I’m guessing you probably didn’t get into music because you wanted to hear someone talk about being sensible and saving for your pension. However, I’m also guessing that if you’ve read this far in the book, you are serious about your career, and you’re very serious about making a living from your music.

Unless you die young, there will come a time when your earnings from music will be reduced. This happens for all artists: As they mature, their fan base contracts.

Fan bases contract for a number of reasons:

Musical tastes change, and as the act becomes less trendy, fans lose interest in music and/or the act, not to mention having other priorities in their lives.

The act may tour less and undertake less promotion. This is not unreasonable: Most people can spend only a number of years living the nomadic lifestyle of a musician on the road before they burn out. In addition, many musicians also broaden their interests, perhaps pursuing other projects that have arisen as a result of their success.

A declining fan base can, but doesn’t have to, lead to a decline in income.

Although a fan base may have declined, the income expectation can become more certain and sustainable (provided the fan base is nurtured). It is not unreasonable to expect that if you have kept a fan for 20 years, that fan is not going to desert you in the short-term, unless you upset him or her, and you may also find that with age, each fan becomes more profitable.

Also, if your fan base is maturing, then your fans’ tastes are likely to change. With a younger fan base, particularly a teenage fan base, you will be able to sell a much greater quantity of merchandise. For the more mature fan base, you are likely to sell less, but the merchandise you sell may be of a higher quality, allowing you to charge higher prices and make better profits.

The financial strategy underlying this book is to develop a long-term, sustainable career that will continue to generate income over as long a period as possible. Provided you can sustain your income over a sufficiently long period, you will avoid the cat-food years—those declining years when your career has gone, the money you had has gone, and you are left so impoverished that all you can afford to eat is cat food.

There are many ways you can achieve this longevity. One strategy would be to make your income from the same sources that you do in the earlier part of your career, such as downloads/CDs, merchandising, and live performances. You will still be able to generate income from these sources, but to a lesser extent as you mature.

As you hit the middle stage of your career, you will probably generate less money from direct sources (downloads and live performances), but you should be able to increase the income you make from indirect sources, such as television and film licensing. Then, as you approach retirement, you can look at possibly selling off the rights to your future income in exchange for a lump-sum payment.

Of course, this is only one option. However, it does show how you can have a steady income over your whole career (or at least over a longer period than you can under a conventional music career).

So will you avoid the cat-food years? Let’s take a look at some income streams.

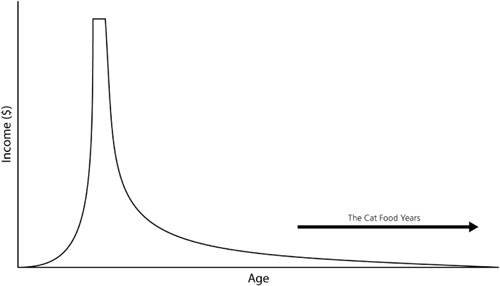

Take a look at Figure 7.1. This shows the earnings pattern for many successful, but now forgotten, artists.

Figure 7.1. The income pattern of an archetypal successful artist. After a few years of struggle, the artist hits the big time, and after the peak, fades into obscurity around the time of his or her 30th birthday.

This graph could show the income for a guitarist in a successful band. Let me explain how his career could play out.

When the band started off, it didn’t generate very much income. This is normal for a band when they are paying their dues. However, this band became successful, signed a deal, and started to sell a lot of records. On the back of this success, the band toured and generated some income (primarily from the merchandising). At this point, the members of the band were starting to see quite a healthy income for the first time and were receiving incomes in the high six figures or into seven figures. (They were very successful.)

After a few years of wild parties and a good bit of money, the band split due to musical differences. The drummer joined a cover band, and the bassist decided to become a professional surfer and moved to Australia. The singer joined another band, and that left the guitarist.

The guitarist still had some royalties coming through (mostly from overseas sources) and started to put together a solo project. The solo project was an artistic success but made a poor financial return, and on his 30th birthday, the label dropped the guitarist.

With no other skills and no inclination to do anything else, the guitarist survived on the last few royalty payments that trickled in over the next few years until the income from his musical career finally dwindled.

We have now reached the cat-food years.

Now think about the income stream you may be able to generate if you take control of your career following some of the ideas set out in this book. Have a look at Figure 7.2. Here, I have superimposed an income stream that could be generated if you follow your own course over the income stream that our unfortunate guitarist received (which was originally shown in Figure 7.1).

Figure 7.2. By taking advantage of the new opportunities that are available, more musicians can develop a long-term career and live on more modest earnings over a longer period. You should also remember that while very few musicians actually earn mega-bucks (and then end up spending huge amounts of this money very quickly), the more modest level of earnings is achievable for many more musicians. You should also bear in mind that I am calling the earnings “modest” because they are lower than the earnings shown in Figure 7.1, but they are still good earnings and would support a good lifestyle. The scale used on the graph only makes these earnings look lower.

