may be needed is taking out (or adding in) what may be termed exceptional costs. Chief amongst these in private companies are realistic rewards for the directors – for example, lower salaries to bring them into line with other directors in group subsidiaries; the savings resulting from the termination of contracts of those relatives employed in the business and who are no longer required; eliminating the cost of unnecessary extravagances such as aeroplanes, boats and overseas homes enjoyed by directors.

TABLE 7.1 Calculating free cash flow for the valuation model

| Operating profit | 100 | |

| Plus | Depreciation | 29 |

| Less | Profit on the sale of fixed assets | (1) |

| Plus/(Less) | Decrease/(increase in stock) | (35) |

| Plus/(Less) | Decrease/(increase in debtors) | (20) |

| Plus/(Less) | Increase/(decrease in creditors) | 9 |

| = | Net cash flow from continuing operations | 82 |

| Less | Investment in fixed assets | (21) |

| Less | Investment in subsidiaries | – |

| Plus | Cash from sale of fixed assets | 2 |

| Plus | Cash from sale of investments | – |

| = | Cash flow before financing and tax | 63 |

Finally, as DCF is concerned with operating cash flow and therefore operating assets, all non-operating assets need to be removed.

The particularly troublesome adjustments are listed below. Please note that some of these will not have a direct effect on the discounted cash flow calculation, but they are needed either to ‘clean up’ the base of the DCF model or play a part in the final valuation calculation.

Fixed assets. As already mentioned, fixed assets should include only assets used in the operations of the business. Excluded from any projections would be investments in, say, marketable securities.

Operating leases. Operating leases represent a type of financing and, if material, should be treated as such. To do this they should be capitalised as follows:

- Deduct interest from the interest charge in the profit and loss (P&L) account.

- Add the implied principal amount both to fixed assets and to debt. Dividing the interest charge by the interest rate is usually a good proxy for the principal amount.

Pension deficits and surpluses. Treat a surplus or deficit on the pension scheme as:

- For a surplus – a loan given

- For a deficit – a loan taken out.

Charge interest through the profit and loss as normal. In order for the balance sheet to continue to balance the retained earnings should be recalculated.

Provisions. Provisions charged through the P&L account are either reserves set up to fund future costs or losses or provisions to smooth future earnings. Either way they should be reversed out of the P&L account and actual cash costs charged when/if they are incurred.

Capitalised expenses. In many ways these are similar to provisions and should be treated in the same way. All costs should be charged as they are incurred. The argument that these have a future benefit does not wash here. If they do have a future benefit, this will be reflected in sales and profits.

Working capital. This is operating working capital, usually stock, trade creditors, trade debtors and some cash. A ‘reasonable’ cash balance is put at 0.5 to 2.0 per cent of sales.4 Excess cash balances would have to be excluded (and included on the financing side of the balance sheet).

Tax. Adjust to a cash basis, which can normally be done by adjusting the annual tax charge on the P&L account by changes in the deferred tax position (to adjust for capital allowances and such like) and in changes in the tax debtors figure (as most taxes are paid after the year end).

Tax losses. Tax losses can be extremely important to the viability of a transaction and justifying it internally. The reality is that they can easily be lost. Try to make them contingent and do not be tempted to include the value of tax losses in the valuation (or anything other than contingent in the price you negotiate).

Nominal or real numbers?5 Nominal! You try working in real numbers (easy for sales and costs but not for assets) and then explaining to the chairman why he does not recognise any of the figures.

Pre-tax or post-tax? Normally, discounted cash flow valuations use post-tax cash flows. That is what corresponds to ‘free cash flow’, i.e. cash which the company is free to do what it wants with. In truth it does not matter whether the cash flows are taxed or untaxed, as long as the discount rate used is consistent. If you use taxed cash flow, then the discount rate needs to be reduced by the tax effect which means that the cost of debt in the cost of capital should be multiplied by 1 minus the tax rate.

