4

Accounting: The Figure in Dialogue

4.1. Performance systems

To illustrate the purpose of the Energy Transition for Green Growth Act (projet de loi relatif à la transition énergétique passed by the French National Assembly on July 30, 2014), energy was described as “this economically vital force, this force in action that irrigates all our activities in the same way as blood circulates in tissues and supplies cells while our communication systems, material and immaterial, manage its production and delivery, its circulation, its switching points and its distribution in the same way as a nervous system”.

This biological allegory positions the energetic transition between two levels of reality. A “force in action” thermodynamically influences the productive system, while the individuals and social groups that make up society retroact “like a nervous system” on the energy system.

If we refer exclusively to the energy sector that supplies French society, the thermodynamic conception of energy predominates. To continue the allegory, the programming of energy transition can, in this case, focus on ingestion, digestion, vascularization and the passage of nutrients to cells.

On the other hand, if we refer to French society in relation to the problems of energy transition, we give a central place to the human sciences. It is then necessary to think of the internal metabolism, according to the movements to which the whole organism is destined. The “energy reality” is then considered in terms of a social project, in a reflection that is no longer only sectoral, but territorial, and therefore qualitative and pragmatic.

Article 183 of the final text of the Energy Transition for Green Growth Act1, promulgated in August 2015, refers to the need for energy research and innovation policies to “mobilize all scientific disciplines and promote the development of multidisciplinary and transdisciplinary scientific communities around key themes”.

From this perspective, we must consider the ways in which these communities will represent the energy system, to collectively think about its transition. It is therefore important, on the one hand, to select the economic representations, methods and practices adapted to this transition, and more generally to sustainable development. It is also necessary to determine the modalities of these selections, which can be the result of a democratic process, as much as a capture and homogenization of collective rationalities by dominant actors.

Limiting oneself to a juxtaposition of views of an object or a physical phenomenon – in a multidisciplinary exclusivity – prevents one from discerning interfaces between the fields of knowledge useful to one’s economic understanding. On the other hand, encouraging the transdisciplinary combination of representations of this object or phenomenon gives rise to new, median knowledge useful for inclusion in a less compartmentalized, and sometimes more appropriate, field of analysis.

The formal emergence of an energy sociology (Zelem and Beslay 2015) offers, for example, the possibility of grasping, without distorting, the technical and social dimensions of energy objects and phenomena. If economics is to make a useful contribution to an ecological transition, the epistemology of a sustainable development economy must be clarified. It is exactly in these terms that the first chapter was introduced, which led to the developments of the first three chapters.

One of the objectives that we are now setting ourselves, by proposing the principles of a dynamic modeling of cost systems (DMCS) approach for sustainable management of the territories, is to combine the median knowledge necessary for interdisciplinary approaches to productive phenomena, with cross-sectoral accounting of the value associated with these phenomena, by the actors in the territory.

The entry point for illustrating the validity of this objective is a research program during which the contributory web portal ePLANETe.Blue made it possible to support actors in a collective representation of the interactions between strategies for circularizing the economy of an industrial sector, and the sustainability of their territory.

4.1.1. Coupling between functional ecosystems

4.1.1.1. Example of the circular economy of a territory

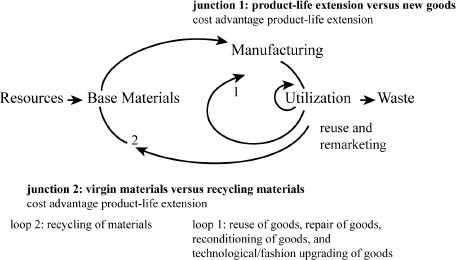

The circular economy model, already mentioned in Chapter 2 (section 2.1.1.1), aims to produce goods and services in a sustainable way by limiting resource consumption (raw materials, water, energy) and waste production. It is a question of breaking away from the linear economy model (extract, manufacture, consume, throw away) to move toward a more “circular” material flow model, described by the “4R” rule (Reduce, Reutilize, Reuse, Recycle).

Figure 4.1. The positive loops of the circular economy. Adapted and translated from Stahel and Reday-Mulvey (1981)

As part of the “Toward a circular economy – methodology and associated services” program led by the Agence Nationale Recherche (French National Agency for Research), the AGREGA project – “Anticipation et Gestion régionales des Ressources En GranulAts (Anticipation and regionalmanagement of aggregate resources)” – focused on the supply of construction aggregates to the Ile-de-France Region, as well as on the management of construction waste in Greater Paris. This project was completed in early 2018.

Compared to other sectors, aggregate producers currently have no demand levers, they can only respond to them, without influencing market developments. This situation makes it difficult to anticipate future needs – which are highly dependent on the speed of development in the Ile-de-France region (Chamaret 2015).

Two scenarios for responding to increasing demand have been identified (DRIEE 2012). The first involves a total consumption of 37.9 Mt/year with a regional dependency ratio maintained at 45%. The second considers the same consumption, but considers additional contributions exclusively from external regions, which leads to an increase in the dependency ratio5.

The response to Ile-de-France’s demand for aggregates involves both an increase in production effort in terms of volume, an increase in the quality of aggregates (ready-mixed concrete for buildings) and an effort to maintain the current level of dependence on external regions. This contradictory injunction is a source of great technical and organizational complexity for end users (development managers in the Ile-de-France region) and for stakeholders in the sector.

In a circular economy approach, the process of improving the construction aggregates sector in Ile-de-France involves broadening the scope of its analysis in order to qualify the performance of this sector in terms of reducing material flow. However, broadening the scope of the performance area considered may also lead to the study of how the aggregates economy fits into the major cycles of the biosphere (carbon, water, etc.).

The reflection then focuses on the first of the three levels of decoupling, described at the end of Chapter 2.

It is possible to further expand the analysis of performance; this time focusing on the social and economic effects generated by this sector at different scales of territory. This involves collectively building the meaning of this industrial sector in terms of social and economic sustainability, beyond a factual description of its effects in terms of material flows and ecological sustainability.

The reflection then focuses on the second level of decoupling: the one that reflects the relationship between multifunctionalities produced within the sociotechnical system and impacts on the energy-material flow, and therefore on the ecosystem.

The contributing web portal ePLANETe.Blue (see section 3.2) was mobilized during the AGREGA project to represent the industrial sector and then to collectively construct the meaning that can be given to the effects of its circularization. The issues considered to describe the system andproduce a deliberation matrix were identified by a socioeconomic study (Chamaret et al. 2015) conducted to initiate the AGREGA project. This study identified 11 sustainability issues for the Ile-de-France aggregates supply chain. Their understanding was then further developed during the project (Douguet et al. 2018).

These challenges of sustainability of the aggregates sector allow a link to be made between the three levels of decoupling.

A decrease in energy-material flow and ecological impacts (first level) implies a change in the sociotechnical conformation of the sector (second level), which can generate changes in use, with the potential to influence the profitability of the industrial activities that make up the sector (third level).

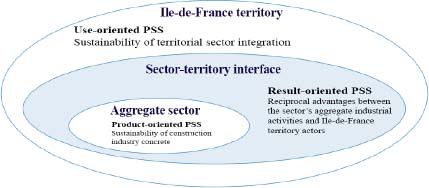

Before outlining an appropriate valuation system, it is necessary to clarify the object to be valued. Our proposal is to consider here the AGREGA project, which falls within a collective strategy led by the actors of the sector, in terms of product-service systems (PSS).

The PSS model is particularly suitable for value analysis at all three levels of decoupling. Comparing the three PSS strategies mentioned in Chapter 2 (section 2.1.1.2) makes it possible to address the diversity of issues, scales, levels and points of view, useful for the analysis of the aggregates supply chain in Ile-de-France.

