28

Sometimes “Cash Flow” Doesn’t Flow

IF YOU ARE INTIMIDATED by or think there are enough headaches surrounding the financial aspects of running a business, you are in for a lot of fun (and by fun, I mean more headaches). In the game of business, financial statements are the key tool to help you keep score. If you can’t keep score, you shouldn’t be playing the game—especially not professionally!

A lot of entrepreneurs are not proficient in any aspect of financial accounting. They particularly do not understand how to manage the cash flow of their businesses. Cash flow illustrates the actual cash impact of running your business on a day-to-day basis, rather than purely the profits and losses. Cash flow has a significant impact on whether your business is healthy and if you as the owner can take home any money—which isn’t always the case, even when your business is showing a profit.

FINANCIAL LINGO

CASH FLOW—Where the cash in your business is coming from and going to (and sometimes where it’s just sitting or waiting to come).

INCOME STATEMENT—Also known as a P&L (profit and loss statement) or a statement of earnings, this shows the company’s expenses and revenues for a given period (such as week, month, quarter, or year) to determine if you have made any income or profits (this is “on paper” earnings, which is different than the change in cash in your business). The income statement includes sales for that period, as well as cost of goods sold, operating expenses (such as administrative costs), depreciation on assets, interest on any loans the business has or interest earned on investments, and sometimes income taxes.

STATEMENT OF CASH FLOWS—The statement of cash flows shows your sources of new cash coming into your business during a given period, as well as your uses of cash during that same period, ultimately demonstrating if your overall cash position is increasing or decreasing. It focuses on the actual change in cash, rather than income statement profits. It is generally organized by cash flow from operating activities, cash flow from investing activities, and cash flow from financing activities. Even if a business is profitable, negative cash flow can cause a business to fail.

WORKING CAPITAL—Your business’s current assets less its current liabilities.

When many entrepreneurs write their business plans, as well as when they do their accounting, they focus on the income statement, which they may or may not really understand. The income statement shows for a given period of time (a month, a year, etc.) the value of the goods or services your business sold (your revenue or sales), the direct cost of those sales (the cost of goods), and then all of the sales, marketing, administrative, and other expenses you incurred while running the business during that period of time. Many entrepreneurs tend to look at their income statement profit literally as what they earned (or will earn) during the period, and they focus on that number as a good snapshot of the business and its health. However, the profit is different from the cash flow of the business, because the profit doesn’t fully capture the money you need to spend on major purchases or take into account the timing of when you get paid or when you pay your suppliers and vendors.

Cash flow from a business includes the operating profits of the business (adding back in any non-cash depreciation) and subtracts any increases in what is called working capital (or if you are lucky enough to have a decrease, adds that decrease back), and also subtracts any increases in investing activities (such as purchases of property, plant, or equipment) in that period. This is the full information required for you to know how much money the business needs for that time period (which, if you raise money during that same period, will be referred to as a financing activity).

Your head is probably starting to spin. Just wait, it gets more fun.

Working Capital Starts with “Work” for a Reason

Working capital deals with the balance sheet of a business. A very cursory and basic explanation of working capital is that it is your business’s current assets less its current liabilities. This includes assets that are considered usable in the short term, like accounts receivable (money owed to you for sales you make), inventory, and pre-paid expenses, less liabilities that are due in the short term, like accounts payable (money you owe to others).

Your eyes may be glazing over now because this is not easy stuff. Working capital definitely takes a lot of work to understand and to manage. Let me try to explain this further. In order for you to have goods to sell, it requires you to outlay cash. You may need to have the goods manufactured or buy supplies for you to make the goods yourself, and you may have one or several vendors or suppliers that supply you with the finished goods or material components. You, as a business owner, want to get the best payment terms (that means take as long as possible to pay your vendors and suppliers) to help you manage your cash flow. If you could be billed by your vendor thirty, sixty, or even ninety days after you received the goods or supplies, this would be fantastic for you. If your vendors agreed to extend payment terms to you, you wouldn’t have to “come out of pocket” for the goods so far in advance of being able to sell them. However, getting favorable payment terms is particularly difficult for new businesses, as you have little clout and credibility—two of the Cs you left behind with your last job.

With your business being new, your vendors will be worried about you paying for the goods, so they will likely require that you pay for part or all of the goods upfront. So, you are starting in the hole outlaying cash. This is not captured on your profit and loss statement. While your money is being held by the vendor to make the goods, you may be able to work on making a sale to a retailer. If you sell to the end consumer, you have to wait until you have the goods in hand before you can sell them. When the goods or supplies are finally sent to you, then you can sell those goods to your customer (assuming you have a customer who has placed an order, otherwise it may take a while for you to make the sale of your goods once you receive them) and record it as a sale for the business. However, the cash that you have outlaid to manufacture and receive your inventory may be gone for quite some time before you make a sale.