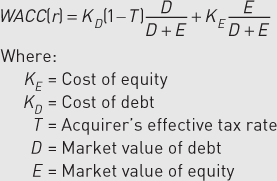

The discount rate

DCF uses the acquirer’s cost of capital as the discount rate. Easily said but small percentage movements in the discount rate can move the valuation by many millions and there is no real scientific answer as to what the right rate is.6 Logical application of a thorough understanding of the principles is therefore the key. First of all:

- The cost of capital is the weighted average cost of capital (WACC) of all sources of capital. Each cost should reflect the risk each is taking (more on that below).

- The weighting should be at market rates – but should reflect target rather than actual proportions.

- Costs should be after tax if cash flows are computed after tax.

- Rates are expressed in nominal terms, because cash flows are stated in nominal terms.

The formula is the cost of equity plus the after-tax cost of debt, as follows:

The cost of debt

The cost of debt should be fairly straightforward to calculate, although hybrid forms may complicate matters. The cost of debt is the annual interest payment divided by the market value of the debt. Always use market values where possible. If the instrument is not traded, the following applies:

- Identify the payments to be made.

- Estimate the credit quality (somewhere between AAA and junk).

- Look up the yield to maturity on similarly rated traded bonds with similar coupons and maturities.

- Calculate the approximate market value by finding the present value of the future payments using the yield to maturity on the traded instrument as the discount rate.

The cost of preferred stock should lie between debt and equity.

The cost of equity

Determining the cost of equity is always an issue. Equity should be valued using market prices where possible. If the company is not quoted then you will have to use figures from comparable companies which are quoted. The cost of equity to a company is the return that an investor expects from it. To cut a long story very short, there are two shortcuts that help arrive at a number:

- The return on an equity comprises a risk-free rate plus a premium for risk.

- The returns on an individual stock are related to the return on the market as a whole.

The yield on a ten-year government bond is the best estimate of the risk-free rate and the historical equity risk premium is in the 4.5 to 5 per cent range. This gives an average return on the market as a whole. Getting from this to the cost of equity for a particular stock calls for the use of betas.

Betas derive from the theory that returns on all individual shares are related to returns on the market as a whole. Again to cut a long story very short, the variability of returns on individual stocks are plotted relative to returns on the market and the beta is given by the point at which the stock in question lies on the slope of the line of best fit. This is illustrated in Figure 7.3. The beta for the market as a whole is 1. The more risky a stock, the higher its beta will be. Fortunately we do not have to calculate betas ourselves because they are published on a regular basis by a number of financial data providers.

FIGURE 7.3 Calculating betas

The resulting beta is then fed into the following formula, which is not quite as fearsome as it looks, to arrive at the cost of equity:

The value of convertible securities are a bit trickier since their value is made up partly of the interest received and partly by the conversion feature. Because the conversion feature has a value, the coupon rate is generally lower than with straight debt and therefore the cost lies somewhere between the cost of debt and the cost of equity.

A minority interest is a claim by outside shareholders on a portion of a company’s business. It arises where the target company has sold a proportion of a subsidiary or made an acquisition and not bought out all of the shareholders. The value of a minority interest is related to the value of the underlying asset in which the minority partner has a stake. If there is no market value and cash flows are not available use a market value proxy, such as comparable company P/Es, to calculate market value.

Terminal value

An additional complication in DCF is that businesses go on forever, whereas cash flow forecasts are normally cut off after five or ten years. This is usually dealt with by dividing the forecast period into two:

- The explicit forecast period – the period you are trying to forecast in detail

- The period after the end of the explicit period to infinity, i.e. the period you are not trying to forecast in detail. (This is often referred to as the ‘terminal value’ or the ‘continuing value’.)

It is sometimes frightening how big the terminal value can be compared with the discounted cash flows for the forecast period. It stands to reason, therefore, that a careful estimate of terminal value is central to valuation. Normally a DCF model uses simplifying assumptions to calculate terminal value. The most popular are:

- Discount terminal asset value – i.e. take the asset value in the final year and discount it back to today’s value. Essentially this assumes liquidation at the end of the forecast period which may not be a sensible assumption to make.

- The final year’s cash flow is assumed to continue to perpetuity. The formula for calculating a value to perpetuity is:

Final year free cash flow/WACC or ![]()

The resulting value is then discounted back to the start of the model by multiplying by ![]() . This assumes that the final year cash flow is sustainable to infinity.