- – Scale of the industry network and focus on material flows. The sale of recycled/reused aggregates within the industrial activity system – that constitutes the aggregates sector – is accompanied by the provision of two types of functionalities that can be recognized as services: extension of the lifespan of the mobilized aggregates (product longevity at the sector level) and lower consumption of virgin resources (benefits at the sector level).

- The system associated with the industrial sector can therefore be represented as a product-oriented PSS.

- – Regional scale and focus on the sustainability of the territorial anchoring of the aggregates sector. The presentation of the 11 sustainability issues (see Box 4.2) indicates that increasing recycling within the sector would be a source of useful functionalities for the Ile-de-France region. In other words, the sale of recycled aggregates within a sociotechnical system open to local actors is accompanied by services distinct from those, that form the basis for the transfer of ownership between manufacturers in the sector.

The system associated with the territorial anchoring of the aggregates sector can therefore be represented as a use-oriented PSS.

- – Views on the interactions between the industrial sector and the territory. The lessons of the AGREGA project (Douguet et al. 2018) highlight functional interactions between the two PSSs described above. These interactions can be illustrated as follows, though not exhaustively:

- - An increase in recycling on the scale of Ile-de-France buildings (material circularity performance) would contribute to fixing local employment while limiting the exhaustion of regional quarries, which would, in particular, make it possible to reduce the volumes and distances of imports and therefore the monetary costs and associated CO2 emissions (sustainability performance of the sector).

- - A capacity of the regional sector to limit, by its conformation, the expansion of the supply area (sustainability performance of the sector) would make it possible to avoid the opening of new supply channels likely to dump, on to the local market, overabundant resources whose presence would break the light competitive advantage currently enjoyed by recycled aggregate (material circularity performance).

More generally, the question of the price of recycled aggregate is part of a multi-criteria evaluation system that calls for a broadening of the scale of representation of performance and economic balances.

If the actors of the territory, and those of the industrial sector, co-construct scenarios aimed at increasing the use of recycling, in order to generate the functional benefits they expect from it, they contribute together to a result-oriented PSS.

Figure 4.2. Result-oriented PSS at the interface between product-oriented PSS and use-oriented PSS (Morlat and Douguet 2018)

The realization of an offer resulting from a coupling between two PSSs – one “product-oriented”, the other “use-oriented” – and giving rise to the recognition of a third – “result-oriented” – can then be sought.

4.1.1.2. Example of the rehabilitation of a building

After this approach to a mesoeconomic system described in terms of functional interactions, services and sustainability performance, it is interesting to consider the microeconomic influences that can be exerted on it.

The approach here will be quite similar to that proposed in the previous point, but the entry point for the illustration is a different research project. Through this project, we will highlight socioeconomic practices, allowing access to a joint level of sustainability and solvency that a technico-economic practice, on its own, would not have been possible to contemplate.

The CIRePaT project – Comment Impulser la Rénovation du Parc Tertiaire ? (How can we boost the renovation of the Tertiary Park?) – supported by the FONDATERRA foundation9 has made it possible to establish that a local authority can facilitate the use of thermal rehabilitation of private commercial buildings. This involves influencing the organization of the real estate sector, and the profitability of operations, through appropriate socioeconomic measures (pedagogy, urban planning, incentives, services).

In this situation, thermal rehabilitation and renovation strategies can be considered, but at financial costs that are often higher than those associated with deconstruction/reconstruction strategies. However, the ecological impacts of the latter are much greater than those of renovation strategies (Fondaterra 2012). Encouraging renovation is therefore necessary to ensure coherence in sustainable urban development.

Studies conducted in both territories revealed that managers of private tertiary real estate assets were often, economically, forced to choose new deconstruction/reconstruction strategies, but were likely to switch to new decision-making approaches.

An initial survey provided a better understanding of the technical characteristics of the parks and the perceptions of stakeholders regarding the project’s purpose. This phase distinguished, on the one hand, the actors of the real estate sector, and on the other hand, the actors of the local authorities.

The next phase catalyzed exchanges between different actors in the real estate sector: tenant companies, landlords and occupants, investors, marketers, developers, managers, etc. The objective was then to identify a set of action levers enabling local authorities to influence the issues identified during the diagnoses; this was in order to encourage owners of the private tertiary park to invest in the renovation of their heritage.

Social and environmental lifecycle analyses such as those discussed in Chapter 2 (see section 2.1.2.1) could reveal the beneficial effects of a shift from new deconstruction/reconstruction strategies to rehabilitation strategies.

Direct effects would appear with regard to the consumption of building materials, energy, water and the management of deconstruction waste. These effects would make it possible to provide more or less tangible and diffuse, but still very real, economic benefits (services) to various activities at different time and territory scales10.

In other words, it is possible to extend the functional ecosystem associated with a building rehabilitation operation. Several strategies are then available.

The operation can be considered as a “product-oriented” PSS. It contributes to improving the intrinsic functionalities of the building, minimizing the resources consumed by the product that constitutes this building, as well as the durability of this product (unlike a deconstruction/rebuilding strategy).

It can also form the basis of more ambitious, “use-oriented” and “result-oriented” PSS strategies (see sections 2.1.1.2 and 4.1.1.1).

The transition from a deconstruction/reconstruction strategy to a renovation strategy provides a much more significant service to the community than the benefits directly related to the building.

From a mesoeconomic point of view, a community could, for example, be interested in the effects of private tertiary rehabilitation on the aggregates sector. A generalization of rehabilitation options would considerably reduce the need for building materials and contribute to reducing the tension on the aggregates market, which weaken the sustainability of the regional sector.

In other words, organizing – at the microeconomic level – the meeting of the interests of local authorities and those of private tertiary real estate actors would bring mesoeconomic functional advantages to the aggregates sector and the territory.

Addressing the composition of these strategies through regional, social and environmental lifecycle analyses would clarify some of the components of these benefits and their beneficiaries. However, these analyses only provide data that must be collectively interpreted in such a way that information is constructed and functional advantages are mutually known – or recognized.

4.1.2. Multiscalar and cross-sectoral scenarios

4.1.2.1. Representing a functional coupling

The term functional coupling refers here to the analytical relationship between two functional ecosystems whose interaction, socially recognized, can also be recognized by the economy.

For example, the fact that an increase in the number of rehabilitations functionally influences the evolution of the regional industrial aggregate supply chain can easily be illustrated; we have just done so in the previous point. The recognition of economic interests in taking action and designing economic strategies that integrate the thinking carried out at these different levels, is less obvious.

Qualifying the benefits of the influence of one activity on another is one thing, combining these benefits with joint variations in the performance of the activities receiving the benefits is another. It is necessary to distinguish how these performances are achieved, to establish who is able to observe them, to qualify them and establish the consequences of taking into account their effects, in terms of valorization.

This analytical coupling approach between two functional ecosystems also implies overcoming certain obstacles, linked to current territorial proximity (spatial, organizational, institutional). The fact that the activities that generate and benefit from functional advantages do not belong to the same sectors may lead to sociological, technical or regulatory limits to the recognition, support and enhancement of performance.

Unlocking the frameworks for representing temporalities and spaces for assessing productive phenomena is then necessary: the profitability of recycling or rehabilitation of buildings is sometimes not immediately obvious at the microlevel, while the performance of these activities is necessary for profitability at the sector level.

A functional coupling of micro- (recycling, renovation) and meso- (aggregates sector) ecosystems would thus testify, not only to the recognition of the interactions between the PSS they incubate, but also to an evolution of the governance process of each one, thus leading – via the reconfiguration of their logic of existence – to a structural coupling of the business models that characterize them.