Payment terms with your customers will dictate if you are going to get paid once you make the sale. Depending on their leverage (i.e., if your customer is a big organization like Walmart or Office Depot), your business’s size, and how desperate you are to make the sale, it may take them thirty, sixty, or even ninety days to pay you. Some customers may try to not pay you at all (then you have to go tracking them down, which means longer before you get paid, if you get paid). You also have to hope that your customers don’t go bankrupt themselves in the meantime (think Chrysler, Sharper Image, and Circuit City), or you will become a creditor, and it will take a long time for you to get paid even a fraction of what you are owed, if anything.

This timing cycle for using cash for working capital in your business isn’t just related to purchasing inventory. If you sell a service, like consulting services, your customer may not pay the bill for thirty days or more. However, if you hire a service provider (like an accountant or lawyer), he may require you, as a small business, to pay a retainer fee up front.

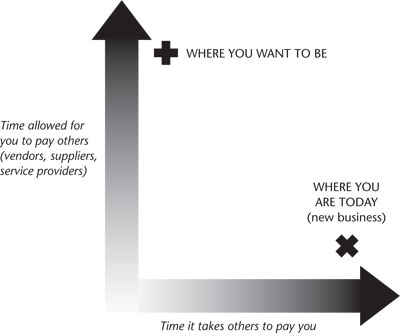

As a new and growing business, you need even more money to manage the business because every vendor and service provider wants you to pay them right away, but your customers will want to take as long as possible to pay you. The diagram below demonstrates where you are when you start out—where the “X” is on the diagram. Your customers are taking a long time to pay you, but your vendors, suppliers, and service providers are requiring you to pay right away (and sometimes in advance). As you become a large company (think Walmart or McDonald’s), you move to the plus sign, where you can dictate the terms because you are an important business with a lot of leverage. Then, you get more favorable terms of payment.

It’s not just working capital that you have to worry about. You may need to make large purchases of equipment, furniture, or other “property, plant, and equipment” for your business. This, too, impacts your business’s cash flow.

Having to worry about the cash flow in your business isn’t just relevant when you start a business. As you grow, you will need to purchase more and more inventory to meet growth demands, as well as more equipment to perform your services or run the business as it goes along. The more the business grows, for every dollar that your inventory, accounts receivable, prepaid expenses, and other current assets grow over and above the dollar growth in things you can put off paying for the same period of time (such as your accounts payable), that is another dollar that you have to finance in order for the business to grow. The same goes for every incremental dollar spent on property, plant, or equipment. This means that you either don’t get to take those incremental dollars home (i.e., they come out of your paycheck to help finance the growth of the business) or you need to find other financing, such as a loan, to pay for them. Ultimately, this means that you are not getting paid as regularly. As the owner, you are the last to get paid, and if the business is going to grow, it is going to require more cash to support it. This cash is coming out of your pocket in one way or another.

A Cash Flow Illustration

Let me give you an illustration of how this cash flow stuff might work for a new business. You start a business that sells widgets. You need to have the widgets produced overseas; so you find a vendor to produce them who requires a 50 percent down payment before shipping the widgets and then 50 percent upon shipment to you. These widgets take sixty days to produce and thirty days by boat to arrive at your warehouse (which is a reasonable timeframe, although many types of goods can take even longer to produce and be received from overseas manufacturers). Once the goods finally arrive at your place of business, you send them to a retailer, Widget World, who has agreed to sell your widgets in its store. Widget World is a big, important customer, so it requests thirty days after the receipt of goods to pay you. You don’t want to risk this important order, and therefore, you gladly agree. While you are waiting for Widget World to pay, you have more widgets produced from your vendors to fill future orders. Your business grows by 50 percent, so you need to order even more widgets than before. That sounds great, right?

It is great, because you are growing, but growth creates a challenge in managing your cash flow. You need to pay for the items before you sell them and with growth, that means that for every new order you place, you are paying for more and more items in advance.

Here is a timeline to show you what your widget business is in for:

So, if it takes you a few days to process your products and then ship them on to your customer, by the time you are able to record a sale on day ninety-five, you have had to put out cash (starting day one) on both the full amount of inventory for that order, plus half of your next order, which is even larger because you are growing. You don’t see a penny from the first sale (which happens officially when you ship the widgets to Widget World) until day 130. This is a typical cash flow issue that is not shown on your income statement and is what makes running the financial aspects of a business even more challenging.

