Vanilla Options Butterfly Spread Strategies

Butterfly spreads are utilized as a market-neutral strategy which combines bull and bear spreads giving the investor a fixed risk and a capped profit. These types of spreads pay the most profit if the market (underlying asset) does not move prior to the expiration of the option.

Key Points

• Combines bull and bear spreads

• Fixed risk with capped profits

• Pays most profit when underlying asset doesn’t move

• Use four options and three different strike prices

• Upper and lower strikes are the same distance from the two at-the-money strikes

• Same expiration date for all call or put options

• Same asset for all options

As mentioned above, the options with the higher and lower strike prices are equidistant from the at-the-money strikes, so if for example the at-the-money strikes are at $50, the higher strike would be $55 and the lower $45. Both strikes being $5 away from the at-the-money strike. Both calls or puts can used for a butterfly spread, so combining the options in various ways creates different types of butterfly spreads, with each type designed to profit from either minimal volatility or normal volatility.

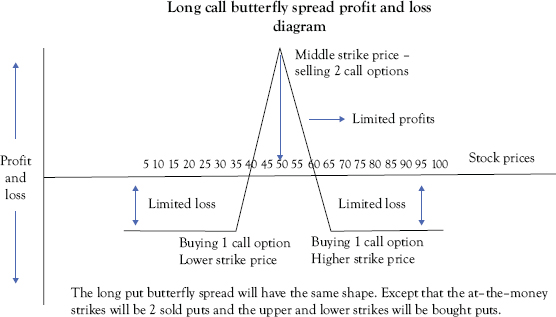

Using the numbers above, the profit-and-loss diagram, Figure 10.1 below, would look like this.

Figure 10.1 Long Call Butterfly Spread

Suppose an investor is buying stocks of company ABC, which is trading at $50 per share. The investor believes that prices will not move a lot over the next few months and there won’t be any major movements; the market will be nondirectional. So, the investor sells two at-the-money $50 call options and receives $6 as a premium. He also buys one lower strike price, in-the-money, call option at $45 and pays a premium of $6, and one higher strike price, out-of-the-money, call option at $55 and pays a premium of $1. Therefore, his net income to enter this position is (+ $6 − $6 − $1) × 100 = (−$100).

If the stock price remains at $50 at expiry:

Long $45 call has intrinsic value of $50 − $45 = $5 × 100 = $500

Both $50 calls allowed to expire worthless

$55 Call allowed to expire worthless

Net debit is initially −$100

Total profit is $500 − $100 = $400 (maximum profit)

If stock price lower than $45 then:

Maximum loss is sum of premiums paid and received = −$1

If the stock price is higher than $55, the profits from the two long calls will be neutralized by the losses on the short calls. See Table 10.1 below.

Table 10.1 Long Call Butterfly Profit and Loss Grid If at expiry stock price remains at $50

Stock Price at Expiration $50 | Sell x 2 $50 Calls | Buy $45 Call | Buy $55 call | Total Profit |

70 | ||||

65 | ||||

60 | ||||

55 | ||||

50 | Expire Worthless | Exercise I Value $5 | Expire Worthless | +$6 + $5 − $6 − $1 = $4 |

45 | 6 | (6) | (1) | (1) |

40 | 6 | (6) | (1) | (1) |

35 | 6 | (6) | (1) | (1) |

30 | 6 | (6) | (1) | (1) |

25 | 6 | (6) | (1) | (1) |

20 | 6 | (6) | (1) | (1) |

15 | 6 | (6) | (1) | (1) |

10 | 6 | (6) | (1) | (1) |

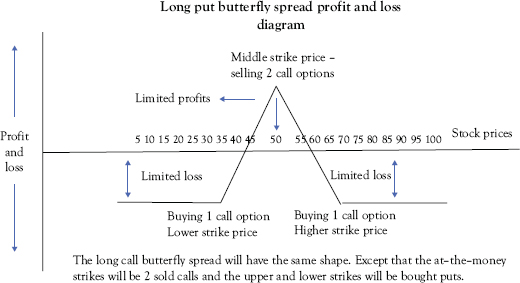

Now let’s look at the long put butterfly spread.

Long Put Butterfly Spread

The long put butterfly spread is set up this way:

Buy one out-of-the-money put option with a low strike price.

Sell two at-the-money put options

Buy one out-of-the-money put options with a higher strike price

The profit-and-loss diagram has the same shape as the long call butterfly spread profit-and-loss diagram. See Figure 10.2.

As with the long call butterfly spread, you would ideally want the two sold at-the-money puts to expire worthless, but instead of the higher strike expiring worthless, you would want the lower strike price to expire worthless, and the stock price to remain around the at-the-money strike price. In this example, the investor receives $8 for the two at-the-money $50 puts. The $55 put costs the investor $5 and the $45 put costs the investor $2. So the total cost to enter the position is + $8 − $5 − $2 × 100 = $100 credit.

Figure 10.2 Long Put Butterfly Spread

If the stock price remains at $50 at expiry:

Long $55 put has an intrinsic value of $50 − $55 = $5 × 100 = $500

Both $50 puts allowed to expire worthless

$45 put allowed to expire worthless

Net credit is initially $100

Total profit is $500 + $100 = $600 (maximum profit) See Table 10.2 below.