The notion of structural coupling is borrowed from Maturana and Varela (1994) and aims here to suggest a limited analogy with the notion of autopoiesis. This describes how a cognitive system will transform – from its own organization – to compensate for disruptions caused by external events (see section 3.2.2.1). The fact that this system continuously adapts to these disturbances, while maintaining its identity, is called structural coupling.

Here, being aware of the limits of the analogy, the mesostructure of the industrial aggregates sector is affected by the “disturbances” induced by the evolution of the microstructures of the industrial sectors, from private tertiary immobilization.

Changing the qualification of these “disturbances” to call them “benefits” is a process of social recognition, consisting of changing the level of representation, in order to address economic and political rationality, at the scale of a new functional ecosystem. This is the approach presented in the previous point: to include two PSSs, “product-oriented” and “use-oriented” in a third “result-oriented” PSS.

During the ANR “AGREGA” program, the contributing web portal ePLANETe.Blue, introduced in Chapter 3, made it possible to support the actors of the Ile-de-France region’s aggregates supply chain in a collective representation of the interactions between circular economy strategies and the challenges of territorial sustainability.

The use of the KerBabelTM Deliberation Matrix (KDM) made it possible to support evaluation sessions of five scenarios for the territorial inscription of the aggregates sector11. These deliberations highlighted the functional nature of the sector: an integrated system and not just an articulation of industrial activities, anchored in a commercial relationship.

During the deliberations, each contributor was able to compose sets of indicators12 allowing them to express a value judgment on how the scenarios address the sustainability issues of the aggregates sector (see Box 4.2, section 4.1.1.1). These indicators have been documented, and their meta-information enriched, in the KerBabel™ Indicator Kiosk (KIK).

As for the KerBabel™ Representation Grid (KRG), it was used both as ex-ante and ex-post: the work of identifying the relevance of the indicators, by putting them in context in relation to the knowledge mobilized by the actors, led to the continuous proposal and updating of a list of indicators adapted to the evaluation of the scenarios.

The ePLANETe.Blue portal could enable actors in the Ile-de-France region to go further, in particular by co-producing an ad hoc evaluation methodology, designed to promote the shared representation of a functional coupling between productions, hitherto considered independently.

This approach was initiated by O’Connor et al. (2015), in the laboratory13, as a complement to the official developments of the AGREGA project.

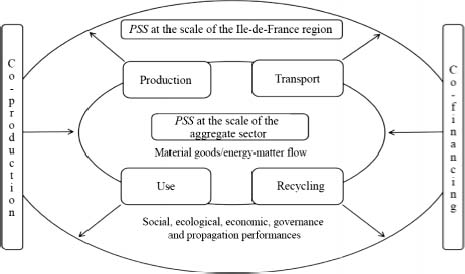

First of all, we distinguished four phases of an “aggregate life cycle” (Production, Transport, Use, Recycling).

This separation of different phases favors the projection of strategies for the joint achievement of micro and meso performance, as well as the structural coupling – and therefore articulation – of the PSS business models likely to be associated with this performance.

Figure 4.3. Functional coupling in the analysis of micro–meso performance and structural coupling of micro–meso PSS merchant offers. The case of the aggregates supply chain in the Ile-de-France region

A multi-criteria evaluation algorithm of the KerBabelTM for You (K4U) type was then developed14 (“Granulates for You” [G4U]). Its construction was based on the crossing of the four phases of the aggregate lifecycle mentioned above, with five performance areas – social, environmental, economic, process and propagation performance (see section 3.1.1.2) – inspired by Bosch et al. (2013).

Each of these axes has been assigned six subsidiary performance objectives, the achievement of which has been described by thematic indicators – quantitative or qualitative.

We have used these indicators to reflect the influence of evolutionary scenarios for each phase of the aggregate lifecycle (columns in Table 4.1) on the achievement of the subsidiary performance objectives of the regional aggregate supply chain (rows in Table 4.1).

There was therefore no question here, contrary to the subject of AGREGA’s official developments, of deliberating on how scenarios for the territorial anchoring of the sector are likely to respond to sustainability issues specific to this sector. The G4U tool provides a multi-criteria evaluation algorithm that is both normative and more generic. Its purpose is both to provide elements for comparison with other sectors and territories, and – due to the phased approach – to reflect differences in the points of view of stakeholders influencing different phases of the aggregates lifecycle.

For some of the subsidiary objectives associated with the performance axes (the “5Ps”), a single indicator makes it possible to cover all four phases of the lifecycle, and the rules of interpretation and standardization are the same for each of these phases. For other objectives, the same indicator covers the four phases, but different standardization rules are proposed, due to the specificities of the activities of these different phases. For others, while the same logic for defining indicators is associated with an objective for all phases, the indicators and associated meta-information vary according to the phases.

The K4U tool, developed by associating six subsidiary objectives to each performance axis, as well as a typology of indicators specific to each of these objectives, constitutes a manageable and synthetic system.

Table 4.1. Indicator system mobilized by the “G4U” algorithm (O’Connor et al. 2015). For a color version of this figure, see www.iste.co.uk/morlat/sustainable.zip

| Indicators | ||||||

| quantitative | qualitative | |||||

| Performance criteria | Lifecycle phase | |||||

| Axes | Subsidiary objective | Production | Transport | Use | Reuse | |

| Social | Health and safety | Work-related accidents | ||||

| Employment | Workforce | |||||

| Job satisfaction | Absenteeism | |||||

| Difficult working conditions | Difficulty | |||||

| Employability | Competencies | |||||

| Noise pollution | Permissible level | |||||

| Environment | Materials | Addition to stock | Traffic | Addition to stock | Stock management | |

| Water | Blue water footprint | |||||

| Energy | Energy intensity | |||||

| Climate | GHG emissions | |||||

| Air quality | PM10 emissions | |||||

| Environmental commitment | Level of environmental commitment | |||||

| Economy | Physical consistency | Forecast availability | Loads continuity | Rational use | Quality of resources | |

| Profitability | Interpretation of the EBE | |||||

| Cost of production | Operating expenses | |||||

| Investment | Depreciation of assets | |||||

| Resilience | Adaptation to demand and flow management | |||||

| Local value | Local value creation | |||||

| Process | Involvement | Involvement of stakeholders | ||||

| Understanding | Shared culture | |||||

| Experience | Solution experience | |||||

| Representativeness | Diversity of influences | |||||

| Social dialogue | Internal reflection | |||||

| Impulse | Leadership | |||||

| Propagation | Technical system | Technical and prospective strategy | ||||

| Economic outlook | Comparative availability | Comparative costs | Comparative costs | Comparativecosts | ||

| Copatibility | Compatibility with the supply chain | |||||

| Acceptability | Societal acceptability | |||||

| Regulation | Regulatory developments | |||||

| Business models | Legal and economic arrangements | |||||

The operation of the “G4U” algorithm was then tested on the basis of a fictitious case. The presentation of the results obtained will be described in Chapter 6 (see section 6.1.2.2.2).

4.1.2.2. Designing new areas for collective performance

Designing the G4U algorithm, dedicated to evaluating the performance of the territorial anchoring of the aggregates sector, required the establishment of the institutional outline of the activities that make up this sector.

To this end, we have used the classification proposed by the Nomenclature d’Activités Française NAF Rév.2.1 (INSEE 2015a). For each phase of the aggregate lifecycle, different classes of this nomenclature have been selected to represent the global overview of activities considered relevant (see Table 4.2).