. This assumes that the final year cash flow is sustainable to infinity.

- A variation on the above is used for growth stocks. Final year cash flow is calculated to infinity but there is an allowance for growth at a constant rate. The formula is:

Final year free cash flow/(WACC – annual growth percentage (g)) or ![]()

In other words, the WACC is reduced by the assumed growth rate g leading to a lower denominator and a higher terminal value. Again the resulting value is discounted back to year zero.

DCF has a lot of advantages as a valuation tool and it does force prospective buyers into a rigorous examination of the business and its future performance. The downside is that, as already mentioned, the results from a DCF modelling exercise can move significantly with just a small change in some of the assumptions. Buyers, therefore, should use more than one approach to valuation, if only as a sanity check on the DCF. The other methods which could be used are set out below.

2. Return on investment

Return on investment (ROI) provides a good safe target on which a valuation can be based. The downsides of the ROI approach are that it does not accommodate the cash implications of the deal and that it can be too broad-brush. On the other hand, acquisitions should not be treated any differently to other forms of capital expenditure so although companies are acquired for long-term strategic reasons, there should be an acceptable return on investment during the early years after acquisition.

The ROI approach to evaluating an acquisition is no different from the standard technique which would be used to appraise any other form of investment. Many large companies use the pre-tax return on capital employed to judge capital expenditure proposals and as a key measure of performance for each of their subsidiary companies. It is not surprising, therefore, that a similar approach is often used as a short-cut method to assess a prospective acquisition.

For comparative purposes with other capital projects this ratio is best kept free from the burden of costs of capital. Thus the profits to be used are prior to any of the funding costs of the acquisition.

ROI is calculated by taking forecast profit before tax in the second full financial year following acquisition, adjusting it for the effects of your ownership and dividing it by the total investment to date:

The second year is used to allow time for the acquisition to bed down – although it may be more relevant to use the third full year of profits if an earn-out deal has been structured to cover three years. The denominator should take into account the initial purchase consideration, any expected earn-out payments and the cash generated from the business or the amount of cash to be invested to achieve the forecast profit growth.

The answer gives a percentage pre-tax return on the proposed purchase price. It is difficult to set a reasonable benchmark.

EXAMPLE The maximum acquisition price

To determine the maximum acquisition price.

- Acquisition made in 2013

- Acquirer expects adjusted profit before tax in 2015 of £2 million

- Additional cash investment required of £1 million by 2015

What is the maximum acquisition price (AP) to give a 20 per cent return?

Therefore the maximum acquisition price = £9 million

3. Price/earnings (P/E) and other profit ratios

Price/earnings ratios attempt to assess ‘market value’ and they provide a useful benchmark for sellers. Other profit ratios are a variation on this theme.

A listed company has a price/earnings ratio noted every day in the Financial Times, Wall Street Journal or elsewhere. The price earnings multiple of a listed company is its share price divided by its earnings. It comprises the following:

or

or

P/E ratios are widely used, and with good reason. They are relatively quick and simple to apply and are readily verifiable. The P/E ratio applied to an unquoted target is derived from the P/E ratios of comparable quoted companies. By using quoted market prices they also build in current market expectations of performance. First find comparable quoted companies, then determine their P/Es and then apply these to an estimate of the sustainable earnings of the target. It sounds simple enough, but there are a number of complications that have to be adjusted for.

Public vs private P/E ratios

Using listed P/Es assumes that the target company could be floated. If the target company is not large enough for this or the conditions are not right, the likely P/E ratio should be reduced by between 30 to 40 per cent. The amount of the reduction should reflect the attractiveness of the particular business sector and the attractiveness of the target. The accountants BDO publish a quarterly analysis of the price/earnings ratio for private company sales in the UK (www.bdo.uk.com/library/pcpi-private-company-price-index) compared with public company P/Es for the same time period.

The reliability of P/E ratios

Theoretically the main factors determining a company’s P/E ratio are its growth prospects and risk. The better the growth prospects then in theory the higher the P/E. On the other hand, the greater the risk, the lower the P/E.

