Earlier in the book, I described the anatomy of cash transactions. The idea of describing it this way came to me when I was in graduate school trying to figure out what was wrong with the accounting treatment of costs as it related to cash. It started with a particular analysis approach well known to engineers.

I’m a degreed engineer, so the approach I used wasn’t just tattooed into my thought process, it was beaten in so hard, it has become a part of my DNA. The basic idea is this. If we’re lost or stuck, we go back to first principles; foundational ideas we believe to be true. In this case, as a mechanical engineer, I thought about thermodynamics. Thermodynamics is one of those courses that you either understood, or you’re beyond lost. I’ll admit, when I first took thermo as an undergraduate, I had no clue what some of the terms meant when thinking of them in the physical versus theoretical/mathematical world. There is enthalpy, entropy, adiabatic, and many other complicated terms that, in some cases, described relatively simple ideas, but came across as being extremely complicated. But the one thing I did understand completely was the notion of a control volume. A control volume is a box you put around what you want to analyze or study and watch what comes into and leaves the box over a given period of time. It doesn’t get much easier to understand than that!

My objective, in this case, was to analyze a company making money, so I used my extensive knowledge of thermodynamics to draw a box around a company. What next? I needed a way to describe what was happening from a cash perspective. Thermodynamics could do this, but the explanations seemed too complex; remember adiabatic, and isothermal. I then turned to system dynamics.

Bingo. System dynamics is a concept created at MIT by Jay Forrester. The idea was to find a way to model systems using engineering tools and concepts. According to Forrester, a system is “a grouping of parts that operate together for a common purpose.”1 The concept of system dynamics has been applied successfully in many areas, such as modeling business dynamics and cycles, populations, and even socioeconomic systems.

One key concept of system dynamics modeling is the level. The level is what we call a state variable. State variables describe the state of a system at any given time. If you studied animals in the wild, for instance, the population of a species or the amount of food sources could be considered state variables and would tell you something about the state of the population system. It would tell you how many of a given species there are, or how much food is available to them in the system you’re studying and ultimately describe or project a system’s dynamics or how it may change over time. For example, an abundance of food as a state variable may lead to increases in another state variable, the population we are interested in studying. An abundance of predators may lead to a reduced population, which may cause the food of the population we are studying to become abundant.

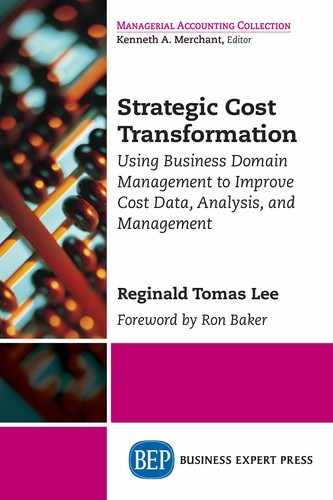

Cash, in this case, seemed to be a good candidate to be a level for a company, and so it became one in the analysis. If you draw a box around a company and watch the cash that comes in and leaves, you can garner a significant amount of information about cash levels, flow, and whether you’re making or losing money (Exhibit 9.1).

With the box around the company, certain analyses are simplified. For instance, you can determine how much cash you have at any time by considering how much you started with and what came in and left the box during the analysis period as stated in Equation 2.1. For instance, your company starts the year with $1M, receives $1M throughout the year and spends $1.2M. At the end of the year, it has $800K. I start my day with $20, I make $2, and give my wife $22. At the end of the day, I’m broke again. This is straight from Equation 2.1.

![]()

Exhibit 9.1 Putting a box around the company and measuring cashIN and cashOUT provides, arguably, the most effective way to model cash over a period. This process also helps focus you on what does, and does not affect cash in ways cost accounting can not

Critical to the analysis is to start with the box. If you read my first book, Explicit Cost Dynamics, the box around the company was the cost-revenue or CR Border. It has now been renamed the CashIN CashOUT or CICO Border. You then measure what comes in and what leaves during the analysis period. Understanding the flow in and out isn’t enough when it comes to managing cash, however. One can argue cash flow statements can try to provide this info. We understand from this analysis and cash flow statements that cash flows but not why it flows. To understand this, we go back to the Business Operations Framework. To understand why and when money comes in and the rate or extent to which it does, we look to what we sold and our payment terms. To understand the flow out of the company and the extent to which it does, you look at what was bought and paid for; capacity, transactions, and TF&R.

This falls right in line with the activities of the Business Operations Framework. When you combine the Business Operations Framework with the Cash Flow Dynamics Framework, you end up with the OC Domain; the 3-D ball. Everything there is to know about the company and its performance, both operationally and financially exists, or is derived from OC Domain data. You know what was sold and what revenue was received versus recognized. You know what was brought in and spent. From this, you know if you’re making money. You know how much capacity you bought, how much was consumed, and how this turned into output. You have practically everything you want to know. However, that one person will raise their hand and ask, “Yes, but what did the output cost?”

1 Forrester, J.W. 1990. Principles of Systems, 1–1, Portland, OR: Productivity Press.