Table 10.2 Long Put Butterfly Spread

If stock price remains around $50 at expiry

Stock Price at Expiration $50 | Sell x 2 $50 Puts | Buy $45 Put | Buy $55 Put | Total Profit |

70 | 8 | (2) | (5) | 1 |

65 | 8 | (2) | (5) | 1 |

60 | 8 | (2) | (5) | 1 |

55 | 8 | (2) | (5) | 1 |

50 | Expire Worthless | Expire Worthless | Exercise Value $5 | + $8 + $5 − $5 − $2 = $6 |

45 | 8 | (2) | (5) | 1 |

40 | 8 | (2) | (5) | 1 |

35 | 8 | (2) | (5) | 1 |

30 | 8 | (2) | (5) | 1 |

25 | 8 | (2) | (5) | 1 |

If stock price higher than $55 then:

Maximum loss is sum of premiums paid and received = +$1

If the stock price is lower than $45, the losses from the two long puts will be neutralized by the profits on the short puts.

Other types of butterfly spreads are:

Short Call Butterfly Spread

Using this strategy, investors would:

• Sell one call option with a lower strike price

• Buy two call options with a middle strike price

• Sell one call with a higher strike price

This strategy is normally created for a net credit, and both the potential profit and maximum risk are limited. The maximum profit is equal to the net premium received, and it is realized if the stock price is above the higher strike price or below the lower strike price at expiration. The maximum risk equals the distance between the strike prices less the net premium received and is acquired if the stock price is equal to the strike price of the short calls on the expiration date.

Short Put Butterfly Spread

The short put butterfly spread is created when investors:

• Sell one put with a lower strike price

• Buy two puts with a middle strike price

• Sell one put with a higher strike price

Investors maximize their profits when the underlying price is more than the higher strike price or less than the lower strike price on expiration date.

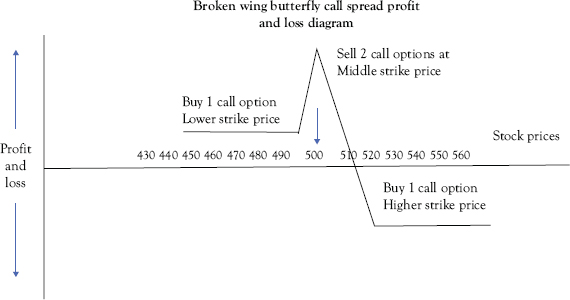

As we have just learned with a regular butterfly, a debit situation is created when you sell two options and buy two options on each side that are equal in distance. See Image 10.1 Profit-and-loss diagram.

However, with a broken wing butterfly, the investor should ensure that the debit spread portion of the transaction is narrower than the credit spread portion of the trade, so that the investor collects a credit upfront and has no risk to the OTM side.

A broken wing butterfly is a long butterfly spread with long strikes that aren’t equidistant from the short strike. This leads to having greater risk than the other, which makes the trade slightly more directional than a standard long butterfly spread.

This net credit strategy is normally used to increase the probability of profit (POP) by moving the transaction toward a credit. The main objective is not to suffer any cost upfront. So, by taking a credit on entry, instead of a debit, the risk of losing money is eliminated if the entire spread expires OTM. See Figure 10.3 below.

Figure 10.3 Long Call Broken Wing Butterfly Strategy

Transaction Details for ABC Stock

Buy 1 Dec 495 call @ 15.25

Sell 2 Dec 500 calls @ 11.50

Buy 1 Dec 500 call @ 5.35

Net Credit: $202

In a broken wing butterfly call, the maximum loss is limited to the difference between the width of the wider and narrower call spreads minus the credit received when the transaction was initiated.

In the aforementioned example, the 500 and 510 legs of the bear call spread are $10 apart; the legs of the 495 and 500 bull call spread are $5 apart.

There is a $10 – $5 = $5 difference between the width of the two spreads.

The butterfly was created for a credit of $11.50 × 2 – $15.25 – $5.35 = $2.40; hence, we have a total maximum potential loss of:

Max loss = 100 × (5 – 2.40) = $260

This maximum loss of $260 will happen if ABC stock rallies above $510 at expiration date.

There is no risk on the downside in this broken wing butterfly; the trade will make a net gain of $240, if at expiry, ABC stock price is below $495.

On the other hand, if the butterfly was created for a debit, the maximum loss would be

difference in width of the spreads + net debit.

Maximum Gain

The maximum gain on a broken wing butterfly happens when the stock closes at the strike price ($500) of the short calls at expiration.

In the above case, the short calls are worthless as well as the long out-the-money call ($510).

In this ABC broken wing butterfly, the butterfly will make a maximum gain if at expiry ABC closes at $500. The maximum gain in this scenario would be:

Strike price short calls – Strike price long in-the-money call + Net credit received

Max gain = 100 × ($5 + $2.40) = $740.

As we can see from the profit-and-loss diagram, broken wing butterflies have a tent-shaped payoff diagram with the potential for very large profits around the short strike of the calls. It is crucial to bear in mind that it is improbable that the trade would actually attain the maximum profit. Experienced investors usually close the position before expiry as their aim is to achieve a 20 to 25 percent return on capital.

Unlike a normal butterfly, the broken wing butterfly delivers income if a stock goes one way and capital gains if it goes the other way. That’s the possibility you have with broken wing butterflies.

A broken wing butterfly is sometimes referred to as a “skip-strike” butterfly. You can see why from the profit-and-loss diagram. If you remember the regular butterfly has the bought options an equal distance from the sold options, however, a broken wing butterfly will skip a strike on one side of the trade. This has the effect of reducing the cost and in many cases will actually result in a net credit which means you can use it as an income trade also.