In practice there is no consistent correlation between current earnings growth and share prices, or between risk and P/E ratios. The earnings figures of individual companies (and hence their P/Es) reflect their gearing and tax positions, and also their accounting policies. These discrepancies may be exacerbated in a period of inflation when earnings figures calculated on an historic cost basis will not be comparable. The main problems with quoted P/Es are threefold:

- Dependence on share prices

- Difficulties in finding truly comparable companies

- Differences in capital structure.

Dependence on share prices

There are two points to bear in mind here:

- General sentiment in the market can shift a company’s P/E ratio dramatically and in the short term this may have little to do with long-term potential.

- P/Es can be artificially high or low depending on where the comparable companies are in their reporting cycles or what the market thinks about future prospects. If a company’s historic profits were low, but the market believes it will recover, price will remain relatively high, and with it the historic P/E, until the next set of results (or the next profit warning!) confirms or confounds market expectations.

Difficulties in finding truly comparable companies

As no two companies in the same sector operate in exactly the same way, with the same customer base, product range and geographic spread, true comparisons are all but impossible. P/Es based on comparable companies must always, therefore, be seen as rough approximations.

Differences in capital structure

Earnings are calculated as shown in Figure 7.4.

Estimating sustainable earnings

It is not good enough just to take the target’s earnings and use that without question. For all sorts of reasons the earnings figure might not be representative of the ‘steady state’. Note that P/Es of comparable companies should be applied to an estimate of the sustainable earnings of the target. Sustainable earnings to which the P/E ratio is applied should generally exclude exceptional items, interest on investments and cash balances not used in the business. For the acquisition of private companies in particular, the owner’s benefits, which will not continue post-acquisition, need to be added back. Equally, costs not accounted for by the vendor in the past which have flattered profits need to be deducted to establish a more accurate picture.

FIGURE 7.4 Calculating earnings

| £ million | |

| Turnover, including related companies | 2562.2 |

| Less turnover of related companies | (442.7) |

| Turnover | 2,119.5 |

| Cost of sales | (1,086.3) |

| Gross profit | 1,033.2 |

| Distribution costs | (237.6) |

| Administrative expenses | (416.9) |

| Research and development | (46.8) |

| Share of profits of related companies | 21.3 |

| Income from other fixed-asset investments | 0.2 |

| Operating profit | 353.4 |

| Interest (net) | (51.9) |

| Profit before tax | 301.5 |

| Tax on profit on ordinary activities | (82.9) |

| Profit on ordinary activities after tax | 218.6 |

| Minority interests | (13.4) |

| Earnings per 25p ordinary share, net basis (undiluted) | 44.98p |

| Earnings per 25p ordinary share, net basis (fully diluted) | 44.37p |

When using P/Es to calculate the value of the target to the buyer, any synergy benefits need to be added to the target’s stand-alone sustainable earnings.

All of this is easier said than done. Given that one of the main objectives of financial due diligence is to establish sustainable earnings, arriving at the sustainable earnings of the target company can involve a lot more than jotting a few numbers on the back of a cigarette packet.

All the above means that the determination of appropriate P/E ratios can be a complex task requiring many judgements and adjustments. Nevertheless, despite the limitations of P/Es in valuation, they are very widely used.

Other profit multiples

It really does not matter much which profit measure is used providing that all data are consistently either pre- or post-tax and pre- or post-amortisation and depreciation. In other words like, has to be compared with like. Other popular multiples are:

| EBIT | Earnings before interest and taxes |

| EBITDA | Earnings before interest, tax, depreciation and amortisation |

| EBT (or PBT) | Earnings (profit) before tax |

EBITDA has become a favourite over the past few years as the importance of operating cash flows in valuations has been recognised. EBITDA is profit before any financing costs and before charges for the largest non-cash items (depreciation and amortisation) and is seen as a good approximation to cash flow.

Profit multiples vs cash flow

Which is best? For M&A valuations there is no right answer to that question. Both techniques have their strengths and weaknesses and both should be used. As far as stock market valuations are concerned, however, the evidence suggests that the market values cash and can see through manipulations designed to increase reported earnings.7

4. Comparable transactions

As well as using comparable companies in P/E and profit multiple calculations, acquirers may also use comparable transactions as a benchmark on the not unreasonable grounds that a comparable transaction ought to be a good guide to the going rate for this type of company. This is fine if used with caution because sometimes companies are bought for strategic reasons and under these circumstances acquirers pay more than the going rate. However, if nothing else, comparable transactions can give buyers comfort that they are not paying too much.