Table 4.2. Indicative classification of activities concerning the “aggregate lifecycle” based on the French NAF Rev.2.1 (2015) nomenclature

| Exploitation | |

| Code: 08.11Z | Extraction of ornamental and building stones, industrial limestone, gypsum, chalk and slate |

| Code: 08.12Z | Mining of gravel and sand pits, extraction of clays and kaolin |

| Transport | |

| Code: 49.20 | Rail freight transport |

| Code: 49.41 | Road freight transport by road |

| Code: 50.40 | Inland water freight transport |

| Code: 52.10 | Warehousing and storage |

| Code: 52.21 | Services auxiliary to land transport |

| Code: 52.22 | Services auxiliary to water transport |

| Use | |

| Code: 46.13 | Intermediaries in the timber and building materials trade |

| Code: 46.73 | Wholesale of wood, building materials and sanitary appliances |

| Code: 23.61 | Manufacture of concrete elements for construction |

| Code: 23.63 | Manufacture of ready-mixed concrete |

| Code: 23.64 | Manufacture of mortars and dry concretes |

| Code: 41.20 | Construction of residential and non-residential buildings |

| Code: 42.11 | Road and highway construction |

| Code: 42.12 | Construction of surface and underground railways |

| Code: 42.13 | Construction of bridges and tunnels |

| Code: 43.11 | Demolition work |

| Recycling | |

| Code: 38.11 | Collection of non-hazardous waste |

| Code: 38.21 | Treatment and disposal of non-hazardous waste |

| Code: 38.32 | Recovery of sorted waste |

| Code: 46.77 | Wholesale of waste and scrap |

For each NAF code with a rank of “XX.XX.”, the details of the subcategories (which do not appear in Table 4.2) have been detailed to provide a precise specification of the activities concerned. This first framework for institutional representation of the aggregate lifecycle is intended to be enriched beyond the actors directly involved in the industrial sector.

The definition of such a “perimeter” of activities is necessarily a subjective choice, but it must not be arbitrary and fixed.

For example, for code 50.40 “inland freight transport”, we considered freight transport on rivers, canals, lakes and other inland waterways, including ports and docks. We also chose to consider the rental of crewed vessels for the inland waterway transport of freight, as this was justified from a functional point of view. However, we did not consider pushing and towing services by river, which is a questionable choice.

We have also taken into account for code 52.22, “services auxiliary to water transport”, the activities of operating terminal facilities such as ports and wharves, operating locks, navigation, pilotage and anchoring activities, as well as rescue and lightering activities.

These “expert” choices, in the laboratory, were intended to emphasize the supporting function of these activities. However, within the framework of a territorial approach, only deliberations between actors – that have led to the emergence of indicators specific to a social understanding of this support function, of its value – would have been likely to legitimize them.

What we wish to illustrate here is that the analytical framework, mobilized by the industrial economy by reference to a homogeneous production unit (HPU), does not directly allow the enhancement of multifunctional productions.

Such a production unit is only observable if a local kind-of-activity unit (KAU) “produces only one type of product and does not carry out any secondary activities” (Eurostat 2013, point 1.60). However, these HPUs are the constituent units of the homogeneous branches of activity of the French NAF rev. 2 nomenclature, of activities and products – CPF rev. 2.1 (INSEE 2015).

As the first level of objectification of interactions between activities in a territory, the HPU is therefore also a first level of reductionism! The economy must integrate this analytical object – the HPU – into another structure for representing production processes.

It is the purpose of the circular economy and industrial ecology strategies (see section 2.1.1.1.1) that reconfigure the functional organization and contractual structure of the links between physical production units. To reinforce this dynamic, a new framework of shared representations must make it possible to describe the influences of actors, outside the HPU that constitute this structure.

In short, it is not only a question of addressing the functional consequences of a reconfiguration of the industrial structure, but also of reflecting the various functional influences – particularly institutional – on this structure.

A carbon tax applied to the HPU “road freight transport” (NAF class 49.41) would lead, for example, to considering the influence of this tax on the relations between an HPU “Construction of residential and non-residential buildings” (NAF class 41.20) and an HPU “Recovery of sorted waste” (NAF class 38.32).

Continuing this approach would imply considering the institutional actor, that is the source of the implementation of this carbon tax, as a producer of a range of phenomena that can be identified as useful to other activities in the industrial sector, and, beyond that, to society. And, once these utilities have been identified, it would be necessary to consider their qualification, in particular through the production of performance evaluation standards, based on social and commercial contracts.

Taking here again the example of the supply of aggregates to the Ile-de-France region, and limiting the hypothesis of applying a carbon tax to the activities of the “transport” phase, two categories of services, provided by the territory to the sector, can then be distinguished:

- – Services directly related to the interactions between the transport activity and other industrial activities, concerned with transactions involving the material property whose transport is taxed.

- – For example, taxing carbon emissions increases the cost per metric tonkm, which leads to a potential preference for the local and encourages recycling activities, which provide feedback on transport activities (modal shift and reduction of long-distance traffic), thus increasing the efficiency of the tax.

- – Services related to indirect interactions between the industrial sector, whose transport activities are taxed, and activities that are not directly affected by the tax or by transactions involving the transported material goods.

For example, increasing the acceptability in urban and peri-urban areas of sorting and processing sites for deconstructed building materials promotes recycling, which helps to reduce tension on local deposits of “natural” aggregates and thus to contain the distance between supply sources, therefore providing feedback on transport activities, thereby increasing the efficiency of the tax.

Both types of services can be characterized by performance commitments, which can be qualified by indicators that can be translated into ratios between non-monetary and monetary data. These indicators and ratios can be included in contracts between actors in the sector and actors in the territory. In other words, they can contribute to establishing communication between the actors of the industrial sector and the actors of the territory, concerning the inclusion of ecological taxation in a shared representation of the territorial economy.

4.2. Cost systems

The first part of this chapter raises a relatively clear question: how do we produce a functional valorization system, when performance representations are captured by the structure of trade in physical goods?

In practice, it is difficult to value functional influences in the space of territorial representation. Transactions are still mainly confined to the “value chain” and “homogeneous branches of activity”. Beyond the established organizational and institutional proximity, actors do not necessarily recognize each other’s mutual interests and most often, have no prior communication experience.

We will take up Zacklad’s (2006) position here: “Recipients may not perceive the benefits of the functionality offer at first sight and providers must demonstrate its usefulness and consistency, as is the case for any innovation. It is in this sense that the functional economy we stand for can be called constructivist15. Functionality does not exist forever; it is the result of a cooperative construction between suppliers and recipients that corresponds to the transformed vision of a series of transactions that were previously independent”.

The objective of the DMCS approach is precisely to make visible the dependency of transactions that currently appear independent.

The aim is to develop collective representations of the economy of a territory, by identifying functional couplings, and to promote consistency in each other’s business models, i.e. to support structural couplings. The challenge is not only to renew the interactions between the activities of a sector, but to allow third parties to analyze these interactions, through a more appropriate reading grid than that of administrative nomenclatures based on the HPU.

Moving from the representation of functional couplings to that of structural couplings, implies encouraging the embodiment of political negotiations through new local management practices – likely to provide feedback to public actors – aiming as much as possible to fundamentally reinforce their ambitions for sustainability, while legitimizing these conditions economically.

Microeconomic market transactions, caused by the renovation activities of the private tertiary park, can have an influence on transactions at the territorial level. And we have illustrated the potential for action by local authorities that invest in cooperative, non-market transactions, in order to put in place various levers to stimulate these renovations.

What is lacking in communication between politics and economics is an ability to account for these changes in scale in value analysis, without separating monetary and non-monetary information, and without the focus on the former reducing the readability of the latter.