Now, let’s go wild and assume you are very successful at selling the widgets and that you sell $20,000 worth of widgets in your first sale to Widget World. You are making a healthy 40 percent margin on that sale, so your direct cost of the widgets is 60 percent or $12,000. That means you have to spend $6,000 on day one and $6,000 on day sixty to get the widgets from your factory. And your next order is for $30,000 of widgets (an incredible 50 percent growth rate that will cost you $18,000 to produce), so you have to put out another 50 percent upfront payment (or $9,000) for the second order on day ninety. You start $21,000 in the hole just from having your first order produced and placing your second order, and you aren’t getting paid your $20,000 on the first order until day 130 from Widget World.

During that time, you will also have ongoing expenses for your business: rent, employees, utilities, insurance, postage, and so forth, will all be due. Once you get the money in from Widget World, you will have a very short window before your next payment is due on order two, and you will have to start thinking about order three. If order three is bigger (because you are growing) that incremental growth will need to be funded by the business, meaning less cash available to pay you.

So, even when you are doing well, managing cash creates an issue. If your cash profits from the business aren’t enough to fund the businesses growth, and you don’t take on financing in some form, you can’t grow the business. If you use the profits of the business, or take on financing to grow, you are either delaying taking home profits or you’re taking on liabilities. If you take on debt and the business has a blip along the way, then you can get into big trouble and be in violation of your bank agreements, which can cause them to put pressure on your business, charge you exorbitant fees, or even take drastic measures like seizing your assets.

The more asset-intensive your business is, the more susceptible you are to cash flow issues. However, in virtually every business there is a lag between your expenditures and the time you get paid. If you have to perform services, you still have to pay for rent, marketing, telephones, payroll, and other fees while you are working on a project and before you get paid by the client.

Why Timing (of Payments, That Is) Is Everything

Suzette Flemming, president of Flemming Business Services, knows the timing issue all too well. Her firm, which has provided accounting, bookkeeping, payroll, and tax services to businesses for more than fifteen years, couldn’t avoid cash flow issues in the recent economic downturn. As an accountant, Suzette knew what to do to enhance her business’s cash flow: require payment up front for all services.

However, she explains, “As the economy started to shift and my clients started having cash flow problems themselves, I let some of the pre-payments slide and would wait thirty or sixty days before knocking on clients’ doors and asking for payment. This has affected my ability to do payroll and to pay my other bills on time to avoid paying late fees.”

She also endured stress and worried that “squeaking too much” could cause her to lose clients but not “squeaking enough” could leave her without any money from the clients. Two of her clients have declared bankruptcy, putting her ability to collect anything for her services related to those clients in jeopardy.

If this sounds incredibly complicated to you, it is. Managing cash flow is one of the trickiest aspects to running a business, and even some of the biggest, most successful businesses in the world have gotten tripped up by mismanaging their cash flow, even though they did a good job managing every other aspect of their businesses.

If you don’t understand financials very well, take the time to really learn and understand this aspect of business, because it creates one of the biggest stumbling blocks out there. You need to put in the time in the financial arena if you are going to be in charge of your own company.

Cash flow and overall financial management also adds an increased layer of risk as you evaluate the potential upside of starting a business, because to grow the business and make more money, it is going to require you to give up more money, which may mean a longer payback period on your investment. As mentioned, in a normal job, you don’t have to pay anything up front to be employed. Other than investing in some work clothing, and maybe a briefcase and transportation to and from work, there aren’t a lot of upfront costs for having a job. To get a raise (growth in your current job), it doesn’t require you investing more money the way it does to grow your business.

Understanding financial accounting, including cash flow management, is required for you to keep score in your business. If those sound like things you don’t ever want to understand, then use this reality as part of your personal screening process related to starting a business.

EXERCISE 19

TARGET FOCUS—FINANCES:

Assessing How Cash Flows Impact Your Risk and Reward

- First, make sure that your financial model has a cash flow statement. If it doesn’t, enlist someone to assist you with creating one (they should help you, not do it all themselves, because you need to understand the impact of the cash flow on your business). I know you may cringe at this, but it is critical to understand how much money you need to run your business.

- Once you have your cash flow statement in place, do what is called a “sensitivity analysis” on the assumptions. This means, change the assumptions and see how that changes your cash flow in your model. Some assumptions you want to change include the following:

- Imagine that 10 percent of the people who owe you money delay paying you by a month. How does that affect your ability to operate your business?

- Can you pay your bills on time, pay yourself, and/or grow under this scenario?

- What if 20 percent or 30 percent of your customers delay paying you by a month?

- What if it takes sixty days or ninety days extra to get payment?

- What if some percentage of your customers (10 percent or 20 percent) never pay you?

Given that it is impossible to predict your financials with 100 percent accuracy, and that most entrepreneurs tend to be overly optimistic, take these sensitivities very seriously. How does this change in the potential financial reward of your business or the extra risk of having money tied up for longer periods in the business change the opportunity for you? Use your findings to further refine and review the risks side of your Entrepreneur Equation.