The first BDM domain I’ll focus on is the OC Domain. The OC Domain, the means, is where all business and cash transactions and activities occur, and it is also where I think most business analyses should occur. This is where Toyota focused. This suggestion may be putting the cart ahead of the horse a bit as it relates to the context of this book, but by addressing it now, I hope to help you create a connection between what happens in the OC Domain and what typical analyses often focus on. This should create context for why we should focus more on the OC Domain and the means, when we delve more deeply into business analyses.

The OC Domain is composed of two parts; the Cash Dynamics Framework and the Business Operations Framework. The Cash Dynamics Framework describes how cash flows into and out of a company, and how cash levels change. The Business Operations Framework models a company’s infrastructure and business operations, activities, and processes, and provides context for the Cash Dynamics Framework. Together, they create a holistic perspective of operations and cash performance. Let’s discuss both.

The Cash Dynamics Framework specifically focuses on modeling a company’s cash transactions. If you put a box around your company as described in Chapter 3 and measure the cash coming in and the cash going out during a period, you will be able to model the company’s cash dynamics. At any time, if you have a beginning cash amount, and you consider both cashIN and cashOUT over an arbitrarily selected period, you will know how much money you will have at the end of the period and how it has changed over the analysis period.

CashIN is money the company receives and can be placed into its coffers. This money comes primarily from sales, but there can be other sources such as money received from loans. CashOUT occurs when money is being paid and, therefore, leaves the company. This usually happens for one of three reasons; purchased capacity, services, and obligations such as taxes, fees, and royalties (TF&R).

When you pick an analysis period, the sole determinants of whether cash increases or decreases is the difference between cashIN and cashOUT during the period. When the difference is positive, the level of cash increases. When negative, it decreases. There are no other data that are more material, accurate, or precise measures of whether you are making or losing money than this difference. This model also sets the stage for modeling organizational improvements. When looking to improve cash performance, you must change cashIN, cashOUT, or the relative difference between the two. This will be discussed in some detail in Chapter 17.

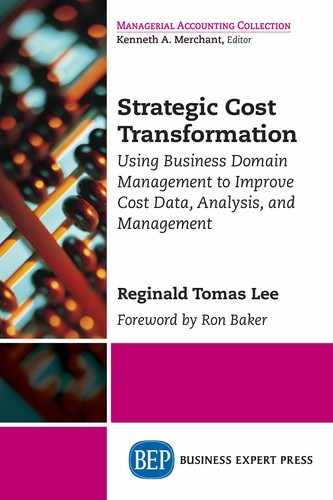

The Business Operations Framework describes how business occurs. There are four components of the Business Operations Framework; what we buy, how we consume it, what we create, and what we sell (Exhibit 5.1). Each of these is discussed in more detail in Chapter 7.

Together, these four areas create the foundation for the Business Operations Framework. Any company and any business activity can be modeled in the context of this framework, and a significant amount of information can be gleaned from it. You know how much capacity you bought and have, and how much of it was used. From this, you can get efficiency information. You know what was created and how effectively capacity was used to do so, which allows you to understand output and determine whether the capacity was used appropriately. You know how much work your infrastructure is able to create and where to focus to improve. In other words, this provides the basis for managing the means.

Exhibit 5.1 The basic activities of the OC Domain are buying (mostly capacity), using capacity to create output, and when it’s an option, selling the output to generate revenue

When combined, the cash dynamics and Business Operations Frameworks create the OC Domain, which is the basis for all business activities and financial transactions. Center to all this is capacity and capacity management. Being the focal point of spending and work, managing it is the key to any company looking to manage costs and make money.