4.2.1. Internalization and territorialization

4.2.1.1 Internalized “green” value

The concept of green value – introduced by the Royal Institution of Chartered Surveyors (RICS) in the United Kingdom – has, since 2005, highlighted a link in Canada and the United States, between the environmental quality of a building and its market value. This concept may be interesting to mobilize in the context of transactions relating to private tertiary real estate.

Different methods from neoclassical logic are used to approach this green value:

The “valorization by comparison” compares prices of two properties: one renovated, the other with similar characteristics except for renovations16.

The “hedonistic” approach (Ridker and Henning 1967; Rosen 1974) makes it possible to refine valorization. It isolates implicit offers and requests for certain components of the renovated property. A statistical calculation then evaluates the possible influences of these offers and requests on the sale or rental price of this property17.

The “total cost” approach evaluates the distribution of building costs over its entire lifecycle, from design to deconstruction (MIQCP 2006; MEEM/CGDD/SEEI 2009). It distinguishes technical and financial costs considered elementary costs, intangible determinants of the economic performance of a real estate asset, and externalities.

The “capitalization” approach considers the influences of the property’s environmental performance on its market value. This performance, combined with a reduction in risks and/or costs, has a positive impact on the ratio of net income to capitalization rate.

Other methods can be used however, we will not focus on them: what is important here is to present the green value as the neoclassical transcription of a valorization of informal services, within an ecosystem of real estate actors. In other words, the green value is the neoclassical expression of a recognition of functional relationships. And from this perspective, the methods described above are sufficient for our demonstration.

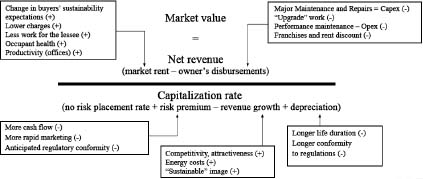

Lorentz (2010) proposes a representation of the determinants of the green value creation process, based on both the hedonistic and the capitalization valuation methods.

Figure 4.4. Formation of “green value” in private real estate, in the case of a rental. Reproduced from Lorentz (2010)

However, distortions in market maturity that may recognize the service components of a building’s energy renovation are regrettable18. Indoor air quality19, considered a cost reduction factor – and factorized in the Lorentz relationship – will only arouse the interest of stakeholders, for example, long after another factor, comfort of use (Bouteloup et al. 2010).

These distortions limit the application of the total cost method, which invites consideration of costs and benefits over the entire lifecycle of the building.

More fundamentally, let us recall here that what neoclassicals call factors corresponds, in a functional economy, to the emerging property of a system composed of elements and functions; and factoring in this property, without taking into account the conditions of its emergence, weakens the evaluation.

Air quality and comfort of use are, for example, inseparable from the emergence of another phenomenon – absenteeism – which by its obvious managerial materiality has a strong impact on investment choices. Extracting from these three phenomena only factorial information intended to be used in the definition of a market price, would make the understanding of their emergence impossible.

Lorrentz’s approach, which is nothing more than an internalization of externalities, must be based on a systemic analysis of value, and this systemic approach must never be abandoned.

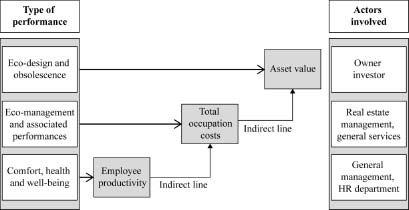

Productivity at work and the reduction in absenteeism, due among other things to increased comfort and the satisfaction of knowing health quality is taken into account, are to be compared with the total cost of occupying office buildings that have been renovated.

Figure 4.5. The beneficiaries of green value and the value chain (offices). Reproduced from Bouteloup et al. (2010)

A use of the comparative method is then just as delicate, if it is simply a question of focusing on prices, and therefore on the exchange value of physical and real estate assets, and not on the value of the uses on which it is based.

Anchoring this comparative method in a broader analysis would make it possible to address the green value of a renovated real estate asset, together with that of other intangible assets, i.e. together with the valuation of the immaterial capital of the entity that owns the building (see section 2.1.2.2).

This would involve comparing the goodwill of the entity that owns the renovated physical property with that of an entity that owns an asset with similar characteristics other than renovations. It would then involve structuring the intangible capital of these two entities in such a way as to highlight the characteristics taken into account by the other three methods described above.

This approach is not inaccessible. Since 2002, IAS20-IFRS21 standards have required “component-by-component” accounting of tangible fixed assets. It then becomes possible to subdivide a real estate asset into several elements, for example by distinguishing the envelope, the energy system, the roof, the equipment, etc. And so, by isolating the different body components, it is possible to approach the equipment/usage relationships with greater precision.

In other words, decomposing tangible fixed assets would allow entities to formalize intangible assets, specifically designed to describe the interface with internal social organizational arrangements, i.e. to characterize the uses that influence building performance.

For Biojo et al. (2012), component-by-component capitalization makes it possible to distinguish between items whose future economic benefits will go to the assets of the entity, and those that will probably go to the investor, as well as to other partner actors.

This is entirely in line with the logic of saving functionality. In the case of the study we presented, a rehabilitation of a building envelope is an investment in an asset component, and this investment, which increases the lifespan of the building, also delays the deconstruction/reconstruction deadline, which has a functional influence on the aggregates sector (reduction of market tension).

At this stage, it remains necessary to consider, more precisely, how the recognition of this useful functional influence – i.e. this functionality – can be formalized at the territorial level. It will then be necessary to propose a logic of integrated analysis of the values associated with the micro-investment, and the mesoeconomic functionalities produced by this investment.

4.2.1.2. Territorialized “green” value

If, as we have just illustrated, the “green value” of a renovated building does not only depend on technical characteristics, and if its recognition is influenced by phenomena internal to the entity managing the property asset (design, occupancy scenarios, technology/competence adequacy, loss of information, facility management, uses, occupant behavior, etc.), it also depends on external phenomena, determined by the local organization of relations between actors.

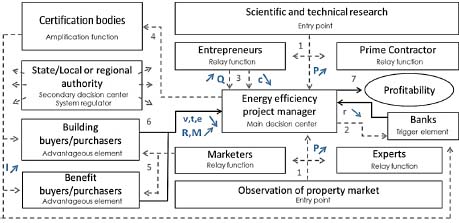

Chazel (2009) approaches the green value production process from a perspective that remains microeconomic but which, unlike the approaches discussed in the previous point, places it in an interorganizational perspective.

For him, constituting evidence of the legal, economic and technical reliability of operations (P) allows owners and project owners (prime contractors) of energy renovation projects to guarantee (1) the achievement of the expected benefits. Communicating (2) this evidence to banks and investors changes their perception of the risk involved, resulting in an improvement in the borrowing rate (r) associated with the project in question22.

Figure 4.6. The process of forming green value. From Chazel (2009)

In the model proposed by Chazel, it is therefore the converging information from the technical and commercial spheres that initiates the process. Prime contractors, due to the reduction in the borrowing rate, may be financially able to carry out ambitious operations of good environmental quality (Q). This ambition is necessary for the organization to be able to benefit from the leverage effect (3) of financing these ambitious operations: the reduction in operating costs (c), due to energy savings as well as all related extra-energy effects having an impact on market value.

Chazel then describes an amplification of this process (4). Certification bodies may jointly recognize the sustainability of the economic structure (certification of the financing system) and the technical quality of the operations (certification23). It is also necessary to take into account the work of marketers who contribute to the acculturation of actors and therefore to the evolution of the local market (5). Properties of good environmental quality then benefit from a better image (I). If this image is conveyed to customers and financiers (6), it increases rents (R) and market (M) values, and contributes to reducing building vacancies (v), marketing times (t), as well as the expenses associated with these valuations and marketing (e). The profitability of the project (7) is then improved.

