Post-Mortem: Delphi Automotive

Throughout the book, we used Delphi Automotive as a case study to illustrate how our 5-step process can be employed to source, due diligence, value, and ultimately manage stock positions. We took you back in time to the decision facing investors in November 2011 when Delphi was going public.

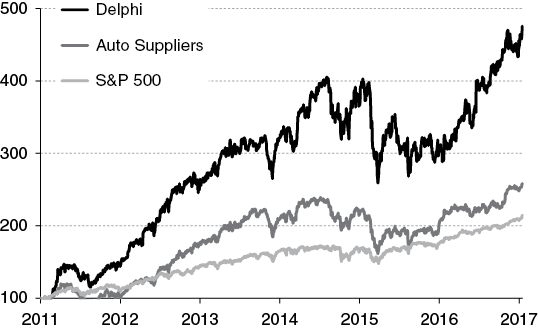

We then walked you through the tremendous success of the ensuing years culminating in the December 2017 spin-off. During this time period, investors were rewarded with a nearly five-fold return. By comparison, over the same period peer auto suppliers and the S&P 500 roughly doubled (see Exhibit PM.1).

EXHIBIT PM.1 Delphi Share Price vs. Auto Suppliers & S&P 500

(indexed to 100)

The Delphi investment decision at IPO relied upon multiple drivers, perhaps best summed up by the opportunity to buy secular growth at a cyclical price. The global auto market recovery was in its early stages and Delphi had a powerful secular story centered on “Safe, Green and Connected,” as well as a compelling growth opportunity in China. All of this was supported by a global best-cost footprint and a highly active Board and management team driven to create shareholder value. This created the opportunity for numerous catalysts, most notably earnings beats, share buybacks, and value-enhancing M&A.

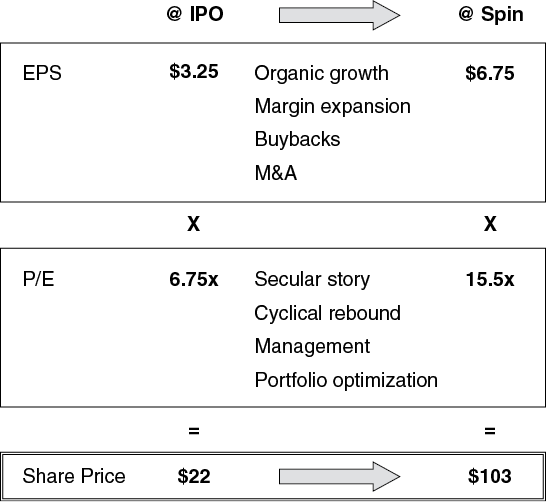

As the share price performance clearly demonstrates, the seeds of the core thesis were firmly planted in the years leading up to December 2017 when Delphi Automotive split into two separate companies, Aptiv (APTV) and Delphi Technologies (DLPH). By that time, EPS had increased from approximately $3.25 at IPO to $6.75. The trailing P/E multiple also expanded from roughly 6.75x to 15.5x by the time of the spin (see Exhibit PM.2).

EXHIBIT PM.2 Delphi Valuation Progression from IPO to Spin

At the same time, the spin transaction presented a natural capstone event for reassessing the investment thesis. First off, any spin merits de novo analysis given there are two new companies with distinct business models, strategies, and management teams. This was particularly relevant here given Aptiv's positioning as a premium auto technology pure play built around leading-edge businesses in active safety, infotainment, electrical architecture, and autonomous driving. Meanwhile, Delphi Technologies represented a pure play powertrain auto supplier whose fortunes were heavily tied primarily to global powertrain engine mix. These were two very different investment theses, indeed …

Furthermore, Delphi's meteoric rise from $22 to over $100 during the prior six years meant that profit taking, rebalancing, and other exit considerations were paramount. Per Exhibit PM.2, the P/E multiple was at a cyclical peak, representing a sizable premium to historical averages, and a solid premium to other auto parts suppliers. Add in a waning, late-stage auto cycle and the increasing drumbeat of trade tensions, and there were multiple reasons to revisit the overall investment thesis.

Post-Spin, 2019 and Beyond …

Sector

In 2018, the global automotive market began to slow. Global auto production estimates were revised downward throughout the year due to a combination of weakening demand, U.S./China trade headwinds, and new European emissions testing standards. Commodities and currencies also hurt auto companies' financial performance. By year-end, auto production was down 1.0% y/y and consensus was calling for another down year in 2019.

Auto stocks were affected accordingly with the average supplier decreasing over 20% in 2018. Across the sector, sales and earnings estimates were guided down throughout the year and multiples contracted, creating a double whammy for share prices.

2019 proved to be more turbulent than initially expected as auto production estimates continued to trend downward, ultimately declining nearly 6% vs. 2018. The biggest culprits continued to be China weakness, trade headwinds, and negative revisions in Europe and North America, including the impact of the General Motors strike.