5. Sector-specific valuation benchmarks

Publicly-quoted engineering companies are usually valued at around sales value. Similar norms exist in most industries. Table 7.2 gives a few examples of the benchmarks of value that might be used in a number of industries.

| Industry/business | Valuation benchmark |

| Landfill | Price per cubic metre |

| Advertising agencies | Multiple of billings |

| Mobile telephone service | Price per subscriber |

| Cable TV | Price per subscriber |

| Fund managers | Multiple of funds under management |

| Hotels | Sale price per room |

| Mining companies | Value of mineral reserves |

| Professional firms | Multiple of fee income |

| Petrol retailers | Multiple of annual gallonage |

| Ready-mixed concrete | Price per cubic metre of output |

6. Impact on earnings per share

A check on value that is popular amongst public companies is to gauge the acquisition’s impact on pro-forma earnings per share. EPS dilution is not something to be tolerated. Of course there will only be dilution if one or all of the following apply:

- The target company is sizeable in comparison to the acquiring group.

- The proposed purchase price values the target company at a significantly different earnings multiple than that of the acquirer.

- The cost of overdraft or loan stock interest to finance the purchase will depress net earnings.

The combined EPS figures should be calculated taking into account the overall impact of the acquisition including the effect of subsequent deferred payments to be made as part of an earn-out deal and the impact of the conversion of any convertible loan stock issued as purchase consideration.

7. Net asset backing

Net assets is a commonly-used basis for valuing small private companies, but it has serious drawbacks. The method is mostly reserved for valuing loss-makers or companies operating at break-even. The valuation of assets in a company’s accounts is rarely useful in the context of an acquisition as:

- Historical cost figures are inadequate and current cost figures which might (in theory at least) be preferable are unlikely to be available.

- Many significant assets may not be valued at all in the accounts (e.g. patents, designs, trademarks, brand names, copyrights, employees, customer lists and contracts). This is why businesses with a reasonable performance are likely to change hands at figures substantially higher than their book asset values.

- Other assets (such as stock) can be overvalued in the accounts.

A valuation based on the target’s assets obviously needs a valuation of the assets. Expert valuations of land and buildings, stock and plant may be required and other balance sheet items may need careful investigation. The real value of work in progress, finished goods and debtors needs to be confirmed as they would in an audit and the adequacy of any provisions needs to be reviewed as does the extent of liabilities, including tax.

Conclusion

The soundest method for valuing acquisition targets is cash flow because it has fewer disadvantages than other methods and forces acquirers to quantify important assumptions. It is less subject to manipulation to produce a result in support of unsound thinking by company strategists. However, it still requires a number of simplifying assumptions which can have an impact on the calculation of value.

Because no one valuation method is perfect, it is best to use three different approaches. This allows the acquirer to ‘triangulate’ on value. It is also a good idea to work out the value of the business to the seller and to other possible bidders. A feel for both will help set the minimum and maximum acquisition prices that need be paid. A thorough and detailed calculation of synergies is vital in setting the maximum price that can be paid.

Notes

1 It obviously depends on the specifics of the transaction, but acquirers should expect to pay somewhere around 5–7 per cent of the deal price in advisers’ fees and there may be other transaction costs to add such as stamp duty.

2 Real options introduce a decision tree approach to DCF by recognising that the projection of cash flows should be made up of a number of decision nodes each with its own value and each with its own probability of occurring, and that the value of a company is the weighted average of this series of uncertain cash flows.

3 See for example Copeland, Tom, Koller, Tim and Murrin, Jack, Valuation: Measuring and Managing the Value of Companies, John Wiley & Sons, New York, 1990, Chapter 5.

4 Copeland et al. (1990), p. 161.

5 Nominal is the number as it is, including inflation: real numbers have inflation excluded.

6 It is possible to take a PhD in the subject, such are its subtleties.

7 See for example Copeland et al. (1990), pp. 81–94.