The approach proposed by Chazel (2009) can be broken down into three phases of information production that involve several stakeholder systems:

- – sociotechnical information validating the state of a “niche” within the sociotechnical system in order to provide proof of technical and commercial reliability;

- – technical and economic information attesting to the effectiveness of the financial leverage that allows technical choices resulting in energy savings;

- – socioeconomic information certifying the project’s performance, translating it into available functionalities and promoting the adequacy of the expression of functional needs, in line with the state of these availabilities.

First of all, it should be noted that the transition from one of these phases to the other corresponds to a Communication in the sense of Luhmann (see section 3.1.2.1). For example, the transition between technical and socioeconomic information, which is the result of a Communication between certifier and client, combines the positions of information (by sanctioning technical performance), communication (production of the label) and the expectation of success (perception of an image of the environmental quality of the building). However, for each of these positions, the couples [indicator – meta-information] are not constructed in the same way24.

Let us then note that the approach we are taking – considering green value in a logic of cooperative transaction in a functional ecosystem – at least prompts opening this Communication to two other levels of dialogue around value:

- – a dialogue between actors involved in the realization and recognition of internal phenomena within the management organization of the renovated building;

- – a dialogue between stakeholders in the territory likely to influence and/or be influenced by interorganizational phenomena in the real estate sector.

It should be recalled that in the context of our approach, the objective of this territorialization of value analysis is, on the one hand, to discern how different levers of action by local authorities (Box 4.4, section 4.1.1.2) could be used to stimulate renovation, and, on the other hand, to identify how and to what extent territorial economic analysis could formalize the link between the political choice to promote a lever of action, and the influence of exercising this lever on the conformations of territorial industrial sectors.

Let us now return to the proposal introduced in the previous point, which considers the possibility of recording accounting assets component-by-component, in order to structure the immaterial capital of entities around a pair [equipment – use].

The most fundamental point we would like to introduce here is that the analytical logic that makes it possible to formalize intangible assets corresponding to a pair [equipment – use], within a real estate entity, can be transposed to the mesoeconomic scale.

In a functional economy, the “equipment” of the territory is, in our opinion, made up of natural capital, manufacturing capital, as well as, of course and above all, human and social capital, the organization of the actor’s game – i.e. governance – and the conformation of the sociotechnical system, its adequacy for the spread of innovative and sustainable solutions. In short, this “equipment” corresponds to the combination of the sociotechnical system in which the functional ecosystem evolves, and the territorial heritage that feeds the emergence of this ecosystem and feeds the permanent reconfiguration of the sociotechnical system.

In our opinion, the “use” of the territory, in a functional economy, corresponds to the revelation of the potential of the territory constituted by the territorial proximities in the sense of Colletis et al. (2005), i.e. a situation of coordination ranging from the collective resolution of a problem, to a territorial project, therefore to the inclusion – in particular contractual – in a common horizon, one of the components of which can be valuation.

Our discussion now and throughout the rest of the book will turn to the adequacy of accounting and political, micro-, and macroeconomic information systems, when it comes to reporting on the co-evolutions between the use of industrial economic equipment and the “use” of “equipment” – or rather the mobilization of a natural and social heritage – of the territorial economy.

4.2.2. Structuring the micro–macro accounting space

4.2.2.1. Microeconomic accounting and territory

According to the definition given by the French General Accounting System (PCG) (article 120-1), “Accounting is a system for organizing financial information in order to capture, classify, record basic figures and present statements that reflect a true and fair view of the entity’s assets, financial position and results at the balance sheet date”.

Although used internationally, particularly in Europe since Council Directive 78/660/EEC of 25 July 197825, it is not defined by the French General Accounting System (PCG) (Revault 2009). This notion is highly controversial26 (Honoré 1994; Haverals 2006). It can only be heard in accordance with the accounting principles and rules in force. “In other words, ‘fidelity’ cannot be assessed in relation to a reality that does not exist in itself: the true and fair view results from the application of the good faith of accounting rules” (CNCC 1989, p. 128).

However, while the first paragraph of Article 10 of the French Commercial Code states that, “The balance sheet, income statement and notes must include as many headings and items as necessary to give a true and fair view of the company’s assets, financial position and income”, Article L. 123-14 of the same Code states that, “When the application of an accounting requirement is not sufficient to give the true and fair view referred to in this article, additional information must be provided in the notes” and that, “If, in an exceptional case, the application of an accounting requirement is not appropriate to give a true and fair view of the assets, financial position or results, it must be waived. This derogation is mentioned in the notes to the financial statements and duly justified, with an indication of its influence on the company’s assets, financial position and results”.

In short, the true and fair view of the entity’s assets (all its properties), financial position (its balance sheet) and result (prepared in the income statement) is based on the current state of institutionalization of accounting practices. And these practices may be called into question when it is necessary to produce additional information or to depart from certain accounting specifications, and then to document this information, these departures and their reasons, in the notes to the financial statements.

However, to be exact, accounting in a functional economy oriented towards strong sustainability of territorial development implies a questioning of accounting practices. However, this challenge cannot be satisfied by an exceptional derogation documented in the accounting Annex.

For Rambaud and Richard (2015), it is the usual double entry accounting system itself that is obsolete. They do not attribute this obsolescence to the technical characteristics of this system, but to its objective: the sole maintenance of financial capital27. Their approach therefore consists of keeping it, but combining it with other objectives and practices to offer a method that we promote because of its strong suitability for the analysis of multifunctional productions: the CARE® system (Comprehensive Accounting in Respect of Ecology). This system, designed by Richard (2012), is also known as CARE/TDL28, the name Rambaud and Richard now give it as they continue to theorize and develop.

To adapt the double entry to a sustainable development objective, CARE® proceeds from an “extension of the application of very traditional accounting principles to human and natural capital” (Richard 2012, p. 147).

Before detailing this approach, it should be noted that CARE®is an “internal – external” accounting system, taking into account the effects of the entity’s activity on the territory, and not only the reverse – as the current accounting system does29. Human and natural capital should therefore be recorded as liabilities, as capital to be retained, instead of considering them “only as resources to be used on the assets side and/or as charges on their profits” (ibid.).

CARE® refers to an open approach to capital: “capital is a capacity (or set of capacities) recognized as having to be maintained over a certain predetermined period of time on the liabilities side of the balance sheet. A resource consists of a capacity (or a set of capacities) directly available to be used on the assets side of the balance sheet” (Rambaud and Richard 2015).

This openness and the internal-external perspective is of interest to us in that they formalize the relationship of an entity to its functional ecosystem through the double entry system, i.e. the balance sheet of that entity.

The entity may consider functional production apparatus, constituted by various activities in the territory, as a capacity to be maintained, and the functional advantages conferred – the functionalities – as capacities available for use. To this end, it will enter on the liabilities side the costs necessary to contribute to the maintenance and/or renewal of the functional territorial productions on which it depends, and on the assets side, that they the use value of the functional advantages it recognizes.

The logic of contributing to the cost of maintaining and/or replacing the entity’s territorial capital derives from a guiding principle of the CARE® system that states that “the value of capital is equal to the costs of its maintenance, according to its ontological specifications and during its predetermined period of re-assessment, if all the corresponding resources are consumed” (Rambaud and Richard 2015).

CARE® is therefore historical cost accounting – a specific representation of the company’s process, independent of supply and disposal markets (Richard 1976). And giving a full account of the specificity of the company’s process implies a specific use of depreciation, which will reduce, on the one hand, the assets concerned (which lose a part of their “cost value”) and, on the other hand, reduce the result of the financial year, i.e. as expenses or reduction of liabilities (Rambaud and Richard 2015).