There are a few things to notice about this alternative income stream:

First, income is generated more quickly by this approach because you begin earning immediately. You don’t wait for a record or management deal before you start generating income.

The income stream builds more slowly. Because you are relying on (assisted) organic growth, the increase in your income will be more controlled. However, see the next bullet.

The income stream remains at its peak for longer. (Indeed, the peak is more of a plateau.) With a more solid fan base, you will be able to sustain momentum over a longer period.

The income stream does not decline to zero—instead, it remains at a reasonable level until around the time that you are ready to retire (and even after that date, it may still provide an income).

What may not be obvious is that under this latter approach, the performer makes more income than under the first approach, because the income is received at a reasonable level for the whole of the musician’s career.

Either you are independently wealthy, or you will need money in order to live. Most people have a range of expenses that include food, keeping a roof over their head (including paying for water, electricity, and so on), gear for making music, and taxes (local, national, and including any social contributions). After that, most spending is on what are, in effect, luxury items.

How much money do you need? It’s an interesting question, and one I propose not to answer. Instead, let me flip the issue over and give you two alternative approaches to dealing with your income.

First, live within your means. You know how much money you have earned: Do not spend more than that. This may mean you will need to cut every possible expense. If you own a house, sell it and move somewhere cheaper; if you’re renting, quit and move back with your parents; if you’re in an expensive location, then move somewhere cheaper. Do everything you can do to stay afloat financially.

Second, if the amount you want to spend exceeds the amount you are earning, then you are not earning enough. You (and you alone) directly control your earnings so, instead of going into debt, go out and earn more money. If that’s too difficult, then you need to live within your means (so go back and read bullet point one again).

As a musician, your pay packet is not determined by the amount you earn. Rather, it is determined by how much is left after all of the deductions. We’ve looked at many other deductions throughout the rest of this book. I now want to look at two very specific deductions that are pertinent to you alone: taxes and pension contributions.

In most jurisdictions, you will be taxed on your earnings. Unfortunately, this is the nature of society, and there is little you can do about it (except find a smart accountant to show you the loopholes, move to a low-tax jurisdiction, or both).

Each country has its own tax regime that will affect its own citizens and foreign citizens working in the country (such as touring musicians) in different ways. Most countries have tax treaties with other countries (often called double tax treaties), whereby foreign nationals can avoid tax on earnings in the foreign country, provided the earnings are taxed in their own country.

Tax is a hideously complicated and dreadfully dull subject, so I don’t want to go into the minutiae of double tax treaties or any of the other tax matters. However, I do want to give an indication of how tax can do really bad things to your income.

Tax systems around the world work in many different ways, and tax rates can vary greatly. However, there are a few principles that are fairly global:

No one wants to pay tax, but people do. If people don’t pay tax, then the tax authorities will pursue them and crush them mercilessly.

Tax for self-employed people (that is, people who are not employed by someone else—as a musician controlling your own career, you will probably be self-employed) is calculated after the deduction of expenses. So, for instance, if your tour earns $1 million, but you have expenses of $900,000, then you will usually be taxed only on $100,000.

In addition to taxes, there are often social charges at a much more modest level. These are often payable irrespective of earnings or based on a stricter calculation of earnings that ignores some expenses.

These are general principles: You should take detailed tax advice in your own jurisdiction (and also consider taking tax advice in any other jurisdiction where you earn money), because each locality will have its own tax laws. For instance, in the U.S., self-employed people (such as musicians) pay an additional 15 percent self-employment tax above regular federal and state taxes. If you’re not expecting this tax hit, it can be quite painful.

As I said, I want to give an example of how tax can eat up your earnings. I’m going to illustrate the loss to your pocket using the UK taxation system, looking at the situation as it applies to self-employed individuals. For this example, I will consider someone who is earning quite a reasonable amount of money: £50,000 (or roughly $85,000) after expenses. This figure may be more than many musicians earn (indeed, it is roughly twice the average earnings throughout the UK); however, I am using it because it will show how the higher tax bands can have a greater effect on earnings (although it does exclude the current UK top rate of tax, 50 percent, which is applicable for taxable earnings over £150,000). I should point out that all figures quoted here are for the 2011/2012 tax year.

In the UK, social contributions are called National Insurance Contributions (often known as NICs). For self-employed people, there are two components—a fixed weekly amount and a percentage based on certain earnings:

The fixed weekly amount is £2.50 per week (or £130 per year).