Overall, 2019 was largely a tale of the haves and have-nots for auto stocks. Those companies tied to strong secular opportunities outperformed and those deemed most susceptible to macro pressures continued to suffer.

Below, we discuss how the 2018 to 2019 period played out for both of the Delphi Automotive successor companies, Aptiv and Delphi Technologies.

Aptiv (ParentCo)

Following the spin transaction, Aptiv began 2018 on a high note. Its secular growth story at the nexus of auto connectivity, electrification, safety, and autonomous driving resonated with investors. Company performance was strong, standing out from other auto players grappling with the headwinds described above. Aptiv actually increased guidance through Q1'18 and Q2'18. By mid-June, the stock was up over 20%.

By the fall, however, negative sentiment around auto stocks intensified—even Aptiv's strong performance and compelling story couldn't fight the tape. In Q3'18, Aptiv delivered top line organic growth of 9% y/y, representing a 12% delta vs. production volumes down nearly 3%. However, management guided to a weaker Q4'18 driven by an anticipated slowdown in China vehicle production, albeit still with respectable 6% organic top line growth, roughly 8% to 9% above the market.

By year-end 2018, Aptiv's share price had fallen from its mid-June peak despite more than delivering on the original full-year 2018 guidance. On a fundamental level, the company's strong secular growth story remained intact, differentiating it from other auto suppliers … and that story was ultimately rewarded in 2019.

Despite the broader macro auto headwinds, Aptiv established itself as a stock market darling in 2019. ESG (Environmental, Social, and Governance) and thematic investors dug in given Aptiv's now proven secular portfolio and better through-cycle performance, and Aptiv became one of the most widely held auto stocks. Towards the end of a choppy H1'19, the company held a well-received investor day where management reiterated its sustainable long-term growth and profit targets, as well as a compelling vision that extended through the middle of the next decade. Strong Q2'19 results lent further credibility to the story as a number of industrial and auto peers struggled.

Then, in September 2019, Aptiv announced the formation of a new joint venture with Hyundai centered on delivering its autonomous driving technology into production-ready vehicles. Aptiv's reputation for value-enhancing portfolio transactions, coupled with its Auto 2.0 positioning, further entrenched its status. By year-end, Aptiv was trading at $95 per share, not far off the pre-spin $103 share price for all of Delphi Automotive, outperforming all U.S. auto peers and more than making up for lost ground in Q4'18.

Delphi Technologies (SpinCo)

For Delphi Technologies, a.k.a., the legacy Powertrain Systems business, the macro headwinds were more pronounced. Negative mix factors related to the Delphi Technologies product portfolio and geographic exposure weighed on performance. Declines in diesel engine volumes, slowing production schedules due to new European emissions testing standards, and an abrupt slowdown in the local China market hurt Delphi Technologies disproportionately more than peers.

Compounding the above were some self-inflicted wounds related to execution, guidance, and communication to the Street. After initially increasing estimates post-Q1'18, management guided down the next two quarters. Unsurprisingly, this (mis)guidance exacerbated the negative reaction from investors.

Perhaps most damaging was the company's announcement on October 5, 2018, a true double jeopardy moment. In addition to disclosing that the CEO1 had abruptly departed, Delphi Technologies dramatically lowered its 2018 full-year outlook. The stock tumbled nearly 13% that day alone.

Its formal Q3'18 earnings call on November 7, 2018 did little to appease investors as management gave a disappointing 2019 outlook. By year-end 2018, the stock had declined precipitously, a function of lower-than-expected earnings and significant multiple contraction.

As anticipated by the market, 2019 was largely a continuation of 2018 for Delphi Technologies. The company began the year by suspending its dividend, and investors questioned its ability to manage through unfavorable China OEM exposure and a choppy macro backdrop. Further, profitability was in question as Delphi Technologies sought to transition its legacy internal combustion engine products to a new generation of products, including those for electric vehicles.

However, towards year-end 2019, new leadership was focused on executing a “self-help” strategy based on a multi-pronged internal restructuring. The new plan was centered on operational rigor, including a right-sized engineering footprint, better launch readiness, and reduced SG&A, as well as double-digit growth in key product lines. Both the company and market viewed 2020 as an important transitional year to start delivering on these initiatives.

Then, in January 2020, competitor BorgWarner announced a deal to acquire the company for $3.3 billion, which translated into $17.39 per share. At deal announcement, this represented a 75%+ premium to Delphi Technologies' pre-deal share price. The combined company would have complementary products and a more complete portfolio in traditional internal combustion engine components, as well as enhanced electric vehicle component capabilities.

Per our discussion in Step V, the post-spin trajectories for both Aptiv and Delphi Technologies are important case studies for proper risk management. The December 2017 spin marked a clear inflection point for the original Delphi Automotive investment that necessitated a baseline reassessment. Rigorous position monitoring, thoughtful sizing, constant re-testing of the investment thesis, timely profit taking, and patience are critical for driving outsized investment returns.

Note

- 1 The Delphi Technologies CEO came along with the MVL acquisition and wasn't part of the pre-IPO management team.