This depreciation is applied jointly but differentially to human, natural and financial capital. This is how the triple depreciation line appears, the importance of which is highlighted in the acronym CARE/TDL.

By reducing the result of the financial year, after depreciation of assets resulting from the use of natural and human capital, the funds needed to maintain/renew these assets ex ante, i.e. for preventive investment, can be released. The result here is therefore a surplus, beyond the maintenance/renewal of the various types of contributions – including financial capital and capacities conferred by the territory. This characteristic makes CARE® a method whose institutionalization would allow accounting with a strong sustainability objective.

The application of this method involves monitoring and managing human and natural capital through the use of “spokespersons” for social groups and ecosystems. These “representatives” (scientists, NGOs, trade unions, occupational physicians, local communities, public bodies, etc.) would have to speak for human and natural capital, with the entity, in order to facilitate the description and analysis of the links between the entity and the territory.

According to Rambaud and Richard (2015), this notion of spokesperson (focused on capital) replaces that of stakeholder, which is considered only as an actor who brings interests and/or risks to the entity. The role of these spokespersons would also be to relay the controversies attached to this capital, the way in which it is represented and managed. The spokesperson would be responsible for bringing these controversies to the level of the entity, but also to the branch of activity and the functional ecosystem. This approach “connects a redefinition of accounting with a redefinition of governance, from a co-determination perspective” (ibid.).

Let us now turn to another microeconomic accounting innovation that could also be useful for Communication between entities contributing to a PSS.

Comptabilité Universelle® (Universal Accounting) (Schoun et al. 2012) is a state-owned cost accounting system whose purpose is to assess the influence of an entity’s external effects on its general accounting. It addresses the influence of the entity’s mesoeconomic and environmental effects: its influence on local governance and its societal anchoring effects – the latter domain can be separated to distinguish social and societal (Schoun et al. 2012, p. 48). Each of these areas is considered through the traditional accounting formalism (double entry, income statement, appendix, etc.).

Table 4.3. Accounting areas of the Comptabilité Universelle® (Universal Accounting)

| social | Environment | Economy | Governance | Societal | |||||

| Balance sheet (€) | Income statement (€) | Balance sheet (€) | Income statement (€) | Balance sheet (€) | Income statement (€) | Balance sheet (€) | Income statement (€) | Balance sheet (€) | Income statement (€) |

Comptabilité Universelle® (Universal Accounting) is therefore an accounting system dedicated to the monetarization of positive externalities. The said external effects attributed to the entity are associated with accounting expenses and income to the income statement of each impacted area. And depending on whether the impacts of these effects are considered positive or negative for the entity’s business, these expenses and income are recorded as a reduction/increase in assets or liabilities on the balance sheet of this area (Schoun et al. 2012, p. 101).

This aspect corresponds to a weak approach to sustainability. However, it is partially offset by other characteristics that make it possible to limit the loss of information incurred by the declinations of neoclassical logic.

First of all, this method prohibits the consolidation of monetarized values between the balance sheets of different domains, considering that, “an economic balance sheet governed by the principle of exhaustiveness cannot be consolidated with balance sheets by areas (environment, social, societal, governance), which cannot by essence be exhaustive” and that, “an economic balance sheet cannot be consolidated with balance sheets of other areas whose indicators do not have a homogeneous scope” (Schoun et al. 2012, p. 48). This positioning avoids the trap of the compensation principle that results from the concept of overall factor productivity (see section 1.1.2.2).

Then, it adapts the analysis periods to the temporalities of the phenomena described by these domains, so that analysis time is no longer trapped in the annuality of the entity’s accounts. The time of renewal of an ecosystem, the time of restructuring a network of actors, or the time of the political process can thus be approached as they are, and not in a permanent tension with the time of financial capital.

Table 4.4. Summary of the major differences in the principles governing traditional accounting and Comptabilité Universelle® (Universal Accounting) (Schoun et al. 2012, p. 60)

| Principles | Conventional accounting | Comptabilité Universelle® (Universal Accounting) | Observations |

| Completeness | Yes | No | The focus is on action |

| Valuation at historical cost | Yes (except IFRS: fair value principle) | No | Valuation at current cost with stakeholders |

| Comparability | Among all the companies | By professional branch | Good practices by professional sector |

| Annuality | Yes | No, not necessarily | Periods from 1 to 20 years or more |

| Perimeter | Fixed perimeter | Variable scope of consolidation | According to the indicators |

| Forecast balance sheet | Not mandatory | Yes | Quantified projection of future actions |

| Consolidation | Yes | No | The environmental, social, societal and governance reports cannot be consolidated with the economic report. |

Finally, the monetarization envisaged by Comptabilité Universelle® (Universal Accounting) is the result of a deliberation with stakeholders to establish local accounting valuation policies for the externalities generated.

Monetary representation is therefore anchored in a system of social representations; it is not an arbitrary and deterritorialized market monetization of these externalities.

These characteristics make Comptabilité Universelle® (Universal Accounting) an accounting system with the aim of “semi-strong” sustainability.

Let us return to the case study we are interested in. Structuring immaterial capital to coordinate communication between stakeholders with regard to several pairs [equipment – use] from different levels of analysis implies, in France, considering divergences in obligations between entities subject to the PCG and IAS-IFRS.

Concerning tangible fixed assets in the construction sector, Biojo et al. (2012) note rather structural differences (see Table 4.5).

Table 4.5. Differences between PCG obligations and IAS-IFRS regarding the accounting treatment of property, plant and equipment. (Source: Biojo et al. 2012)

| French PCG system | International IAS-IFRS system | |

| Valuation of tangible fixed assets | At historical cost30, but can now be measured at fair value31 | At their fair value32 |

| Recording of major maintenance and rehabilitation (MMR) expenditures | Either recorded as expenses and provisions, or recorded as assets | Mandatory capitalization, with possible provisioning, but without the possibility of a related tax deduction |

| Recording depreciation | Fixed assets as a whole | Approach by “component” |

| Depreciation over time | Standards according to the type of asset considered | Based on the actual expected useful life of the component – duration defined by the entity itself |

CARE® allows a depreciation system to be integrated directly into PCG financial accounting, allowing maintaining costs of an extended capital (human and natural, not only financial) to be reported as liabilities. By distinguishing three depreciation lines, CARE® opens the possibility of recording depreciation component-by-component.

The costs needed to renovate a building, recorded as liabilities, give rise to the accounting formalization of natural, human and economic assets (e.g. reduction of GHG emissions, indoor air quality and reduction of energy costs).

In addition, basing the method on an “internal–external” perspective makes it possible to design these costs as an investment in the sustainability of multifunctional means of production that the entity does not own. This approach has the effect of strengthening the entity’s control over its assets. CARE® moves the lines between material and immaterial assets by encouraging both a reconciliation of the points of view of the manager and the accountant, and a comparison of the interests of the entity and those of the stakeholders in the territory.

As for Comptabilité Universelle® (Universal Accounting), the use of this method by an entity subject to or wishing to apply IFRS would give that entity a better understanding of the concept of “fair value”. To consider with stakeholders an approach aimed at classifying externalities – positive and negative – by area of territorial performance issue of its activity, then to monetize these externalities, would lead the entity to place directly in its general accounts the monetarized value of a service that has not been contracted for.

As a result of this operation, in the case of building rehabilitation, monetarization of avoided GHG emissions would provide both the value of a product and an asset to the environmental operating account. If training of occupants in the uses of the building is financed, then the cost of this training that is reported as an expense in the operating account of the social domain also gives direct value to an intangible asset in the balance sheet of the same domain.