The percentage-based amount is 9 percent of earnings between £7,225 per year and £42,475 per year. So in our example, the individual would pay the maximum amount of £3,172.50 (that is, 9 percent of £35,250, which is the amount of earnings between £7,225 and £42,475).

So in this example, National Insurance Contributions of £3,172.50 are due on earnings of £50,000. National Insurance Contributions cannot be set against tax.

Under the tax system, a basic allowance of £7,475 is given. This means you can earn £7,475 before any tax is paid. So in our example, only £42,525 (in other words, £50,000 – £7,475) is taxable. There are then two tax bands (the starting rate of 10 percent does not apply here):

The first £35,000 of taxable earnings is taxed at the rate of 20 percent.

The next £7,525 (the taxable earnings after the £7,475 basic allowance and the £35,000 basic rate band) is then taxed at 40 percent.

Some figures should help to illustrate. Look at Table 7.1.

So in this example, the tax amounts to £10,010 (or 20 percent of earnings).

The total deduction from earnings is £13,182.50 (£10,010 tax plus £3172.50 National Insurance Contributions), or 26 percent of earnings.

After deduction of tax and National Insurance Contributions, the take-home pay is £36,181 (or £3,068 per month).

To illustrate the effect of tax, take a look at Figure 7.3, which shows each component of the pay packet.

Figure 7.3. The effect of income tax and National Insurance Contributions on earnings. Under current UK legislation, as earnings increase, the tax burden will increase, until 50 percent of income is taxed.

As I mentioned at the start of this section, this example shows the effect of UK taxes. This book is about how to develop a career in music; because it is not a book about tax, I have not illustrated the tax position for every jurisdiction in which you may work. Non-UK tax laws would obviously paint a different scenario than our UK example, but the overall outcome is the same in either country: You must pay taxes, and they will eat up a significant portion of your income.

I now want to talk about one expense that you may think is irrelevant: pensions, or as you might want to think of them, retirement funds.

Conventionally, the purpose of a pension (and a retirement fund) is to provide income when you stop working. However, under the model I am advocating in this book, you will hopefully be generating income over a much longer period. Ideally, your music will still be generating income after you retire. Don’t get too hung up on any difference between pensions and retirement funds. They are essentially the same thing—a source of income when you retire.

However, instead of thinking of a pension as being just for when you retire, consider it as another income stream that will come online as your earnings decrease. The idea should be that your combined earnings and pension will maintain your income at a certain level when you decide to make the transition into retirement (see Figure 7.4). Then if (or when) the earnings from music cease, you will have another income source.

Figure 7.4. You can use the income from a pension to ease the financial transition as your earnings from music decline.

There is one problem with pensions: They cost a lot. Let me first explain how they work. Once I’ve done that, I’ll look at some of the practical steps you can take.

Pensions are a gamble: nothing more, nothing less. What makes them interesting is that they are a bet on your life!

Perhaps the most secure way to provide a pension for yourself is to buy an annuity. An annuity is another way of saying an income for life. Annuities are sold by financial institutions, such as insurance companies. The cost of an annuity is determined by many factors, but it is essentially a guess by the financial institution about how long you will live (based on statistics about the population as a whole).

If you live longer than was assumed, then you make a profit. If you don’t live longer, then you won’t have made a profit. You will only be able to know how long you lived after you have died, so any profit or loss will then be immaterial. However, the key factor about annuities is that they can provide you with security—they protect you against the risk of living longer than you expected.

The risk of living longer than you expected is a serious problem. Suppose your income ends when you are 60, and at that point you have savings of $500,000. You might expect to live for another 20 years. Ignoring the effects of interest and inflation, that would mean you could spend $25,000 a year (that is, $500,000 ÷ 20) or roughly $2,000 per month for the rest of your life. If you then die at the age of 80, your money would be gone.

But what happens if you don’t die when you expect to? If you knew you were going to live to be 90, then you could spend $17,000 a year, or $1,390 per month. If you knew you were going to live to be 100, you could spend $12,500 a year, or $1,000 per month.

Unfortunately, we don’t know when we are going to die, so there is a tendency to spend less and hold back some capital. However, this can never counter the effect of someone living to an unexpected old age. Take the previous example: What would happen if the person lived to be 110? Although not many people live to be that age, can you be sure that with all of the advances in medicine and technology, you will not live to be that old? Or older?

Because of the uncertainty, annuities have a great use. However, because of the uncertainty, annuities can look very expensive (although to be fair to insurance companies, they take a very small profit on this element of their business).

As a side note, you might think that all this stuff about annuities is dull and you can just live on the interest of your capital. Apart from tax, possibly living to be 120 years old, and fluctuations in interest rates (which could lead to wide swings in your level of income), another factor that makes this a risky strategy is inflation, which will erode the value of your capital. You would therefore need to reinvest some of your interest to ensure that the interest level retains its buying power, whereas an annuity can include inflation protection.