In Chapter 6, we will propose an articulation of CARE® that corresponds in every respect to our approach of sustainable territorial anchoring of valorization, with an adaptation of the Comptabilité Universelle® demonetized balance sheets. The assembled accounting modules will thus make it possible to consider a Communication between the entities subject to IFRS and the other entities of the territorial functional ecosystem.

This territorial functional ecosystem includes, of course, the entities involved in PSS built around the couples [equipment – use] in which we are interested to anchor the functional economy in accounting. It also includes public administrations, particularly those in charge of national accounts.

4.2.2.2. For a national accounting of political economy

The European System of Accounts ESA 2010 (Eurostat 2013), which came into force in France in September 2014, establishes guidelines for the national accounts of EU Member States. It currently guides the construction of the future French national accounts, which should be used by 2025.

Based on the United Nations System of National Accounts (SNA-2008) – itself carried out under the joint responsibility of Eurostat (European Commission), the IMF, the OECD, the World Bank and the United Nations – the main focus of the ESA 2010 is to propose, in addition to the aggregates of the central framework (place of monetary representation) a series of satellite accounts (place of representation by non-monetary indicators).

The central framework of the ESA 2010 describes the economy with strictly monetary information. This framework consists of the integrated economic accounts (institutional sector accounts), which provide a synthetic overview of all economic flows and stocks (Eurostat 2013, point 22.03); the input–output framework that provides a synthetic overview of resources and uses of goods and services at current prices and volumes; tables linking the branches of activity of the input–output framework and the institutional sector accounts (ibid.); tables on expenditure by government, household and corporate function; tables on population and employment (ibid.).

Satellite accounts are used to prepare or modify the tables and accounts of the central framework. The objective is to “meet specific data needs by providing more detail, by rearranging concepts from the central framework or by providing supplementary information, such as non-monetary flows and stocks” (Eurostat 2013, point 22.04). The non-monetary data in question, relating to physical or intangible objects, may cover any field deemed useful to illustrate the links between the national economy and various political and analytical issues (Eurostat 2013, point 22.54). As for the reorganization of concepts, it makes it possible to induce the use of additional concepts, different basic concepts, as well as the use of models or the inclusion of experimental results (Eurostat 2013, point 22.06).

Let us now detail how the ESA 2010 system works. The aggregates of the central framework are synthetic indicators that provide a monetary reading of the value representation process, for a particular set of entities, from the local to the national level (precisely according to the level of aggregation). Introducing satellite accounts, and through them a non-monetary analysis, is a way of placing the reading of these monetary aggregates within a broader framework of representation, favorable to the description of multifunctional productions in a territory of activity. The ESA 2010 is therefore, beyond the accounting system, a tool of political economy.

Two types of satellite accounts – “functional” or “specialized” – can be constructed:

- – functional satellite accounts describe the main economic functions considered by national accounts (environment, health, R&D, productivity and growth, etc.);

- – specialized satellite accounts target a branch of activity, a product, or a set of industries and products, or even a subsector or set of subsectors.

The ESA 2010 thus establishes the possibility of targeting a territory of activity. Cross-referencing these two types of accounts reveals an analytical framework that is extremely well suited to cross-sectoral analysis, and therefore to the description of multifunctional productions.

Including certain specialized accounts in the integrated economic accounts of the central framework, makes it possible to “see the respective shares of the key sector and other sectors in transactions and account balances”, in particular by “showing in additional tables the ‘from-whom-to-whom’ relationship between the key sector and other sectors, including the rest of the world” (Eurostat 2013, point 22.41).

These analytical cross-references are made possible by an essential feature of functional satellite accounts; the latter are not structured according to an institutional approach.

This characteristic allows the analyst to consider productions in plural and complementary ways:

- – in a “function approach”: analysis of national (and regional and local) expenditure for a given function (Eurostat 2013, point 22.23), which makes it possible, in particular, to initiate a “vertical” dialogue between actors;

- – in a “product approach”: analysis of the activities and products involved in each function considered (Eurostat 2013, point 22.22), in an intersectoral approach and therefore compatible with the territorial economy.

In addition to this, we believe that there is a “service approach”33, which involves not only identifying the products to be isolated from the central framework, but also the activities that record capital formation, transfers corresponding to the field in question (Eurostat 2013, point 22.24), in order to compare them with non-monetary data.

The combination of these approaches highlights details that are not visible in the central aggregated framework. It requires the development of functional aggregates, non-monetary indicators, ratios between monetary and non-monetary data, additional data and concepts, and different basic concepts.

The examples presented in Table 4.6 refer to well-established satellite accounts that are the subject of international recommendations or are already part of an international transmission program34.

Other satellite accounts, developed in different countries, illustrate the scope of possible application: cultural and creative sector accounts; education accounts; energy accounts; fisheries and forestry accounts; information and communication technology (ICT) accounts; redistribution by public expenditure accounts; residential building accounts; safety-related accounts; sports-related accounts; water-related accounts, etc. (Eurostat 2013, point 22.7).

This diversity of satellite accounts illustrates the limitations of the central framework. “For example, environmental accounts expand the central framework to account for environmental externalities, and household production accounts expand the production boundary to include unpaid household services. In this way, they demonstrate that the central framework’s concepts of product, income and consumption are not complete measures of welfare.” (Eurostat 2013, point 22.9)

Table 4.6. General presentation of the ESA 2010 satellite accounts and their main features. Adapted from Eurostat (2013, Table 22.1)

| Eight characteristics of satellite accounts | |||||||||

| Special sector accounts | |||||||||

| Functional accounts | Link to industries or products | Link to institutional sectors | Inclusion of non-monetary data | Extra detail | Supplementary concepts | Different basic concepts | Experimental results and more use of modeling | Part of EU transmission program | |

| Examples of satellite accounts described by the ESA 2010 | |||||||||

| Agricultural | x | x | x | x | |||||

| Environmental | x | x | x | x | x | x | x | x | |

| Health | x | x | x | x | x | x | |||

| Household production | x | x | x | x | x | ||||

| Employment and SAM | x | x | x | x | |||||

| Productivity and growth | x | x | x | x | x | x | x | ||

| R&D | x | x | x | x | x | x | |||

| Social protection | x | x | x | x | |||||

| Tourism | x | x | x | x | x | ||||

| Balance of payments | x | x | x | ||||||

| Government finances | x | x | x | x | |||||

| Monetary and financial statistics and financial flow of funds | x | x | x | x | |||||

| Supplementary pension table | x | x | x | x | x | x | |||

| Other examples of satellite accounts with international recommendations or as part of a comparison program | |||||||||

| Corporate activity | x | x | |||||||

| Informal sector | x | x | |||||||

| Non-profit institution | x | x | x | ||||||

| Public sector | x | x | |||||||

| Tax revenue tables | x | x | x | ||||||

4.3. Conclusion

The comparison of the various functional satellite accounts articulated in the central framework of the ESA 2010 is based on a will to distinguish the dimensions of analysis, of the effects of what we call multifunctional production. A similar motivation prompted the designers of the Comptabilité Universelle® method to propose an analytical accounting system for internalizing externalities, according to five balance sheet and income statement areas. It is still a strong motivation, but fed by another level of demand (strong sustainability, rejection of the internalization of externalities), which led the designers of CARE® accounting to distinguish three lines of depreciation of human, natural and financial capital.

One of the most spectacular pitfalls of the neoclassical economy is to consider that data produced in relation to a given valuation time and space retains the same informative power in another valuation time and space. However, despite the relative similarities in the intentions of the accounts described, they do not observe the same spaces, nor do they perceive the same temporalities. They therefore do not value the same productive phenomena and do not remove the pitfall of the relativity of space and time in accounting representation.