The cost of an annuity varies according to a number of factors, including:

Geographic location. Annuities are calculated in different manners in different jurisdictions.

Age. If you are younger, an annuity may be expected to be paid for a longer period and hence will be more expensive.

Pension increases. You can buy annuities that provide the same amount for every year. However, these annuities mean that the pensioner becomes poorer over time because prices will rise due to inflation. To counter this, you can buy an annuity that increases. The increases can be linked to inflation or can be a fixed percentage. The cost of an annuity will increase if you want pension increases (because the amount the annuity provider will pay out will increase).

Dependants. Many people want to also provide for their spouse/significant other in the event of their death. It is common for an annuity to provide a pension for a spouse/significant other on the death of the original annuitant. Often the dependant’s pension will be of a lower level, perhaps two-thirds or one-half of the original pension. A dependant’s pension will increase the cost of an annuity.

Prevailing market conditions. The financial institution will invest the money you pay to buy your annuity. If the company thinks it can do better with its investments, then it will charge you less for your annuity. However, if the company thinks the financial markets do not offer much scope for profit, then it will charge you more.

I said annuities are expensive. Let me give you a practical example. These are indicative market figures (in the UK) taken in mid-2011.

For this example, I have taken the following scenario:

An individual retiring at age 60...

...with a spouse who is the same age...

...with the pension increasing in line with UK price inflation, and...

...on the death of the annuitant, the spouse will receive a pension for the rest of his/ her life of 50 percent of the pension that was being paid at the date of death.

Based on these assumptions, a pension will cost more than 34 times the yearly amount that is to be provided. So, if you wanted to provide a pension of £15,000 (roughly $25,000) that would cost £512,300 (more than $850,000).

Once you have pondered the eye-watering expense of pensions, let’s move on and look at some of the practical steps you can take to ensure that you secure a modest income in retirement.

If you want to provide a reasonable pension for yourself (and perhaps your loved ones) when you retire, then either you can hope you have a very large chunk of money when you retire (which is quite unlikely) or you can start making financial provisions (in other words, saving) now.

Several factors will affect the amount of money that is available to you when you want to buy an annuity:

The amount you invest

When you invest

The returns generated by your investments

Clearly, the amount you invest will have a direct effect on the amount of money available when you come to retire.

The timing of your investment also has a significant effect on your income. The earlier you invest, the longer that investment will have to grow. If you invest $10 on your 20th birthday and $10 on your 40th birthday, by the time you get to your 60th birthday, ignoring any financial disasters, the $10 you invested on your 20th birthday will be worth much more than the $10 you invested on your 40th birthday.

The statement in the last paragraph assumes that your investments always go up. As we know, depending on the nature of the investment, returns can go up and down. Broadly speaking, if you take fewer risks, then you would expect lesser returns, but those returns are more likely to be certain. However, if you take more risks, then you would expect greater returns, but there is also a much greater risk of your investment performing poorly.

The nature of your investments will vary depending on your attitude to risk and the returns you are looking for. One thing you should always remember is that any investment returns need to be greater than the rate of inflation to have any real effect. For instance, if inflation stands at 3 percent and your investment returns 2 percent, then you will actually make a loss of 1 percent. However, if the investment returns 5 percent, then you would have achieved a real return of 2 percent.

This is a book about your music career, not about financial investment. However, your investments are important because they have such a direct impact on your living standards, so you should always take proper financial advice before making any investment decision.

Pensions are eye-wateringly expensive, but there is a small bit of silver in this pension cloud. In most jurisdictions, pension contributions can be set against tax.

You should, of course, take advice in your jurisdiction to confirm whether these contributions are allowable for tax purposes, and if so, what conditions apply.

I’ve thrown a lot of figures at you. I make no apologies for this: The factors affecting your take-home pay and your financial well-being are complicated.

Whatever your personal situation, you need to understand what will affect your earnings and how much money you need to be able to live your life at a reasonable standard. You then need to make some serious decisions about how you make money from music. Those decisions may be uncomfortable because two of the factors you will have to consider are:

Does the music I am producing have sufficient commercial potential? Remember my example earlier about poets—a highly successful book of poetry may sell around 800 copies in a year. If the poet does really well and makes $3 for each book of poetry sold, that still only works out to $2,400 income, which really isn’t enough to live on. Are you just being a musical poet, condemned to live your existence in poverty?

Am I/are we really good enough? Or is the reason for your lack of income simply that you are rubbish?

If your music has sufficient commercial appeal and you’re good, then you stand a fair chance of making a living, provided you cultivate and nurture your fan base.